APEI - American Public Education: Diversified Segments Negatively Impacting Bottom-Line

2023-12-15 00:43:56 ET

Summary

- Since Q3 2023 earnings, the stock has increased by 72.92%, but the five-year trend shows a 66.08% decline.

- Revenue rises, but inconsistent bottom-line performance persists due to struggling Rasmussen University and Hondros College of Nursing segments.

- Cautious of declining enrollment, compliance issues, and profit variances between segments.

American Public Education, Inc. ( APEI ) is slowly improving its top and bottom line financials, as seen in its most recent Q3 2023 earnings report . Since posting the earnings in November, we can also see that the stock price has increased by 72.92% over the last month. If we take it back, we can see that the company has seen its stock lose 66.08% in value during the previous five years. Currently, the EV is much higher than its market cap and could be considered an opportunity at the current price if the company continues to improve and achieve what it has stated; namely, it foresees positive enrollment growth by mid-2024 and profitability across all four of its education segments. However, there are still critical obstacles towards this journey, which I will cover in this article. As I have yet to see a straightforward turnaround success story, I recommend a wait-and-see hold rating.

Five year stock trend ( SeekingAlpha.com )

{kind=link}

Company overview

American Public Education was founded in 1991, and it provides postsecondary education and career learning opportunities through both online and campus-based programs. The company has made efforts to adapt to the changing education industry, including acquiring Rasmussen University and GSUSA. However, it still faces certain challenges. Currently, the company operates through three segments: American Public University System, Rasmussen University, and Hondros College of Nursing. Although the company's revenue has grown due to these acquisitions, its operating expenses have also increased, presenting a notable downside to the company's bottom line.

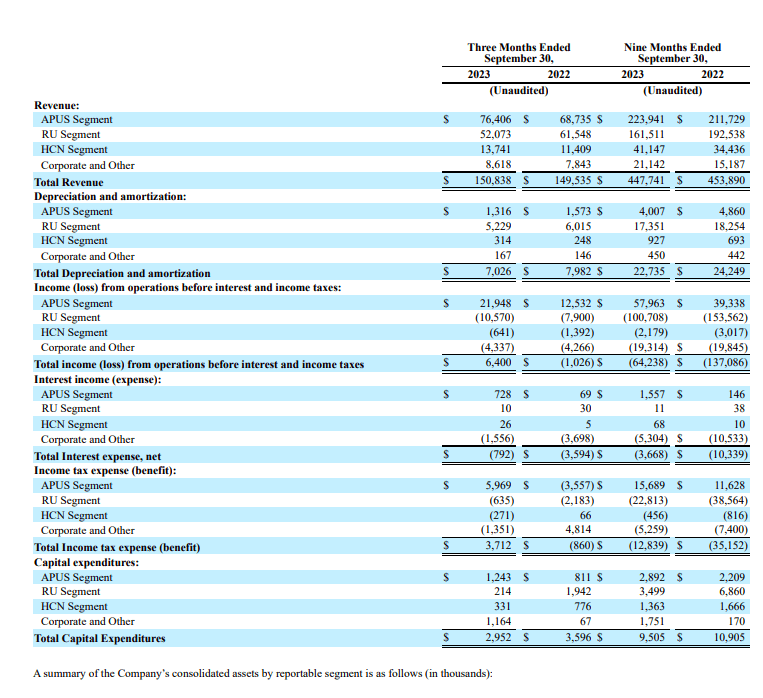

Financials by segment Q3 2023 versus Q3 2022 ( Sec.gov )

{kind=link}

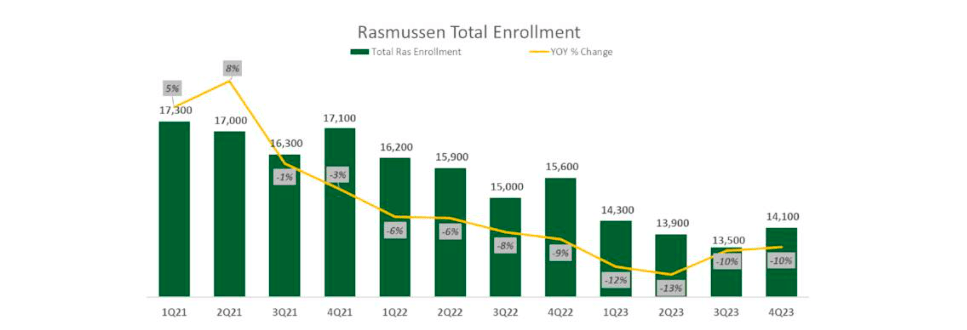

The financials for Q3 2023 versus Q3 2022 highlight Rasmussen University's, and to a lesser level, Hondros College of Nursing negative impact on the company's total bottom line. Cost adjustments, such as increased tuition and staff cuts across segments, were implemented. Rasmussen witnessed online enrollment growth but suffered a substantial decline in its ADN nursing program, leading to a 10% drop to 14,100 students. The declining enrollment is due to self-imposed enrollment caps due to lower NCLEX scores and operational challenges. The ADN program is currently operating at a negative margin of 10%.

{kind=link}

Another concern is the compliance with the Department of Education's 90/10 rule. In the past the company collected funds related to prior years, but uncertainties loom regarding changes in calculation methodology for the rule, which might impact compliance in the current and upcoming years.

The company has not yet established a guideline for 2024 , but it expects to see positive enrollment growth in the second half of that year. While diverse revenue streams can help create new growth and opportunities, we can also see that if these are not managed effectively, they can cut into the overall performance of the business. While losses have improved YoY, there is still a long way to go and plenty of challenges for the company to overcome prior to profitability across all of its segments.

Financial overview

The company has shown promising revenue growth over the past five years, but its bottom line has been inconsistent. In FY2022, the company reported losses for the first time in five years, with a negative non-GAAP EPS of $5.91. Although the expected EPS for FY 2023 is also negative, it would be an improvement at negative $3.43 per share.

Annual income statement ( Marketscreener.com ) Annual net income ( SeekingAlpha.com )

{kind=link}

Despite these figures, the company has maintained a positive trend in certain operational aspects. It has a TTM levered free cash flow of $14.02 million and $25.63 million in cash from operations. This positive cash flow positions the company to reinvest in its growth, appease investors, and settle debts. The company has initiated a $10 million share repurchase program, supplementing an earlier $8 million allocation announced earlier in the year.

Levered free cash flow ( SeekingAlpha.com )

{kind=link}

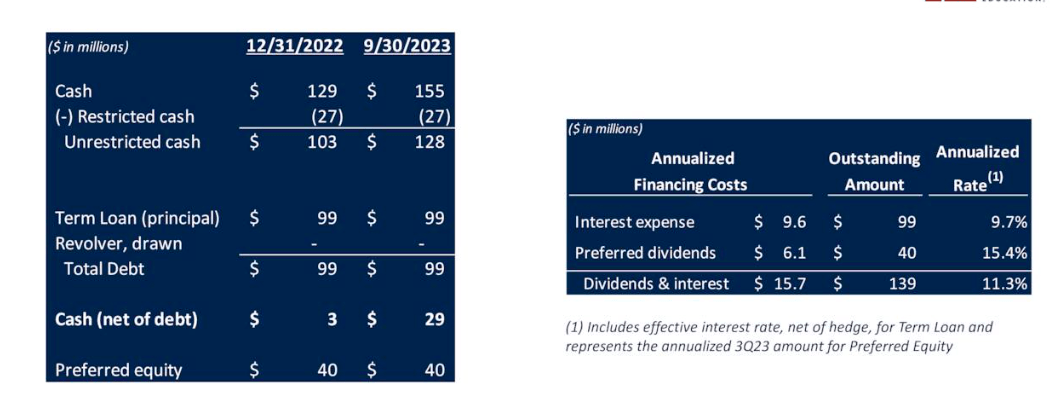

Moreover, the company has a total debt of $99 million. We can also see that the company displays enough liquidity to cover its short-term obligations, indicated by a quick ratio of 1.96 .

{kind=link}

Valuation

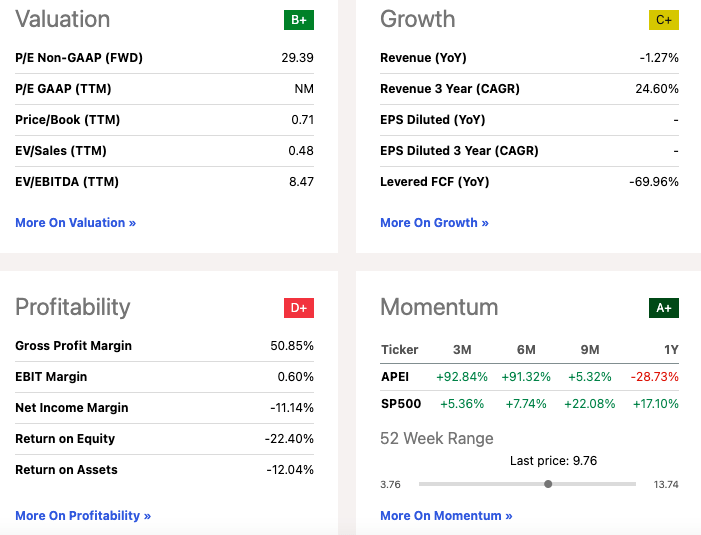

We can see that over time, the company's total value appears more substantial than its future potential when evaluating its EV of $287.72 million against a market cap of $167.08 million. This discrepancy could reflect investor concerns over declining earnings, notably impacting the stock, which has depreciated by 66.08% in the past five years. Furthermore, the small market cap coupled with a high EV-to-market-cap ratio signifies higher indebtedness than available cash, elevating the investment's risk profile. Although Wall Street analysts rate it a 3.75 Buy, considering the limited coverage, this assessment requires caution. Yet, the stock might appear appealing due to its notably low price-to-book ratio of 0.71, suggesting investors pay less than the company's intrinsic value. However, the challenges to improve the company's profitability across two of the three segments remain a concern on both the cost-cutting side and the growth side, which has been tackled by increasing tuition fees.

{kind=link}

Final thoughts

American Public Education showcases signs of a potential turnaround following its Q3 2023 report and the subsequent stock surge. Still, investors should be cautious of its five-year stock decline and ongoing challenges for the company to reach profitability and increase its enrollment numbers. While the company aims for mid-2024 enrollment growth and profitability, hurdles like Rasmussen's struggling ADN nursing program, regulatory compliance uncertainties, and two unprofitable segments raise concerns. Therefore, I recommend a wait-and-see hold until we see a more evident growth and profitability path.

For further details see:

American Public Education: Diversified Segments Negatively Impacting Bottom-Line