ABC - AmerisourceBergen: Great Company Wrong Price (Rating Downgrade)

2023-07-28 12:14:11 ET

Summary

- AmerisourceBergen has seen a 3x return on investment in the past 3 years, outperforming the market. I think it's a very solid company in pharma and healthcare distribution.

- Investing in high-quality companies when they are cheap is crucial for maximizing returns.

- AmerisourceBergen is a conservative and safe option in the pharma and healthcare industry, but has now reached a valuation of where I would consider it a "HOLD".

Dear readers/followers,

I last wrote about AmerisourceBergen ( ABC ) almost three years back . It's a small position I've held going on five years now, and the returns on the company since my last article has been absolutely stellar, 3x'ing the market (almost).

Seeking Alpha ABC RoR (F.A.S.T graphs)

It goes to show you that you really want to be Investing In above-quality companies when things are cheap. Things being cheap isn't a time to go for "cheap" or bad stocks - It's a time to double down on quality - which was what I did.

I, unfortunately, did not double down on quality "enough" at the time. So my position in ABC, despite everything, Is rather small. It's a solid gain - but unfortunately a solid gain on a small position.

While pharma and healthcare companies come in many flavors, few of the ones available share the conservative and overall safe nature of ABC.

Let's look at what ABC can offer you, after a 3-year 100% RoR.

ABC - Plenty to like even after 100% RoR.

Remember, ABC doesn't develop any drugs - they just sell them. What the company does is act as a drug wholesaler in the distribution and service business, with a focus on Improving overall patient costs and outcomes.

Of course, ABC also leverages the position it has in the drug value chain, so they "clone" existing drugs, distributing generic versions at substantially higher margin levels than the other drugs that are being sold.

ABC remains a NA/US-only company with customers in the form of hospitals, pharmacies, health systems, physicians, clinics, and different types of facilities and living centers with both brand-name drugs and generics, healthcare products, home healthcare supplies, and equipment.

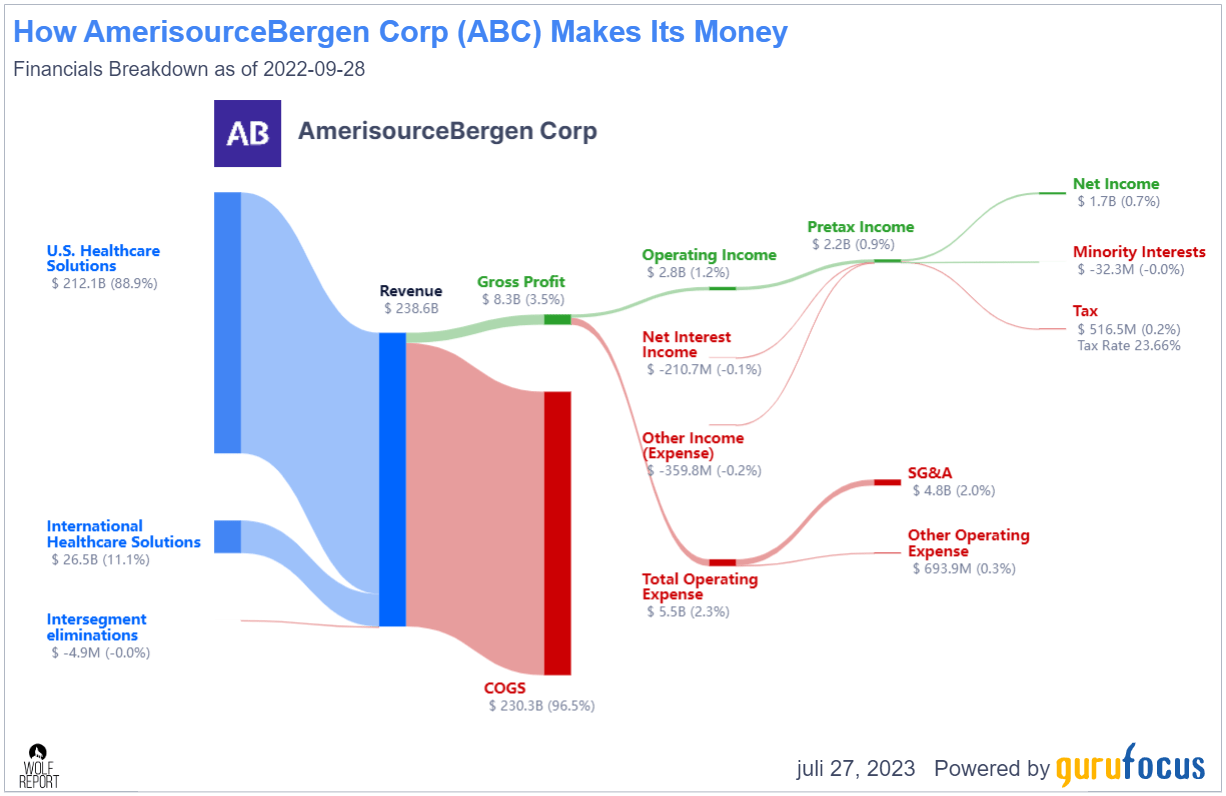

The company, like most businesses in this sector, is a very low-margin player. It works with scale and moat, not necessarily margins. Gross margins are as low as 3-4%, with operating margins below 1.5% for 2022, and net margins below 1%.

This is the COGS-heaviest business I've ever reviewed, with a revenue/net structure as you see below.

{kind=link}

I don't think it's a strange situation per se when you consider exactly what the company does and what the cost structures might be. Still, the company is profitable, and when the sum of revenues is large enough, the profit is still "good". And that is the case for ABC. Even a 0.7% net profit margin on a revenue of over $230B turns out to be over $1.6B in revenues.

This is how this company works. A net margin increase even of just 1-5 bps would be a non-trivial development for AmerisourceBergen. 2Q23 from May is the latest report we have, and to me it confirms the overall upside for this business.

The company reported a strong 2Q with an increase in guidance/outlook, due to a demonstration of strength in the company's pharma-centric approach and strategy.

This is based on a near-double digit 9.9% revenue increase, a 2.7% improvement in gross profit, but still a decline in operating Income of 28.2% for the quarter. The reason for this was mostly expense-related. Operating expenses are up almost 20% YoY, and it's not really sector-agnostic either. Healthcare solutions saw improvement in operating Income - it's the International healthcare solutions segment that saw a significant decline in Income.

Still, the latest results did come with an improvement in operating increase insofar as expectations go.

{kind=link}

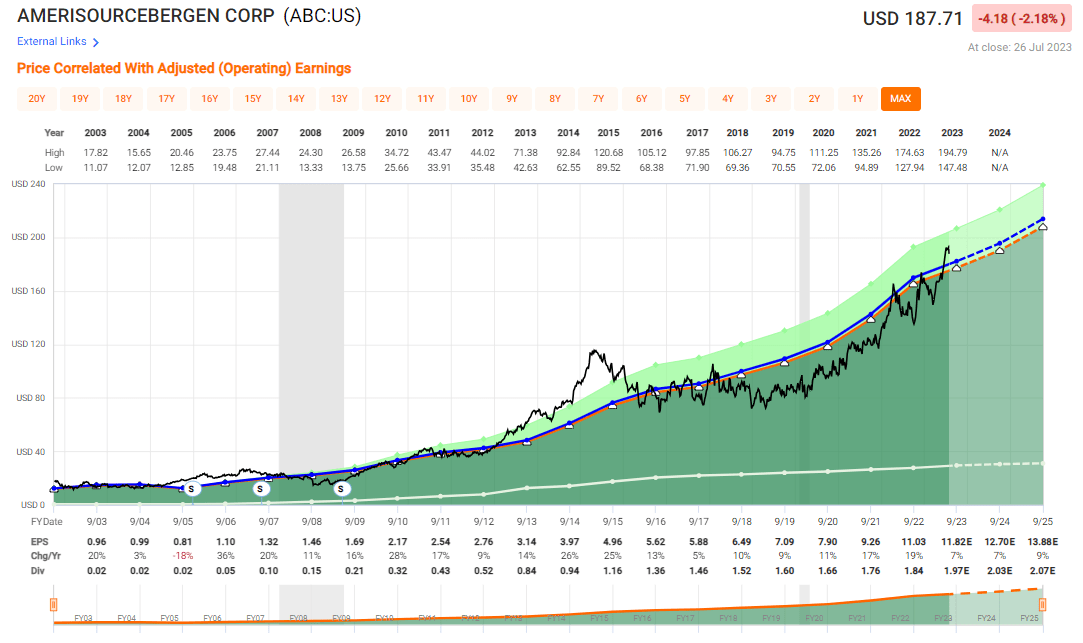

Obviously, the entire COVID-19 story was a major contributor to ABC, and the growth rates that we saw, including double-digit 11%, 17%, and 19% growth rates seem unlikely to be repeated on a forward basis. Going forward, analysts expect single-digit growth rates for this company - 7% this year, 7% 2024E and 9% 2025E. These are still good earnings growth rates, just not as high. It's also worth mentioning that ABC has held to its historical valuation averages to an almost slavish degree. Any deviation from the long-term trend has been short in nature and with the exception of one during 2013-2015, has corrected itself quickly. I was lucky enough to pick the company up cheap - but I'll show you in the valuation portion of the article why things are in fact no longer "cheap".

ABC is nonetheless a great company in my view. It focuses on specialty medicine and services, working with market leaders, and leveraging its position to drive efficient solutions.

One of the primary risks to ABC that I actually see is customer concentration. Walgreens is, at over 30% of revenues, is still a major customer for ABC, and there are more customers like that who come in at double digits. So any shortfall or large customer elimination here would be significant.

However, it's also important to remember that as things are now, it's a pretty homogenous market. Not many players large enough to matter exist.

in terms of competition - ABC does have it, it comes in the form of businesses like Cardinal Health ( CAH ) and McKesson ( MCK ). I've owned both of these businesses previously - but sold them due to overvaluation, and I'll show you in a bit why it might be valuable to consider doing the same with this particular one.

ABC's largest segments compete directly with MCK and CAH, as well as with national generic distributors and pharmaceutical firms and manufacturers who directly sell their products to customers or companies (such as pharmacies) that handle their own warehousing.

On a high level, this means that ABC must rely on efficiency, competitive edges, VAP programs, service, customer satisfaction, credit availability, and other factors.

To be completely honest with you, this is not the sort of business I would look at running or being involved in. I know how slim these margins are, and how every bps of margin must be calculated because there are such slim margins to begin with. I do not envy the company its position and the demands upon it, especially with rising inflation, wages, and costs going up. Logistical costs especially have proven to be tricky for ABC.

Things I would keep an eye on when it comes to ABC trends are the changes in the insulin market. With the current fee-for-service model that's about to change in terms of what the company needs to charge. ABC's focus is preserving its economics - but this comes at an already-high expectation for ABC to actually have a very high amount of inventory for this sort of product, which isn't easy as interest rates are increasing. This is an important question because ABC has a 30% nationwide market share for GLP-1 drugs and insulin/diabetes overall.

The core question becomes, if ABC in the environment we're currently seeing with pressure on pharma and medicine prices is going to be able to receive the same sort of margins, or how they'll go about ensuring their continued profitability. I think it's very hard to provide any sort of good guidance or expectation on this because the official company answer regarding this question is as follows, from 2Q23.

As we -- we don't really get into individual product economics.

(Source: Steve Collis, 2Q23 Earnings Call )

Beyond saying that they provide a portfolio for their customers, and those products they're providing are diversified which in turn provides a value proposition, and they're relying on that scale to provide margins - combined of course with extensive knowledge of the market.

The company does have the right, to in case of changed product economics, negotiate with their suppliers.

However, I've been following this discussion for years. I simply see very few, or no scenarios, where the unit economics for products/medicines are going to be improving here. Not even ABC is talking of improvements, but maintaining product economics - and this should tell you something.

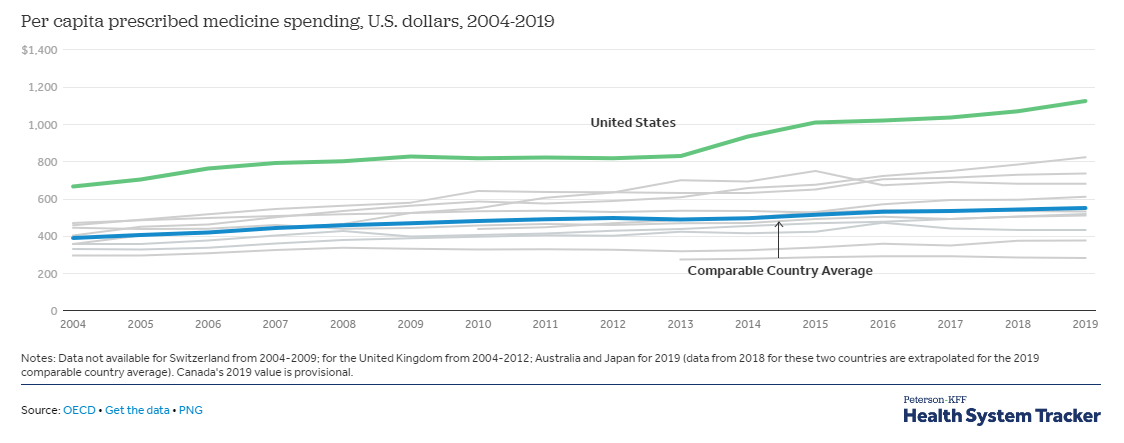

My base case is that the profit margins will tighten further. Countries like the US need to get their medicine spending down. it's no secret that on an International comparison, the USA is so beyond the average, that it's eyebrow-raising.

{kind=link}

But still, this is not an article about the differences in medicine prices. What I believe is that there is so much room for normalization here, at least in theory, that I view any premium for a company like ABC to be a very bad idea.

So with that, let's look at valuation.

AmerisourceBergen - Why I'm cutting my rating

So, important things first.

I'm cutting my rating on AmerisourceBergen. it's now a "HOLD".-

This is due to an overvaluation I consider to be very clear here. because of the problems associated with the near-term and mid-term future of ABC, I believe that ABC should be bought at a discount to what is otherwise an excellent sort of growth rate. We no longer have that discount.

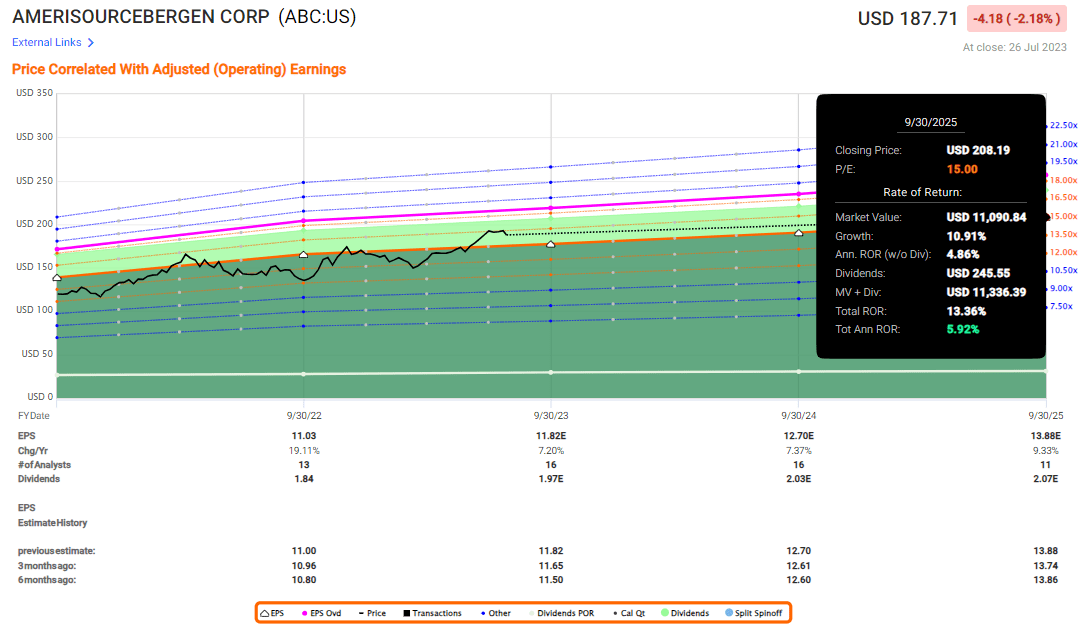

As it stands today, AmerisourceBergen trades at an average weighted P/E of over 16x. The last time we had that was over 5 years ago. Before that, not since 2014-2015. it's not a typical valuation for the company, and it's not one the company is usually at for a very long time.

{kind=link}

The way I view AmerisourceBergen is actually fairly simple. it's very easy to forecast, and I view the 15x P/E to be either okay or I go lower to 13x. Because a 15x P/E for the company goes no higher than a 13.3% RoR at this time until 2025E, or an annualized RoR of less than 6%, I consider this to be extremely unfavorable, and with the context of the pharma industry, justification enough for a rotation.

{kind=link}

S&P Global analysts have the company at a range of $149 up to $213. 8 out of 16 analysts are at a "BUY" recommendation here, with a PT of $194/share. I'll set myself at more than $30/share below this PT, and I wouldn't "BUY" ABC at anything above $160/share.

What's more, the current share price of almost $190/share justifies rotation to me. So that's what I'm looking at. it's a great company, a great RoR, but the time has come to call quits on this one and move on.

Here is my thesis for the company.

Thesis

- AmerisourceBergen is a very qualitative healthcare and pharma distributor. Together with a small list of comps, it's probably one of the better companies in the entire segment. I've made triple-digit returns since my investment, and I'm happy with my RoR - very happy.

- However, at the same time, the company is facing pricing and margin pressure, it has no real net margin (less than 2%), and its dividend is less than 1.1% in a world where we get 3.3% for "free" on a savings account. I do not view this as positive.

- The combined thesis here makes me go "HOLD" for ABC here, and I'm potentially rotating my shares in the investment to something more profitable and with more upside. I don't like holding overvalued equities, and I view ABC as overvalued here.

- My PT for the company comes to $160/share - no more.

Remember, I'm all about:

1. Buying undervalued - even If that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes onto overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

This company is overall qualitative. This company is fundamentally safe/conservative & well-run. This company pays a well-covered dividend. This company is currently cheap. This company has a realistic upside based on earnings growth or multiple expansion/reversion .

The company is not cheap, and while it does have an upside, I don't view it as significant enough in this context. I say "HOLD"; and I say that you could even rotate your investment here.

For further details see:

AmerisourceBergen: Great Company, Wrong Price (Rating Downgrade)