AWK - American Water Works: No Thanks Too Risky For Me

2023-12-09 05:16:02 ET

Summary

- US water utilities face structural risks, including lack of affordability, infrastructure investment needs, potable water availability as a human right, and liability risks.

- Affordability of water is a significant issue, with prices increasing by 80% between 2010 and 2018 and many low-income residents facing high water costs.

- The Biden Administration's plan to mandate lead pipe replacement poses a significant cost burden on water utilities, with an estimated $30+ billion shortfall.

In December 2020, SA published an article outlining my concerns with publicly traded US water stocks, titled The Growing Risk for Regulated Water Investors . In Sept 2022, I penned another article, Algonquin Power Is The Only Water Utility I Own , reiterating the longer term, structural hazards for water utility stocks. The 2022 article advocated reducing the risk of pure water utility exposure by investing in the industry as part of a larger company or a component of an ETF. Algonquin Power ( AQN ) is the only utility I own with exposure to the water business, but AQN has fallen into severe hard times with its non-water utility business. The latest water industry news adds additional risks not identified in 2020 and 2022, reinforcing my belief that investors should continue to shy away from US water utilities.

The unique attributes of investing in water utilities have offered attractive and profitable selections for over 20 years. Beginning in the mid-1990s, US water trends was a favorite investment topic, and occupies a chapter in each of my stock selection process and personal finance books published by McGraw Hill in 2000 and 2002. However, post-Flint water crisis in 2015, I did an about-face and have avoided the water utility segment, except as small part of a larger utility, but even that is questionable as I believe AQN should shed its Liberty Water business, which comprises 20% of revenues, to further pay down debt.

The negative outlook is not from a lack of profitability or a lack of opportunity in the roll-up nature of US water utility growth, as there are currently 148,000 municipal water districts. Unfortunately, the negative trends are not a company-specific issue, but rather are structural in nature for the entire industry.

The unique risks associated with water utilities fall into several different categories. Negative water trends include a lack of affordability, huge investment needs to upgrade water pipe networks, water availability as a human right, and Flint-like financial liability risks. Now, investors must add the likelihood of a federal government mandate to replace all lead service water pipes over the next 10 years. While the federal government will subsidize some of the costs, there is a pending tens-of-billions-of-dollar shortfall that will rest on the shoulders of the utility provider - both municipal and investor owned.

Affordability of water - In 2020, Consumer Reports and the Guardian published a detailed study on water affordability. It found in the 12 US cities reviewed, the price of water and sewer service increased by 80% between 2010 and 2018. The study reported 40% of residents in some cities live in neighborhoods where water costs are classified as "unaffordable", or more than 4% of disposable monthly income. As of 2018, almost three out of every ten low-income residents lived in an area where the average water and sewer bill cost more than 12% of household disposable income. In 2023, Bluefield Research concluded that in 50 of the largest U.S. metropolitan areas, monthly household water and sewer bills averaged $121, based on typical US household consumption and the combined bill has increased by 56.2% since 2012.

According to Bluefield Research, there is a wide disparity of average monthly water and sewer bills based on location. For example, typical monthly water bills range from a low of $20 in San Antonio, TX, to a high of $121 in Portland, OR. Monthly sewer bills range from a low of $11 in Long Beach, CA, to a high of $170 in Seattle, WA. Forbes reported in early 2023 on water affordability and the geographic disparity. California has the highest monthly water-only (no sewer) bill at $77 and Wisconsin and Vermont are tied for the lowest at $18.

An exceptionally large operating cost for a water utility is their electricity bill. Mechanical pumping driven by electric motors is a major component of maintaining pressure throughout the water and sewer piping systems. The EPA estimates electricity costs often make up 25% to 30% of a water and sewer utility's total operation and maintenance costs. According to Utility Dive magazine and the U.S. Bureau of Labor Statistics, the average consumer cost of electricity spiked 14.3% in 2022 alone. Water customers and investors should expect to see continuing upward pressure on pricing, making water affordability for many in the US a significant issue, and a structural risk for the industry.

Ballooning costs of water infrastructure investment - There is a water main break somewhere in the US every two minutes, and the American Society of Civil Engineers estimates 6 billion gallons of treated water is lost each day, sufficient to fill over 9,000 swimming pools. ASCE estimates there are 240,000 water main breaks annually in the US. The City of Baltimore reports 1,000 water pipe and main breaks a year, or almost three a day. According to the Pew Research Group, the EPA in 2021 estimated the 20-year cost to upgrade the nation's potable water infrastructure at $625 billion. Most of that expense (68%) will be required to maintain and improve transmission and distribution systems, compared to 13% for storage and new sources of water. NY alone has identified over $40 billion in water infrastructure improvements required over the next 20 years.

These are not new numbers. What is alarming is the ballooning estimates of the total 20-yr cost for US water infrastructure maintenance and improvements. The EPA periodically issues Drinking Water Infrastructure Needs Survey and Assessment report and the 2022 report is the 7th update since 1995. In 1995, the initial report estimated the 20-yr investment needs for drinking water infrastructure upgrade and maintenance at $292 billion in 2021 dollars, which is adjusted for inflation. The 2021 report estimates the 20-yr investment needs have ballooned to $625 billion, in 2021 dollars. Over the past 30 years, in constant dollars, the investment needed to maintain distribution of potable water in the US has more than doubled.

Potable water availability is a basic "human right". Over a decade ago, the United Nations General Assembly approved a resolution approving potable water and sanitation as a "human right". As such, governments should guarantee all people have access to potable water and sanitation service. However, this resolution has not created a groundswell of activity as there are still millions of people around the world without affordable access to drinking water and sanitation services.

For investors in the US water industry, there is not much current impact of the movement to classify water as a right. However, as water affordability and lead pipe leaching become a larger issue in the US, the "human rights" aspects of potable water availability will begin to be a more frequent topic. While not as prominent a risk as others, the human rights aspect of US potable water and sanitation will become a serious topic as costs of providing these services continue to escalate.

Flint-like liability. We need not rehash nor retry the lead leaching problems in Flint, Michigan starting in 2014. The Flint water crisis was precipitated by a state-appointed emergency manager's approval of the switch of drinking water supply from Lake Huron to the Flint River to save money. However, the switch also included the discontinuation of previous treatment and purification processes. Without specific chemical additives to keep lead from leaching out of service pipes, the river water corroded city pipes and prompted a citywide water crisis. It is sufficient to say that managerial decisions at the municipal Flint Water District created an environment for increased leaching of lead into the drinking water from lead supply pipes from the street to residential homes. For water utility investors, the important aspect is the costs associated with the Flint lead pipe crisis. The state of Michigan spent $87 million for replacement of lead and galvanized steel service lines in Flint. In addition, in 2023, the State of Michigan agreed to a court settlement exceeding $626 million in legal settlements with Flint residents, paid by the State of Michigan. More than 50,000 people have registered to file claims.

While not to downplay the severity of lead poisoning, especially in children, it is critical for water utility investors to appreciate the liability risks associated with providing water service. The single Flint incident settlement costs exceed $650 million, or 14x the combined market capitalization of the top 9 publicly traded water utilities listed below and represents 25x the market cap of American Water Works ( AWK ), the largest in the industry.

Mandating lead pipe replacement . The Biden Administration is working on new EPA regulations that will mandate all lead service pipes be replaced over the next 10 years. Known as the Lead Service Line Replacement LSLR program, the plan is currently under review and open for public comments. The program mandates both public and investor-owned water providers to identify all lead service lines by Oct 16, 2024. The new regulation also reduced the current lead action level from 15 µg/L to 10 µg/L, matching the Euro action level and higher than the Canadian action level of 5 µg/L. Upon testing levels above the new standard, the utility will be required to begin replacing lead service pipes in their jurisdiction.

Again, while an admirable goal, this issue for investors becomes one of cost for US publicly-traded water utilities. The EPA estimates there are 9.2 million households, ~7% of US households, and upwards of 400,000 schools and childcare centers with lead pipe exposure and has set a target cost analysis of $45 billion for replacement of all lead service pipes in the US. The average cost of lead pipe replacement is ~$4,500 per installation (2023 dollars), with costs ranging from $1,200 to $12,000 for each job. The 2021 Infrastructure Investment and Jobs Act sets aside $15 billion for both replacement of lead service pipes and removal of lead paint. EPA administrator Michael Regan has stated these funds will be depleted by 2028.

So, who gets the honor of paying the $30+ billion not currently funded by taxpayers? Radhika Fox, head of the EPA Office of Water has been quoted as saying, "we strongly, strongly encourage water utilities to pay for it."

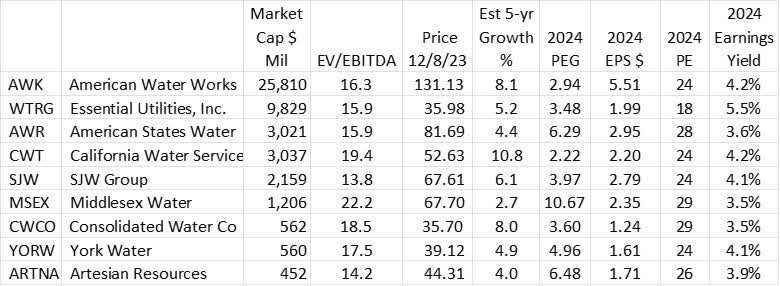

The US publicly traded water utility industry can be characterized as a few small-cap companies. The nine largest water utilities are, by market cap, American Water Works ((AWK)), Essential Utilities ( WTRG ), American States Water ( AWR ), California Water Service ( CWT ), SJW Group ( SJW ), Middlesex Water ( MSEX ), Consolidated Water Co. ( CWCO ), York Water ( YORW ), and Artesian Resources ( ARTNA ). As a comparison, the nine largest companies in the industry have a combined market cap of $43 billion and is smaller than Aflac ( AFL ), Carrier ( CARR ), or General Motors ( GM ).

Below is a table of the stock fundamentals of these nine water utilities.

Fundamental Stock Analysis US Water Utility Industry (Guiding Mast Investments, Morningstar, SPGMI)

{kind=link}

While seven of the nine water utilities rate as A or A- by CFRA for 10-year consistency in earnings and dividend growth, SJW and CWCO are rated B+, I question whether current investors are being adequately rewarded for the risks outlined above, especially the financial jeopardy.

I believe the financial risk to the industry was clearly and graphically demonstrated by the Flint water crisis. I could not image the investor consequences if Flint's water service was provided by American Water Works rather than the Flint Water District, owned by the city and supported by state taxpayers. While I sincerely doubt AWK's management, or any of the others listed above, would have created a similar environment which allowed for extensive and dangerous lead leaching, water utility investment risks should not be brushed aside. The exception may be Cayman Islands-based Consolidated Water due to its water utility business mostly in the Caribbean and growing exposure to seawater desalinization and wastewater treatment.

After personally investing in and offering positive commentary on water trends for investors for over 20 years, I sold all of them in 2015 and believe there are better utility investment opportunities elsewhere. After reviewing the valuations of the nine water utilities above, I agree with the activist shareholder suggestion Algonquin Power management should exit both its merchant renewable power and its water business.

Bottom line: "No Thank You" to the publicly traded US water utility industry. The valuation of their stocks does not compensate me for their unique risks.

For further details see:

American Water Works: No Thanks, Too Risky For Me