AMH - American Homes 4 Rent: Too Expensive For Me

2023-12-07 17:26:27 ET

Summary

- AMH has grown to own over 59,000 homes and has a strong operating performance, with high occupancy and rental growth.

- AMH's current valuation is not compelling, trading at a premium to NAV, posing a significant risk if there are adverse developments in the SFR market.

- Tricon Residential remains the top pick for the single-family rental sector due to its valuation, despite AMH and Invitation Homes being more attractive in terms of fundamentals.

Summary

In this report, I conclude my dive into the US single-family rental universe by looking at American Homes 4 Rent ( AMH ). Having covered the 3 big players (Tricon Residential Inc. (TCN), Invitation Homes Inc. (INVH), and AMH), Tricon remains my top pick for the SFR sector purely on valuation. While I prefer Invitation and AMH to Tricon in certain aspects, mainly leverage and simplicity, their valuations appear full at this time. While Tricon deserves to trade at a discount to Invitation and AMH due to its leverage and complexity, I have factored this into my valuation and still see a far more attractive return potential than its peers. I also see more positive catalysts for Tricon through its development pipeline, the upcoming launch of its third JV, and the potential for outsized FFO and AFFO per share expansion if rates come down due to its floating rate exposure and upcoming maturities. As with Invitation, I give AMH a Sell rating based purely on valuation.

History

AMH's origin follows a similar path to Invitation Homes . In 2011, David Singelyn and Bradley Wayne Hughes, the founder of Public Storage ( PSA ), saw an opportunity to aggregate a large portfolio of single-family homes ("SFHs") at highly depressed prices in the wake of the GFC. Historically, SFHs have not been viewed as an institutional asset class due to the relatively small size and difficulty of acquiring and managing individual assets. The pair bought a few houses in Las Vegas as a test case and leveraged recent technological advances that enabled them to streamline their underwriting and asset management workflows.

The pair officially launched AMH in 2012 and took it public the following year, in 2013. Since then, the Las Vegas-based REIT has grown to own over 59,000 homes, with a further ~2,900 under management through several JVs.

Unlike Invitation and Tricon, AMH has not formed a significant relationship with large, active private capital managers. The invitation was largely a creation of Blackstone, who also holds a ~$300MM convertible preferred stake in Tricon. AMH received a large initial investment from the Alaska Permanent Fund, with which it continues to manage a JV. However, this relationship appears far less meaningful than in the case of Invitation and Tricon.

Business Overview

Portfolio/Operating Performance

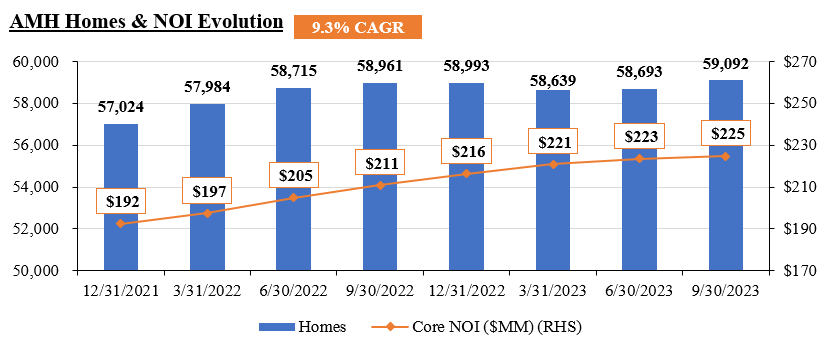

AMH owns 59,092 homes (n.b., including 700 held for sale) and manages another 2,936. Its top 20 markets account for ~95% of the book value of its real estate assets (n.b., 50,920 homes), and ~75% of these homes are located in the Sun Belt. Its average home is ~1,990 sqft and rents for ~$2,100/month.

AMH Top 20 Markets (AMH; Author)

The total home count has increased ~4% since Q4 '21, though AMH has been actively disposing of certain assets (n.b., "mid-3%" cap rate on dispositions in Q3 '23). Core NOI has grown at a ~9% CAGR over the same period.

{kind=link}

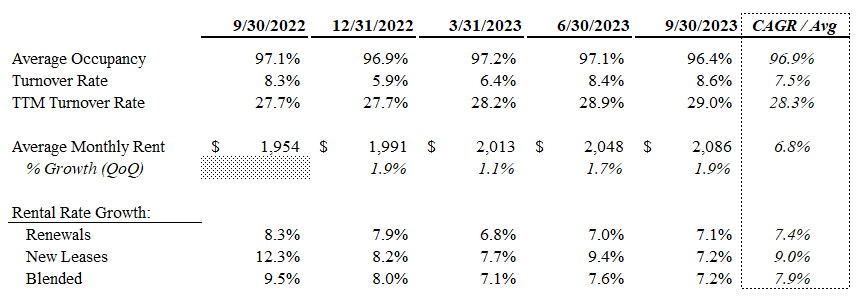

The performance of AMH's portfolio in recent quarters has been as strong as expected for an SFR platform. Occupancy has remained high at ~97%, with ~7% annualized AMR growth. The last 5 quarters' operating performance for the same store portfolio as of Q3 can be seen in the table below. It is interesting to note that AMH has seen much less deceleration in new lease rent growth than Invitation, despite having a slightly lower loss-to-lease (n.b., estimated at 5-7% vs 6-8% for Invitation and 12-15% for Tricon).

{kind=link}

Financials

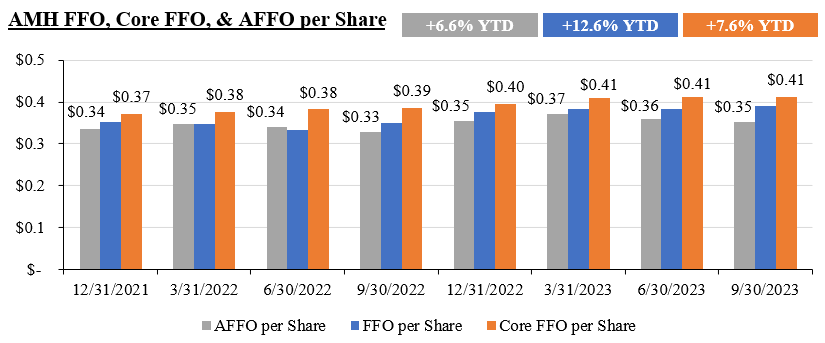

The chart below shows that, like Invitation, AMH has delivered mid to high single-digit FFO/Core FFO/AFFO per share growth through '22 and '23. YTD AFFO per share is up ~7% from the comparable period in '22 (n.b., ~13% for FFO and ~8% for Core FFO). This is a function of the solid operating performance discussed above and the REIT's predominantly fixed rate and long-dated debt profile, which insulated it from much of the impact of interest rate hikes.

{kind=link}

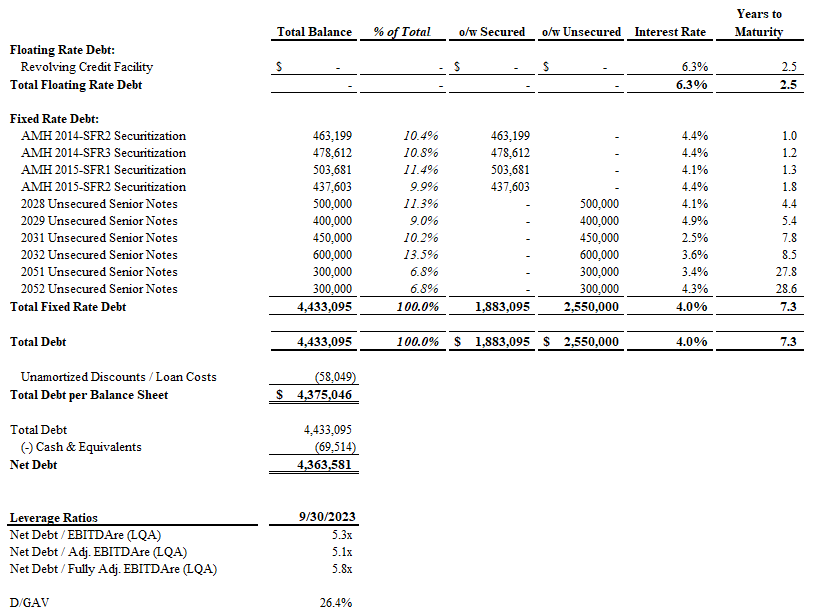

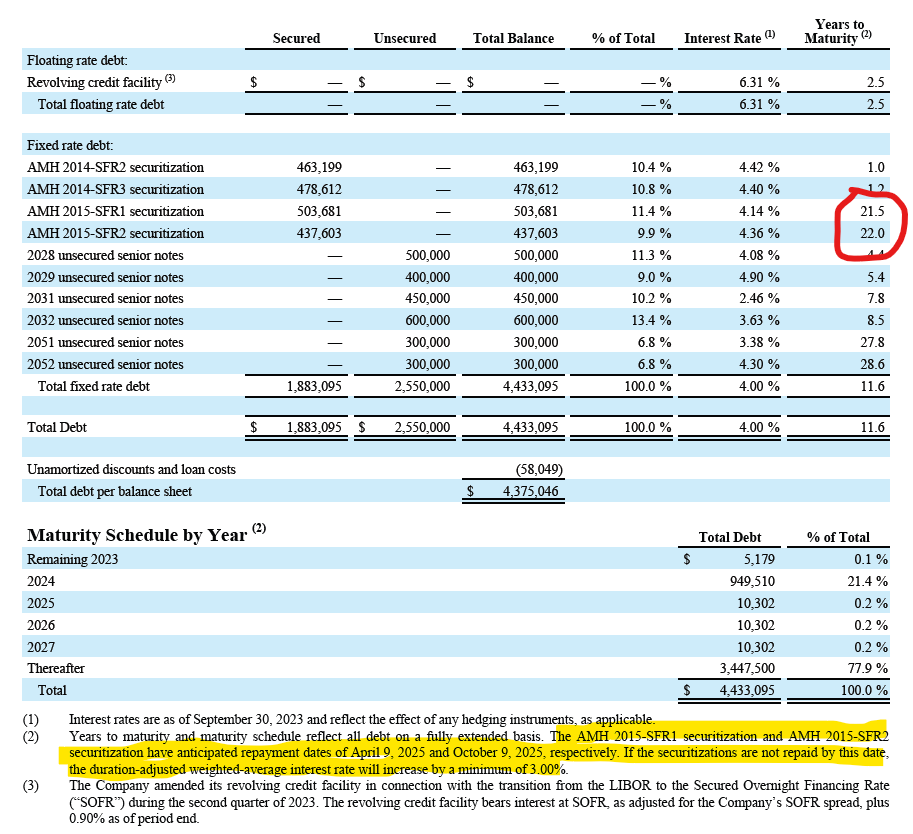

As we see below, 100% of AMH's debt is a fixed rate, and its average interest rate is 4.0%, slightly higher than Invitation at ~3.8% but below Tricon at ~4.5%. Leverage is ~5.3x EBITDAre and D/GAV is ~26%.

{kind=link}

I estimate the weighted average term to maturity for the debt to be ~7 years (n.b., ~5 years for Invitation and ~2.5 years for Tricon). Below, we can see that the reported WATM is ~12 years; however, in footnote 2, this assumes that the 2015-1 and -2 securitizations are fully extended. The anticipated repayment dates for these facilities are actually April and October 2025. If they are not repaid by then, the effective interest rate will increase by at least 300bps, resulting in a minimum rate of ~7.1% and ~7.4% for 2015-1 and 2015-2, respectively. AMH will not carry +7% debt just to report a longer WATM (n.b., Tricon recently refinanced a similar securitization for an effective ~5.9% rate), so I adjusted the WATM to reflect the anticipated repayment dates. Even with this adjustment, AMH still has the longest-dated maturity profile of the SFR peer set.

AMH Reported Debt Profile (AMH)

{kind=link}

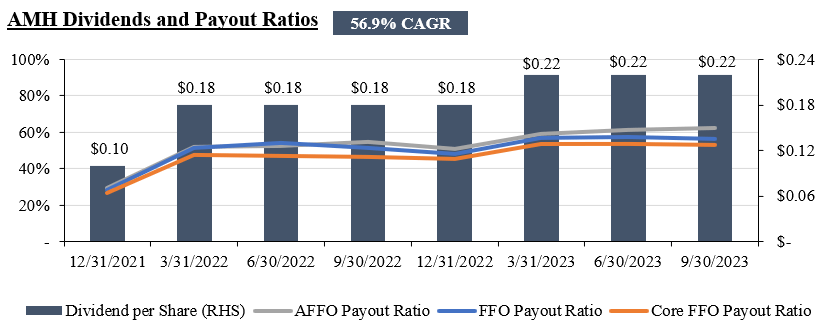

The combination of strong operating performance and well-structured debt profile has enabled AMH to raise its dividend twice in this period, +80% in Q1 '22 and +22% in Q1 '23 (n.b., ~57% dividend CAGR), while maintaining healthy ~50-60% payout ratios (vs ~60-70% for Invitation and ~40-50% for Tricon).

{kind=link}

Valuation

AMH currently trades at ~23x FFO, ~22x Core FFO, and ~25x AFFO (n.b., ~15% premium to my NAV estimate, ~5.4% implied cap rate).

AMH Valuation Summary (Author)

My NAV estimate of ~$31/share (n.b., implying ~13% downside) is based on a 6.0% cap rate (n.b., same cap rate as I used for Tricon and Invitation) and NTM NOI of ~$944MM (n.b., ~7% higher than LTM, ~6% implied CAGR Q3 '23 - Q3 '24). It also includes a positive adjustment of ~$45MM, my estimated value of the management business based on 8.0x LQA management fee revenue. This is identical to the property management and development multiple I used for Tricon , rather than the 12.5x asset management multiple. I took this approach as AMH's management business is far smaller and less developed than TCN's, and to implicitly account for the related overhead (n.b., using 8x results in a materially identical value as if I were to assume a similar margin to the rental business). This is also the same approach I used for Invitation.

While it could be argued that 5.4%-5.5% is an appropriate cap rate given Invitation's recent portfolio acquisition at that price, this still implies AMH is trading flat to NAV. It generally takes a lot for me to be comfortable paying full value for a REIT's NAV, let alone a premium. It can make sense when a REIT has a large acquisition pipeline, a significant mark-to-market opportunity, or some other such catalyst. AMH has ~13,000 lots optioned and scheduled for future delivery, a modest loss-to-lease of 5-7%. While these metrics should support strong growth over the next year, I do not see them as sufficient to overcome the ~15% premium to NAV.

Risks

Property Tax Expense Growth

In its Q3 earnings call , Invitation's management called out what it expects to be a material increase in property tax expense:

While the fundamentals that have favored housing are well known to us, we originally anticipated property tax millage rates in both Florida and Georgia would decline to at least partially offset some of the unprecedented home price appreciation that's occurred there. Based on the property tax bills we've received or expect to receive during the fourth quarter, that's not been the case and causes us to now expect full year same-store property tax expense growth of approximately 10% to 10.5%.

This is also a significant development for AMH, with Florida and Georgia collectively representing ~20% of the book value of its portfolio. If local governments in other jurisdictions follow suit, this could pose a serious risk to NOI margins.

Home Ownership Affordability Mean Reversion

US SFR operators are benefitting from a significant undersupply of housing and a large affordability gap favoring renting vs buying a home. The affordability gap is primarily a function of elevated home prices and high mortgage rates. Home prices surged during COVID as demand for space, particularly in less urban areas, soared. This was enabled by the low interest rates of '20 and '21. While home prices have normalized somewhat, there is still a wide bid/ask spread in many markets. Meanwhile, mortgage rates have exploded. In their Q3 earnings call, Invitation's management estimated that renting a home was ~$1,100 per month more affordable than buying in its markets (n.b., significant overlap with AMH's portfolio).

If sellers capitulate, causing home prices to decline and interest rates to fall (n.b., likely in this scenario as homeowner distress would correlate with a recession), this affordability gap may narrow, softening SFR fundamentals in the medium to long term.

Valuation

As discussed above, AMH is currently trading at a ~15% premium to NAV (n.b., or roughly at NAV under a more generous cap rate assumption). As a result, its performance should broadly track the underlying performance of its portfolio and the SFR market. Without a significant margin of safety, any adverse developments in the SFR market, such as those discussed above, pose a significant risk to the shares.

Catalysts

As there is no apparent undervaluation, I see few, if any, discrete catalysts for AMH. I expect SFR fundamentals to hold for the foreseeable future (though this could change quickly) and for AMH's shares to track its operating performance. The only credible catalyst I see is an acceleration in acquisitions. Of course, these acquisitions need to be accretive and likely require a significant correction in home prices. As discussed above, a home price correction would present challenges to AMH; however, buying homes at very low/distressed prices could help offset the resulting weakness in the rest of the portfolio.

Comparison to Tricon and Invitation

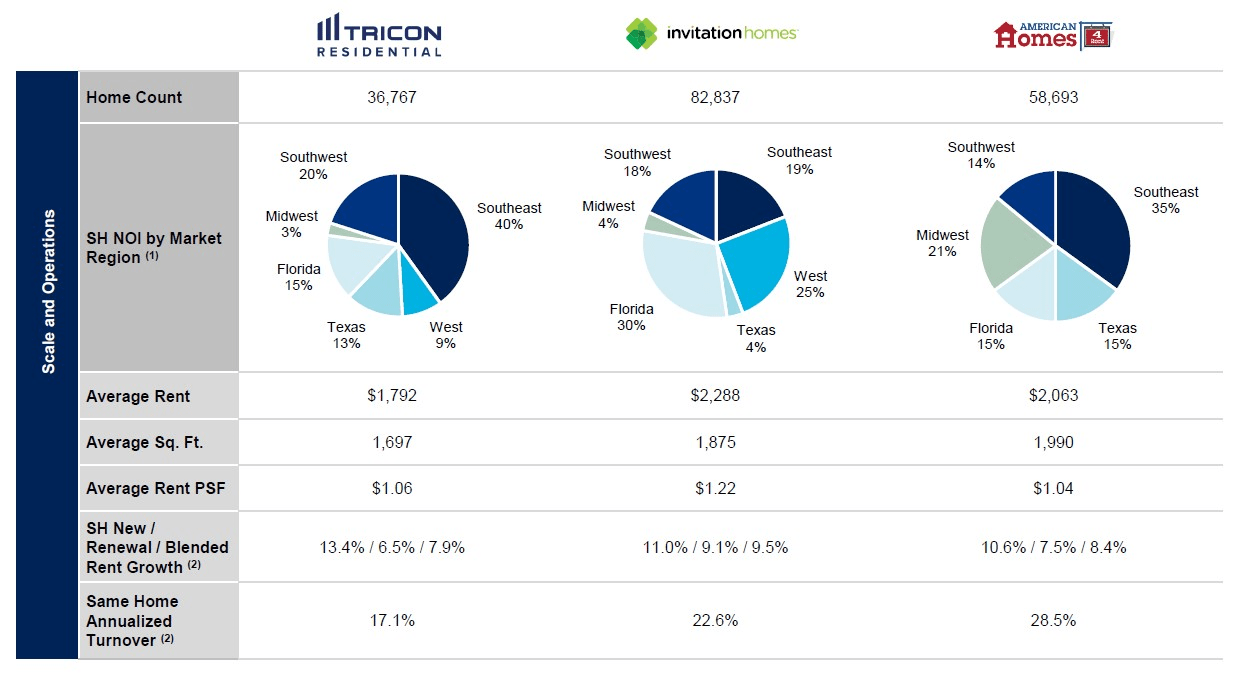

Invitation is the largest among the 3 main US SFR REITs (TCN, INVH, and AMH). Its average home size is significantly larger than TCN's but slightly smaller than AMH's. Its AMR is the highest of the 3, partly due to its higher exposure to the more expensive Western and Southwestern US markets.

{kind=link}

Based on my analysis of Tricon and Invitation, I see the below as the primary points of difference.

- Scale / Efficiency: Despite Invitation's far greater scale, AMH's NOI margins are slightly higher at (n.b., ~64% LTM average for AMH vs ~60% for Invitation and ~69% for Tricon). Some of this is likely due to Tricon's lower turnover rates, though it could also be a function of cost allocation. This is a point in favor of Tricon.

- Management Business: Tricon's Strategic Capital business is a much more significant component of its overall business and strategy than Invitation's or AMH's JV management agreements. This is positive for Tricon as it provides a lower-risk revenue stream and a slight diversification benefit. However, it complicates the business model, which might make it less attractive to investors seeking pure-play SFR exposure.

- Geographic Exposure: Tricon has ~10% points more exposure to the Sun Belt than Invitation and ~15% points more than AMH (n.b., ~90% for Tricon vs ~80% for Invitation and ~75% for AMH). This is a point in favor of Tricon.

- Leverage: This is the most significant difference between the three. AMH's leverage of ~5x is moderately lower than Invitation's (n.b., 5.5-5.7x EBITDAre) and significantly lower than Tricon's ~8-12x (see my Tricon report for details). AMH and Invitation have virtually no floating rate exposure and limited or no near-term maturities, while Tricon has ~27% floating rate exposure (n.b., though only ~7% considering interest rate caps, though some will expire early next year) and ~45% of its total proportionate debt matures in '24 and '25. Overwhelmingly, this is a point in favor of Invitation and AMH. The only way to spin this as a positive for Tricon is that it is better positioned for an outsized FFO/AFFO per share uplift when rates come down. I have also factored in an interest rate MtM adjustment for Tricon's upcoming maturities in my valuation.

As discussed above, I do not consider AMH's current valuation compelling. This is especially true with Tricon trading at a ~20% discount to my target price (n.b., despite the ~13% rally since my initiation report) with a mid-teens loss-to-lease, the imminent launch of its next JV, and a large development pipeline.

While I like the fundamentals of the US SFR market, I do not have enough conviction to make a pure market bet, which is exactly how I see AMH (and Invitation) at current prices. AMH and/or Invitation would have been the clear pick over Tricon heading into the recent rate hike cycle, with their largely fixed rate and long-dated debt profiles. However, with the market having already priced in AMH and Invitation's strength relative to Tricon, and the rate picture beginning to change, Tricon is my current preference in the SFR space.

Conclusion

I continue to like the SFR space, particularly in the US Sun Belt, for its attractive supply/demand dynamics and demographic tailwinds. Having now covered the 3 major players in the sector, Tricon remains my top pick, despite AMH and Invitation being more attractive from a fundamentals basis. Their revenue management seems much more aggressive than Tricon's, and their balance sheets are far superior. Both are much more of a pure SFR play than Tricon, with the latter having small but significant development, multi-family, and asset management businesses. However, the market has realized this and priced AMH and Invitation accordingly. As with Invitation, I am giving AMH a Sell rating purely for its valuation, with shares fairly priced at best. The yield is unappealing, and the price appreciation potential is inadequate to compensate for the risk profile.

For further details see:

American Homes 4 Rent: Too Expensive For Me