AMH - American Homes 4 Rent: Strong Fundamentals Are In The Price

2023-11-28 13:58:08 ET

Summary

- American Homes 4 Rent has performed well despite higher interest rates, but its valuation suggests it is a "hold" rather than a compelling buy opportunity.

- The company's adjusted funds from operations in Q3 were slightly below expectations, but management expects FFO growth of 7% for the full year.

- The rental market has cooled off, but AMH remains strong due to the undersupply of housing and its focus on desirable locations.

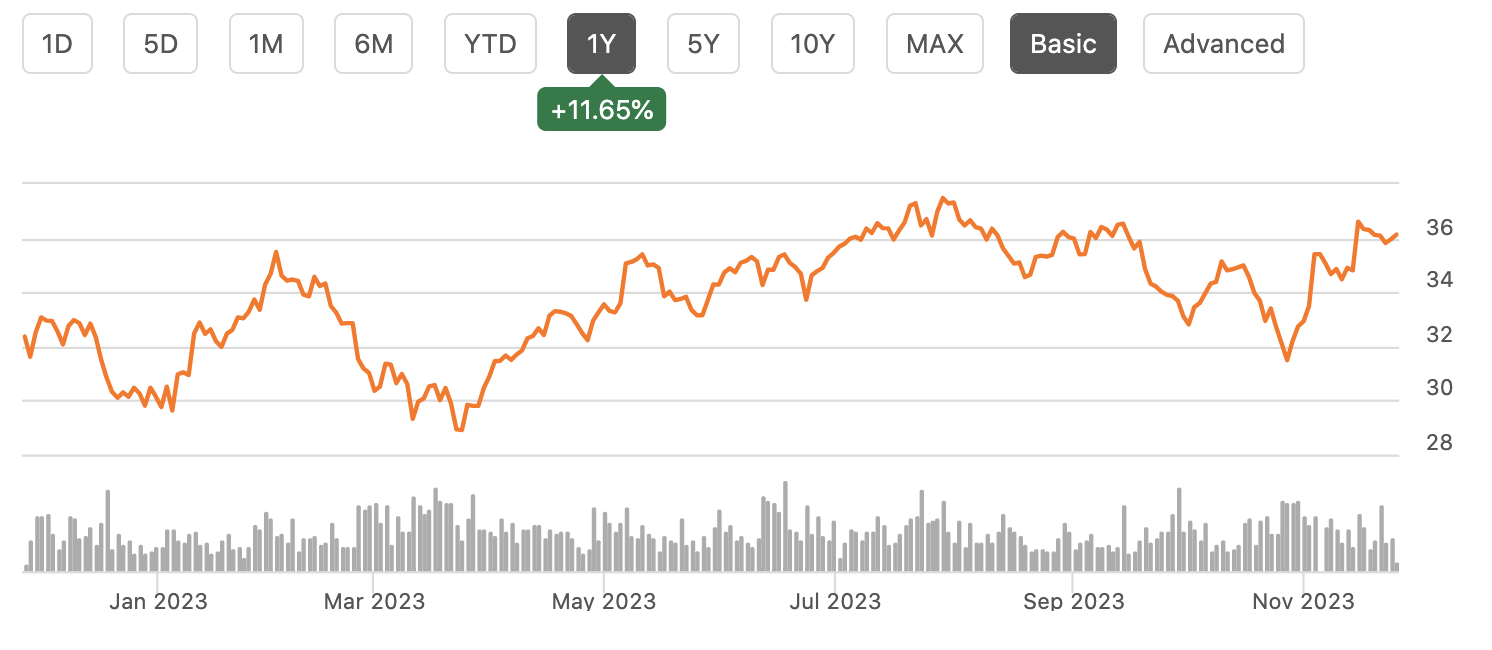

Shares of American Homes 4 Rent ( AMH ) have been a solid performer over the past year, rising over 11%, despite the impact of higher interest rates on most real estate-related stocks. American Homes has been performing well with unique aspects to its business model, helping it manage through a shortage of housing inventory. Given its outperformance though, I believe its valuation reflects this, making shares a “hold” rather than a compelling buy opportunity.

{kind=link}

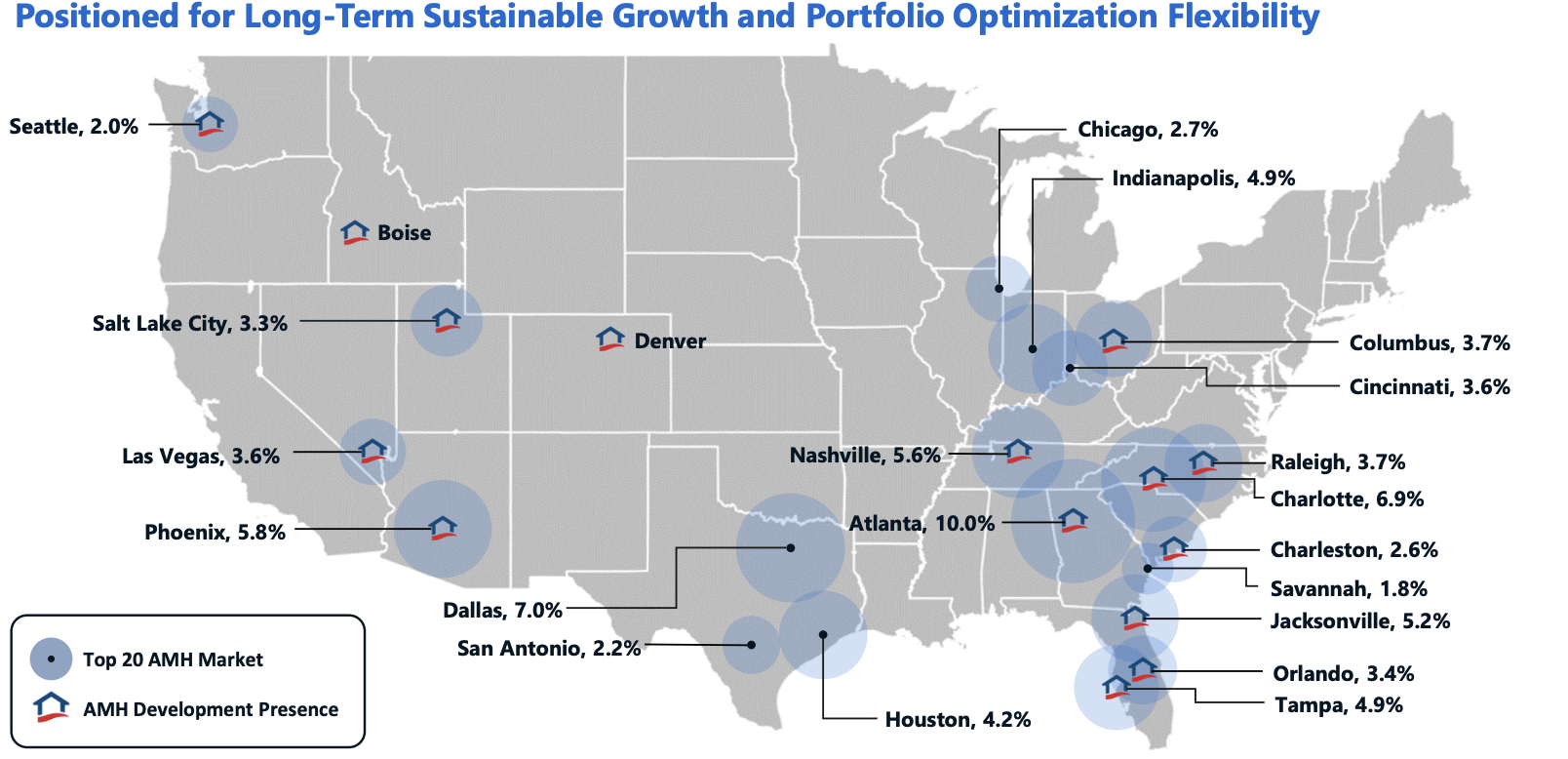

In the company’s third quarter, funds from operations (FFO) were $0.35, which was $0.06 below estimates even as revenue rose nearly 8% to $422 million. This was primarily due to cap-ex timing with core FFO coming right in-line at $0.41 . Core FFO was up 5% from last year. Alongside this, management now expects full year FFO of $1.64-$1.66, representing about 7% growth as same-home net operating income (NOI) rises by 4.5% AMH owns over 58,000 single-family houses, which it rents out. While most rental companies are multifamily, AMH and Invitation Homes ( INVH ) focus on single family units. Even as the company has a presence across the entire country, it is focused in the faster-growing Sun Belt. Atlanta is 10% of its business while Florida is nearly 14%, across several cities.

{kind=link}

Over the medium term, I believe real estate investors will benefit from investing in locations with strong population growth, aided by domestic migration patterns. This does make AMH’s footprint favorable, even as the South has in the near-term seen more supply as builders have focused their efforts here. As supply has hit the market and as disposable income growth has stayed slow, we have seen the rental market cool off across the nation. Over the past year, rents are down 1.2% , though this is largely concentrated in the traditional apartment sector.

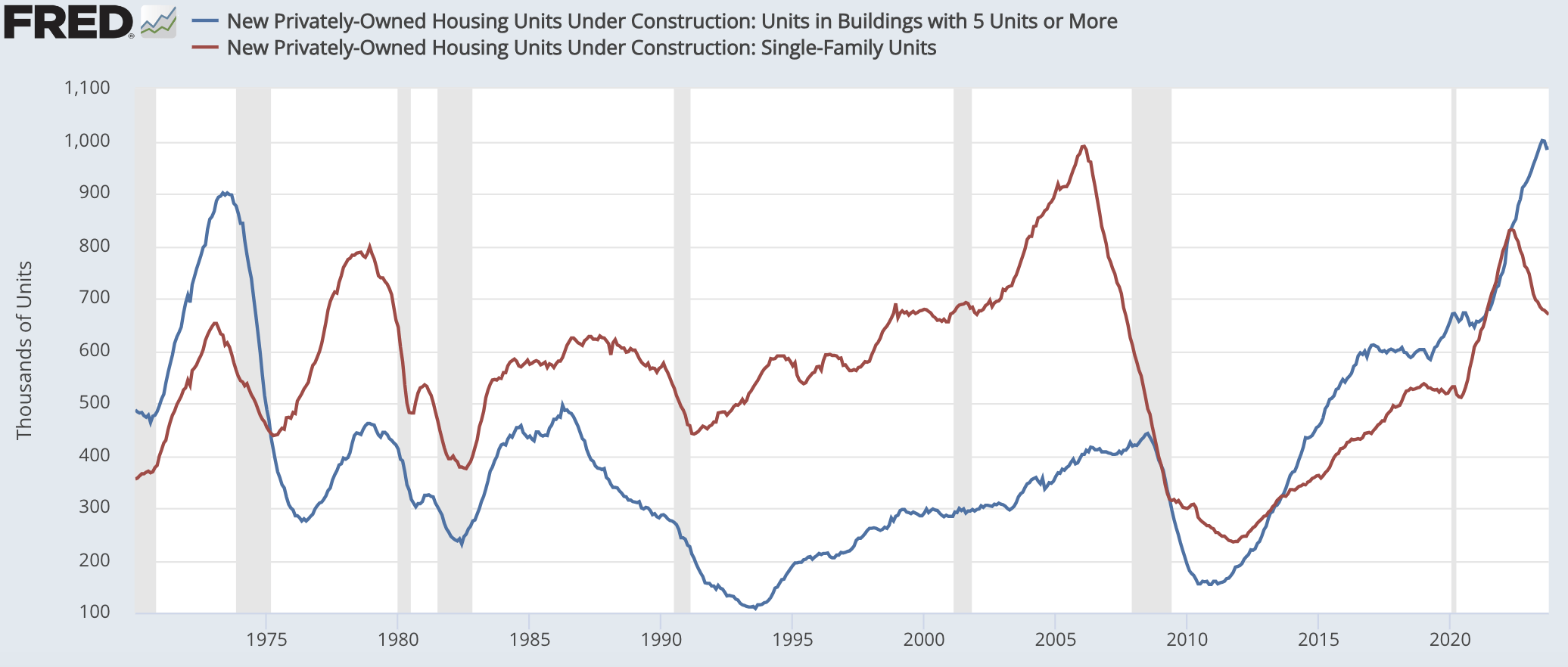

As you can see below, the number of multifamily units under construction has hit a record as the surge in rents post-COVID enticed a wave of building. By and large, multifamily units are built to be rented. Conversely, single-family units are primarily built to be sold. When rates began rising sharply last year, homebuilders pulled back, leading to a decline in units under construction, though they remain above pre-COVID levels.

{kind=link}

While there is undoubtedly a connection between apartment and single-family rental rates, I would argue these markets are different. Multifamily units are more urban on average than single-family. Their respective renters are likely seeking and valuing different things (i.e. having your own yard), particularly if they have children. While extreme differences in rent prices could move renters from an apartment to single-family home, or vice versa, we are unlikely to see a one-for-one correlation.

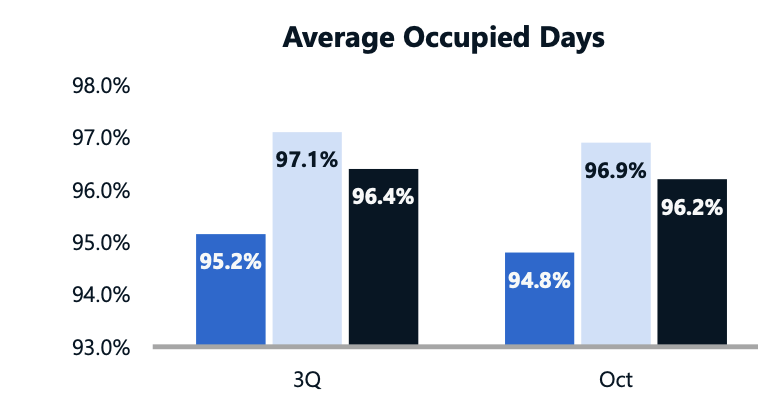

This has indeed played out. While AMH has not been immune to the weaker rental market, it has held up fairly well. Rents rose 7.2% in Q3, which is solidly positive, though down from 9.5%. We have seen some continued cooling with October at 5.8%. Still, this is meaningfully better than the 1.2% rent decline nationally. Due to mix shift from new units, AMH’s average realized rent rose a more modest 1.9% to $2,086. Where we do see some weakness is on occupancy, which was down 70bp from last year.

American Homes 4 Rent

{kind=link}

This metric is below the record levels seen last year when the rental market was extremely hot. However, it does remain 140bp above the pre-COVID norm. This is consistent with my view that the rental market has cooled down but that it continues to operate at a strong level. This is because the housing market is fundamentally undersupplied. As you can see below, we have built four million fewer homes over the past twenty years than we have created households.

Census Bureau, My Own Calculation

During the 2000s, we actually built more homes than formed households given the housing bubble’s surge in construction. However, construction fell so much during the crash that we fell behind and the rise in household formations in 2020 exacerbated this shortage, causing rents and home prices to rise substantially. It is profitable to operate in supply-short markets, as that provides meaningful pricing power. It is a reason why I am structurally bullish on US housing-related investments over the medium term, as I expect rents to rise faster than inflation. With single-family houses under construction now declining, this shortage is poised to continue for some time. While we are unlikely to return to double-digit rental growth, if inflation is targeted at 2% by the Fed, I do view 3+% rental inflation as likely to persist.

One headwind for AMH’s results over the past year has been that while revenue has risen by 8% thanks to property count growth and rent increases, property owning expenses rose by 10% to $167 million, which is why FFO is rising just 7%, showing no operating level from this revenue growth. This strong expense growth is largely out of AMH’s control. In fact, property management expenses rose by just 3% to $30.8 million.

On the other hand, property taxes were up 12.9%. These tend to lag home prices as appraised values rise to catch-up with the price gains seen in 2020-2021. With home prices stabilizing, we should see property tax growth slow next year. The other major headwind was insurance, which was up 27% to $4 million. This is a relatively small expense, but a large rise. The significant increase in construction costs caused losses for insurers as severity of claims was higher than expected, which has led them to raise premiums to recoup pricing.

With construction inflation having moderated from supply-chain impacted levels in 2021 and 2022, we should begin to see insurance premiums rise more slowly next year. In essence, tax and insurance premiums, given their annual payment profile, tend to lag underlying cost changes. While rental growth may slow, slowing expenses should help to mitigate this impact on FFO. Further, AMH has seen average recurring cap-ex of $421/house rise about 9% from last year. This is about 7% of monthly rent. With construction costs normalizing, we should begin to see this cost growth also moderate next year. Indeed, while up 9% in the quarter, this metric is up 19% year to date, so we have seen meaningful deceleration throughout the year, an encouraging sign.

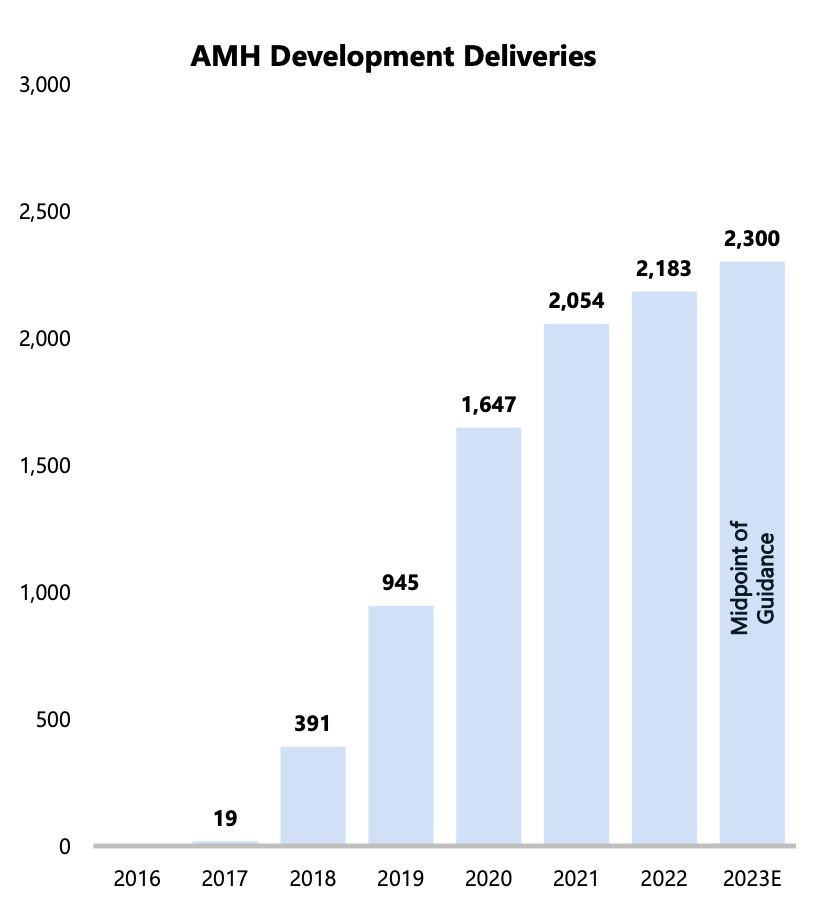

One thing that is unique about AMH is how it adds properties to its portfolio. Of course, it actively purchases homes on the existing home sales real estate market. However, supply here has been constrained as owners with low mortgage rates locked in are reluctant to sell. It also can use its size to arrange bulk purchases with the major national homebuilders should they have excess inventory they need to sell. Most interestingly though, it builds its own homes to rent. This allows AMH to model units according to the most valued metrics favored by its renters.

It has a 13,000 unit pipeline of self-built homes. AMH will receive about 1,850 wholly-owned deliveries this year, and 2,300 total through joint-ventures. This provides it a way to continue to grow property counts in desirable locations without facing inventory constraints in the existing resale market.

{kind=link}

Critically, AMH sizes its building program based on what it can fund out of retained cash flow rather than needing to leverage its balance sheet to fund construction. This is prudent in a time of high interest rates and in keeping with AMH’s strong balance sheet with 5.4x debt to EBITDA. It carries just $4.43 billion of debt for a 37% debt to capitalization. Considering that a new homebuyer puts down 20% often, borrowing 80% for an 80% debt to capitalization, AMH essentially carries less than half as much debt as it could. This gives it ample balance sheet flexibility to fund new purchases and manage through economic uncertainty.

Overall, AMH is performing solidly, operating in an attractive niche within the US housing market. It is benefitting from relatively light supply and solid rental pricing power. Assuming rent slows to about 3%, and with about 5% property growth, AMH should be able to generate upper-single digits revenue growth next year, which I expect to result in 7-10% FFO growth or about $1.75-1.80. That provides ample room to grow its 2.44% dividend yield.

Shares have about a 4.9% 2024 FFO yield. Now, this is not higher than apartment REITs, given the difference in supply discussed earlier. By comparison, a company like Mid-America Apartments ( MAA ) has a 7.7% 2024 FFO yield. Given my view about medium-term housing market fundamentals, I do think investors should look past near-term apartment supply and believe there is likely to be more upside in shares of REITs like MAA than AMH, given the different valuations. Still with its starting yield and 5-7% dividend growth capacity, AMH can generate upper single-digit returns over the medium term. I would not be a seller of shares and would buy shares if there was a 10% pullback, but given its outperformance, I see shares as a hold given opportunities elsewhere.

For further details see:

American Homes 4 Rent: Strong Fundamentals Are In The Price