APOG - American Woodmark Still Offers Upside Despite The Pain That Lies Around The Corner

2023-06-30 07:59:44 ET

Summary

- Despite a solid 2023 fiscal year, American Woodmark Corporation, a producer of cabinets and similar products, is expected to have a weaker 2024 due to the weakening remodeling and new home construction markets.

- The company's financial performance improved significantly from 2022 to 2023, with revenue increasing by 11.3% and the firm going from a net loss of $29.7 million to a net profit of $93.7 million.

- Despite the expected weakening, the shares of American Woodmark look affordable and the author maintains a 'buy' rating for the stock.

When it comes to investing, many investors and analysts equate weakening financial performance with the idea that you should become bearish on the company experiencing said performance changes. This is unfortunate, because sometimes, the best investment opportunities are those that are experiencing issues. The idea behind this is that, as the market anticipates further weakening, shares can be priced at levels that are lower than what they should be. Buying in on the cheap to take advantage of this mindset can be incredibly profitable. One really good example that I could point to that has played out over the past several months now involves American Woodmark Corporation (AMWD), a producer of cabinets and similar products. Even though the company had a solid 2023 fiscal year, 2024 looks set to be painful by comparison. Even with this pain, however, shares of the company look cheap, both on an absolute basis and relative to similar enterprises. Given how cheap the stock currently looks, and in spite of the fact that share price appreciation has been rather impressive in recent months, I would argue that further upside for investors exists from here.

The picture is worsening

It's important, when it comes to investing, to look at an opportunity from multiple angles. For instance, you cannot just look at annual data only and expect for things to turn out well. Changing economic conditions, not to mention changing conditions on a company specific level, always need to be monitored. And sometimes, the first signs of change occur in the course of a single quarter. To see what I mean, let's start with looking at the financial performance of American Woodmark during its 2023 fiscal year compared to how it performed in 2022.

{kind=link}

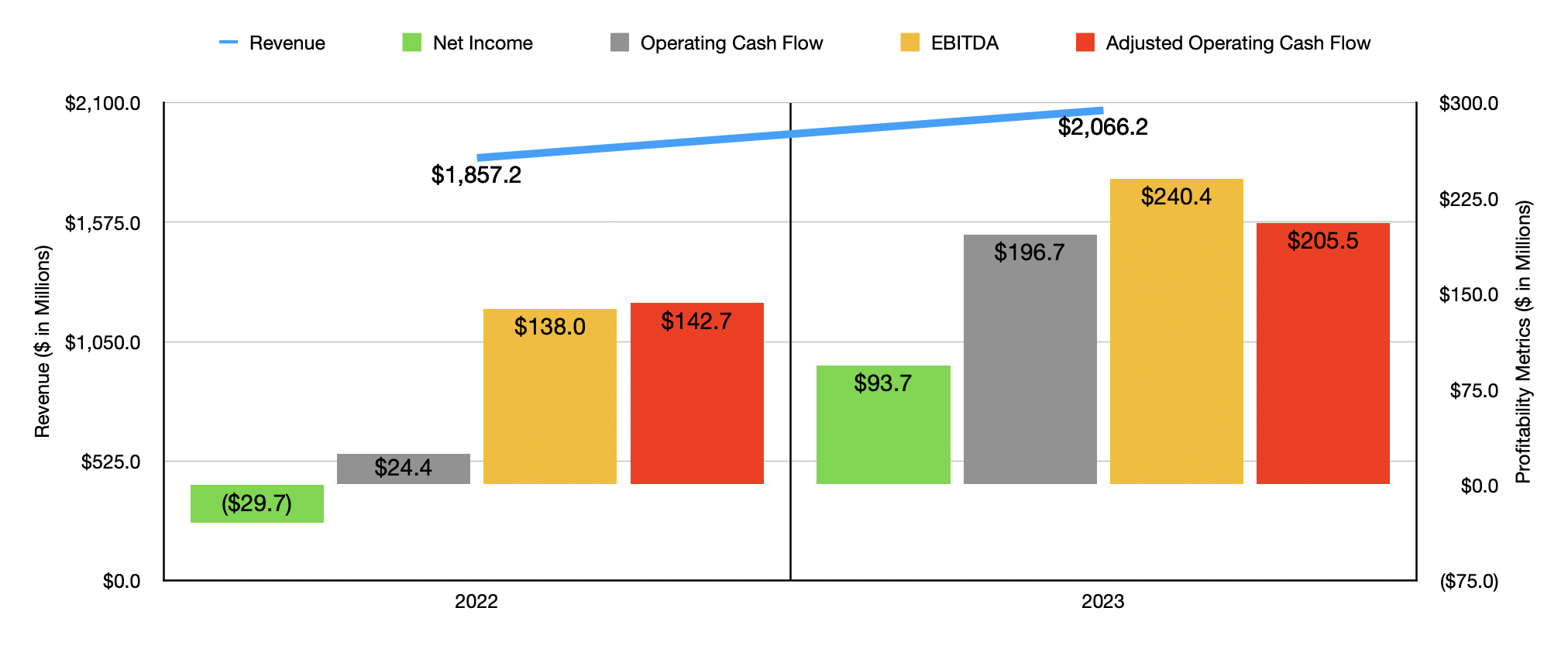

In the chart above, you can see that the company generated revenue of $2.07 billion. That's 11.3% above the $1.86 billion the company generated in 2022. This move higher was largely driven by a 21.1% rise in its builder channel and a 22.2% increase in the dealer distributor channel, with both of those benefiting significantly from price increases that the company imposed on its customers.

On the bottom line, the picture for the company also improved nicely. The firm went from generating a net loss of $29.7 million In 2022 to generating a net profit of $93.7 million in 2023. In addition to benefiting from a sales increase, the company also saw some of its costs improve materially. Most significantly, American Woodmark reported a rise in its gross profit margin from 12.2% to 17.3%. This expansion was driven largely by an increase in prices that the company charged for its offerings, as well as by operational improvements aimed at boosting manufacturing efficiencies, addressing supply chain issues, and more. Other profitability metrics also improved nicely. Operating cash flow, for instance, grew from $24.4 million to $196.7 million. If we adjust for changes in working capital, we would have seen this number grow from $142.7 million to $205.5 million. And finally, EBITDA increased from $138 million to $240.4 million.

{kind=link}

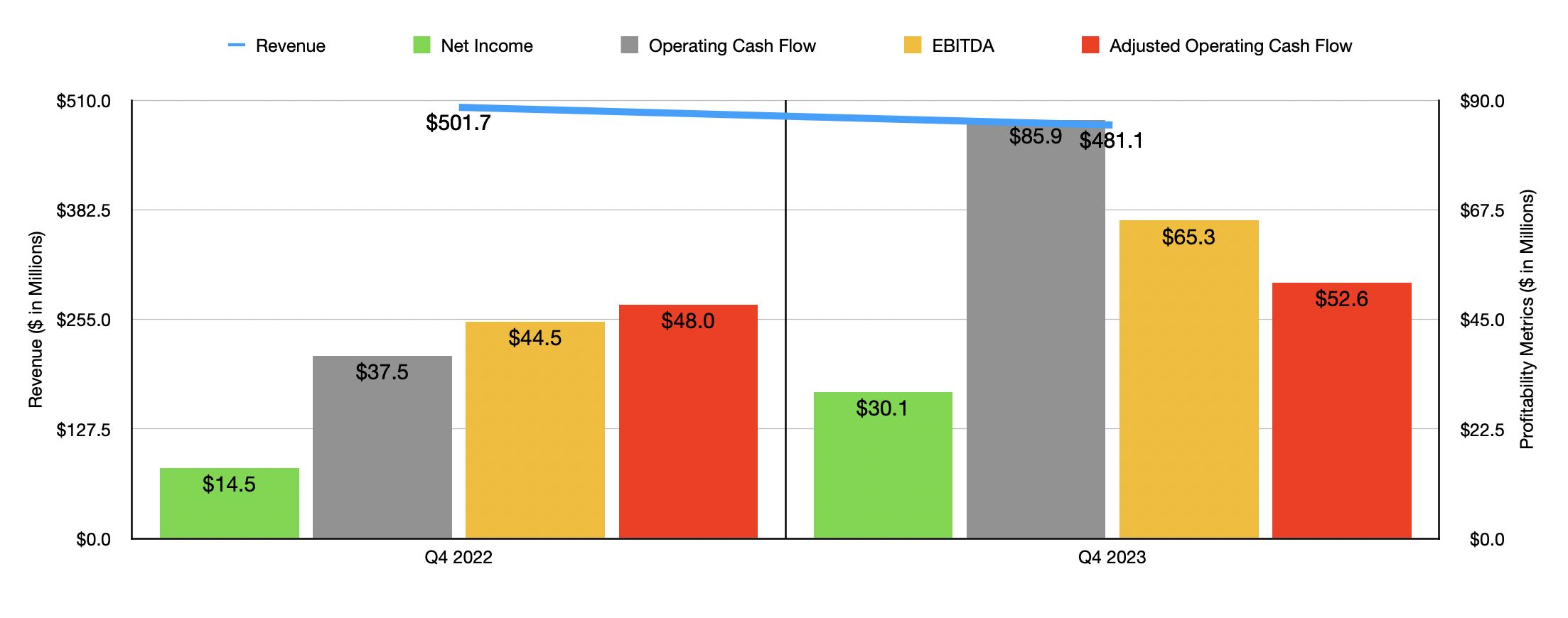

Based on these results on their own, you would expect the optimism centered around the company to be quite material. But the picture is not that simple. If we look at the fourth quarter of the company's 2023 fiscal year, for instance, we would see that revenue came in at only $481.1 million. That's a decline of 4.1% over the $501.7 million that the company generated one year earlier. Despite this top line weakness, bottom line results were actually very positive. Driven by the same margin expansion mentioned already, net profits for the company more than doubled from $14.5 million to $30.1 million. Operating cash flow more than doubled from $37.5 million to $85.9 million, while the adjusted figure for this grew from $48 million to $52.6 million. And finally, EBITDA for the company jumped from $44.5 million to $65.3 million.

Even at this point, investors could be forgiven for thinking that the weakness experienced in the final quarter is just a one-time event. Sadly, however, this does not seem to be the case. In guidance that the company provided to investors, management stated that overall revenue for the 2024 fiscal year should fall at the low double-digit rate. As I have touched on in other articles such as here and here , the remodeling and new home construction markets are showing significant signs of weakening. Unfortunately, American Woodmark is tied significantly to this space. So any weakness on this front is absolutely going to impact it as well.

On the bottom line, management has been more precise in terms of what they expect. When it comes to profitability, the company said that EBITDA should come in at between $205 million and $225 million. If we take the midpoint of that range, that would imply $215 million, which would be 10.6% below the $240.4 million the company generated in 2023. If we assume the same year over year decline when it comes to adjusted operating cash flow, we would expect a reading for the year of $183.8 million.

{kind=link}

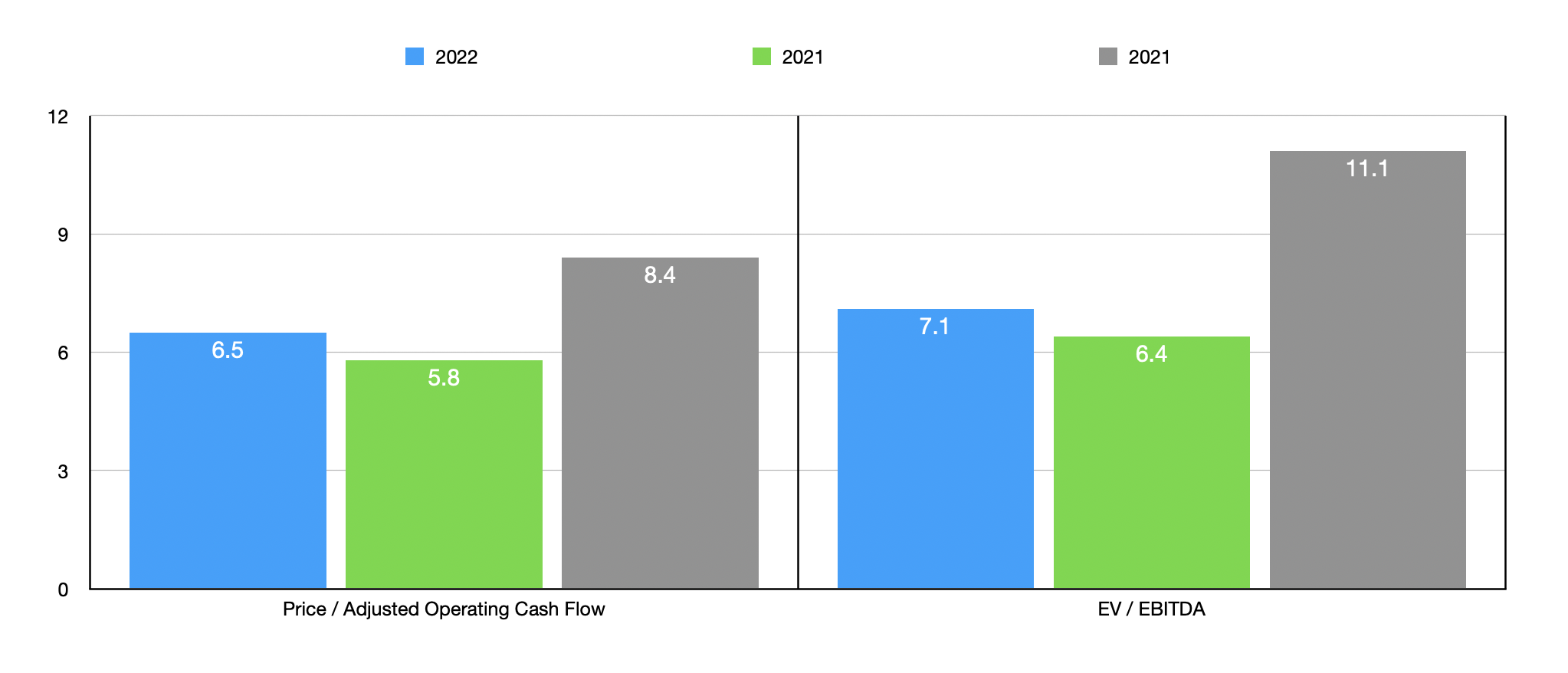

In the chart above, you can see how shares are priced on a forward basis. You can also see how they are priced using data from both 2022 and 2023. Even if financial performance were to revert back to 2022 levels, I have a difficult time imagining the stock to be all that pricey. In the table below, I decided to compare American Woodmark to five similar enterprises. Even though I would normally prefer to use the most recently completed fiscal year for comparison, I do my best to be conservative in my calculations. So instead, I decided to compare the forward estimates for American Woodmark to the most recent trailing 12-month data for the five companies in question. Even doing this, I found out that, in both the price to operating cash flow scenario and the EV to EBITDA scenario, only one of the five companies ended up being cheaper than our target.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| American Woodmark |

| 6.5 |

| 7.1 |

| AZZ Inc. ( AZZ ) |

| 15.9 |

| 8.0 |

| Apogee Enterprises ( APOG ) |

| 6.9 |

| 7.3 |

| Quanex Building Products ( NX ) |

| 6.4 |

| 6.8 |

| JELD-WEN Holding Inc. ( JELD ) |

| 6.8 |

| 9.4 |

| PGT Innovations ( PGTI ) |

| 8.5 |

| 9.9 |

Takeaway

Operationally, there is no doubt that American Woodmark looks set to weaken this year. It's not unthinkable that this weakness could even worsen into the next calendar year. But even with this pain factored in, shares of the company look very affordable on an absolute basis. For those who may not recall, it's worth pointing out that I did previously rate the business a 'buy' back in February of this year. Since then, the stock has generated upside of 23.3% compared to the 9.7% the S&P 500 generated over the same window of time. In spite of this upside and because of how cheap the stock remains, even on a forward basis, I would argue that further upside is justified and that the 'buy' rating I assigned the stock previously still holds.

For further details see:

American Woodmark Still Offers Upside Despite The Pain That Lies Around The Corner