CTVA - American Vanguard: Current Pessimism Represents A Good Opportunity For Long-Term Investors

2023-09-28 07:57:35 ET

Summary

- Revenues are declining after a strong 2021 and 2022 as customers are emptying their inventories.

- Debt is increasing as the company keeps accumulating inventories.

- Profit margins remain depressed, but related headwinds are temporary.

- Increased interest expenses are putting extra pressure on the balance sheet.

- This represents a good opportunity for long-term investors as the company is prepared to navigate current headwinds.

Investment thesis

American Vanguard (AVD) is currently facing a delicate situation, which has caused a share price decline of 71% from all-time highs. Although the coronavirus pandemic did not significantly affect operations in 2020, profit margins have been negatively impacted in recent quarters due to the subsequent higher production, labor, and transportation costs, as well as supply chain issues that caused disruptions in the production of higher-margin products.

Despite the recent deterioration in margins, sales increased significantly in 2021 and 2022, which caused an increase of over 50% in the share price in 2022, but this trend has reversed in 2023 as revenues declined year over year in both the first and second quarters as customers are destocking their inventories. This destocking process is understood, in part, by recent interest rate hikes, which have increased the cost of carrying debt. Therefore, the company's customers are emptying their inventories in order to reduce their debt levels and manage smaller inventories. Although volumes should eventually recover, the company's debt is currently higher than usual as it holds unusually high inventories, so interest expenses have skyrocketed to levels that, although not excessively worrying thanks to the long-term profitability profile of the company, put additional pressure on a balance sheet that is already facing the effects of contracted margins as the company reported negative net income in the second quarter of 2023.

Still, I strongly believe that the recent share price decline represents a good opportunity for long-term investors as the company holds more inventories than long-term debt, and the management plans to reduce debt levels significantly once demand returns to normal. Furthermore, the company has been profitable over the years and the dividend cash payout ratio has historically been very low, so now that supply chain issues are things of the past, the company should be able to start generating enough cash from operations on its own and accelerate debt reduction.

A brief overview of the company

American Vanguard is a global manufacturer of chemical, biological, and biorational products for agricultural, commercial, and consumer uses. The company was founded in 1969 and its market cap currently stands at $319 million as it employs over 800 workers.

{kind=link}

American Vanguard's strategy is clear. It is an agrochemical company that acquires brands and formulations from third-party companies to include them in its product portfolio while launching its own products through its own R&D efforts. As of now, it has over 1,000 product registrations in 56 nations worldwide, and the company keeps acquiring and launching new products, which so far has translated into growing revenues over the years.

Currently, shares are trading at $10.87, which represents a 70.91% decline from all-time highs of $37.39 on September 24, 2012. This drop responds to profit margins that have contracted as a result of increased production, labor, and transportation costs, in addition to supply chain issues and declining volumes as revenues declined year over year in the first and second quarters of 2023 due to customer destocking. To all this, we must add the rising interest rates, which have caused a significant increase in interest expenses in recent quarters at a time in which the company finds itself with an unusually high debt derived from the acquisitions it has carried out in recent years. Also, this debt level has increased even more than expected as a result of a high accumulation of inventories.

Latest acquisitions

The company has expanded over the years thanks to acquisitions, which have allowed it to expand its product portfolio. Below I will summarize the most recent ones.

In November 2018, the company announced the acquisition of Tyratech (until then, it owned 35% of Tyratech's shares), a manufacturer of non-toxic insecticides and green solutions for pest control, and a few months later, in January 2019, it also acquired Agrovant and Defensive , two Brazilian suppliers of crop protection products and micronutrients.

In December 2019, the company acquired four herbicide brands from Corteva Agriscience (CTVA), including Classic, First Rate, Hornet, and Python, and in April 2020, it acquired 8% of the total shares outstanding of Clean Seed Capital Group (CLGPF). A few months later, in October 2020, the company also acquired AgNova , a manufacturer of specialty crop protection and production solutions for agricultural and horticultural producers and selected non-crop users. During the same month, it also acquired Agrinos , the manufacturer of High Yield Technology, which increases crop yield, improves soil health, and reduces the environmental footprint of traditional agricultural practices. Agrinos has 50 patents issued and nearly 100 pending worldwide.

In May 2021, the company announced the acquisition of rights of Envoke in the United States from Syngenta Crop Protection. Envoke is a post-emergent herbicide for use in cotton, sugarcane, and transplanted tomatoes for control of certain broadleaf weeds, sedge, and grass weeds delivering effective control of many troublesome weed species, including many of those missed by glyphosate, and after a pause, in January 2023, it also acquired BioMop-Plus and DrainGel , two products that are used by restaurants, hotel kitchens, and institutions that have persistent drain and fruit fly infestation, from American Bio-Systems.

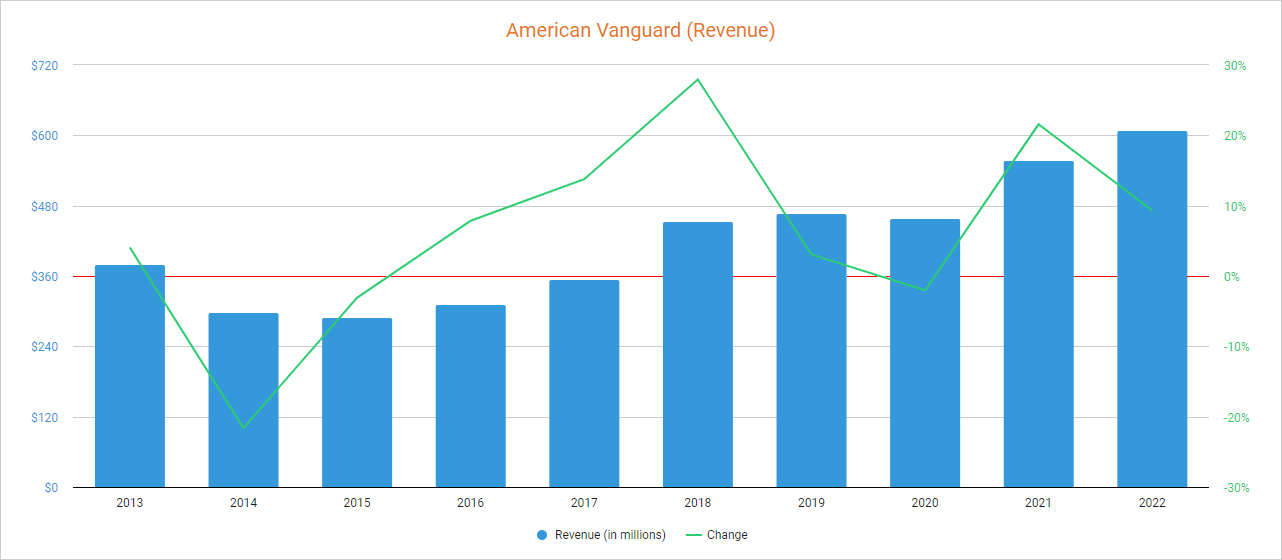

Revenues are stabilizing after a strong 2021 and 2022 as customers are destocking their inventories

Over the years, and largely thanks to the acquisition of new companies and formulas, the company has managed to increase its sales at very acceptable rates as they doubled from 2014 to 2022. In this regard, 2021 and 2022 were two strong years as revenues increased by 21.58% and 9.31% respectively.

{kind=link}

Despite this, the trend has changed in the first half of 2023 as revenues declined by 16.52% year over year during the first quarter and by 10.40% (also year over year) during the second quarter as customers are destocking their inventories in order to clean up their balance sheets in the face of the recent increase in interest rates. Nevertheless, the management expects significant improvement during the second half of 2023 as it expects net sales to stand at $615 to $625 million for the full year 2023 (which represents a 1% to 3% increase compared to $610 million in 2022), boosted by tighter customer inventories and supply chain improvements.

Using 2022 as a reference, 60% of the company's revenues take place within the United States, whereas 40% come from international operations, which means the company enjoys wide geographical diversification, and although sales are significantly above pre-pandemic levels, the sharp decline in the share price experienced in recent years has caused the P/S ratio to plummet to 0.555, which means the company currently generates $1.80 in revenues for each dollar held in shares by investors annually.

This ratio is 56.09% lower than the average of the past 10 years and represents a 74.22% decline from decade-highs of 2.153 reached in 2017, which reflects the current pessimism among investors as they are placing much less value on the company's sales not only due to expected sales stagnation and unusually high interest expenses but also due to the company's lower capacity to convert said sales into actual cash.

Margins keep deteriorating, but headwinds are temporary

Before the coronavirus pandemic, the company used to enjoy a gross profit margin of ~40% and an EBITDA margin of ~12%, but coronavirus-related disruptions and subsequent inflationary pressures, supply chain issues, and higher labor and transportation costs have recently caused a margin contraction as the trailing twelve months' gross profit margin currently stands at 35.42% and the EBITDA margin at 7.68%, and ongoing expense management initiatives are failing to stabilize margins as now declining volumes is added to the equation. This decline has been significant as supply chain issues caused the unavailability of higher-margin herbicides in recent quarters, and generic price competition in Central America and Brazil is putting even more pressure.

In this regard, declining volumes have recently caused a further margin contraction as the company reported a gross profit margin of 32.31% and an EBITDA margin of 7.68% during the second quarter of 2023, although some improvement can be expected in the coming quarters as higher-margin herbicides are beginning to become available again while inflationary pressures appear to be starting to subside. Also, declining customer inventories should eventually push them to start purchasing new products again, which should help volumes stabilize.

This margin recovery will be important for the overall picture to improve because, if the company manages to improve its profit margins once the macroeconomic outlook improves and customers finish adjusting their inventories, it should be able to begin reducing its debt levels, which should significantly improve long-term prospects and allow for new growth initiatives.

Debt is manageable despite increased interest rates

Over the years, the company has managed to keep debt at sustainable levels thanks to a careful M&A strategy, but debt exposure is starting to put some pressure on operations as long-term debt increased to $161 during the second quarter of 2023 compared to $101 million during the same quarter of 2022. Furthermore, cash on hand is low in comparison at $14.63 million.

This recent increase in long-term debt has caused a significant increase in interest expenses, which has been driven even further as a consequence of increased interest rates as the trailing twelve months' total interest expense currently stands at $7.68 million, and the management expects paying down some debt by the end of 2023 in order to reduce its cost.

Nevertheless, the company reported a total interest expense of $3.21 million during the second quarter of 2023 as interest rates increased to 6.9% (compared to 2.2% a year ago), which means it is expected to pay around $13 million per year at current rates and debt exposure. Luckily, inventories have increased along long-term debt and currently stands at $238 million, which is significantly higher than the long-term debt of $161 million.

This means that the company should be able to generate strong cash from operations in the foreseeable future, especially once customers have their inventories tighter, and the management expects to start selling part of these inventories during the fourth quarter of 2023 or the first quarter of 2024. In this regard, long-term debt should start declining as soon as demand stabilizes, and now that higher-margin herbicides are again available, improved margins should help generate positive cash from operations with which accelerating debt reduction.

The dividend is safe as the cash payout ratio has historically been very low

After a significant cut in 2016 to $0.01 per share and quarter (from $0.05), increased revenues in recent years have allowed the dividend to be tripled to $0.03 per share. The latest increase was announced in December 2022 when the management raised the quarterly dividend by 20% to $0.03 per share.

This leaves investors with a dividend yield of 1.10% which, despite being very low from a dividend investing perspective, allows the company to invest in other items equally important for investors' interest (R&D, acquisitions, debt reduction, and share buybacks) as the cash payout ratio has historically been very low. In the table below, I have calculated the company's ability to cover the dividend by calculating what percentage of the cash from operations it has used each year to cover dividends paid and interest expenses.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| -$34.1 |

| $78.6 |

| $46.4 |

| $59.0 |

| $11.7 |

| $9.6 |

| $90.3 |

| $86.4 |

| $57.1 |

| Dividends paid (in millions) |

| $5.7 |

| $1.1 |

| $0.6 |

| $1.6 |

| $2.2 |

| $2.3 |

| $1.2 |

| $2.4 |

| $2.8 |

| Interest expense (in millions) |

| $3.1 |

| $2.6 |

| $1.6 |

| $1.9 |

| $4.0 |

| $7.2 |

| $5.2 |

| $3.8 |

| $4.1 |

| Cash payout ratio |

| - |

| 4.71% |

| 4.74% |

| 5.93% |

| 52.99% |

| 98.96% |

| 7.09% |

| 7.18% |

| 12.08% |

As one can see, the company has allocated a very small portion of cash from operations to cover the dividend and the cost of debt, which has allowed year after year to invest large sums of cash in the business as the trailing twelve months' capital expenditures currently stands at $15.07 million.

Despite all these expenses, the company has the ability to steadily improve its balance sheet in normal years, but the trailing twelve months' cash from operations is currently negative at -$12.3 million due to margin contraction and increasing inventories. During the second quarter of 2023, the company reported cash from operations of -$55.2 million as unearned revenue decreased by $42.9 million and inventories increased by $18.5 million. In the same period, accounts receivable decreased by $14.4 million, and accounts payable increased by $4 million, and the company reported a net income of -$1.1 million. Nevertheless, this is expected to improve in the short term now that the company is selling higher-margin herbicides again thanks to supply chain improvements, and lower customer inventories should also help in volume growth, which should also deliver improved profit margins due to improved manufacturing efficiency. Therefore, I consider that the dividend is relatively safe as headwinds are poised to start subsiding in the foreseeable future, which should enable positive cash from operations and net income. Despite this, the management could decide to pause share buybacks until operations improve.

Taking advantage of lower share prices through share buybacks

Since 2022, the company has started buying back its own shares in order to reduce the total number of shares outstanding, which should allow for per-share improved metrics in the long run if these continue. Thanks to these recent repurchases, the total number of shares outstanding declined by 3.23% in the past 3 years.

On May 25, 2023, the company announced a $15 million share repurchase program, and share repurchases are expected to continue taking place in the long run as long as the cash payout ratio remains low once headwinds subside. Despite this, the management could pause these buybacks in the short term as cash from operations is currently negative and cash preservation should be a top priority given ongoing headwinds.

Risks worth mentioning

In the long term, I consider American Vanguard's profile to be relatively low as the company is profitable in normal years and the management seems to have a clear vision of the future they want for the company, but despite this, there are certain risks that I would like to highlight in the short and medium term.

- If demand does not recover soon, the company could continue with reduced volumes in the short and medium term, which would make it difficult to recover profit margins despite recent supply chain improvements.

- The company could have difficulty emptying its inventories in a low-demand scenario, which could force it to increase its debt levels even further. This would lead to an increase in interest expenses, which would put even more pressure on the balance sheet.

- If the company fails to significantly increase sales of higher-margin herbicides now that they are back in stock, margins may not recover as much as expected.

- If current headwinds do not ease in a relatively short period of time and profit margins remain depressed, the company could decide to cut or even cancel the dividend in order to preserve as much cash as possible.

Conclusion

American Vanguard's current share price decline reflects strong pessimism among investors, and this is in my opinion justified as headwinds have been hitting the company's operations one after another since the coronavirus pandemic back in 2020. In the last few years, the company has faced increased production, labor, and transportation costs. Supply chain issues then reduced the availability of higher-margin products, which added even more pressure to profit margins. As if that were not enough, customers are now emptying their inventories, which has caused a decline in volumes that has resulted in further margin contraction and an increase in long-term debt due to higher inventories. Furthermore, this increase in long-term debt has come at a time marked by much higher interest rates, with which interest expenses have also skyrocketed.

But despite all these headwinds, it seems that light is beginning to be seen at the end of the tunnel. First of all, it's been two quarters in a row of reduced revenues, which suggests that customer destocking is in a relatively advanced phase. Eventually, these volumes should recover as customers find themselves comfortable with their adjusted inventories. Additionally, the company is manufacturing higher-margin products again as supply chain issues recently eased, which should drive some margin expansion. Regarding debt and increased interest expenses, the company has inventories significantly higher than long-term debt, which significantly reduces the risk that debt poses as they should allow the company to report stronger cash from operations as soon as demand picks up again, and net income is currently negative but not at catastrophic levels, which means a slight margin expansion should allow the company to report positive net income and positive cash from operations with which accelerate debt reduction.

In short, I consider that the temporary nature of the current headwinds, given their direct link to the macroeconomic context, together with the profitability profile that the company has shown in normal years, make the current pessimism among investors a good opportunity for long-term investors with enough patience to wait for American Vanguard's picture to improve.

For further details see:

American Vanguard: Current Pessimism Represents A Good Opportunity For Long-Term Investors