AXP - American Express: Undervalued And Misjudged In The Banking Sector Comparison

2024-01-16 04:36:45 ET

Summary

- American Express, often grouped with Visa and Mastercard, is undervalued in the market due to the inaccurate comparisons with traditional banks due to its status as a bank holding company.

- The bank holding company status actually benefits American Express from diversified revenue streams, lower borrowing costs, and access to federal reserve funding.

- American Express reported robust results in its financial metrics like network volume, cards-in-force, and strong free cash flow compared to Visa and Mastercard.

- Despite these advantages and strong performance, American Express faces risks including changes in partner policies and increasing delinquencies, which investors should consider when evaluating its long-term potential.

American Express (AXP) is often compared with Visa (V) and Mastercard (MA). However, American Express' valuation is usually at half of what Visa and Mastercard are valued at due to misconception of American Express' status as a bank holding company. I believe that this misconception provides a fantastic opportunity for American express to reward investors in the long term.

Introduction - History of American Express

American Express started in 1850 as an express mail business. It is growing rapidly by consolidating other smaller companies. The pivotal moment came in 1958 when American Express launched its signature charge card making its entry into the credit card business. From there, American Express has evolved into one of the 3 oligopolies along with Visa and Mastercard dominating the global credit and network services sector. American Express became publicly traded company in 1977 while Visa and Mastercard went public in 2006 and 2008.

As of January 13, 2024, American Express' market capitalization is 134 billion with 1.3% dividend yield, posing as one of the well-known blue chip investments.

Misconception

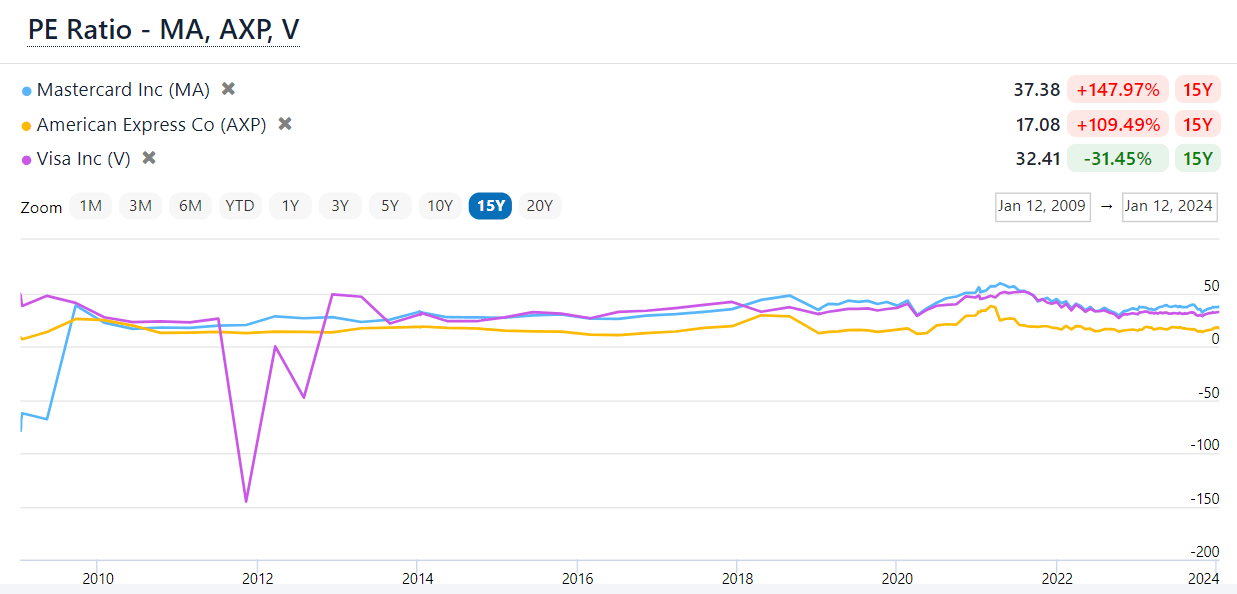

American Express is often compared with Visa and Mastercard. However, American Express' valuation is usually at half of what Visa and Mastercard are valued at. For example, most recently, American Express is PE ratio is 17.08 while Visa and Mastercard's PE ratios are at 32.4 and 37.38 respectively. This situation has persisted since approximately 2013 as shown on the chart below. In 2006 when Mastercard went public, Mastercard was actually trading at the same PE ratio as American Express, and even lower than American Express from time to time. Unfortunately, American Express' valuation diverged slowly from 2008 onward since that American Express's application to become a bank holding company was approved.

/www.financecharts.com/compare/MA,AXP,V/value/pe-ratio

{kind=link}

Investors interestingly discount American Express's value significantly by the fact that American Express won the approval to become a bank holding company in addition to its staple payment processing business. However, I think that not only American Express' value shouldn't be discounted, American Express' value should actually be increased because of its status as a bank holding company.

The main reasons for this rationale are:

Diversification

The lending and customer deposit business helps diversify American Express' business model.

As you can see from the PE ratio chart above, Visa and Mastercard's valuation are more volatile compared to American Express thanks to its vast network of high quality customers. When interest rate is rising and the economy is naturally going into recession, Visa and Mastercard may be impacted by retracted consumer spending. However, not only American Express' customers with higher income are more immune to the impact of recession, American Express can benefit from the rising interest rate through its banking business. In addition, while new payment processing companies such as OVO, Square, Stripe, Nuvei, as well as burgeoning blockchain companies may disrupt Visa and Mastercard's market share relatively easily, it is significantly more difficult for any company to disrupt American Express' network of high quality loyal customers that use American Express cards for its rewards and prestige.

Lowering Borrowing Costs

The banking business helps lower borrowing costs for its core payment processing business. American Express has the luxury of holding a whopping $124 billion in customer deposits with a relatively low interest rate on its balance sheet as of September 30, 2023. With the requirement of only holding a minimum of 7% in reserve for the effective period from Oct 1, 2023 to Sept 30, 2024, American Express has about $115.3 billion to finance its card member loans and receivables that it earns revenue and fees on providing an overall superior product to its card members. However, Visa and Mastercard will need to issue long-term debt at a higher interest rate to finance its business.

Access to Government Funding

As a banking business, American Express has access to Federal Reserve funding in case of an emergency same as the other banks while Visa and Mastercard don't have this luxury of protection. For example, just recently amid the Silicon Valley Bank fiasco, Federal Reserve provided $300 billion in emergency lending that American Express National Bank can have access to if needed.

Virtuous Network Effect

The lending and customer deposit business creates virtuous network effect as a significant competitive advantage to help retain its high-quality customer base. Rather than simply processing a payment, American Express works with its customers directly to provide various solutions and financial products that these customers can't receive from Visa or Mastercard.

American Express KPIs

American Express regularly reports a variety of metrics on its financial reports. Given the complexity of the various metrics. I will briefly discuss how several key metrics from its Q3 2023 10-Q present a solid picture of American Express' financial performance.

Network Volume: this is the volume of total transactions going through American Express' network. On an annual basis in 2023, American Express processes about $1.6 trillion in transactions, which is much smaller compared to Visa ($12 trillion) and Mastercard ($8 trillion). However, the revenue ($14 billion in Q3 2023) American Express generates on "just" $1.6 trillion transactions is fairly close to what Visa ($11.7 billion in Q3 2023) and Mastercard ($6.5 billion in Q3 2023) can generate, demonstrating the value of American Express' high-quality customers.

For the 3 months ended September 30, 2023, American Express' network volume grew by 7% compared to the same quarter in prior year, indicating that American Express is growing at a faster pace than inflation. In comparison, Visa's network volume grew by approximately 6% for the same period.

Cards-In-Force: this is the number of cards American Express issued both on its own and through network partners such as a bank or airline including supplementary card that the primary card member applies for their family. This KPI demonstrates the base where American Express depends on to generate discount revenue, card fees and interest income. For the quarter ended September 30, 2023, American Express' total number of cards-in-force increased by 5% compared to the same quarter in the prior year. When compared to the 7% increase in network volume discussed above, it appears that American Express not only is adding new cardholders to enlarge its revenue base, its existing cardholders are organically spending more.

Average Fee Per Card: this metric increased from $82 to $93 in the quarter ended September 30, 2023, indicating that on average its cardholders are moving toward more premium cards as well as retaining cards beyond the 1st year (sometimes the credit card fee for the 1st year is waived through promotion).

Other Notable Observations from Q3 2023 10-Q

Non-interest revenue increased by 11% over the same quarter in prior year to $4.68 billion, primarily driven by a whopping 20% increase in net card fees from premium card portfolio. It appears that American Express' high quality customers are very loyal. Once they use American Express products, they are likely to move up toward more premium cards (I am a good example myself).

T&E Spend (travel and entertainment spending, which is a major expense category for American Express cardholders) increased by 13% over the same quarter in prior year. While the economy is likely sliding into a recession, it appears that American Express' customers are not too affected and in turn are spending more on travel and entertainment.

While other sectors are struggling such as retail and tech from cutting dividends and laying off employees, American Express along with Visa and Mastercard seems to do fairly well increasing its dividend by 15% and 20% in the past two years. In addition to the incredible dividend growth rate, American Express has repurchased 7.9 million shares just in Q3 2023, representing approximately 1% of its total common shares outstanding.

As a result of its banking business amid rising interest rate, American Express also saw an increase of 20% in Customer Deposits year over year, helping to grow its card member loans and other investments portfolios.

Valuation

As discussed previously, the market appears to have discounted American Express significantly from a PE ratio standpoint due to its banking business.

On Seeking Alpha, the Quant Rating for American Express is a "Hold". When analyzed closely, one may find that American Express' valuation is benchmarked with the banking sector's PE ratio medium of about 10.24. As a result, American Express gets a "D" on sector relative grade. The score looks even worse for American Express on other metrics such as price/book ratio when compared to actual banks. However, if benchmarked with Visa/Mastercard, American Express should earn a "Buy" or "Strong Buy" rating.

seekingalpha.com/symbol/AXP/valuation/metrics

In addition to PE ratio, American Express earned $10.7 free cash flow per share in the quarter ended September 30, 2023 while Mastercard only earned $3.19 per share and Visa only earned $4.43 per share in the same quarter.

Overall, I believe that American Express is significantly undervalued by being benchmarked to the wrong sector.

Risk Factors

Although American Express has delivered another strong quarter in Q3 2023, there are several risk factors that investors should be aware of.

Part of American Express' revenue is through cards issued by its network partners such as airlines. American Express and Delta have been partners for many years. Recently, Delta left a sour taste in the mouths of its Delta American Express card members who were furious this week after the airline started restricting access to its premium Sky Club airport lounges effective Jan 1, 2024 and making it harder for them to earn points. This change in Delta's policy will undoubtedly affect American Express' revenue to some extent in 2024.

In addition, although still not significantly affecting American Express' net profit, delinquency rate is increasing. Total provision for credit losses increased by a whopping 58% from $778 million in Q3 2022 to $1,233 million in Q3 2023, primarily due to net write-offs of card member receivables. It indicates that a portion of its customers are experiencing financial difficulty.

In addition, last week, debit card users obtained class certification that allow them to sue American Express. Debit card users in some states accused American Express of indirectly driving up the cost of rival cards through rules that allegedly limited competition and hurt consumers without AMEX cards.

Conclusion

Despite being part of an oligopoly alongside Visa and Mastercard, American Express remains undervalued possibly due to misconceptions about its banking business. This banking business not only shouldn't discount American Express' value, but it should increase its value. This status provides American Express with advantages like diversified revenue streams, lower borrowing costs, access to federal reserve funding, and resilience to economic fluctuations. Its robust and consistent financial performance shows its potential as a valuable investment. However, investors should remain aware of risks such as partnership dynamics and increasing delinquencies, which could impact future performance.

For further details see:

American Express: Undervalued And Misjudged In The Banking Sector Comparison