AMWL - American Well Reduces Revenue Guidance On Converge Replatforming Progress (Downgrade)

2023-08-11 16:19:30 ET

Summary

- American Well Corporation reported Q2 2023 financial results, missing revenue and EPS estimates.

- The company provides a telehealth platform for health system participants in the U.S. and overseas.

- Due to re-platforming issues, legacy system churn, and high operating losses, my outlook on American Well is to Sell.

A Quick Take On American Well

American Well Corporation ( AMWL ) aka "AmWell" reported its Q2 2023 financial results on August 2, 2023, missing revenue and EPS estimates.

The firm provides a telehealth platform for health system participants in the U.S. and overseas.

I previously wrote about AmWell with a Hold outlook.

Given management's comments on migration issues, legacy system churn combined with a recent Morgan Stanley downgrade and continuing high operating losses, my outlook on American Well Corporation is to Sell it.

AmWell Overview And Market

Boston, Massachusetts-based AmWell was founded to develop the AmWell Platform, a telehealth system that enables a wide variety of healthcare services to be delivered remotely.

Management is headed by Chairman and Co-CEO Ido Schoenberg, MD.

Ido was previously co-founder of iMDSoft and co-founded AmWell with his brother Roy Schoenberg, who is the company President and Co-CEO.

The firm has clients among health systems, health insurance plans, employers, and retailers.

The company's primary offerings include:

-

Telehealth.

-

Telestroke.

-

Telepsychiatry.

-

On-demand consultations.

-

Scheduled consultations.

-

Pre-packaged care modules & programs.

-

EHR Integration.

-

"Converge" with third-party and device integration support.

The company works with large entities to embed its telehealth capabilities within their workflows and pursues new business via a direct sales force.

According to a 2020 market research report by MarketsandMarkets, the global market for telehealth software and services is expected to reach $55.6 billion by 2025, up from a forecast $25.4 billion in 2020.

This represents a strong CAGR of 16.9% from 2020 to 2025.

The main drivers for this expected growth are a sharp increase in the monitoring of chronically ill and elderly patients and improved telehealth monitoring devices and connectivity.

Also, providers continue to offer an increased number of specialty services via remote means as they seek to improve care quality while increasing productivity and reducing costs.

Below is a chart showing the historical and projected growth rates in telehealth usage by global region:

Telehealth Market (MarketsandMarkets)

Major competitive or other industry participants include:

-

Doctor On Demand.

-

Teladoc Health.

-

MDLIVE.

-

Philips.

-

Medtronic.

-

GE Healthcare.

-

Cerner.

-

Siemens Healthineers.

-

GlobalMed.

-

Chiron Health.

AmWell's Recent Financial Trends

-

Total revenue by quarter has plateaued; Operating income by quarter has remained substantially negative.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has trended lower in recent quarters; Selling, G&A expenses as a percentage of total revenue by quarter have risen sharply more recently.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have remained sharply negative, as the chart shows below:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

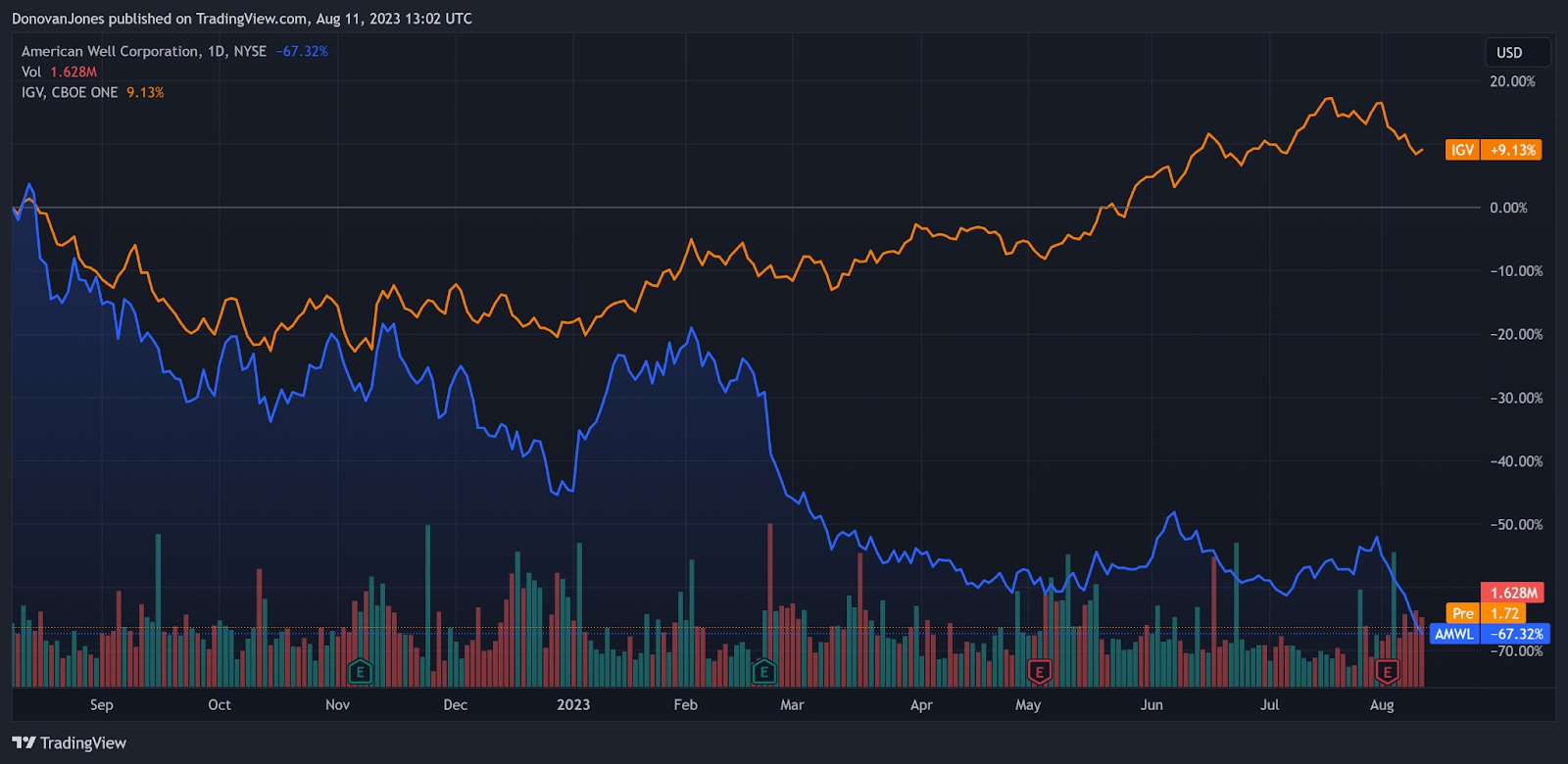

In the past 12 months, AMWL's stock price has fallen 67.32% vs. that of the iShares Expanded Technology-Software ETF's ( IGV ) rise of 9.13%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For the balance sheet , the firm ended the quarter with $458.7 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash used was ($156.0 million), during which capital expenditures were only $0.3 million. The company paid $78.8 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For American Well

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.3 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.8 |

| Revenue Growth Rate |

| 4.2% |

| Net Income Margin |

| -226.1% |

| EBITDA % |

| -84.1% |

| Net Debt To Annual EBITDA |

| 2.0 |

| Market Capitalization |

| $498,180,000 |

| Enterprise Value |

| $70,540,000 |

| Operating Cash Flow |

| -$155,700,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.22 |

(Source - Seeking Alpha).

As a reference, a relevant partial public comparable would be Teladoc Health (TDOC); shown below is a comparison of their primary valuation metrics:

| Metric [TTM] |

| Teladoc |

| AmWell |

| Variance |

| Enterprise Value / Sales |

| 1.9 |

| 0.3 |

| -86.2% |

| Enterprise Value / EBITDA |

| 254.9 |

| NM |

| --% |

| Revenue Growth Rate |

| 13.3% |

| 4.2% |

| -68.1% |

| Net Income Margin |

| -158.8% |

| -226.1% |

| 42.4% |

| Operating Cash Flow |

| $242,910,000 |

| -$155,700,000 |

| --% |

(Source - Seeking Alpha).

Commentary On AmWell

In its last earnings call ( Source - Seeking Alpha ), covering Q2 2023's results , management highlighted continued client migrations to its new Converge platform.

The firm also launched a new "very large strategic payer client on Converge," but did not name the customer.

Leadership is seeing the Converge platform reduce customer call center volume, indicating better customer service and cost savings.

However, a recent Morgan Stanley report cut AMWL to a Hold due to slower-than-expected growth, viewing the stock as more of a 2024/2025 story and cutting its price target to $2.50.

Management didn't disclose specific client or revenue retention rate metrics but said that customer churn was related to its legacy system and none to its new Converge platform.

Total revenue for Q2 2023 fell 3.3% YoY while gross profit margin dropped 4.6%.

Selling, G&A expenses as a percentage of revenue rose 16.2% year-over-year, a negative signal indicating worsening efficiency and operating losses increased by 3.2%.

The company's financial position is moderate, with plenty of liquidity but high free cash use, giving the firm three years of runway.

Looking ahead, management revised its forward full-year revenue guidance to $260 million, or a decline of 6.2% YoY.

If achieved, this would represent a reversal versus 2022's growth rate of 42% over 2021.

Analysts questioned company leadership about how it will reach breakeven. Management will likely cut back on R&D, while reducing product delivery costs and improving sales efficiency.

A potential upside catalyst to the stock could include faster migration of clients to Converge, as well as an increase in new clients to the system.

However, given management's comments on migration slowness and legacy system churn combined with the MS downgrade and continuing high operating losses, my outlook on American Well Corporation is to Sell it.

For further details see:

American Well Reduces Revenue Guidance On Converge Replatforming Progress (Downgrade)