HZNP - Amgen: Not An Investment Mistake But It Was Better Before

2023-09-07 11:35:48 ET

Summary

- Amgen could report great quarterly results with revenue, operating income and EPS growing with a solid pace.

- The stock is undervalued in my opinion and Amgen could be seen as a good investment.

- However, I think the Horizon acquisition was not the best use of cash and the high debt levels of Amgen are a red flag.

In my last article about Amgen Inc. ( AMGN ), I questioned the acquisition of Horizon Therapeutics Plc ( HZNP ), and I switched my rating from "Buy" to "Hold". In the meantime, the stock increased about 6.5% and clearly underperformed the S&P 500 ( SPY ), which gained about 13%. News stories of the last few days are indicating that Amgen will be able to close the deal in a few weeks as most approvals, which are necessary, have been granted.

This is a good time to look at Amgen and the acquisition once again and assess if the stock is a good investment or not. But we start by looking at the last quarterly results.

Quarterly Results

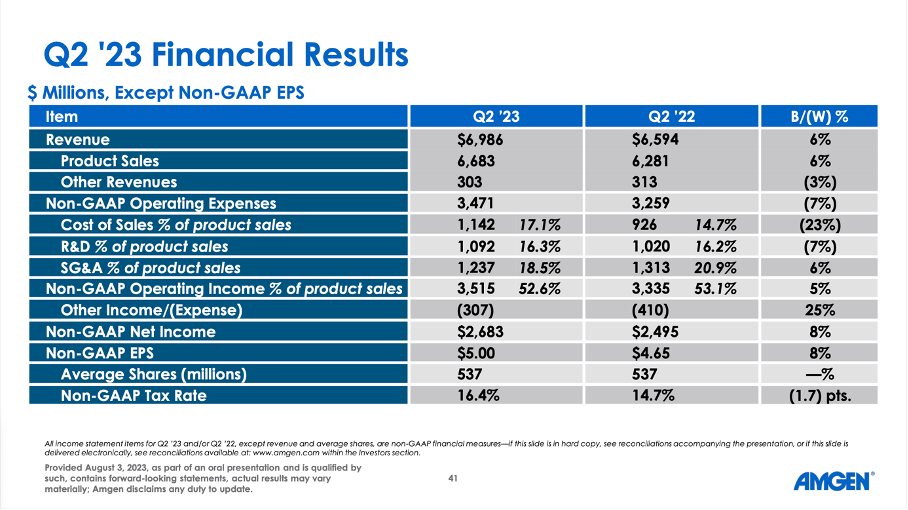

We start by looking at the last quarterly results, which were quite good and the company reported the highest quarterly growth rates for revenue and operating income in a long time. Total revenue increased from $6,594 million in Q2/22 to $6,986 million in Q2/23 - resulting in 5.9% year-over-year growth. Operating income increased even 23.3% year-over-year from $2,176 million in the same quarter last year to $2,684 million this quarter. And diluted earnings per share increased from $2.45 in Q2/22 to $2.57 in Q2/23 - resulting in 4.9% year-over-year growth.

{kind=link}

And non-GAAP earnings per share increased 7.5% year-over-year from $4.65 in Q2/22 to $5.00 in Q2/23 while free cash flow more than doubled. Compared to a free cash flow of $1,684 million in the same quarter last year, Amgen reported a free cash flow of $3,838 million this quarter - resulting in 128% year-over-year growth. And while the free cash flow a year ago was rather low (which explains the high growth rates), we still can see the free cash flow this quarter being exceptionally high.

During the last earnings call , management also commented on the free cash flow:

The company generated $3.8 billion of free cash flow in the second quarter of 2023 versus $1.7 billion in the second quarter of 2022, primarily driven by the timing of tax payments and includes higher interest income and higher operating income. We expect strong cash flow for the remainder of the year, consistent with our full year 2023 financial outlook and includes a non-GAAP operating margin of roughly 50%.

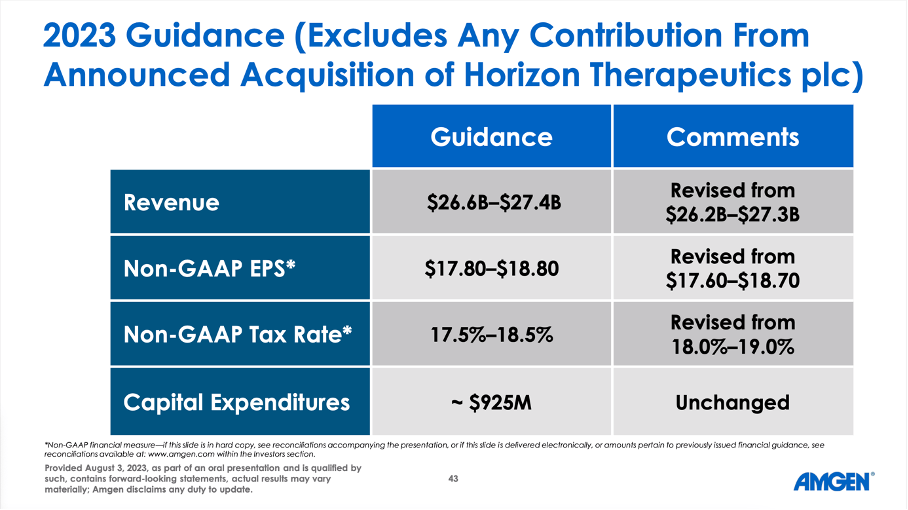

And not only is management expecting strong cash flow for the rest of the year, the company also raised its guidance for revenue as well as non-GAAP earnings per share. Amgen is now expecting revenue to be in a range of $26.6 billion to $27.4 billion and non-GAAP earnings per share in a range of $17.80 to $18.80. It is important to point out that the guidance is excluding any contributions from the acquisition of Horizon Therapeutics - we will get to this later.

{kind=link}

Results in More Detail

In total, product sales growth was driven by 11% volume growth, which was partially offset by 2% lower net selling price as well as 1% negative impact from foreign exchange. The two top selling products remain Prolis (which generated $1,028 million in quarterly revenue) and Enbrel ($1,068 million in quarterly sales).

{kind=link}

For the coming quarters, Amgen is expecting higher volume for Enbrel (due to new patients) but a declining net selling price. And considering the "patent cliff" for Amgen in 2023 - for Enbrel as well as Prolia major patents expire in 2023 - this is great news. During the earnings call, CEO Bob Bradway commented on Enbrel being strong despite competition:

Yes, you're right. Enbrel has - did have a strong quarter and is benefiting from quite frankly, the best access we've ever had on Enbrel, where we're covered across all the major PBMs now. So we're seeing really nice new patient growth on Enbrel, so more new patients coming onto treatment with Enbrel, and we think that that will support sustained volume through the course of the year. We did give up a bit of price to do that, so that's also flowing through Enbrel. But overall, I think there was some concerns perhaps last quarter that the biosimilar activity in this category was somehow impacting Enbrel. And I was pretty clear last quarter that wasn't what we were seeing. And it's definitely now clear in second quarter that biosimilar competition for Humira is not negatively impacting Enbrel. So we're - we see stability in Enbrel going forward.

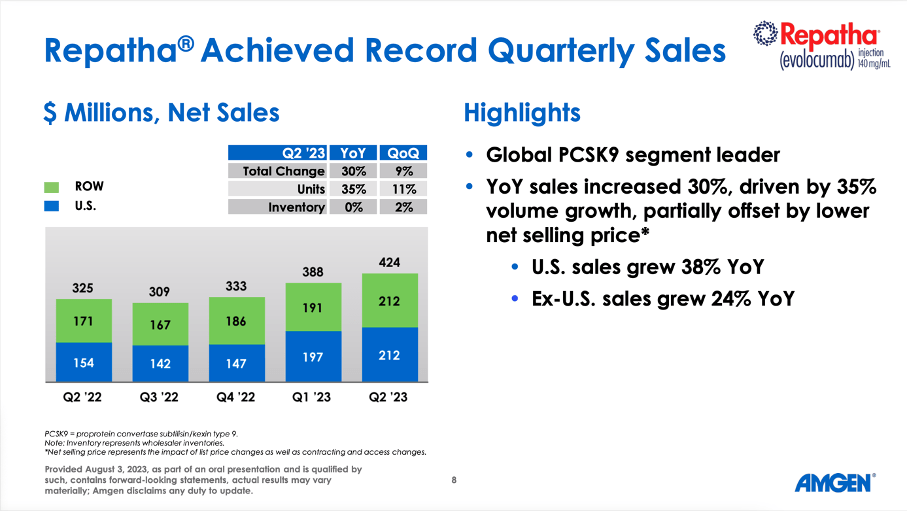

And when focusing on Repatha, which has "full patent protection" at least till 2028/2029 in Europe and the United States, we see strong growth. Repatha generated $424 million in sales last quarter - a 30% increase compared to the same quarter last year. The growth was once again driven by higher volume but offset by a lower net selling price.

{kind=link}

Another driver of growth was EVENITY, which complements Prolia in the company's "bone portfolio". In Q2/23, EVENITY generated $281 million in sales resulting in 47% year-over-year growth. The increase was once again driven by volume growth.

Horizon Acquisition

Aside from high growth rates in the second quarter, the major news story in the last few months regarding Amgen was the acquisition of Horizon Therapeutics. I already wrote about the acquisition in my last article about Horizon Therapeutics and I was not so euphoric about the acquisition - in contrast to Amgen management:

Turning to our planned acquisition of Horizon Therapeutics, we remain very enthusiastic about what our companies can achieve together for patients suffering from rare serious diseases. Horizon has certainly accomplished a great deal as an independent company. Amgen's global commercial manufacturing and R&D capabilities, especially for biologic products, will enable Horizon's medicines to reach even more patients more quickly than Horizon could have achieved on its own.

And last week it was reported that the Federal Trade Commission settled with Amgen over the Horizon acquisition. As part of the agreement , Amgen must fulfill a few conditions:

Under the proposed order , Amgen is prohibited from bundling an Amgen product with either Tepezza or Krystexxa, Horizon's medications used to treat thyroid eye disease ((TED)) and chronic refractory gout ((CRG)), respectively. In addition, Amgen may not condition any product rebate or contract terms related to an Amgen product on the sale or positioning either one of these drugs. Amgen also is barred from using any product rebate or contract term to exclude or disadvantage any product that would compete with Tepezza or Krystexxa."

And the Irish high Court has set a hearing for October 5, 2023 on the planned acquisition. The approval from the Irish High Court is the last remaining clearance necessary before Amgen can go through with the acquisition.

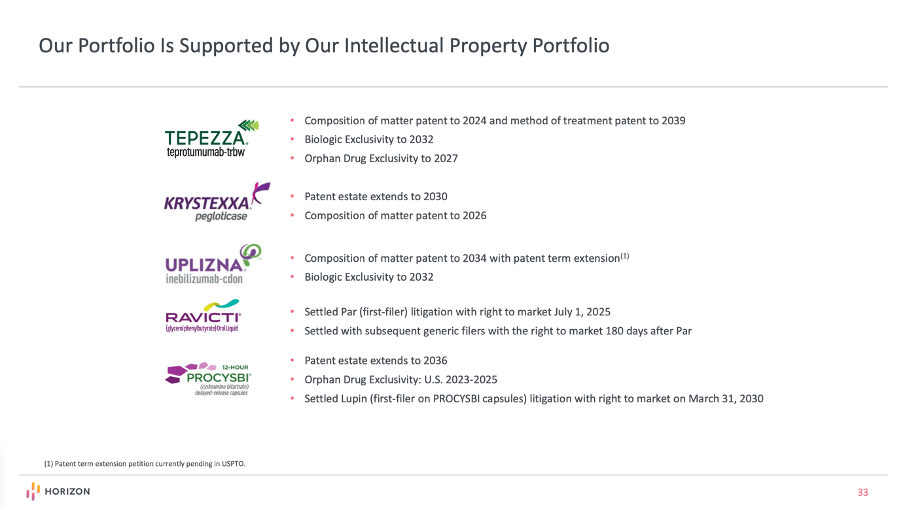

When looking at Horizon Therapeutics, we see a business already generating billions in revenue and a few products that have either reached blockbuster status or a rather close. Often billions are paid for pharmaceutical companies that have no real revenue yet - in case of Horizon Therapeutics it is different. And the major products are also patent protected for quite some time.

Horizon Therapeutics Q2/23 Presentation

{kind=link}

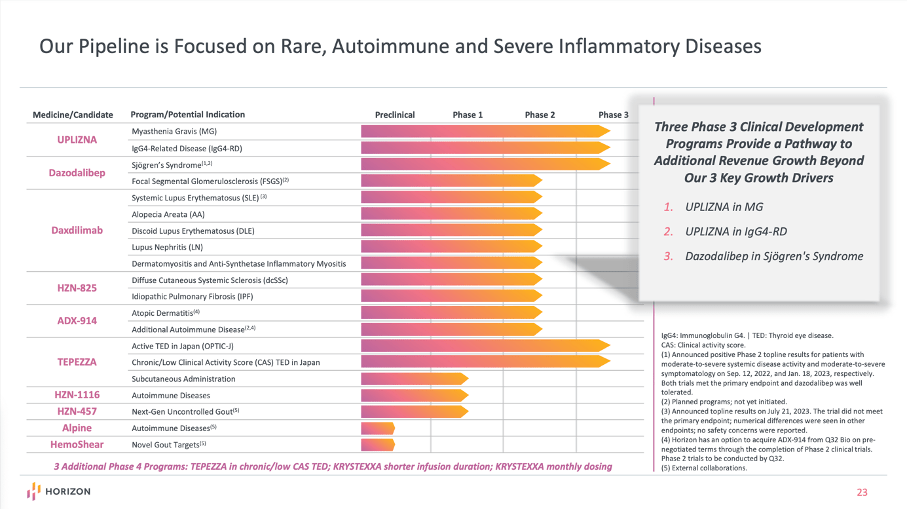

And aside from the pharmaceuticals already introduced to the market, Horizon Therapeutics has a solid pipeline with several medicines in phase 2 and a few candidates already in phase 3.

Horizon Therapeutics Q2/23 Presentation

{kind=link}

In Q3/22 (earnings release), Horizon estimated Tepezza peak sales globally being greater than $4 billion as management got more optimistic about non-U.S. sales (estimating now at least $1 billion in sales). In Q2/23, Tepezza sales were $445 million and in the first half of 2023, sales were $850 million - implying an upside of more than 100% for sales in the years to come. But we also must point out that Horizon had to report declining sales for Tepezza in the last two quarters.

In its Q1/22 presentation , Horizon Therapeutics provided more information about estimated peak sales for different products. Back then, management estimated above $1 billion in U.S. annual sales for Krystexxa (and with $431 million in sales in the first half of 2023 we are rather close to this estimate). Additionally, management is expecting peak sales above $1 billion for Uplizna, which generated only $122 million in sales in the first half of 2023, and we therefore see a huge upside potential here. And so far, Uplizna is growing with a high pace.

Of course, it is always difficult from the outside to assess the pipeline of a pharmaceutical business and to estimate peak sales for the different products. I don't think Horizon Therapeutics is a bad business and that Amgen made a terrible mistake. However, I think Amgen could have used its free cash flow (and cash reserves) maybe in a better way as the price for the business was rather high - and Amgen had to take on huge amounts of debt for the acquisition.

Debt Levels Too High

The major concern in my last article were the high debt levels for Amgen - as consequence from the acquisition. I wrote:

One of the major news stories about Amgen in the last few months was the planned acquisition of Horizon Therapeutics for $116.50 per share (or $27.8 billion in total). This would be one of the major pharmaceutical deals of the last few years and is probably the reason for Amgen reducing its share buyback program in fiscal 2023 to $500 million or less to preserve cash. And although share buybacks have always been an important part of Amgen's capital allocations strategy (see section above) and a smart move in my opinion, preserving cash seems like a good idea as the acquisition will have a huge negative impact on the balance sheet.

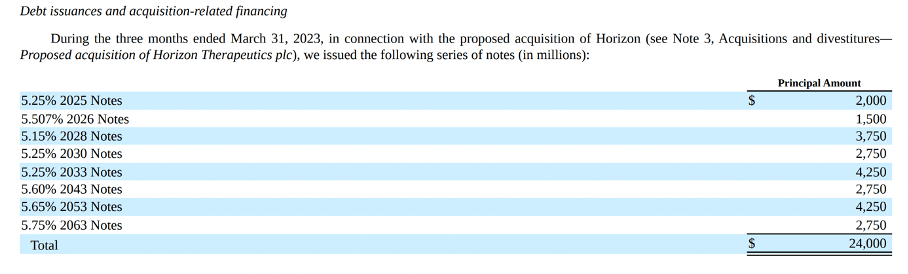

And not very surprisingly Amgen issued $23,798 million in additional debt in the first quarter of fiscal 2023 and with already existing cash on the balance sheet the deal will be financed. However, this had a huge impact on the balance sheet (also no surprise).

On June 30, 2023, the company had $34,248 million in cash and cash equivalents but we must keep in mind that Amgen will need $27.8 billion in cash for the Horizon acquisition and therefore about $6.5 billion in cash and cash equivalents will remain. On the liabilities side, Amgen has now $2,167 million in short-term debt as well as $59,377 million in long-term debt. Total stockholders' equity was $6,781 million.

When calculating a debt-equity ratio, we get a horrible number of 9.08. And while such a high D/E ratio is clearly a red flag, we should rather look at the free cash flow (or operating income) a business can generate annually and how long it will take to repay the outstanding debt. In the last twelve months Amgen could generate an operating income of $10,219 million and it would therefore take about 6 times the current operating income to repay the outstanding debt (when using the free cash flow, the calculation is similar).

{kind=link}

I am not worried about Amgen getting in trouble - part of the debt is due in 20, 30 or 40 years from now. But when just looking at these additional $24 billion in debt, Amgen has additional interest payments of around $1,300 million annually. This will result in almost $3 billion annual interest (at least in the next few years). The additional interest payments Amgen must make, are also much higher than the operating income Horizon Therapeutics can generate ($644 million in the last 12 months; the TTM was as high as $1,067 million a few quarters ago).

Finally, the acquisition will also add billions in goodwill to the balance sheet. Of course, when acquiring an asset light business that is depending on intangible assets (like patents, know-how and talent) it is difficult to avoid goodwill as the price paid for the business is almost always higher than the assets on the balance sheet are worth. Nevertheless, high amounts of goodwill are not great.

Summing up, the debt levels of Amgen are too high in my opinion and especially in an environment of rising interest rates I don't know if I want to invest in a business with such high debt levels.

Intrinsic Value

While the balance sheet of Amgen is anything but great (and a reason not to own Amgen), the different valuation metrics are speaking another language and are rather indicating that Amgen is an extreme bargain.

Right now, Amgen is trading for 16.8 times earnings and 13.8 times free cash flow. And for a business that has most likely an economic moat around and is also growing with a solid pace, this is a rather low valuation multiple and indicating an undervalued stock.

This assessment can also be backed up by using a discount cash flow calculation to determine an intrinsic value for the stock. As basis for our calculation, we can take the free cash flow of the last four quarters (which was $9,685 million and in line with previous results). Now we can add about $1 billion in free cash flow Horizon Therapeutics will contribute and subtract about $1.3 billion in additional interest payments (mentioned above). Let's be cautious and assume a free cash flow of $9 billion for the "new" Amgen business. When calculating with 10% discount rate and 537 million outstanding shares, Amgen must grow its free cash flow about 3% annually right now to be fairly valued.

When looking at results in the past, Amgen could grow its operating income with a CAGR of 5.54% in the last ten years and earnings per share with a CAGR of 8.17%. And growth even slowed down - Amgen could report even higher growth rates in previous years. Analysts are also cautiously optimistic and assume earnings per share to grow with a CAGR around 4.4%.

Therefore, we can make the argument for higher growth rates. In my opinion, 5% annual growth from now till perpetuity seems realistic for Amgen and would result in an intrinsic value of $335 for Amgen.

Conclusion

To be honest, I liked Amgen better before the acquisition and in my opinion, it would have been better to use the free cash flow (and maybe cash on the balance sheet) and repurchase shares as I considered Amgen's stock undervalued. But with the additional debt and the additional annual interest payments, I don't think Amgen is such a great bargain anymore. And although I don't want to be bearish on the stock, I am torn between being neutral and slightly bullish. I also don't think you will make a mistake by buying Amgen at this point as it has a solid dividend yield of 3.35% (and the dividend seems to be safe). But Amgen was a better investment before the acquisition - at least in my opinion.

For further details see:

Amgen: Not An Investment Mistake, But It Was Better Before