AFG - American Financial Group: Q2 Bullish On Revenue And Bearish On Underwriting

2023-08-22 06:11:29 ET

Summary

- American Financial Group reported Q2 2023 earnings with lower non-GAAP EPS but higher revenue than expected.

- AFG is making progress in reducing unrealized losses and showing promise in medium-term securities and alternative investments.

- There are challenges in the underwriting game and a spike in claim expenses, suggesting a cautious "hold" rating for the stock.

Thesis

Taking a look at American Financial Group's ( AFG ) Q2 2023 earnings, they came up short on the non-GAAP EPS by $0.41 , landing at $2.38; however, on the flip side, they pulled in $1.84 billion in revenue, which is $230 million more than what analysts were expecting. Peeling back the layers, they're making headway on reducing those unrealized losses and the company is showing promise in medium-term securities and alternative investments. However, there's some turbulence in the underwriting game and a spike in claim expenses. So, even though there are some solid points in AFG's playbook and it might be undervalued in the market scene, there are a few bumps to keep an eye on for the next stretch.

Company Overview

American Financial Group, Inc., headquartered in Cincinnati, Ohio, operates as an insurance holding entity focusing on property and casualty insurance within the U.S. spectrum. The company's portfolio encompasses insurance coverage for various transportation modalities, including buses, trucks, and marine vessels, alongside those catered to agricultural sectors. In addition, they delve into casualty insurance sectors, covering professional and general liabilities, with special packages designed for businesses of varying sizes. The firm also forays into the financial insurance landscape, catering to lenders with products such as fidelity, surety, and trade credit insurance. Their distribution model leans on the expertise of independent agents and brokers. A notable element of their history is their establishment in 1872, cementing their longstanding presence in the insurance arena.

American Financial Group's Q2 2023 Earnings Highlights

Reviewing the latest financials, the company shaved down its unrealized losses from a hefty $630 million at the end of 2022 to $587 million by mid-2023 - it's not a massive drop, but it's definitely moving in the right direction.

Now, on the topic of how AFG is handling their investments: they've invested cash into medium-term securities that have been giving back about 5.5%. And if you remember, just a quarter before, they were looking at a 4.62% yield. They're even hinting that the yield might nudge up by 10-20 basis points by year-end.

Their Property & Casualty section has been doing some heavy lifting, with the net investment income ramping up by 22% compared to 2022. And here's something that caught my eye: their side venture in alternative investments. In this year's second quarter, they pulled in a solid 9.6% annual return, and they owe a hat tip to areas like multifamily housing and private equity for that boost. If we're talking history, over the past five years, they've managed an average annual yield of about 14% from these alt investments.

Looking at their financial health check from June 30, 2023, AFG's sitting on a comfy cushion of around $700 million in extra capital. The move to grab CRS? That looks like a play to make good use of this extra cash and dive deeper into specialized areas. Co-CEO Carl Lindner added some color on this by noting:

CRS is clearly a strategic fit within our crop division and solidifies Great American as the fifth largest provider of multi-peril crop insurance in the United States and the largest U.S.-owned participant in the United States multi-peril crop insurance program, and serves as an example of our nimbleness and efficiency in executing a transaction of this nature.

Moreover, as a toast to AFG for not forgetting their shareholders, since the curtain dropped on 2020, they've given back a cool $3.6 billion, mostly through special dividends. According to management, they're even considering funneling more than $500 million for buying back shares or rolling out more dividends by the end of this year.

Two numbers to chew on from Q2 2023: AFG's book value per share along with dividends climbed up by 3.1%, and they've seen a bump of 12% in gross premiums and 10% net, year over year. And one more fact: they've been consistently hiking up their renewal rates, marking the 28th straight quarter they've done so.

Performance

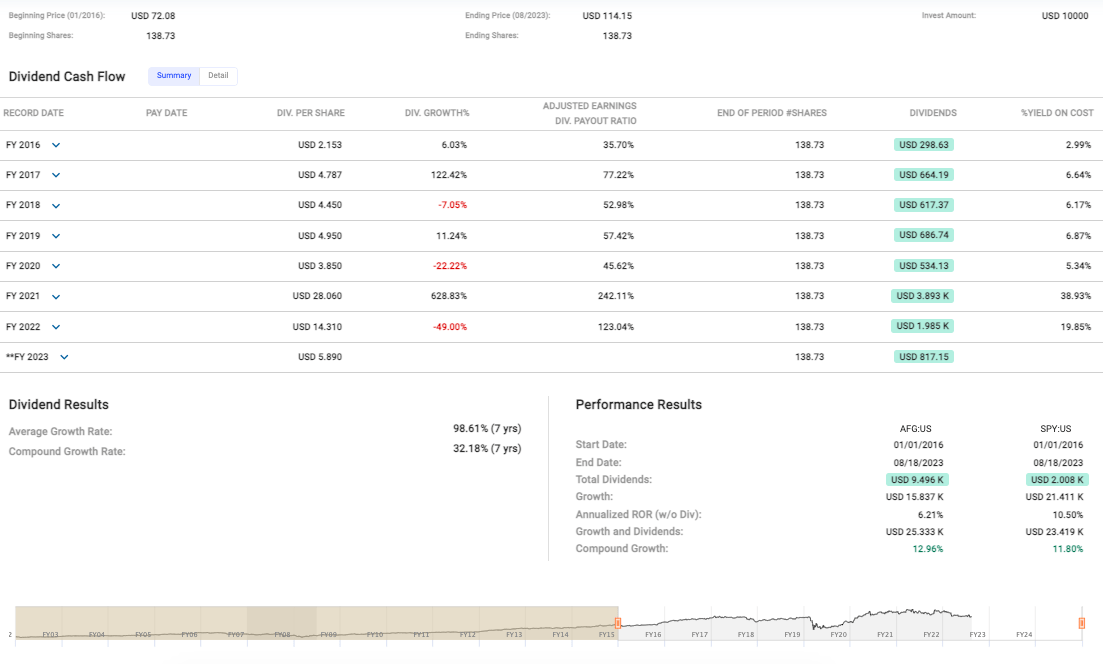

The first thing that catches my eye is AFG's dividend growth: an average growth rate of 98.61% over seven years, which has a compound growth rate of 32.18% is remarkable and suggests that AFG has had significant cash flow that's been channeled back to the shareholders over this medium-term time frame (see data below). However, the inconsistency in dividend growth is worth noting but doesn't raise any immediate red flags.

{kind=link}

In the broader context, when juxtaposing AFG's performance with the S&P 500 Index, some interesting disparities arise. While the absolute growth in dividends for AFG stands at USD 9.496K (on a hypothetical initial USD 10k investment), overshadowing S&P's USD 2.008K, it's the overall growth where the S&P takes the lead with USD 21.411K compared to AFG's USD 15.837K. Consequently, the annualized Rate of Return (ROR) without dividends for AFG is lower at 6.21% compared to the S&P's 10.50%. This indicates that despite its commendable dividend performance, AFG's core business growth might not have kept pace with the broader market.

However, when combining both growth and dividends, AFG manages to move ahead with a total of USD 25.333K, marginally ahead of the S&P's USD 23.419K that further solidifies AFG's position with a rate of 12.96%.

Valuation

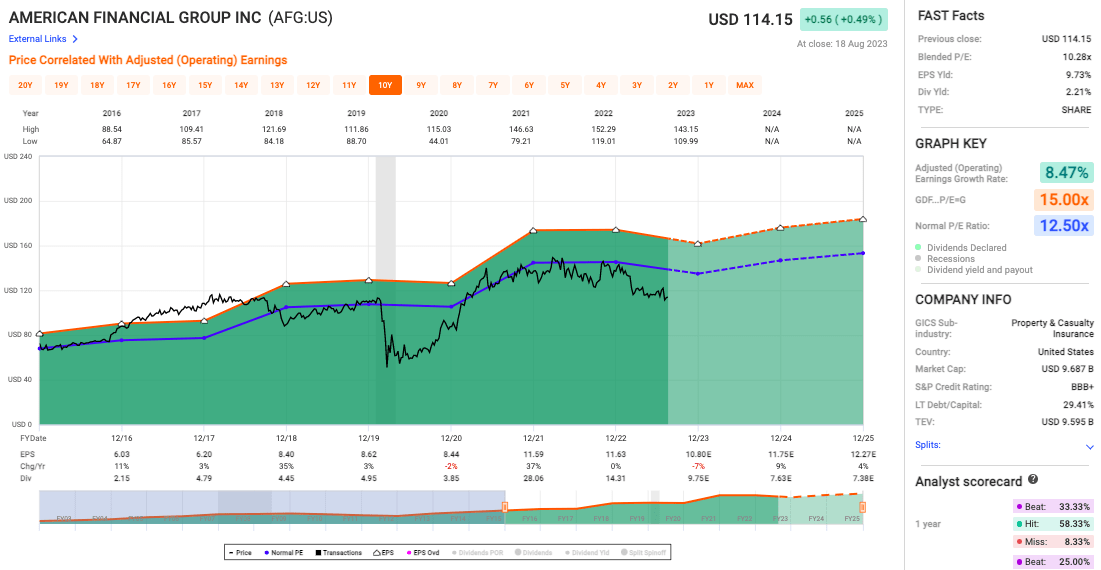

AFG's Blended P/E of 10.28x (see chart below) is noticeably below the company's historical norm of a P/E ratio at 12.50x which could imply that the company is currently undervalued compared to its historical pricing. When you consider the adjusted (operating) earnings growth rate at 8.47%, it becomes evident that the company has demonstrated a strong and consistent growth pattern. This rate, combined with the current P/E, makes me wonder if the market is perhaps overlooking some growth prospects for the company.

{kind=link}

Risks & Headwinds

Diving into the numbers, the returns on the aforementioned alternative investments in Q2 2023 did catch the eye, but there's a bit of a step back from the 12.4% we saw in the same period of 2022.

Then there's the combined ratio - a key barometer to get a sense of how profitable an insurance company really is. For Q2 2023, this ratio clocked in at 91.9%. Put simply, that's an uptick of 6.1 percentage points from the year before. Reading between the lines, the company had a bit more going out in claims and expenses than what was coming in from premiums.

Next, the impact of catastrophic losses: they piled on an extra 3.5 percentage points to that combined ratio in Q2 2023. To give that some context, it's an increase of 2 points from the year before - something investors might want to keep an eye on for sure.

Breaking it down by group gives us a bit more color on the year-to-year differences. The Property and Transportation Group? Their underwriting profit came in at $32 million for Q2 2023, a tad lower than the $39 million from Q2 2022.

The Specialty Casualty Group had a similar story. Their underwriting profit dropped to $95 million this quarter, down from a heftier $130 million in the same period the year before. And the Specialty Financial Group? They posted an underwriting profit of $10 million in Q2 2023, a pullback from the $37 million in Q2 2022.

Given all these shifts, it seems like a smart move on the company's part to revise its core net operating earnings outlook for 2023 a bit downwards from what they first thought.

Rating: Hold

From the data given, AFG has been good at cutting down those unrealized losses and they're seeing some growth in their investments. Plus, with their dividend game and their current P/E ratio, it looks like the stock might be priced lower than its worth. But here's the other side: they're spending more on claims and their underwriting profits took a hit. And while there could be room for growth, there are some bumps along the way; therefore, I believe a "hold" is the way to go in the near-term until we see which way the wind's really blowing.

For further details see:

American Financial Group: Q2, Bullish On Revenue And Bearish On Underwriting