AMOT - Ametek: Shares Are Getting Rather Pricey

Summary

- AMETEK is a solid business that continues to grow on both its top and bottom lines.

- This has proven bullish for shares in recent months during a time in the market where robust performance is difficult to come by.

- But now shares are getting rather lofty and investors should be careful moving forward.

When it comes to companies that manufacture and sell industrial products, the amount of diversity between them can be significant. After all, the term ‘industrial’ is rather vague in and of itself. But when you start talking about specific areas of focus, you can encounter a wide variety of interesting businesses. One such firm worth looking at is AMETEK ( AME ). At present, the enterprise focuses on two different product categories. The first of these would be Electronic Instruments such as analytical, test, and measurement instruments that are used across a wide variety of industries. And the other would be Electromechanical products such as thermal management systems, automation solutions, specialty metals, and more. Recent financial performance achieved by the company has looked rather impressive. Even so, shares of the company look to be quite pricey. Interestingly enough though, this, combined with the pain the broader market has experienced, has not stopped the company from seeing its share price rise significantly. I wouldn't go so far as to call the company overvalued at this point. But I do think that if this trend continues, there could be some downside for investors before long.

At risk of becoming overvalued

The last article I wrote about AMETEK was published in early June of 2022. By that point, the company had just fully recovered from the COVID-19 pandemic and was showing signs of continued growth beyond that. All things considered, the company looked healthy and I believed that it would ultimately create some attractive value for investors in the long run. But because of how shares were priced, I ended up rating the company a ‘hold’ to reflect my view that shares should generate upside or downside that would more or less be in line with what the broader market would achieve. Since then, the market has vehemently disagreed with me. While the S&P 500 is down 3.2% since the publication of the article, shares of AMETEK have generated upside of 18.5%.

{kind=link}

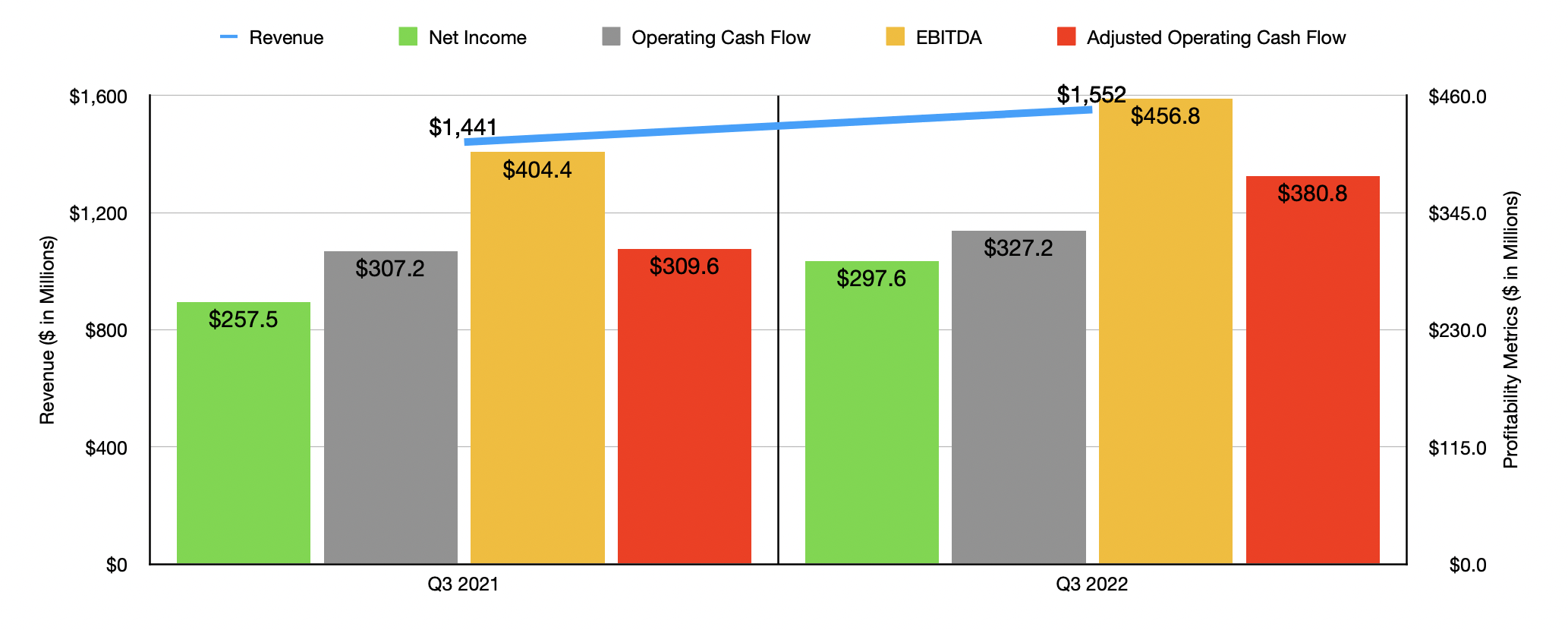

This return disparity seems to have largely been driven by robust financial performance reported by management. To see what I mean, we should first look at how the company performed during the third quarter of its 2022 fiscal year. This is the most recent quarter for which data is available for the enterprise. During that time, sales came in at $1.55 billion. That's 7.7% higher than the $1.44 billion reported the same quarter one year earlier. Organic revenue growth for the company was even more impressive, coming in at 11% year over year. The company also benefited to the tune of 1% from acquisitions. Unfortunately, some of this upside was offset by a 4% impact caused by foreign currency translation. The greatest growth for the company came from its Electromechanical segment, with revenue jumping 8.5%. A 13% rise in organic sales, driven at least in part by pricing actions enacted by management, was instrumental in this regard.

On the bottom line, the picture for the company improved as well. Net income jumped from $257.5 million to $297.6 million year over year. One thing that the company really had going for it was its ability to increase prices by more than the cost increases imposed upon it by supply chain issues and higher material costs. This brought the company's segment operating margins to 26.4% in the third quarter of 2022 compared to 25% reported one year earlier. Other profitability metrics followed suit. Operating cash flow rose from $307.2 million to $327.2 million. If we adjust for changes in working capital, it would have increased even more from $309.6 million to $380.8 million. Meanwhile, EBITDA for the company improved from $404.4 million to $456.8 million.

{kind=link}

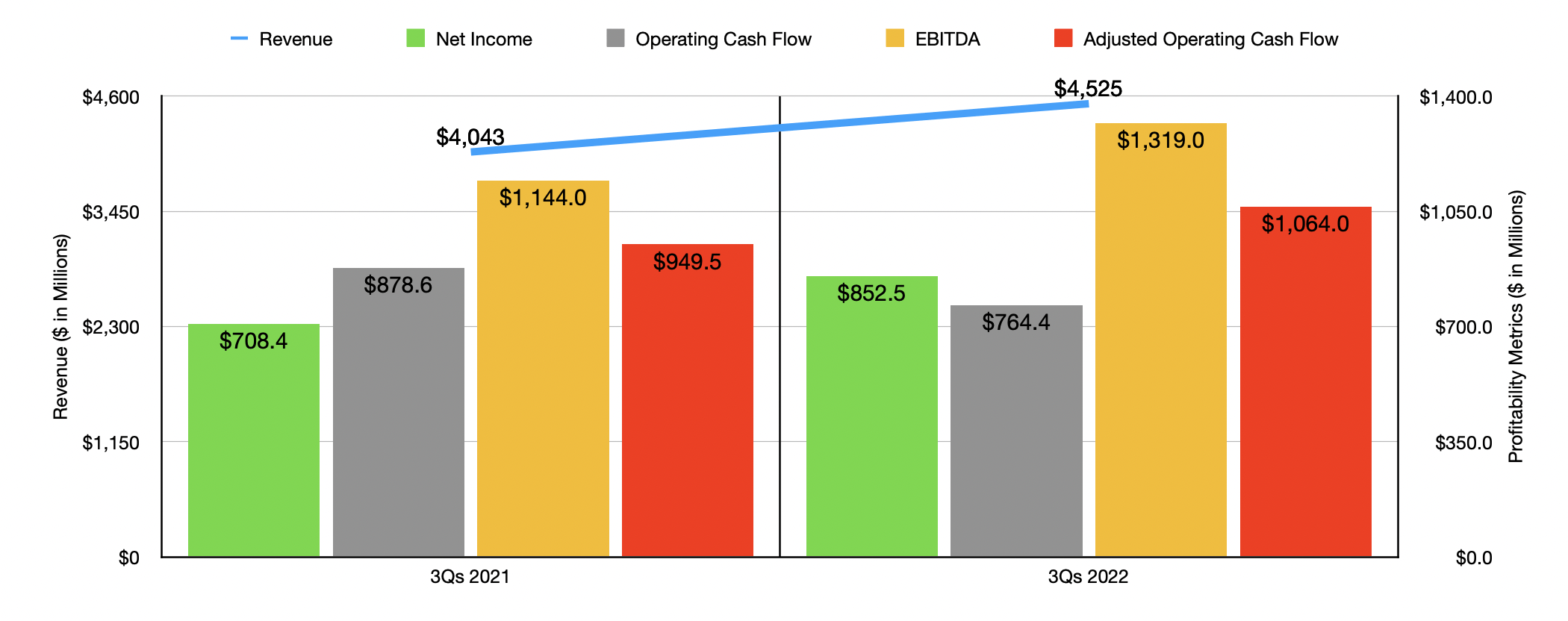

The third quarter of last year was only one of the quarters that were responsible for pushing up results year over year. For the first nine months of 2022 as a whole, the company did quite well, with sales of $4.53 billion beating out the $4.04 billion reported the same time of the 2021 fiscal year. The increase in revenue, combined with improved margins, helped push net income from $708.4 million to $852.5 million. Operating cash flow interestingly did fall, dropping from $878.6 million to $764.4 million. But if we adjust for changes in working capital, it would have risen from $939.5 million to $1.06 billion. And finally, EBITDA for the company expanded from $1.14 billion to $1.32 billion.

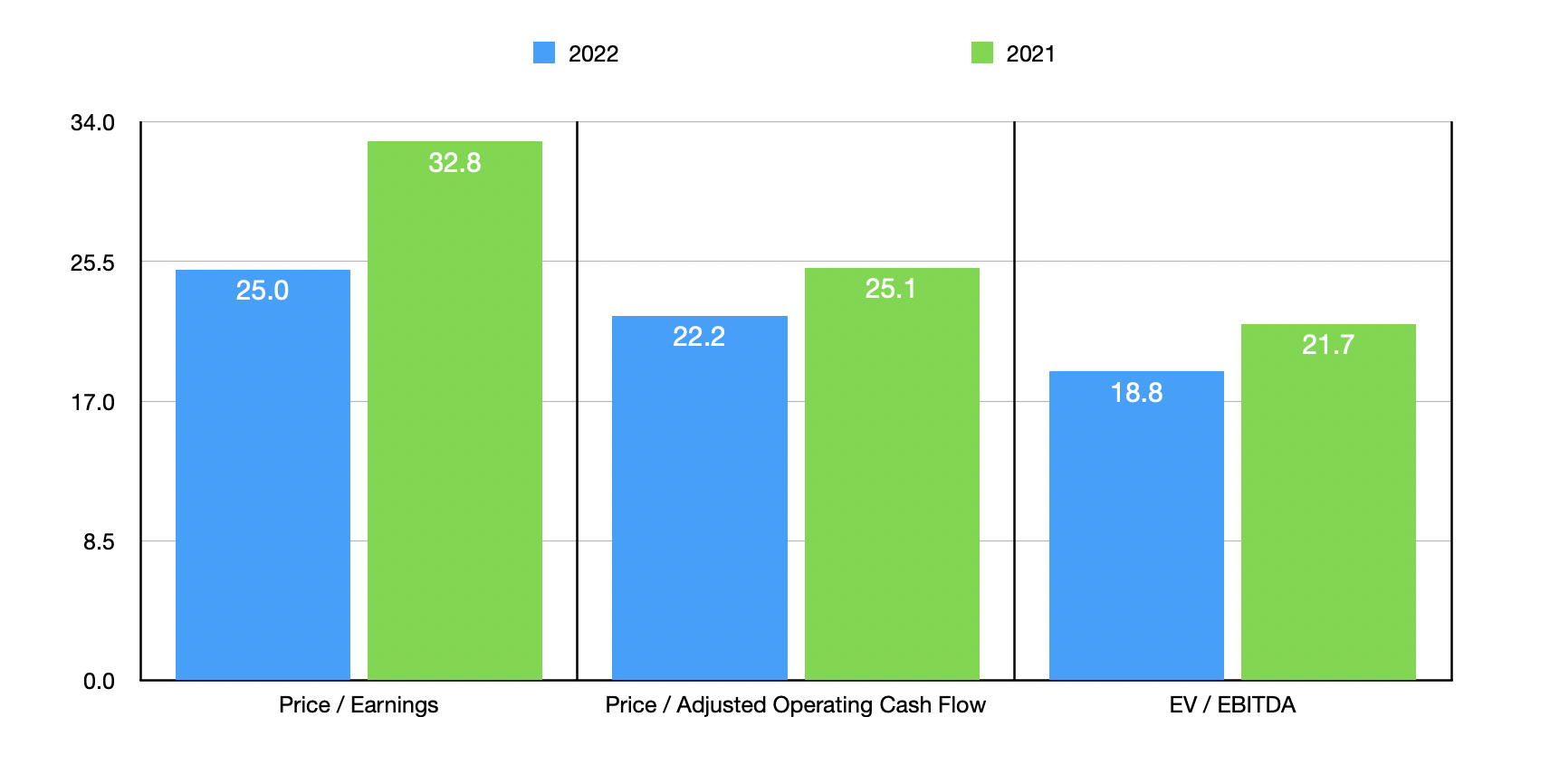

For the 2022 fiscal year in its entirety, management forecasted sales growth of roughly 10%. They also said that earnings per share should be between $5.61 and $5.63. Using the midpoint here, that should translate to net income of just under $1.30 billion. No guidance was given for the other profitability metrics. But based on the company's financial performance for the first nine months of the year, a reasonable estimate for adjusted operating cash flow should be $1.46 billion, while EBITDA should come in at around $1.84 billion.

{kind=link}

Based on these figures, the company is trading at a price-to-earnings multiple of 25. The price to adjusted operating cash flow multiple is 22.2. And the EV to EBITDA Multiple should come in at around 18.8. If, instead, we were to use data from the 2021 fiscal year, these multiples would be 32.8, 25.1, and 21.7, respectively. As part of my analysis, I decided to compare the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 4.2 to a high of 41.3. When it comes to the price to operating cash flow approach, the range was from 4.5 to 50.6. In both of these cases, three of the five companies were cheaper than our target. Using the EV to EBITDA approach, the range was from 2.2 to 23.9. In this scenario, four of the five companies were cheaper than AMETEK.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| AMETEK |

| 25.0 |

| 22.2 |

| 18.8 |

| Encore Wire Corporation ( WIRE ) |

| 4.2 |

| 4.5 |

| 2.2 |

| Atkore ( ATKR ) |

| 5.8 |

| 6.6 |

| 3.8 |

| Allied Motion Technologies ( AMOT ) |

| 41.3 |

| 50.6 |

| 16.0 |

| Acuity Brands ( AYI ) |

| 15.8 |

| 14.0 |

| 9.5 |

| Rockwell Automation ( ROK ) |

| 33.6 |

| 38.0 |

| 23.9 |

Takeaway

By pretty much every fundamental account, AMETEK seems to be doing quite well for itself. In the long run, I suspect that this trend will continue. But this doesn't mean that the company makes for a prime investment opportunity at this moment. Shares of the company do look quite lofty at this moment and they look slightly pricey compared to similar firms. All of these items considered together have led me to believe that a ‘hold’ rating is still appropriate at this time, but that continued share price appreciation could lead to the stock becoming overpriced and warranting a meaningful downgrade.

For further details see:

Ametek: Shares Are Getting Rather Pricey