INVH - American Homes 4 Rent: A Great Catalyst But At A Not-So-Great Price

2023-03-26 11:43:46 ET

Summary

- American Homes 4 Rent has demonstrated itself to be a great firm with an amazing ability to grow over time.

- On top of this, the firm has a nice growth catalyst that should translate to greater returns for investors moving forward.

- But shares, while cheaper than in the past, are not yet low enough to justify attractive upside for investors.

From my experience, it's rare that you come across a company whose name describes exactly what it does. But one such example where this is the case involves a business called American Homes 4 Rent ( AMH ). As its name suggests, the company is a REIT that acquires, develops, renovates, leases, and manages homes as rental properties. In particular, it focuses on single-family homes. With its footprint spread across 21 different states, and 58,993 homes under its belt, American Homes 4 Rent is a massive player in its market. Recently, financial performance achieved by the company has been rather robust. On top of this, the company also has some appealing catalysts to push revenue, profits, and cash flows all higher in the years to come. In the long run, I suspect that the business would do just fine for itself and its investors. Though I do maintain that the stock is not yet cheap enough to warrant a meaningful vote of optimism. Given this, I would still rate the business a ‘hold’ as opposed to anything more bullish than that.

Recent financial performance is encouraging

The last article that I wrote about American Homes 4 Rent was published in July of last year. Back then, I acknowledged that the company was doing well from a fundamental perspective, with pretty much all of its important metrics showing growth year over year. At that time, however, shares of the company looked a bit lofty. This, combined with growing economic uncertainty, caused me to take a more cautious approach to the business, ultimately resulting in a ‘hold’ rating. Since then, however, shares have taken something of a tumble, generating a loss for investors of 14.5% while the S&P 500 is up 3.6%.

{kind=link}

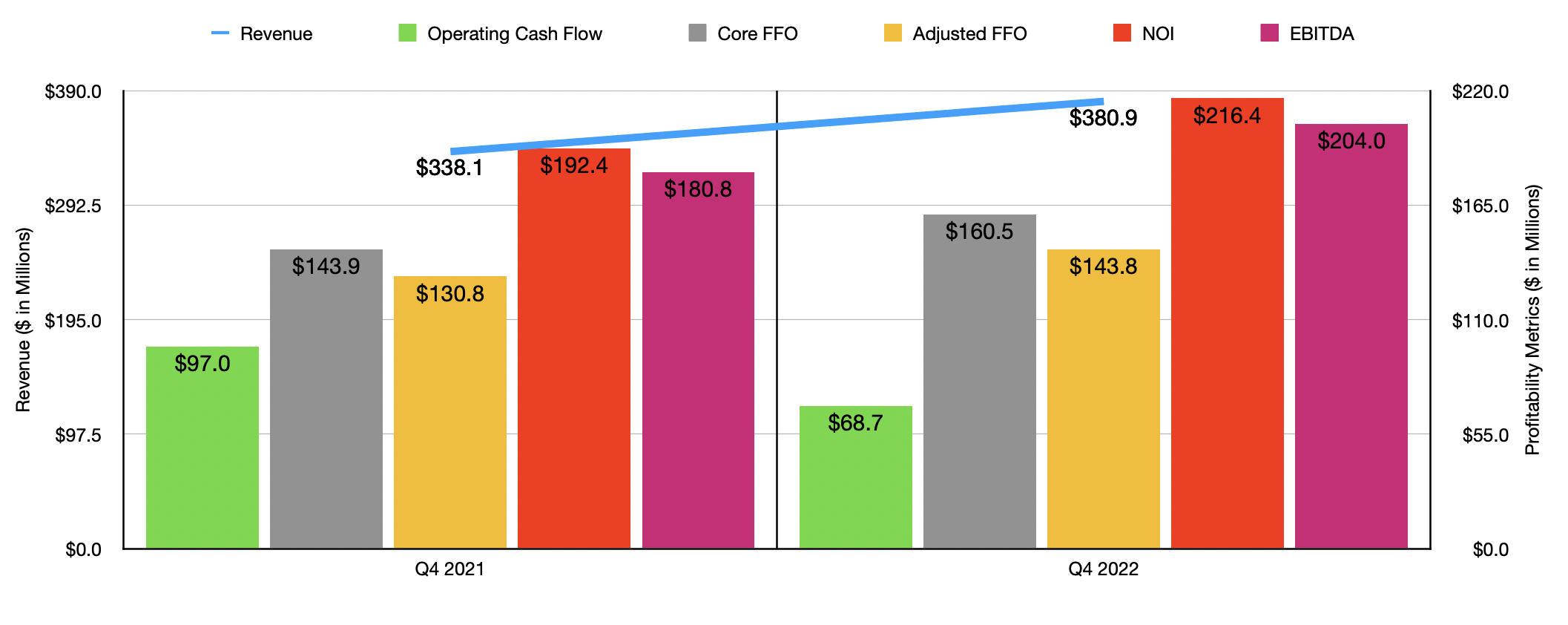

Given this return disparity, you might think that the fundamental condition of the company was worsening. But that has not in fact been the case. Consider how the business performed during the final quarter of its 2022 fiscal year . This is the final quarter for which data is available. During that time, sales came in at $380.9 million. That represents an increase of 12.7% over the $338.1 million reported only one year earlier. Some of this increase can be attributed to the fact that the occupancy rate of its properties inched up from 95.7% to 95.8%. However, the company also benefited significantly from a rise in the number of properties in its portfolio from 57,024 to 58,993. This excludes the 659 properties that the company held for sale at the end of 2021 and the 1,115 that were held for sale at the end of last year.

For the most part, this rise in revenue brought with it improved profits. The one exception involved operating cash flow. During the quarter, this metric was $68.7 million. That's down from the $97 million reported one year earlier. If we look at other metrics, however, we see that the picture has mostly improved. Core FFO, or funds from operations, expanded from $143.9 million to $160.5 million. On an adjusted basis, FFO expanded from $130.8 million to $143.8 million. Another metric, called NOI, or net operating income, grew from $192.4 million to $216.4 million. And finally, EBITDA for the business expanded from $180.8 million to $204 million.

{kind=link}

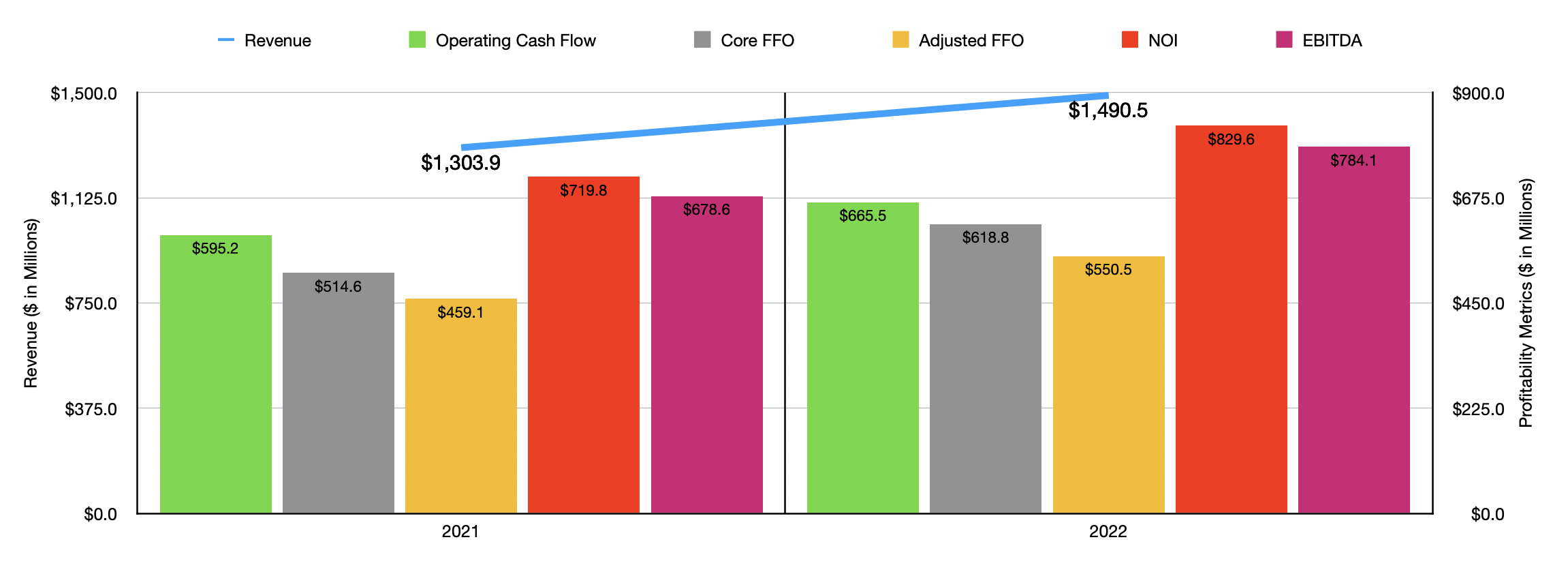

The final quarter of 2022 was not the only time in which the company saw expansion. As you can see in the chart above, results for 2022 as a whole were better than they were in 2021. In addition to this, management seems to think that core NOI this year will be between 3% and 5% higher than it was in 2022. On the other hand, core FFO per share should weaken, dropping from $1.77 last year to between $1.58 and $1.64 per share this year. This bottom line weakness should come even as the company anticipates between 2,200 and 2,400 deliveries for 2023.

{kind=link}

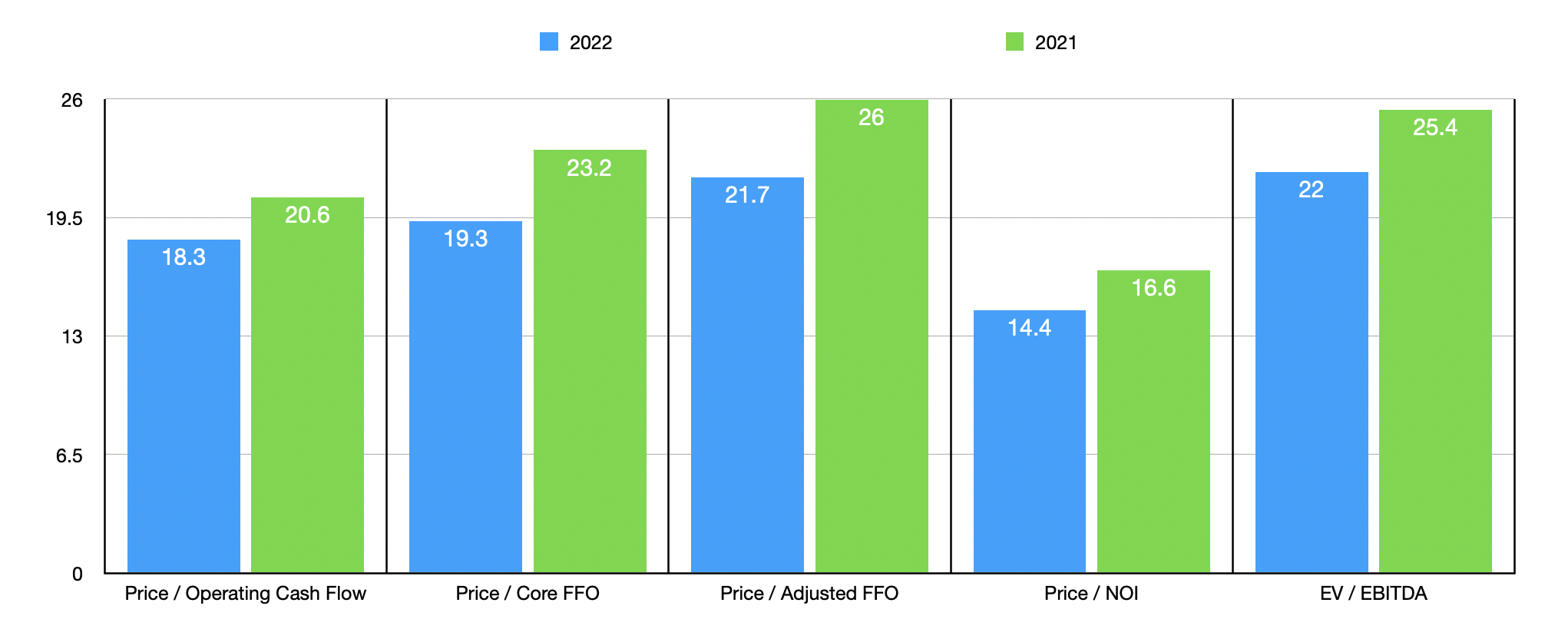

Despite this weakness, the company does still look to be in solid condition. But this doesn't necessarily mean that it makes sense to buy into at this time. Consider, for instance, the chart above. In it, you can see various pricing metrics for the company for both 2021 and 2022. And in the table below, you can see how the company is priced using two of those metrics compared to five similar businesses. On a price to operating cash flow basis, these companies have trading multiples of between 13.4 and 35.6. Two of the five firms were cheaper than American Homes 4 Rent. Meanwhile, using the EV to EBITDA approach, we get a range of between 15.8 and 25. In this case, three of the five firms were cheaper than our target.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| American Homes 4 Rent |

| 18.3 |

| 22.0 |

| Equity LifeStyle Properties ( ELS ) |

| 20.9 |

| 24.1 |

| Sun Communities ( SUI ) |

| 22.0 |

| 20.8 |

| Invitation Homes ( INVH ) |

| 17.6 |

| 18.9 |

| UMH Properties ( UMH ) |

| 35.6 |

| 25.0 |

| Essex Property Trust ( ESS ) |

| 13.4 |

| 15.8 |

An attractive catalyst for future growth

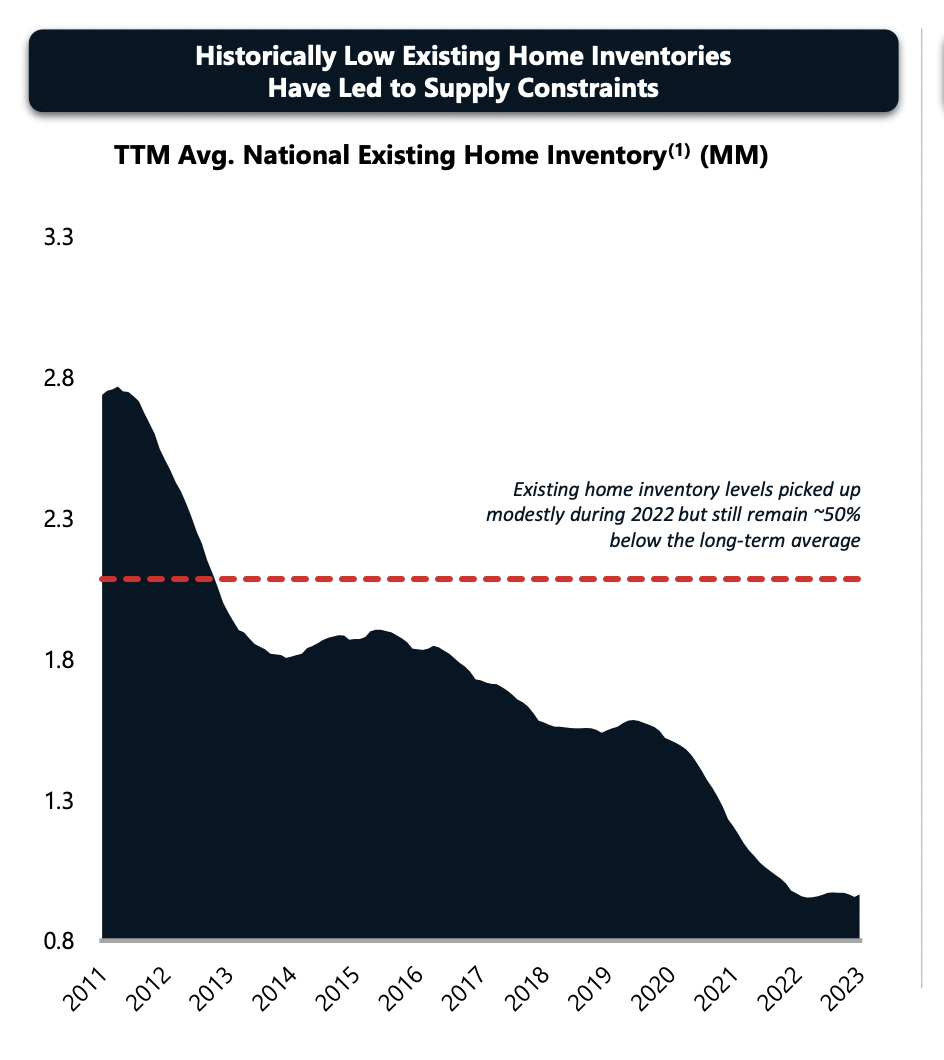

Although I acknowledge American Homes 4 Rent as a quality company that should continue to grow in the long run, I also believe that the stock is not cheap enough to warrant all that much consideration from value-oriented investors. At the same time, I can also understand why some investors would be drawn to the firm. The fundamental data aside, the company does have some really great things going for it. For instance, right now, the national existing home inventory is quite low . In fact, it's lower than at any point between 2011 and the present day. For perspective, back in 2011, roughly 2.8 million homes were counted in housing inventories. Today, that number is around 900,000.

{kind=link}

In addition to there being a rather tight market, there also is not much in the way of single-family permits. After bottoming out in 2011, at around 400,000 permits, the number began to increase year after year, eventually hitting nearly 1.2 million in 2021. But as you can see in the chart below, that trend was broken in 2022 and looks set to fall further this year and over the next few years. What this suggests, when coupled with a continuously growing population, is that demand for housing should still rise while supply remains constrained. This should, in theory, push the cost of buying properties up even more, which could prove to be a boon for property owners that rent out.

{kind=link}

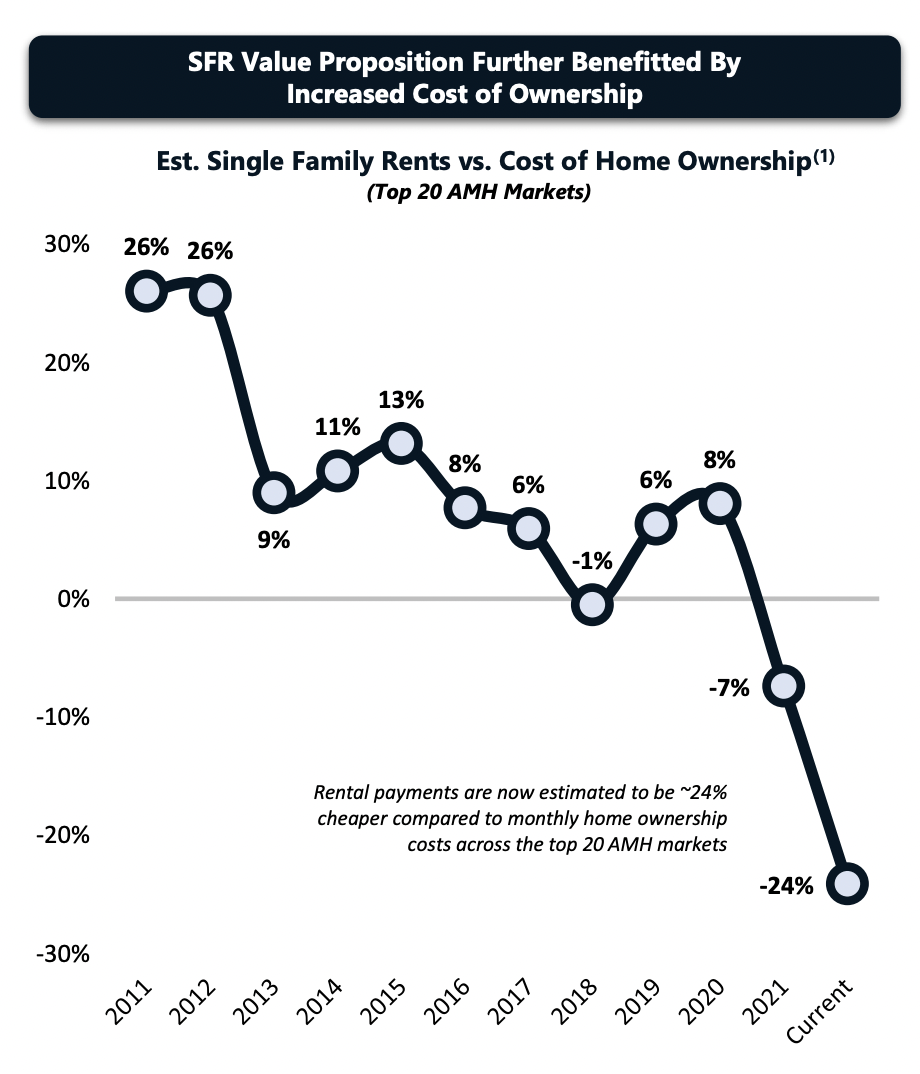

Based on the data available, at least when it comes to the top 20 markets in which American Homes 4 Rent operates, we are already seeing some benefit that should accrue to the business. As you can see in the chart below, it is now cheaper to rent in those markets than it is to own a home. When coupled with the other data I already mentioned, this implies that companies like American Homes 4 Rent should be able to raise their prices further without experiencing any decrease in their occupancy rates.

{kind=link}

Takeaway

Fundamentally speaking, American Homes 4 Rent looks to be in really solid shape. Long term, I suspect the company will continue to grow and I believe that it should ultimately increase in value for shareholders unless something materially changes. The company currently has a positive catalyst that should help to push revenue and cash flows higher. And even though the market for single-family properties is constrained, the business continues to grow its portfolio. These all spell a recipe for success. But I just can't get behind the company yet because of the price at which shares are trading. If the stock falls further, perhaps another 10% or 15%, I believe that I could get around to rating it more highly. But until that comes, I believe that there are better opportunities that can be had and that this business warrants a ‘hold’ rating.

For further details see:

American Homes 4 Rent: A Great Catalyst, But At A Not-So-Great Price