VIG - American Express Vs. S&P 500

2023-09-01 14:22:14 ET

Summary

- American Express Company is a large financial corporation known for its iconic products, but its stock performance is less than impressive, given the elevated volatility.

- The company has growth opportunities in younger customer segments and international markets.

- American Express' commitment to premium offerings and partnerships showcases its competitive edge, but its high volatility and competition raise concerns.

Introduction

The American Express Company ( AXP ) isn't just one of the largest financial corporations in the world with its $117 billion market cap, but it's also a company that has made a name for itself, thanks to its iconic products.

A website actually kept track of every (major) mention of American Express and its famous black card in pop culture. That's no surprise, as the Centurion Card looks very cool, and you need to spend at least a quarter of a million with other Amex cards to be able to apply for this card.

American Express

When it comes to impressing people, a black credit card in the wallet goes well with a Swiss watch on one's wrist.

Having said that, the American Express stock performance is less impressive. It's not bad. It's just less than perfect.

In this article, I'll walk you through my thoughts as we assess the pros and cons of buying shares in this financial giant. While I believe in the company's ability to generate consistent long-term shareholder value through organic growth and secular tailwinds, the risk/reward isn't great, as a common dividend growth exchange-traded fund, or ETF, may be the better place to put one's money for similar returns with lower risks.

So, let's dive into the details!

Not Bad, Just Not That Great

American Express is known as a global integrated payments company offering a wide range of products and services to consumers, small businesses, mid-sized companies, and large corporations worldwide.

The company is a leader in credit and charge card issuance, and its cards are accepted by most merchants around the globe.

AXP serves diverse customer groups through various channels, including mobile and online applications, affiliate marketing, and more.

American Express

On top of issuing cards, the company has a well-integrated payments platform that allows it to analyze customer spending, underwrite risk, reduce fraud, and offer targeted marketing and information services to merchants and cardholders.

The company maintains direct relationships with both Card Members and merchants, creating a closed-loop system that distinguishes the company from traditional bankcard networks.

American Express

Speaking of competition and differentiation, AXP aims to expand its leadership in the premium consumer space, strengthen its position in commercial payments, grow its global network, and leverage its unique global presence.

They also have an Environmental, Social, and Governance ("ESG") strategy focusing on diversity, climate solutions, and building financial confidence.

Having said that, AXP investors have been in a good spot - at least when it comes to the returns.

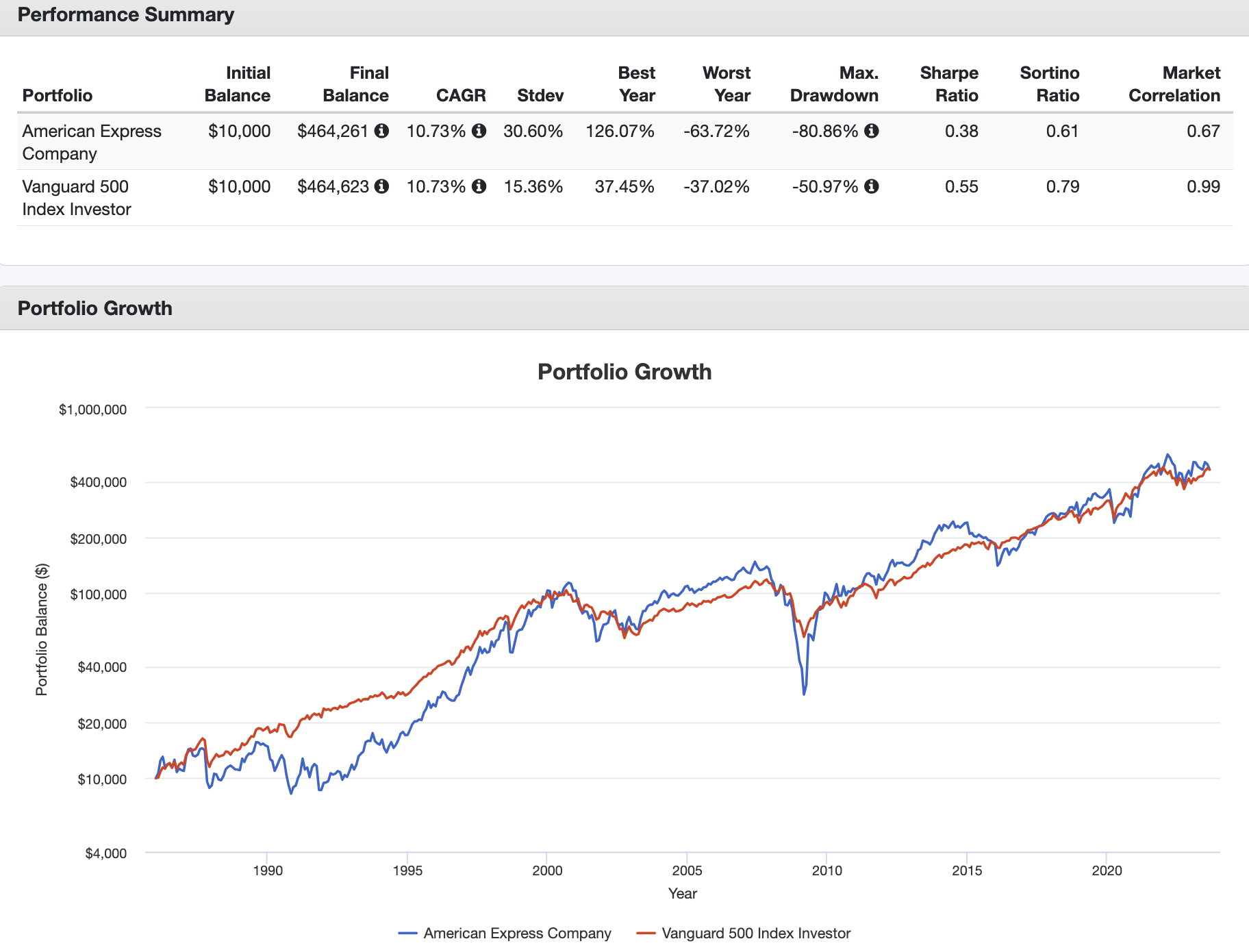

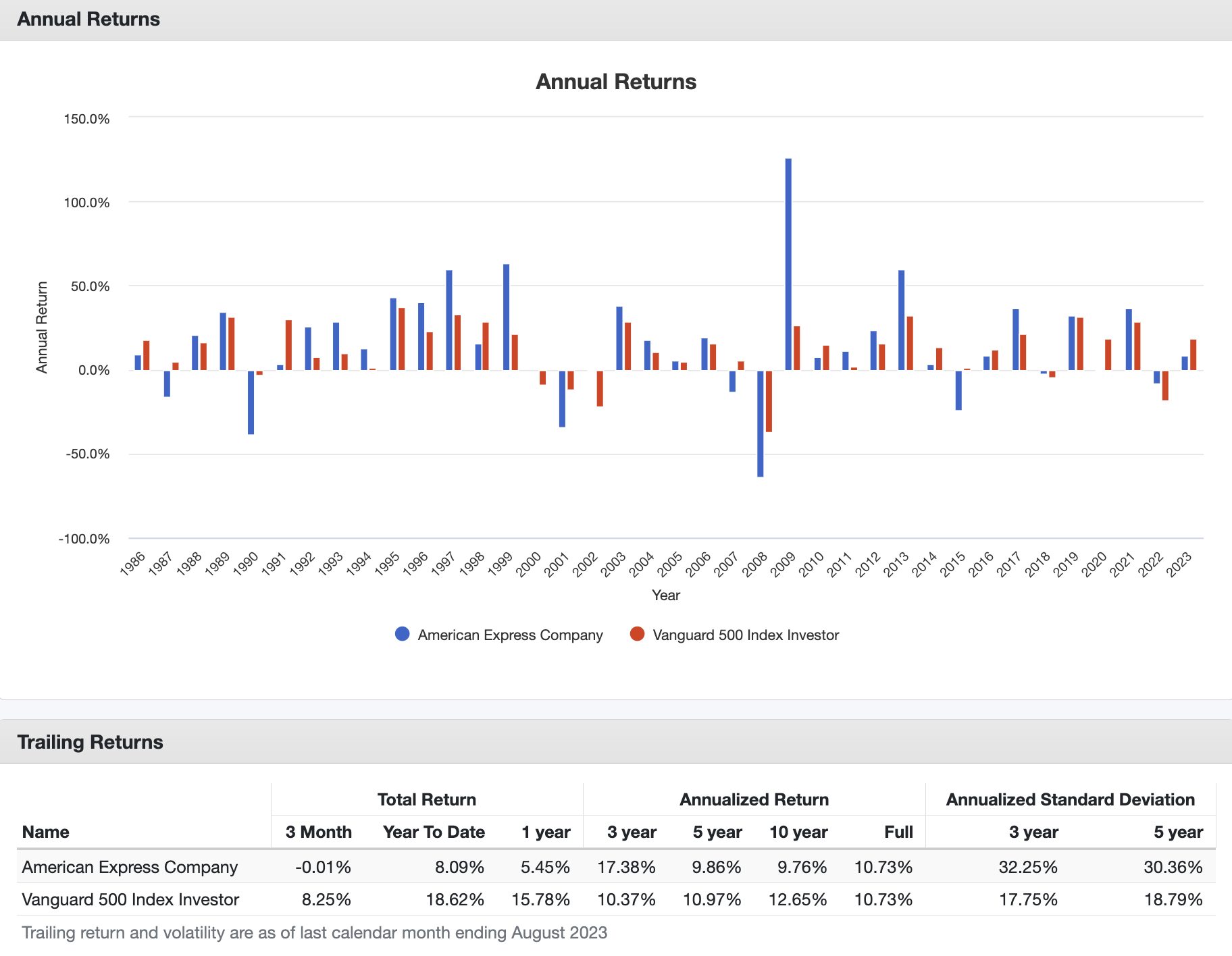

Going back to 1986, AXP shares have returned 10.73% per year, turning a $10,000 investment into roughly $464 thousand. Interestingly enough, the S&P 500 also returned 10.73% per year during this period.

{kind=link}

So far, so good.

The problem I see is the valuation. While investors didn't generate alpha (they didn't beat the market), they were subject to a 30.6% standard deviation, which is very high and a result of the company's exposure to a very cyclical industry.

Unfortunately, these developments have gotten a bit worse.

Over the past ten years, AXP shares have returned 9.8% per year. That's not bad. However, the S&P 500 (SP500) returned 12.7% per year. The standard deviation was still 30.4%.

{kind=link}

When looking at the ratio between the AXP total return and the S&P 500 total return since the mid-1990s, AXP hasn't outperformed the market since the early 2000s.

Needless to say, I would not have written this article if AXP were a bad stock.

It's not a bad company. It's just not ideal in a market where buying an index fund is so easy and profitable (compared to stock picking).

After all, the SPDR® S&P 500 ETF Trust (SPY) also has a similar dividend yield. The Vanguard Dividend Appreciation Index Fund ETF Shares ( VIG ) has a 1.9% and similar dividend growth, but more on that later in this article.

Volatility also has its benefits.

Weakness can cause opportunities, especially when dealing with a stock that tends to bounce back well beyond prior highs.

American Express is such a stock.

What Makes American Express Attractive

American Express may have a less favorable risk/reward profile - at least historically speaking - but it's far from dead money.

The company has plenty of growth opportunities left.

For example, during this year's Bernstein Strategic Decisions Conference, the company made clear that it has seen significant growth in younger customers like millennials and Gen Z, with millennials spending up 28% year-on-year.

The shift in approach involved moving away from fee-free products for younger customers and instead focusing on providing value through premium offerings.

So far, the company's success with products like the Platinum Card, Green Card, and co-brand cards has resonated with these customers.

It is also looking to expand internationally.

In 2022, the company generated 78% of its revenue in the United States. It's the biggest consumer market in the world and its home base, but there's faster growth in certain markets abroad.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| United States | ||||

| 33,103 | ||||

| 78.1 % | ||||

| 41,396 | ||||

| 78.3 % | ||||

| EMEA | ||||

| 3,643 | ||||

| 8.6 % | ||||

| 4,871 | ||||

| 9.2 % | ||||

| APAC | ||||

| 3,418 | ||||

| 8.1 % | ||||

| 3,835 | ||||

| 7.3 % | ||||

| Latin America, Canada, and the Caribbean | ||||

| 2,238 | ||||

| 5.3 % | ||||

| 2,917 | ||||

| 5.5 % | ||||

| Other Unallocated | ||||

| -22 | ||||

| -0.1 % | ||||

| -157 | ||||

| -0.3 % |

In the case of AXP, the focus is on key markets such as the U.K., Japan, Canada, Mexico, and Australia, where AXP's brand and offerings resonate well.

Except for Mexico, these markets aren't emerging markets. However, they have a strong consumer base and are relatively easy to penetrate for American Express.

The international approach has been restructured to improve efficiency and agility, bringing together international small business and consumer operations using both proprietary and partner channels.

It goes without saying that the company is not alone in its market, which is highly competitive.

Hence, it helps that the company has great name recognition and successful services that have made it the leader in areas like fraud prevention.

Furthermore, during its Q2 2023 earnings call , the company emphasized its competitiveness a bit more.

The company's model primarily revolves around fee-based premium products, driving a spend-centric economics framework and generating a growing stream of subscription-like revenues.

This approach prioritizes spending over lending, which sets them apart from many players in the industry.

They foster long-term relationships through a unique membership model, attracting and growing with customers over time.

American Express

Partnerships play a pivotal role, with the announcement of a 10-year extension of the company's partnership with Hilton.

Unfortunately, the company's growth is highly cyclical.

While net income has grown by 59% over the past ten years, it has been through two major down cycles. The same goes for free cash flow.

This brings me to the next question.

How's AXP Doing In this Environment?

AXP shares peaked in early 2022. They are now 18% below their all-time high and 22% above their 52-week low. Shares are up 7.7% year-to-date.

FINVIZ

That's not a poor performance, especially not considering the poor state of the consumer.

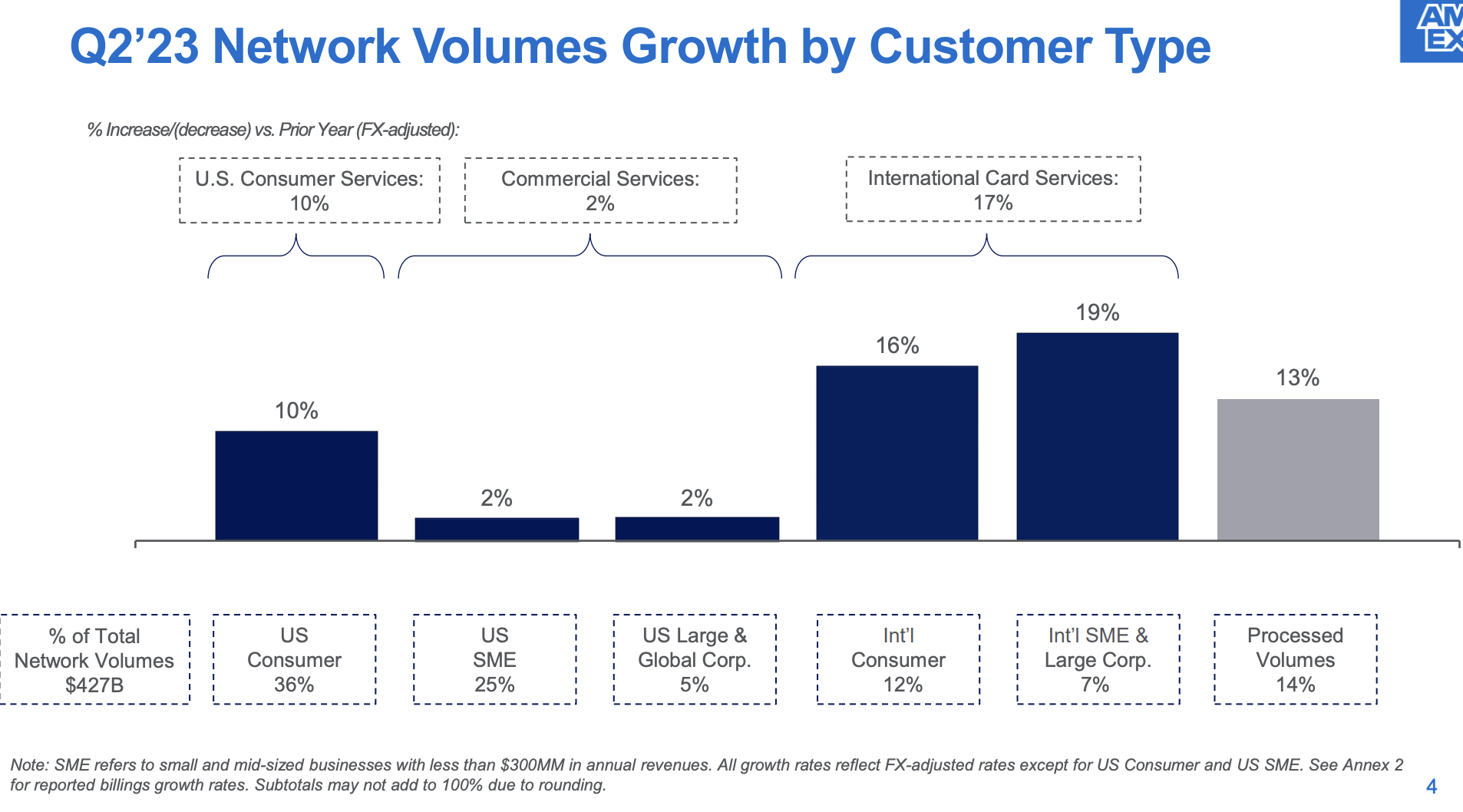

In the second quarter, Card Member spending reached an all-time high, both in the U.S. and internationally, offsetting some softness in U.S. small business spending.

{kind=link}

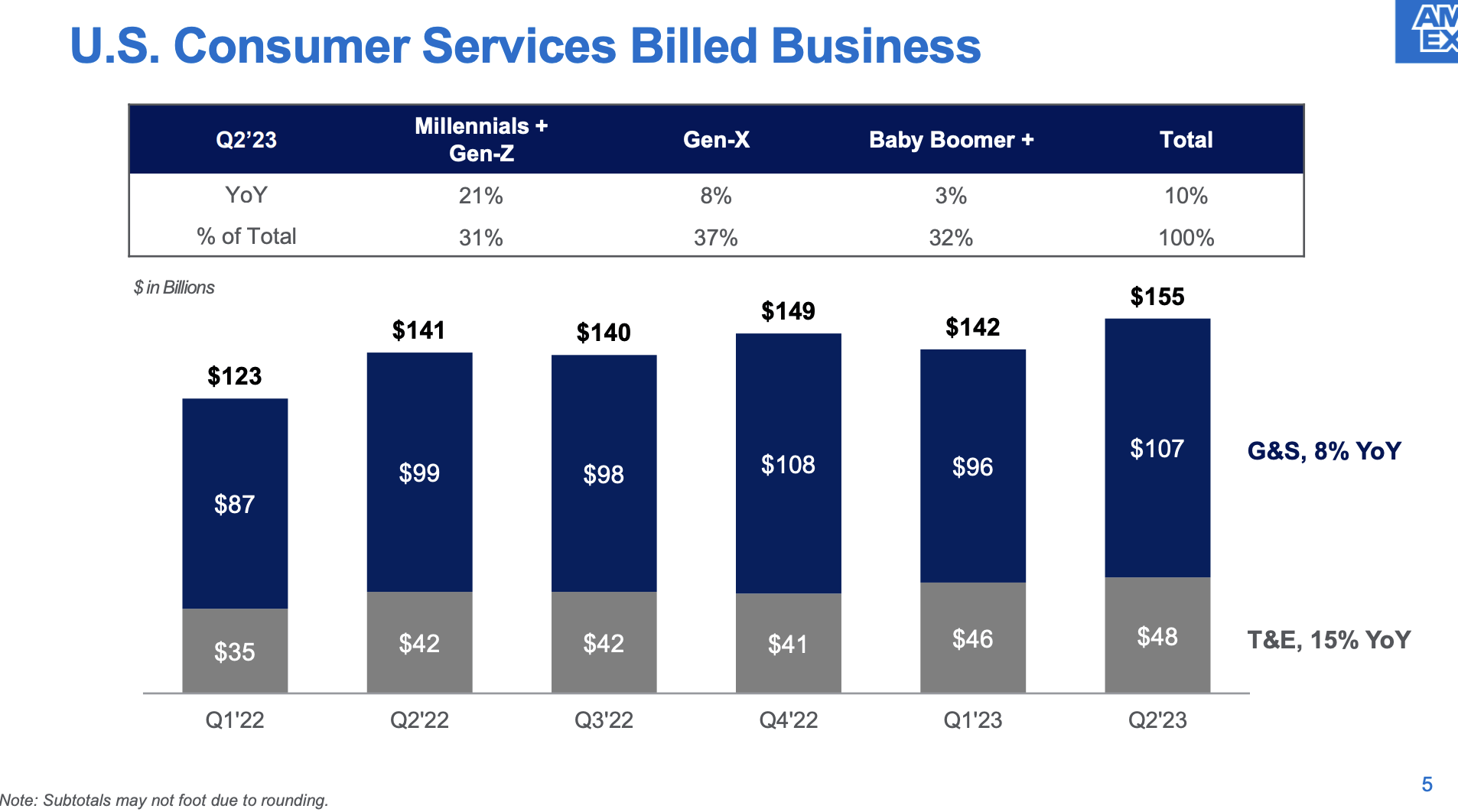

- Millennials and Gen Z consumers are the fastest-growing segment of its customer base, with a notable 21% increase in U.S. billings in the quarter.

- The International Card business, previously the company's fastest-growing segment, regained that status.

- Travel and Entertainment spending continued to surge, remaining strong across customer categories and geographies.

{kind=link}

The quarter also saw record restaurant reservations through the company's Resy platform, and consumer travel bookings reached pre-pandemic levels.

American Express also reported robust demand for premium products, with a significant proportion of new accounts acquired on fee-based products, emphasizing quality and revenue potential.

Total network volumes and billed business were up 9% and 8% year-over-year, respectively, on an FX-adjusted basis.

Furthermore, only 8% of U.S. Card Member loans and receivables were from customers with a FICO score of less than 660.

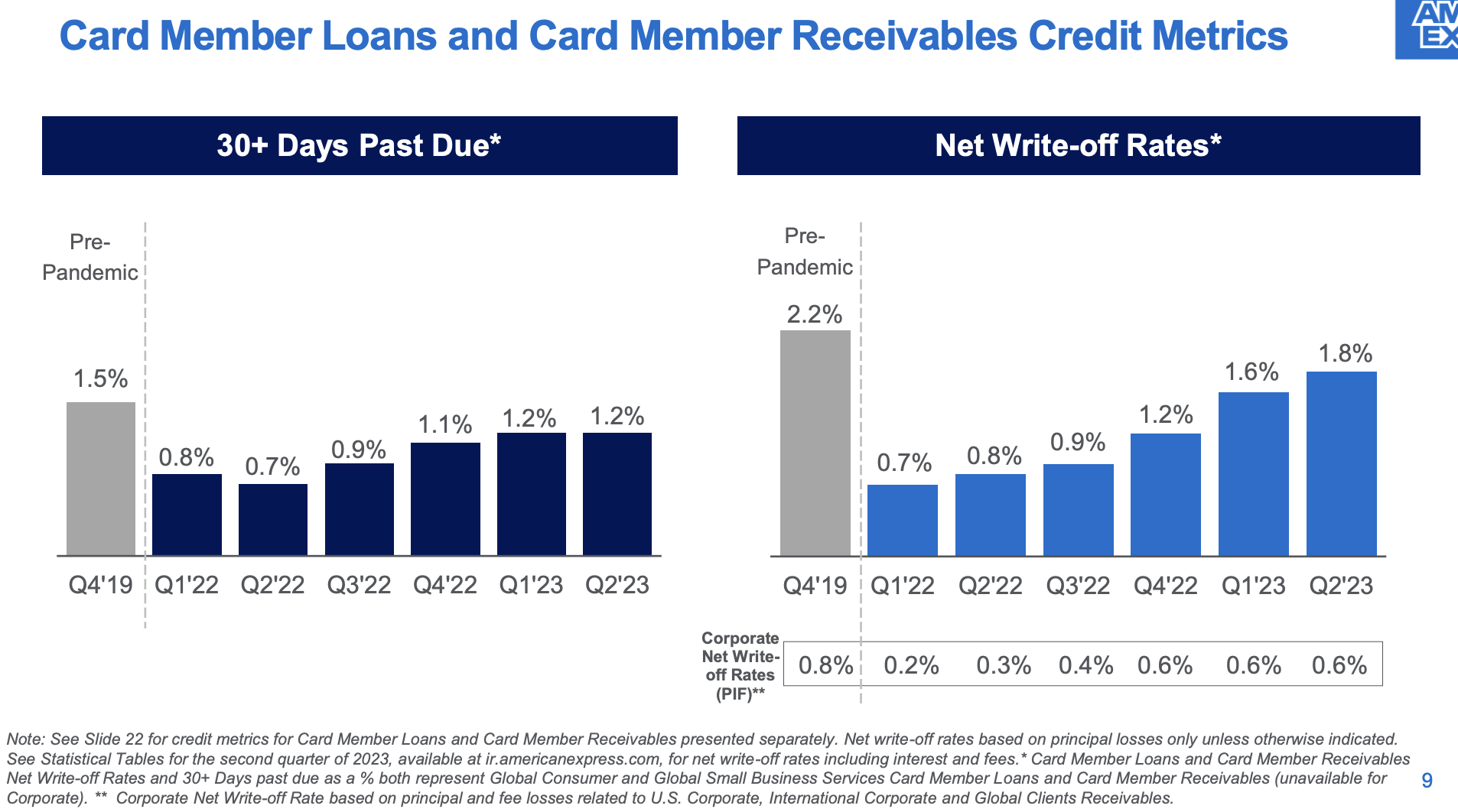

Credit performance remained strong, with write-off and delinquency rates below pre-pandemic levels.

{kind=link}

This is also reflected in the company's provisions.

Provision expenses rose to $1.2 billion in the second quarter, primarily driven by loan balance growth.

Reserves stood at $4.7 billion, representing 2.6% of total loans and Card Member receivables.

It is expected that the reserve rate will continue to increase slightly in 2023.

I agree with that assessment, as excess savings in the economy are quickly fading - compared to pre-pandemic levels.

Wells Fargo

So, what about the dividend?

The AXP Dividend

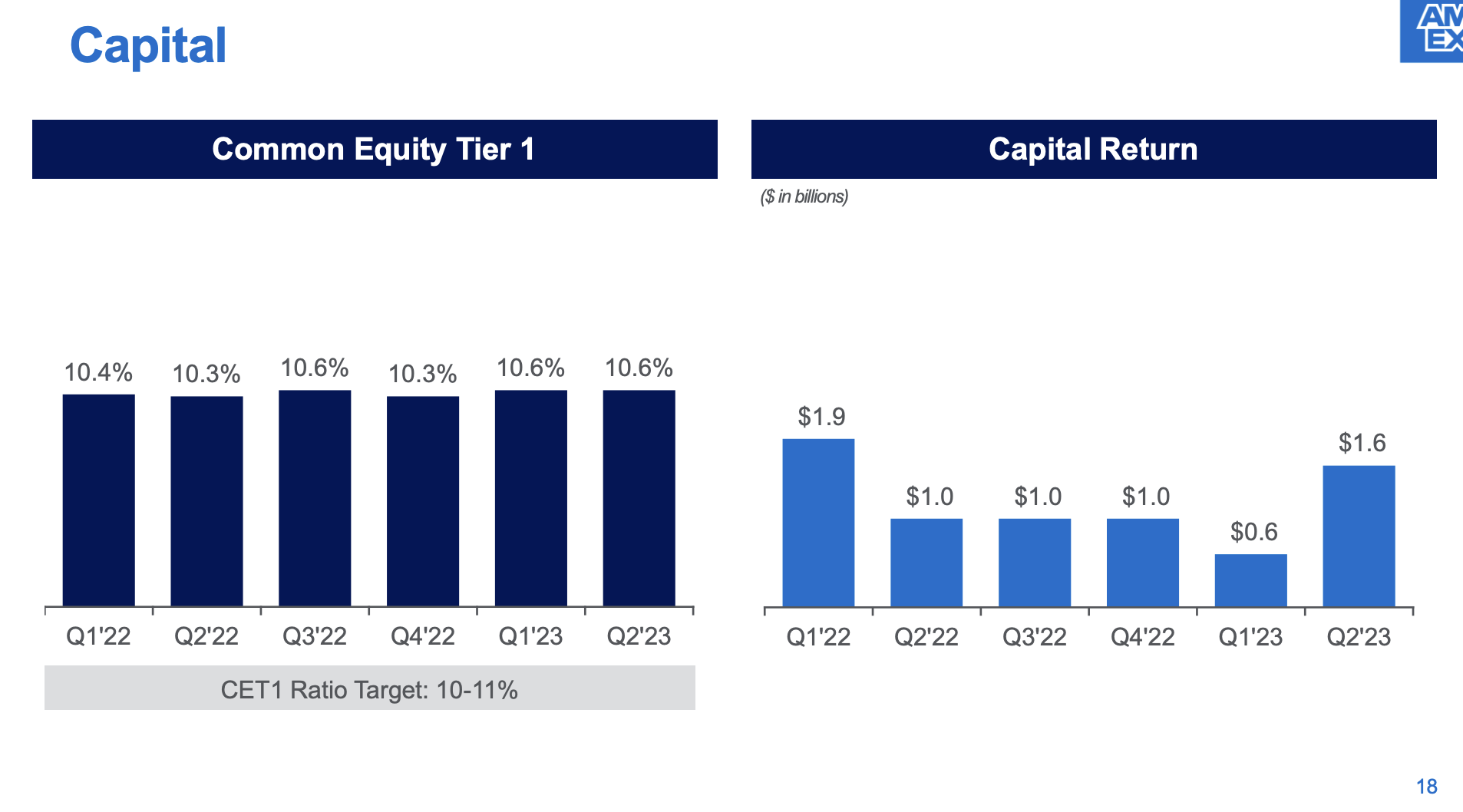

In the second quarter, American Express returned $1.6 billion to shareholders through stock purchases and dividends, which was possible because of strong free cash flow and a strong balance sheet .

The CET1 ratio stood at 10.6%, within the target range of 10% to 11%.

{kind=link}

Hence, the company planned to continue returning excess capital to shareholders while supporting balance sheet growth, with no significant changes expected in the near term.

Currently, AXP yields 1.5%, which isn't something to write home about. It has a 23% payout ratio, which is very healthy, and a 9.9% 5-year dividend CAGR, which isn't bad! As I already briefly mentioned, it has the same yield as the S&P 500 and a similar growth rate as the Vanguard Dividend Growth ETF, which yields 1.9%.

AXP did not cut its dividend during the Great Financial Crisis.

The only reason why it is yielding just 1.5% is the fact that capital gains have offset dividend growth in the past, which is good for existing investors. It's less great for income-focused investors looking for a position in AXP.

Moreover, as I already briefly mentioned, buybacks are a big part of (indirect) shareholder distributions.

Over the past ten years, the company has bought back 31% of its shares.

These shareholder distribution numbers are great, and unless we enter a major recession, I expect dividend growth to continue at a solid pace - backed by buybacks.

Valuation

AXP's valuation is fair. The company is trading at 4.4x its tangible book, which is close to the longer-term median.

The same applies to the price/earnings ratio, which is at 14.3x NTM earnings.

The current consensus price target is $181, which is 13% above the current price.

Given that the economy is still supporting elevated credit card rates and spending (despite serious cracks in consumer spending), I believe this valuation is warranted.

However, I wouldn't be a buyer at these levels. AXP has a very volatile history and is a better buy on significant weakness.

In light of sticky inflation and the fact that the Fed may have to keep rates elevated, we could be in for a harder landing.

A harder landing could provide us with attractive buying opportunities.

Outside of steep corrections, I believe that investors are better off buying index funds like the S&P 500 or other dividend growth stocks that we frequently discuss on this website.

I dislike the risk/reward of holding AXP shares on a long-term basis. While the company has growth potential, competition is fierce, and elevated volatility doesn't make it a must-own stock, especially in light of the strong performance of index funds and low-cost dividend growth ETFs.

On a side note, I will present a few appealing ETFs that I like in the weeks ahead, so stay tuned for that!

Takeaway

American Express may have its allure with its iconic black card and strong brand recognition, but when it comes to stock performance, it's a mixed bag.

While it has delivered respectable returns over the years, its high volatility and competition raise concerns.

The company is not to be underestimated, though, with growth opportunities in younger customer segments and international markets.

AXP's commitment to premium offerings and partnerships, like the one with Hilton, showcases its competitive edge.

However, it operates in a cyclical industry, making it susceptible to economic fluctuations.

From an investment perspective, American Express Company's current valuation seems fair, but it's not a buy at these levels. The potential for a more challenging economic environment suggests waiting for better entry points.

In the meantime, investors may find more stability and potential in index funds or low-cost dividend growth ETFs.

For further details see:

American Express Vs. S&P 500