AFG - American Financial Group May Not Produce Desirable Returns

2023-03-18 09:59:21 ET

Summary

- Although American Financial's stock has produced huge returns historically, in the upcoming years, returns might lag substantially due to the relatively higher valuation.

- Consider that the significant rise in investment income has resulted from a one-time gain on equity earnings.

- The stock reflects the actual value of the business, and from this price point, holding the stock might not produce desirable returns.

American Financial Group (AFG) provides specialty property and casualty insurance to commercial customers. With a long operating history, the company has expanded its business reach through strategic acquisitions and organic developments; as a result, over time, AFG could grow its book value per share at a double-digit annual rate.

Over the last 20 years, the management has been focused on consistent growth, which has resulted in huge value generation for the shareholders, who enjoyed substantial returns from stock price appreciation along with huge dividend payouts.

The company operates on an entrepreneurial business model, where each company-owned business has autonomy over underwriting policies; such an attractive business model might be a reason behind the success of the business in various segments.

Also, the company has a diversified underwriting portfolio, which is separately managed by its 35 subsidiaries; these subsidiaries have strict underwriting policies that help AFG to keep its loss ratio below the average.

Although the stock has produced huge returns historically, in the upcoming years, returns might lag substantially due to the relatively higher valuation. The higher dividend yield that the shareholders have enjoyed in the last two years are the result of one-time gain; therefore, I believe in the future, the dividend yield might go down to about $500 million (as per the historical data).

Historical performance

Over the last ten-year period, revenue has grown from $5.1 billion in 2013 to about $7 billion by 2022 ; However, the growth rate does not seem attractive; the share prices have appreciated considerably, resulting from multiple expansions.

Due to its strong operating performance, cash flows have been considered attractive over the period, and management's capital allocation has been bearing fruit for the investors.

share price (YCHARTS)

From 2009, the stock rose more than six folds, producing a significant return to the shareholders; after recovering from the 2020 crash, the stock is currently trading near its all-time high level of $120 per share. Buying a stock during the crash of 2009 has produced a huge value, but from this price point it may not produce desirable returns.

Strength in business model

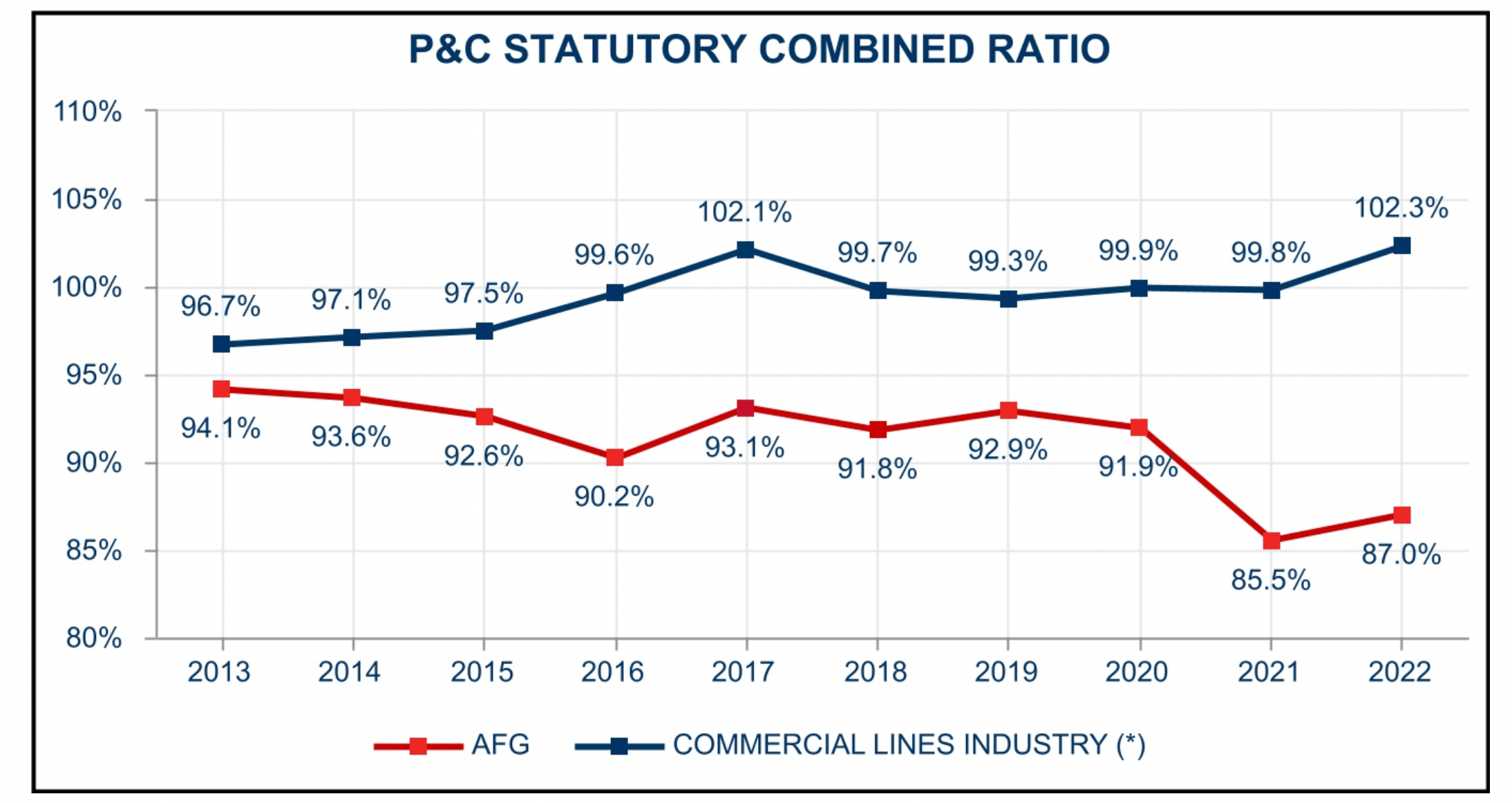

combined ratio (annual report )

{kind=link}

Strict underwriting policies have been playing an important role for the company; as a result, over a very long period, the combined ratio has remained below the industry averages, producing significant underwriting profits for the company. It should be appreciated that the company has maintained its loss ratio at an adequate level while expanding in various segments through organic expansions and acquisitions. Due to the strong operating performance over the period business has generated significant cash flows, which have been used for CAPEX, dividends, and share buybacks, resulting in considerable value creation for the shareholders.

{kind=link}

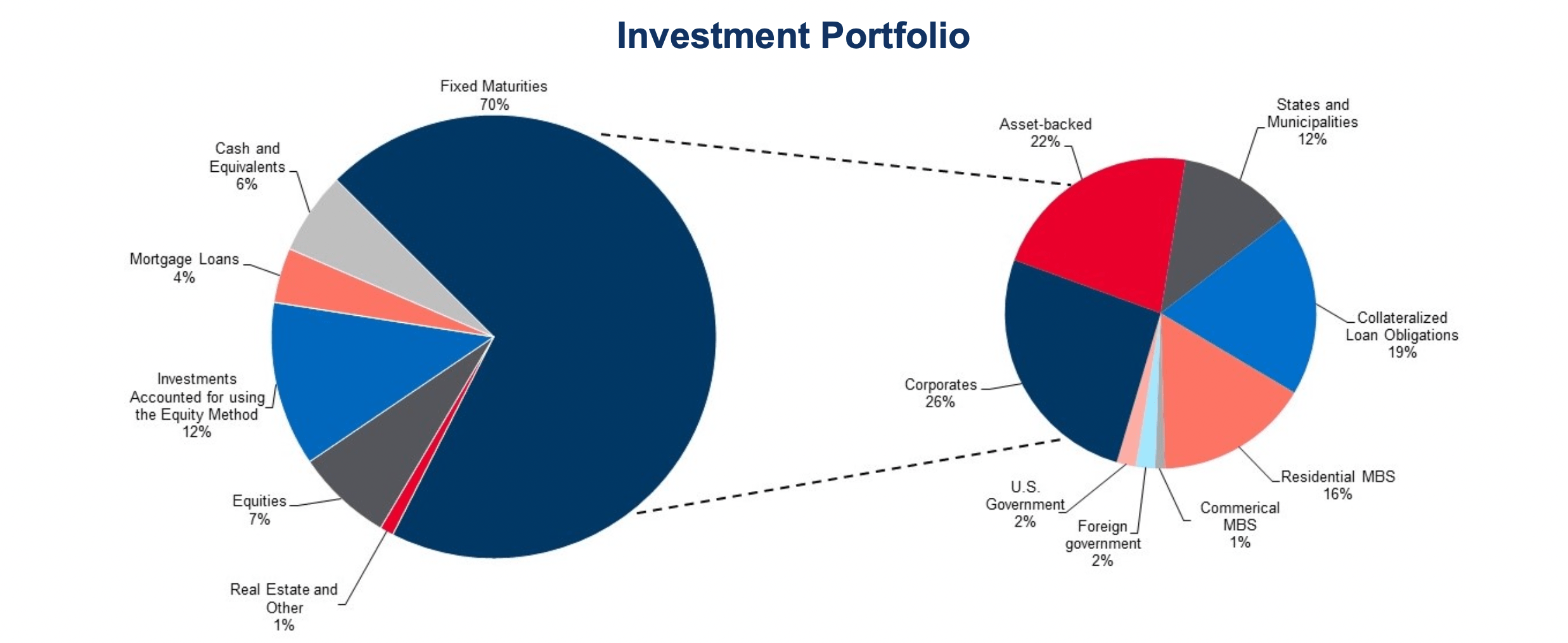

The insurance business generally has two sides of operations, one where the strong underwriting performance brings profits and another where the insurers get benefitted from investment income; In the case of AFG, the underwriting side is very strong and expected to remain strong due to its strict policies, whereas investment results might bring volatile earnings, due to its exposure of equity investments.

Furthermore, due to a significant part of investment income coming from fixed-income securities, the investor can expect a fixed income of about $350 million (as per the current investment). Historically this side of the business has produced stable and consistent earnings.

Risk factors

Currently, I do not see any major risk that can affect the business model, but there are various things that I think investors must take a look at it.

{kind=link}

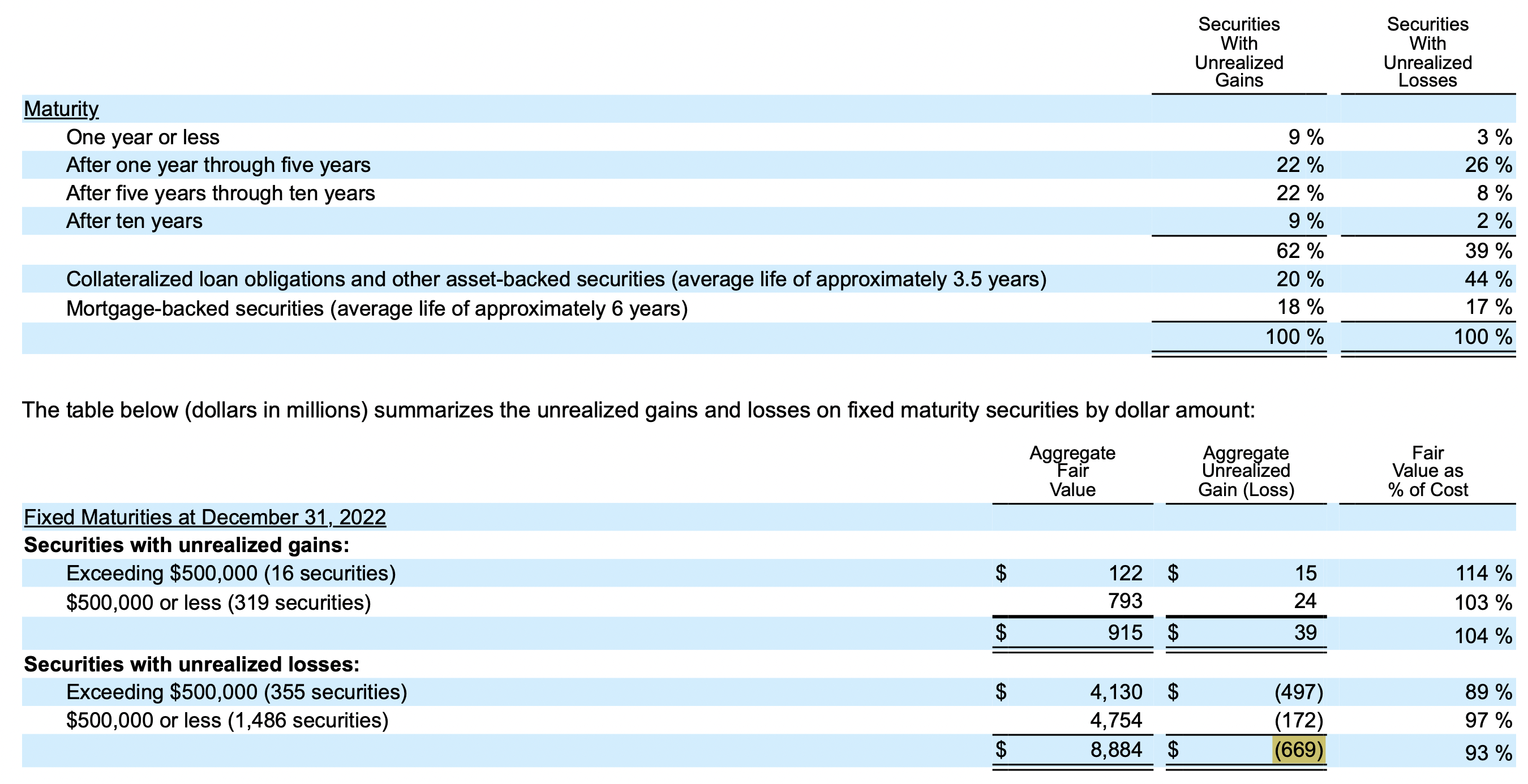

During the pandemic, to get better yield, management had allocated considerable capital in long-term mortgage-backed securities; as interest rates started rising, the value of these relatively low-yielding instruments started dropping; as a result, the company has accumulated an unrealized loss of nearly $669 million. Although the loss can be mitigated by holding the instrument until its maturity, investors must be aware that if the condition becomes adverse, it can affect the company's ratings; in such cases, the company might suffer significantly.

investment income (annual report )

{kind=link}

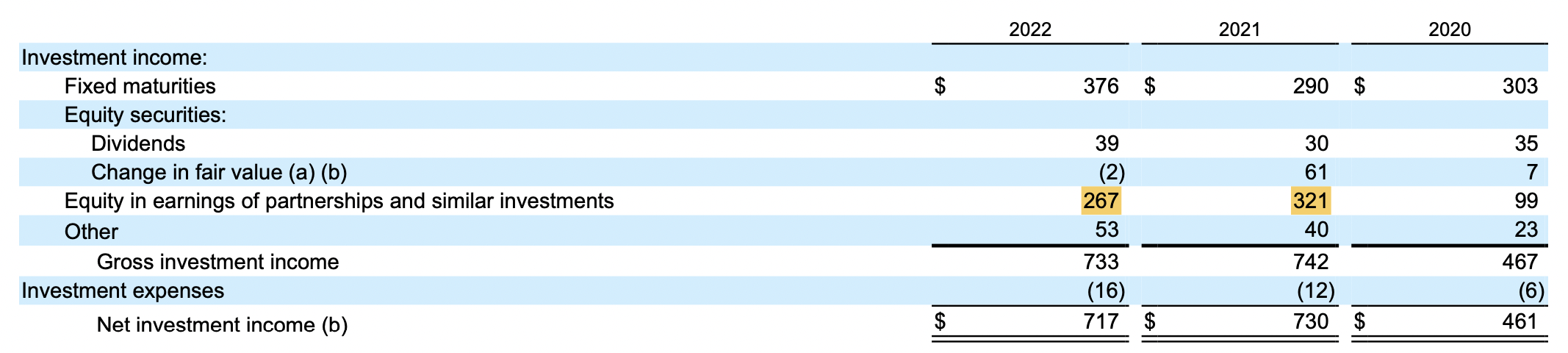

Also, the substantial profits that the company has been enjoying over the last two years are partially attributed to solid investment income; consider that the significant rise in investment income has resulted from a one-time gain on equity earnings, and such gains might not last for a longer duration; therefore, I expect that the profitability might reduce significantly in the upcoming years.

Furthermore, the sharp rise in dividend income is attributed to one time gain on the sale of the business ; therefore, I also expect that in the upcoming years, dividend payout might reduce to the historical average range of nearly $400 million to $500 million.

Recent development

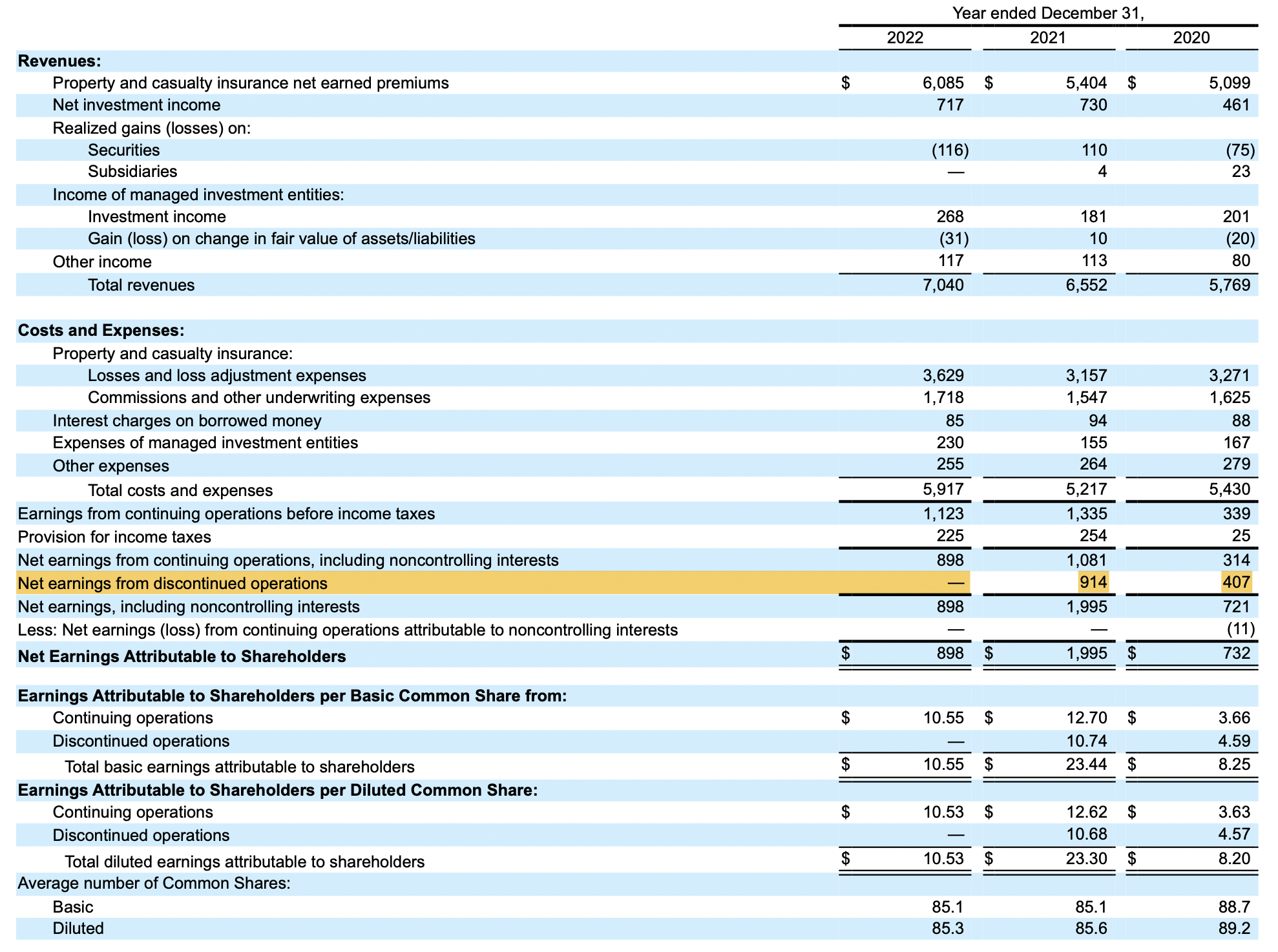

income statement (annual report )

{kind=link}

In 2022, revenue reached $7 billion from $6.5 billion last year, the company has posted earnings of $898 million, resulting from strong underwriting profits and a substantial investment income. Although the company has incurred unrealised losses on investment securities, the management could tackle the situation by holding these instruments till maturity. AFG produced substantial cash flow during the year, which has been used for debt reduction and dividend payment. Over the period debt levels have reduced to $1.4 billion; making the financial position of the company even stronger.

Currently, the company is trading for about $9.88 billion , whereas it has produced over $900 million in net profits (but consider that the recent rise in earnings is attributed to one-time gain on equity instruments); In my view earnings might drop because of the reasons discussed above; therefore, based on the historical performance I consider that the earning power of the business is in the range of $400~$500 million. Based on the assumption, the stock is currently trading for about 20 times its earnings; which seems fairly valued. I assign SELL ratings to the stock, as the stock reflects the actual value of the business and from this price point holding the stock might not produce desirable returns.

For further details see:

American Financial Group May Not Produce Desirable Returns