ABCB - Ameris Bancorp: Reducing The Earnings Estimate But Maintaining A Buy

2023-05-30 15:29:55 ET

Summary

- Ameris Bancorp's earnings estimate for 2023 has been reduced to $4.56 per share due to decreased margin estimates and increased provisioning expense estimates.

- The company's risk level appears manageable. Unrealized losses are low, uninsured deposits are well covered, and exposure to office properties is limited.

- A buy rating is maintained on Ameris Bancorp with a target price of $39.00, implying a 20.1% upside from the current market price and a total expected return of 22.0%.

I'm reducing my earnings estimate for Ameris Bancorp ( ABCB ) for 2023 as I've decided to decrease my margin estimate and increase the provisioning expense estimate. Overall, I'm expecting the company to report earnings of $4.56 per share for 2023, down 8.6% year-over-year. The year-end target price suggests a high upside from the current market price. Therefore, I'm maintaining a buy rating on Ameris Bancorp.

Loan Growth Likely to Slightly Improve After Dismal Performance

Ameris Bancorp's loan growth plunged to 0.5% in the first quarter of 2023 from 5.5% in the fourth quarter of 2022. The first quarter's growth rate is the lowest since the third quarter of 2021. Going forward, management expects loan growth to improve slightly from the first quarter's level. Management is targeting loan growth to be in the low-to-mid-single digit range, as mentioned in the conference call .

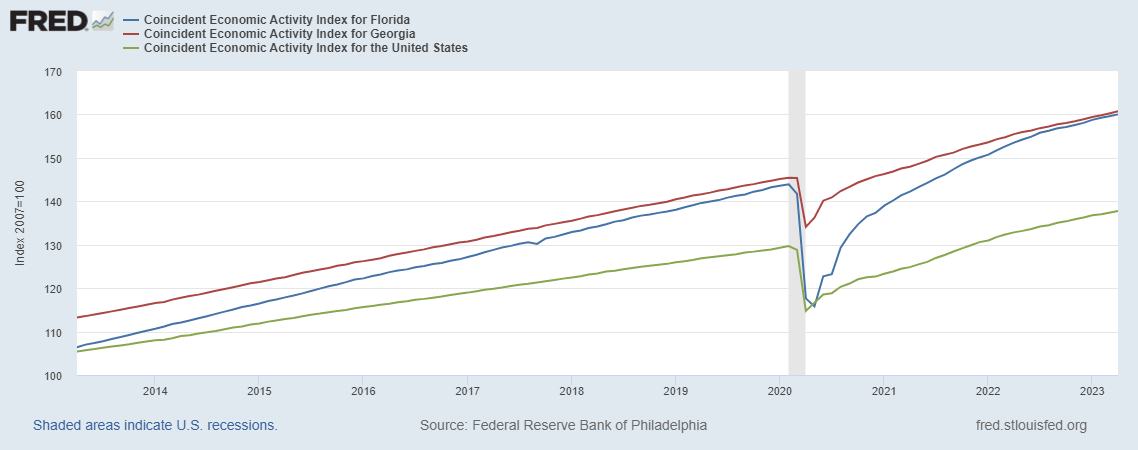

In my opinion, regional economies seem conducive to loan growth. The current economic activity in Ameris Bancorp's markets is satisfactory. The company mostly operates in the metropolitan areas of Greenville, SC, Charlotte, NC, Atlanta, GA, Moultrie, GA, Savannah, GA, Jacksonville, FL, and Gainesville, FL. Among these markets, most of the loans are concentrated in the Florida and Georgia markets. As can be seen from the slopes of the trendlines below, both states are currently doing quite well in terms of economic activity.

{kind=link}

As a result, I'm expecting Ameris Bancorp to report loan growth of 3.6% in 2023. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 343 |

| 505 |

| 638 |

| 655 |

| 801 |

| 861 |

| Provision for loan losses |

| 17 |

| 20 |

| 145 |

| (35) |

| 72 |

| 89 |

| Non-interest income |

| 118 |

| 198 |

| 447 |

| 366 |

| 284 |

| 226 |

| Non-interest expense |

| 294 |

| 472 |

| 599 |

| 560 |

| 561 |

| 583 |

| Net income - Common Sh. |

| 121 |

| 161 |

| 262 |

| 377 |

| 347 |

| 316 |

| EPS - Diluted ($) |

| 2.80 |

| 2.75 |

| 3.77 |

| 5.40 |

| 4.99 |

| 4.56 |

| Source: SEC Filings, Earnings Releases, Author's Estimates (In USD million unless otherwise specified) |

Risk Level Appears Under Control

Despite the ongoing panic in the banking sector, Ameris Bancorp's risk level appears manageable due to the following reasons.

- Uninsured and uncollateralized deposits represent 29.5% of total deposits and a total of $5.91 billion, as mentioned in the May presentation . In case of a deposit run, these deposits can be easily covered by available sources of liquidity, whose capacity totals around $9.4 billion.

- Due to the hybrid work and work-from-home culture, loans for office properties pose the risk of default. Further, there is a risk that the value of office properties will dip. Fortunately, Ameris Bancorp's exposure to the office segment is limited. Office loans totaled $1.4 billion at the end of March 2023, representing 7% of total loans.

- Unrealized loss on the Available-for-Sale ("AFS") securities portfolio totaled just $44.2 million at the end of March 2023, which represents less than 3% of book value, according to details given in the latest earnings presentation .

Maintaining a Buy Rating

Ameris Bancorp is offering a dividend yield of 1.8% at the current quarterly dividend rate of $0.15 per share. The earnings and dividend estimates suggest a payout ratio of 13% for 2023, which is in line with the five-year average of 14%. Therefore, my earnings outlook does not present any threat to the dividend payout.

I'm using the peer average price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Ameris Bancorp. Peers are trading at an average P/TB ratio of 1.27 and an average P/E ratio of 7.65, as shown below.

| ABCB |

| CATY |

| SFBS |

| ASB |

| SFNC |

| FHB |

| Peer Average |

| TBVPS - Dec 2023 ($) |

| 34.1 |

| 34.1 |

| 34.1 |

| 34.1 |

| 34.1 |

| Target Price ($) |

| 36.4 |

| 39.8 |

| 43.2 |

| 46.6 |

| 50.0 |

| Market Price ($) |

| 32.5 |

| 32.5 |

| 32.5 |

| 32.5 |

| 32.5 |

| Upside/(Downside) |

| 11.9% |

| 22.3% |

| 32.8% |

| 43.3% |

| 53.8% |

| Source: Author's Estimates |

Multiplying the average P/E multiple with the forecast earnings per share of $4.56 gives a target price of $34.90 for the end of 2023. This price target implies a 7.4% upside from the May 29 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple |

| 5.7x |

| 6.7x |

| 7.7x |

| 8.7x |

| 9.7x |

| EPS 2023 ($) |

| 4.56 |

| 4.56 |

| 4.56 |

| 4.56 |

| 4.56 |

| Target Price ($) |

| 25.8 |

| 30.4 |

| 34.9 |

| 39.5 |

| 44.0 |

| Market Price ($) |

| 32.5 |

| 32.5 |

| 32.5 |

| 32.5 |

| 32.5 |

| Upside/(Downside) |

| (20.7)% |

| (6.6)% |

| 7.4% |

| 21.4% |

| 35.5% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $39.00 , which implies a 20.1% upside from the current market price. Adding the forward dividend yield gives a total expected return of 22.0%. Hence, I'm maintaining a buy rating on Ameris Bancorp.

For further details see:

Ameris Bancorp: Reducing The Earnings Estimate But Maintaining A Buy