WTRG - American Water Works: Down 18% In 2022 Yet Still Richly Valued

Summary

- Utilities generally outperformed during the 2022 bear-market, but American Water Works' stock was down 18%.

- Despite the drop, AWK still trades at a rather rich TTM P/E = 21x and a forward P/E = 34x.

- However, strong federal water infrastructure support, growth by acquisition, and expectations for margin expansion are positive tailwinds for the company going forward.

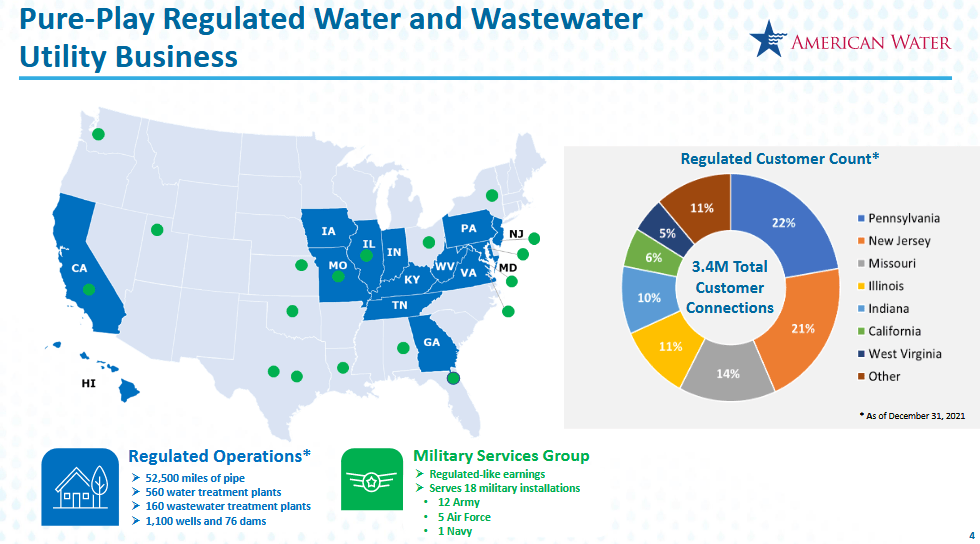

American Water Works ( AWK ) provides water and wastewater services to approximately 1,700 communities across 14 states that serve approximately 3.4 million residential and commercial customers. The stock had a tough 2022 (see below), but while FY22 revenue is expected to dip slightly on a yoy basis (~4%), earnings per share are expected to show a nice increase for full-year FY22. And while its projected CAGR over the next five years (~8%) is generally above peers, and despite the big stock decline last year, AWK appears fully valued, in my opinion.

Investment Thesis

Like many utility companies, AWK has a relatively low-risk profile given the fact that it generates the majority of revenue and income from relatively stable and regulated water and wastewater services (see below). However, as you can see from the above graphic, the company's returns in 2022 trailed that of the SPDR Select Utilities ETF ( XLU ) by ~19%. Could the stock price drop be an opportunity for investors going forward? Let's take a closer look.

{kind=link}

Source: September Investor Presentation

Earnings

AWK reported Q3 earnings at the end of October, and the results beat consensus estimates on both the top and bottom lines. Highlights from the report included:

- Q3 GAAP EPS of $1.63/share was an $0.11 beat, and $0.10/share better than Q3 of last year.

- Revenue of $1.08 billion (-0.9% yoy) beat by $10 million.

- FY2023 earnings guidance was for a range of $4.72-$4.82 per share.

- Guidance for long-term EPS CAGR, and dividend growth expectations, were both in the range of 7-9%.

Susan Hardwick, AWK President and CEO, commented on the quarter:

We made great progress in executing our regulatory and acquisition strategies these last few months. Achieving settlements in the rate cases in our two largest jurisdictions, New Jersey and Pennsylvania, is a constructive step forward for our customers and our operations in each state. We also announced a few weeks ago an agreement to acquire assets serving another nearly 15,000 wastewater customers in western Pennsylvania. We look forward to completing that transaction in 2023.

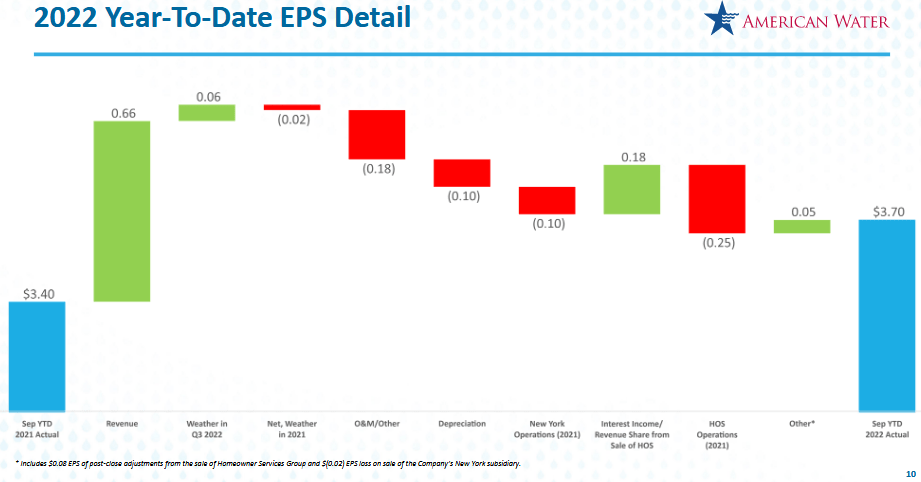

As you can see from the following graphic, YTD EPS performance over the first nine months of this year is up significantly over last year:

{kind=link}

AWK

Source: AWK Q3 Presentation

In addition, AWK continues its strategy of growth through acquisitions. Through the first nine months of the year, AWK added 65,300 new customer connections via 15 closed acquisitions across 6 states (primarily Missouri and Illinois) for $308 million.

Going Forward

Earlier this month, AWK reached rate-case settlement with the state of Pennsylvania, as well as in Illinois . These settlements reduce uncertainty and, in general, are positive developments for AWK moving forward. Margin could rise up to 200 basis points next year as compared to FY22.

In addition, AWK has agreements in place to - once the deals are closed - add another 21,600 new customer connections via 29 acquisitions in nine states for an additional $118 million. The point being, AWK's capex growth pipeline is strong and relatively impressive.

Valuation

The midpoint of FY23 EPS ($4.77/share) compares to expected EPS of $4.44/share for this year, implying EPS yoy growth of 7.4%.

However, the midpoint of FY23 EPS equates to a forward P/E = 32x based on the closing price last week of $152.42. In my opinion, that's a relatively frothy P/E in comparison to the expected 7.4% EPS growth next year.

AWK's current $0.6550/share quarterly dividend equates to a yield of only 1.72%, which is significantly below the 2.92% investors can get from the XLU Utilities ETF (let alone around 4.5% from 18-24 month CDs). In comparison, direct peers like American States Water ( AWR ) and Essential Utilities ( WTRG ) currently sport yields of 1.72% and 2.41%, respectively.

Risks

American Water has some important differences from its electric and gas utility peers: Its capital projects, in general, are much smaller on average than those in the electric and natural gas industries. Another difference is that AWK's greenhouse gas emissions footprint is very small compared to most other publicly traded electric and gas utilities. In aggregate, both of these are relative risk migrators as compared to the utility industry as a whole.

Rising interest rates and increased chemicals costs could put pressure on margins going forward due to AWK's growth-by-acquisition strategy. In addition, as mentioned earlier, investors can currently get significantly higher income from relatively short-term CDs, or even the XLU ETF. This is likely to put a cap on the stock's appreciation potential in 2023 given that the Fed is still set to raise interest rates further.

Summary and Conclusion

While AWK's high-quality low-risk profile is relatively attractive given the current macro-economic challenges, the stock looks fully valued in my opinion. That being the case, I find it - and the yield - to be relatively uncompelling in comparison to alternatives, including plain old two-year CDs and/or the XLU ETF - which is obviously over-weighted in electric utilities and therefore not really a direct apples-to-apples comparison (see XLU: Suddenly, Utilities Rock! ).

I rate AWK a HOLD and suggest investors wait for a significantly lower entry point in the coming year before dipping their toes in the "water." I would get interested if the yield rose to, say, 2% - at which point the total returns potential of the stock would be more compelling.

I'll end with a five-year total returns comparison between AWK and the XLU ETF and note that AWK has outperformed the XLU ETF by ~24.5%:

For further details see:

American Water Works: Down 18% In 2022, Yet Still Richly Valued