CPER - Amerigo Resources: A Mineless Copper Bet With 9%+ Yield

Summary

- Amerigo Resources derives the vast majority of its revenue from copper, yet it has no mines.

- The business model of the company makes its risk profile far superior to that of a typical miner.

- Management has significant skin in the game and has been focusing on shareholder returns.

- My forward EV/EBITDA estimate of 3.3 implies serious upside when compared to the sector median.

Amerigo Resources ( OTCQX:ARREF ) (ARG:CA) offers investors a lucrative value proposition. The company produces copper from tailings and has no mines itself, eliminating risks faced by a typical miner. Management has significant skin in the game and has been focusing of returning capital to shareholders through dividends and share buybacks. The dividend yield of Amerigo is more than 9% at current prices, while my estimation for the forward EV/EBITDA of just 3.3 implies considerable upside when compared to the sector's median.

Company overview

Registered in Canada, Amerigo Resources is a small copper producer with assets in Chile. Yet, unlike a typical metals' producer, the company has no mines. Instead, through its wholly owned subsidiary - Minera Valle Central S.A. ((MVC)), Amerigo derives its revenue from processing tailings from Codelco's El Teniente copper mine.

Amerigo's operations (Amerigo Resources)

This business model has superior risk profile than that of a miner, as it eliminates exploration, permitting and operational risks that come from operating the mine. Unlike mining, Amerigo's business is not nearly as capital-intensive, which allows for more focus on returning value to shareholders.

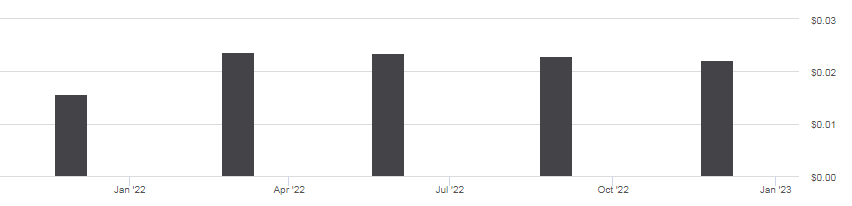

Amerigo's dividends (in US$) (Seeking Alpha)

{kind=link}

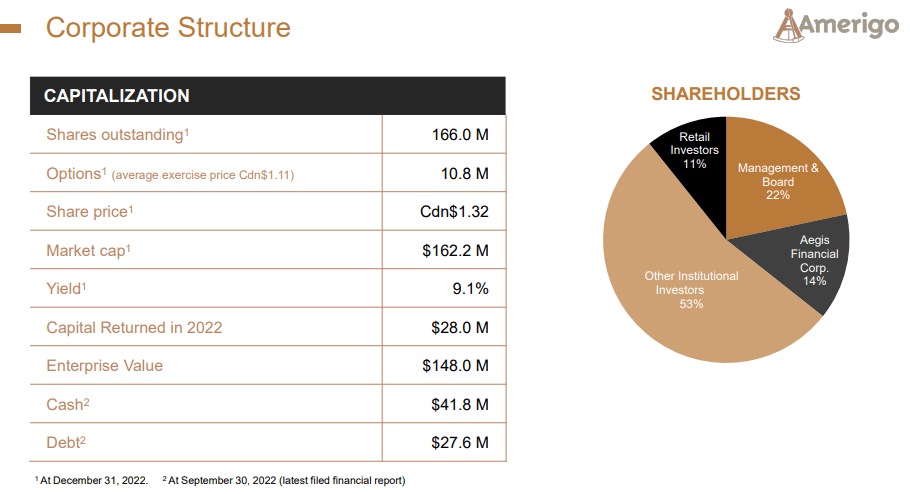

Speaking of returning value to shareholders, Amerigo has begun paying quarterly dividends in 2021 with the annualized dividend yield amounting to 9.5%. In addition, the company has been repurchasing shares as the share count declined from 182M in Sept'21 to 166M in Sept'22 (-8.8% YoY). 22% of the shares are owned by insiders, which implies significant skin in the game.

Amerigo's capital structure (Amerigo Resources)

{kind=link}

Financial overview and expectations

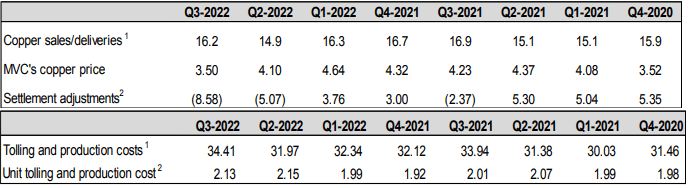

During the past few quarters, Amerigo has been maintaining production rate of about 16Mlbs of copper, which equals annualized production rate of 64Mlbs. Falling copper prices and negative settlement adjustment of US$8.6M have led to 36% YoY decline in Q3'22 revenue, which amounted to US$30.9M. It has to be noted that the negative settlement adjustment is due to Amerigo selling its production on M+3 basis, while copper prices were falling in Q2'22. In a rising commodity price environment, the adjustment should be positive. Tolling and production costs remained pretty stable and advanced only 1% YoY to US$34.4M. As a result, gross profit was negative at US$3.5M, while the bottom line came at negative US$4.4M, compared to a profit of US$8.4M a year ago.

Amerigo's key metrics (Amerigo Resources)

{kind=link}

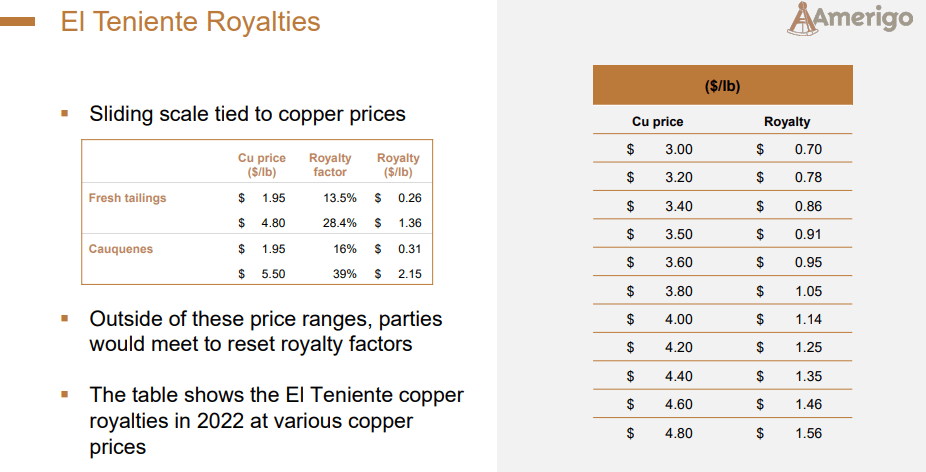

Note, that Amerigo was able to maintain its unit tolling and production costs relatively stable in the last two years, despite the serious inflationary pressures that were faced by other commodity producers. Despite that, total operating costs of Amerigo are relatively high, as royalties are quite high and increasing with the market price of copper. For Q3'22, total cost/lbs amounted to US$3.18.

Amerigo's royalty structure (Amerigo Resources)

{kind=link}

The financial position of Amerigo is solid with US$41.8M of cash and equivalents, while IB debt stood at US$27.5M as of the end of Q3'22. This gives the company a certain cushion to continue its dividend policy even if copper prices fall for a short period of time like in Q2 and Q3. That being said, now that copper prices rebounded towards the US$3.80/lbs level, I expect the company to generate sufficient cash in order to maintain its dividend. Assuming annual production of 64Mlbs of copper at prices of US$3.80/lbs, around US$14M of revenue from molybdenum, cash costs of US$1.93/lbs and total costs of US$3.33/lbs, I estimate 2023 EBITDA of US$44M. Given the low sustaining CAPEX of around US$6M, suggested by management and US$7M for the construction of a new sump, there seems to be enough room to maintain the current dividend, which is around US$15M per year and maybe even continue the buybacks.

Share price and valuation

Although Amerigo's return to shareholders during the past year has been negative, it managed to outperform the copper price, represented by the United States Copper Index Fund ( CPER ).

Looking at the upside potential, given the current EV of Amerigo of US$146.7M and my estimate of US$44M for 2023 EBITDA, the company is trading at forward EV/EBITDA of 3.3. At the same time, the materials sector, according to data from Seeking Alpha, has median forward EV/EBITDA of 7.3, implying more than 100% upside. While such multiple may seem high, due to Amerigo being a small company with a single asset, I think it's justified given the superior risk profile of the company, compared to the typical miner.

While there seems to be no company specific upside triggers, the share buyback program could be a source of upward pressure to the share price. The dividend yield of 9.5% at current levels is also very attractive and should put the stock on investors' radar as it continues to be paid quarterly. The ESG profile of Amerigo is also superior as it processes tailings and doesn't mine the material. This may attract ESG focused funds as well.

Copper price risk

Immune to copper prices? (Amerigo Resources)

{kind=link}

Amerigo is quite vulnerable to fall of copper prices, especially close to or especially below the US$3.20/lbs mark as total cost of production is in that area. In that regard, management's claim in the corporate presentation that shareholders are immune to copper price volatility seems a bit misleading. While the company's current financial position is solid and would allow for a few "weak" quarters, if copper prices remain low for a considerable period, the dividend won't be sustainable.

Conclusion

Amerigo Resources offers investors pure-play copper exposure without the need to assume geological risks that come with investing in a miner. With its business model built around tailings processing, the company has also a better ESG profile. The solid financial position allows for the dividend payment to continue even in times of short-term weakness in copper prices. Trading at just 3.3 forward EV/EBITDA, Amerigo could offer more than 100% upside from current levels.

For further details see:

Amerigo Resources: A Mineless Copper Bet With 9%+ Yield