HZNP - Amgen: Questioning The Horizon Therapeutics Acquisition

2023-03-24 05:18:59 ET

Summary

- Amgen reported solid results for fiscal 2022 with the bottom line growing in the double digits.

- The company recently announced the acquisition of Horizon Therapeutics and while the acquisition might make sense it is increasing the total debt to rather extreme levels.

- While Amgen is undervalued from a fundamental point of view, I rather consider the stock a hold due to the debt levels.

In my last article I called Amgen ( AMGN ) a good pick for the next recession as the business can be seen as rather recession-resilient. And I would still see it this way and consider Amgen a good investment if it wasn't for the acquisition of Horizon Therapeutics ( HZNP ) and the resulting huge debt levels Amgen will have after the acquisition. In the last few months, AMGN stock declined about 22% from the previous high as investors obviously seem to have similar doubts about the merger. Let's take another look at the business and stock price to determine if Amgen is still a buy.

Annual Results and Guidance

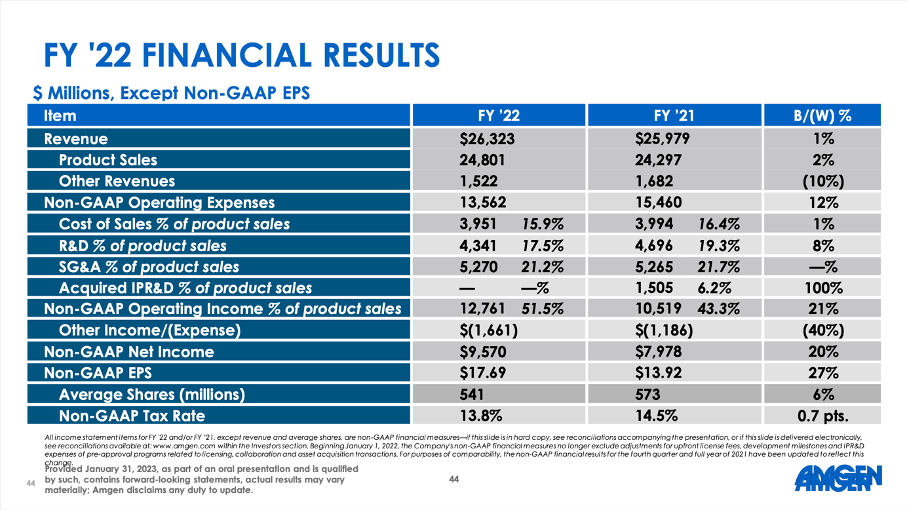

Annual results for fiscal 2022 were not great as top line growth slowed down, but they also were not terrible either. Product sales increased from $24,297 million in fiscal 2021 to $24,801 million in fiscal 2022 and total revenue increased 1.3% year-over-year from $25,979 million in the previous year to $26,323 million in fiscal 2022. But while the top line grew only slightly, operating income increased 25.2% year-over-year from $7,639 million in fiscal 2021 to $9,566 million in fiscal 2022. And diluted earnings per share increased from $10.28 in the previous year to $12.11 in fiscal 2022 - resulting in 17.8% YoY growth.

{kind=link}

And adjusted earnings per share increased even 27.0% from $13.92 in fiscal 2021 to $17.69 in fiscal 2022. Although many see the results as rather underwhelming, we also must acknowledge that Amgen is reporting high growth rates for operating income as well as the bottom line.

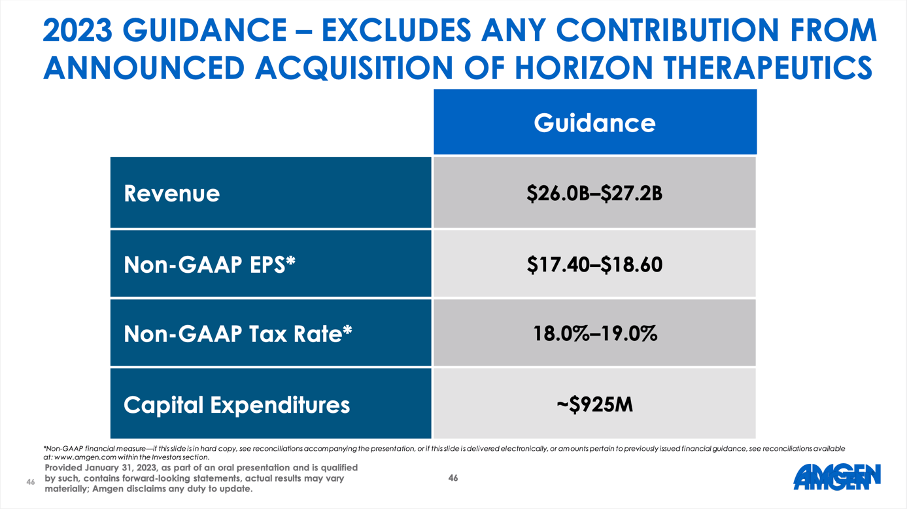

The guidance for fiscal 2023 was also seen as reason for disappointment. Total revenue is expected to be in a range between $26.0 billion and $27.2 billion, which would either mean a small decline or in the best case about 3% growth.

{kind=link}

And while earnings per share on a GAAP basis are expected to be in a range between $13.16 and $14.41 - and therefore reflecting about 8.5% to 19% growth - non-GAAP earnings per share are expected in a range between $17.40 and $18.60. And this would either mean a decline of 2% in the worst case or an increase of 5% in the best case. In my opinion, this is not the best guidance a company can give but considering a potential difficult year 2023 ahead of us, the guidance is also no reason for outrage or disappointment.

Capital Allocation

One reason for the rather moderate bottom line growth for fiscal 2023 might be the announcement of Amgen's management that share repurchased will not exceed $500 million in fiscal 2023. And when considering the huge amounts Amgen spent in the past on share buybacks, this is certainly worth mentioning.

| 2022 | 2021 | 2020 | 2019 | 2018 | |

|---|---|---|---|---|---|

| Share Buybacks | |||||

| $6,360 million | |||||

| $4,975 million | |||||

| $3,486 million | |||||

| $7,702 million | |||||

| $17,794 million |

And while Amgen will decrease the amounts spent on share buybacks dramatically, it still increased the dividend 9.8% last time from a previous quarterly dividend of $1.94 to a quarterly dividend of $2.13 right now. This is in line with the 5-year dividend growth rate of 10.76% and is resulting in a current dividend yield of 3.66%.

However, when comparing the expected annual dividend of $8.52 to earnings per share of $12.11 in fiscal 2022, we get a payout ratio of 70% which is rather high. In combination with rather low growth expectations for fiscal 2023 we must be cautious if Amgen can continue increasing its dividend with a similar pace. When comparing the annual dividend to the non-GAAP earnings instead, we get a payout ratio of only 48% which should make us more confident that Amgen will be able to increase its dividend in the years to come.

Horizon Therapeutics Acquisition

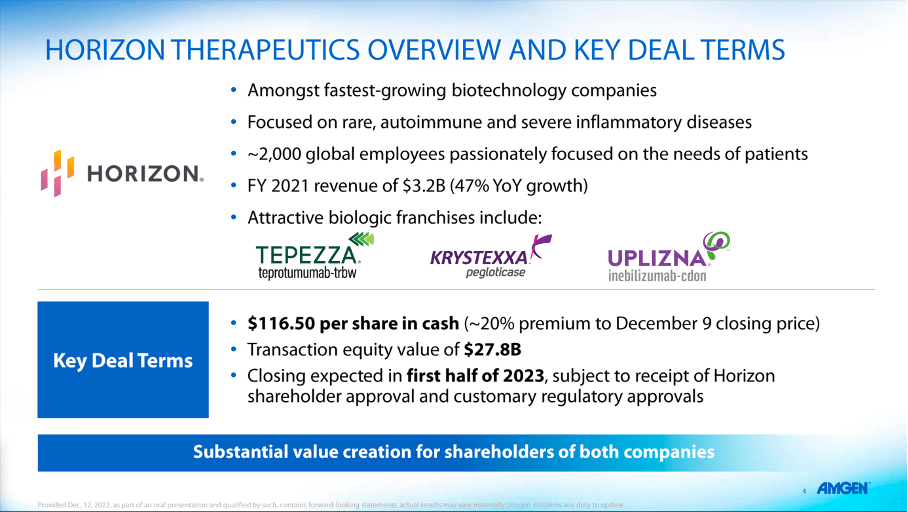

One of the major news stories about Amgen in the last few months was the planned acquisition of Horizon Therapeutics for $116.50 per share (or $27.8 billion in total). This would be one of the major pharmaceutical deals of the last few years and is probably the reason for Amgen reducing its share buyback program in fiscal 2023 to $500 million or less to preserve cash. And although share buybacks have always been an important part of Amgen's capital allocations strategy (see section above) and a smart move in my opinion, preserving cash seems like a good idea as the acquisition will have a huge negative impact on the balance sheet.

Amgen Horizon Therapeutics Acquisition

{kind=link}

When looking at the balance sheet on December 31, 2022, we already see an imperfect balance sheet. Short-term debt was $1,591 million and long-term debt was $37,354 million. When comparing the total debt of $38,945 million to the stockholders' equity of $3,661 million we get a terrible debt-equity ratio of 10.6. And when comparing the total debt to the operating income of fiscal 2022 (which was $9,566 million) it would take a little more than four years to repay the outstanding debt. However, when also considering cash and cash equivalents of $9,305 million it would take only about 3 years to repay the outstanding debt.

But now we also must consider the acquisition of Horizon Therapeutics. In mid-February it was reported that Amgen sold a $24 billion investment-grade bond with the company raising notes in eight parts. This will increase Amgen's total debt to over $60 billion and lead to - in my opinion - unacceptable metrics for solvency.

We can assume about $1 billion in operating income from Horizon Therapeutics and even when being optimistic and assuming about $10.5 to $11 billion in operating income after the deal, it would take Amgen about 6 years to repay the outstanding debt. Of course, both Amgen (and especially Horizon Therapeutics) have the potential to grow the operating income in the years to come, but in my opinion, Amgen would be highly leveraged after the deal and that is barely acceptable for an investment. And Amgen also had rather high debt levels - since 2014 the total debt did not really decline below $30 billion, but now debt will almost double.

Growth

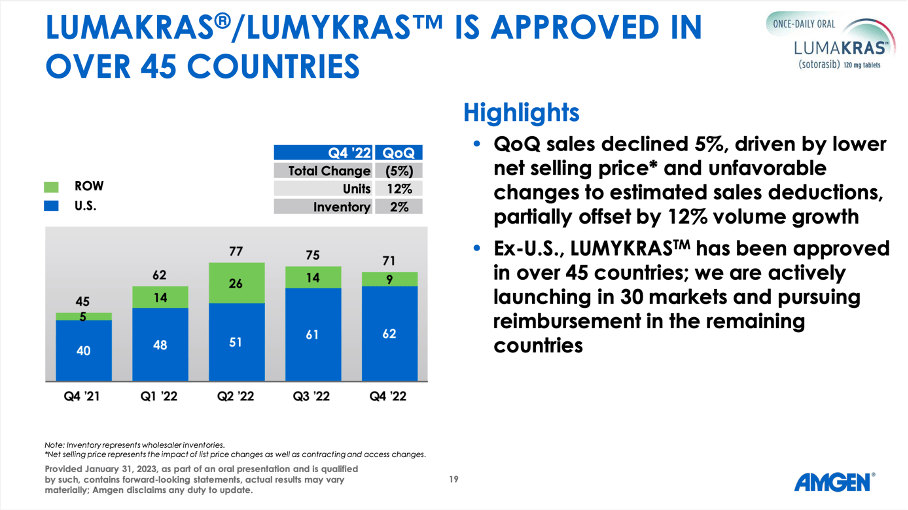

When talking about the growth potential in the years to come, we can start by looking at Amgen's core business - and we see light and shadow. For example, Lumakras, about which I was rather optimistic in my last article (although I mentioned there are warnings signs about growth slowing down) turned out to be a disappointment so far.

{kind=link}

In the fourth quarter, the company still increased sales 58% year-over-year to $71 million. But sales peaked in Q2/22 and in the following two quarters sales declined - especially sales outside the United States were rather a disaster.

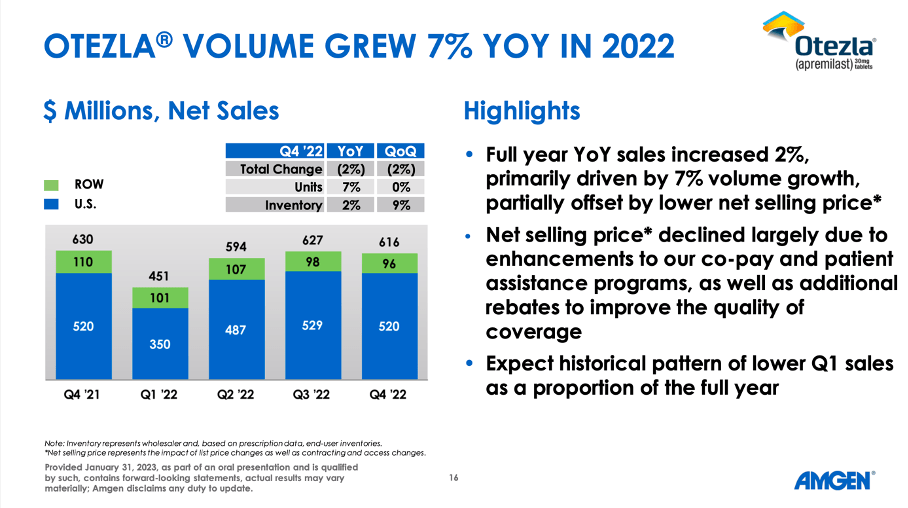

On the other hand, Amgen is still reporting growth for Otezla, which grew its volume 7% in 2022 and full year sales increased 2%.

{kind=link}

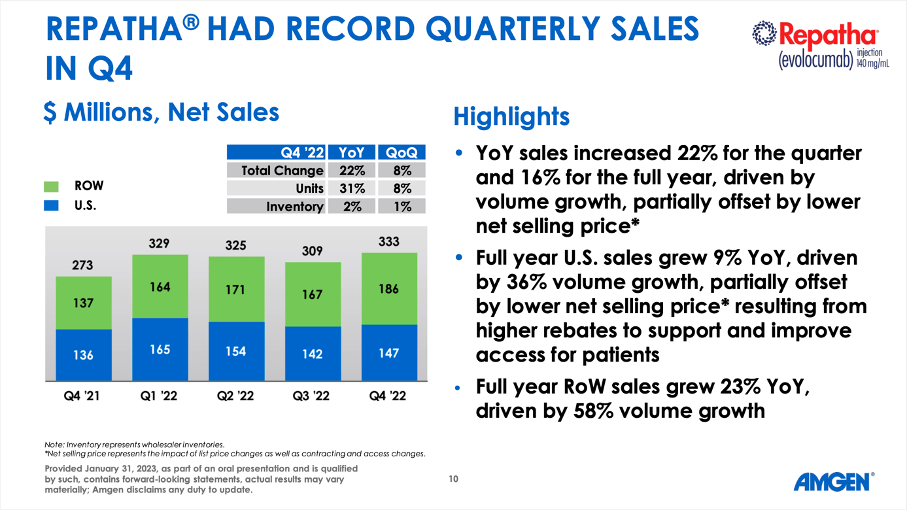

Aside from Otezla, Repatha had record quarterly sales in the fourth quarter of fiscal 2022 and sales increased 16% for the full year of fiscal 2022 - driven mostly by volume growth.

{kind=link}

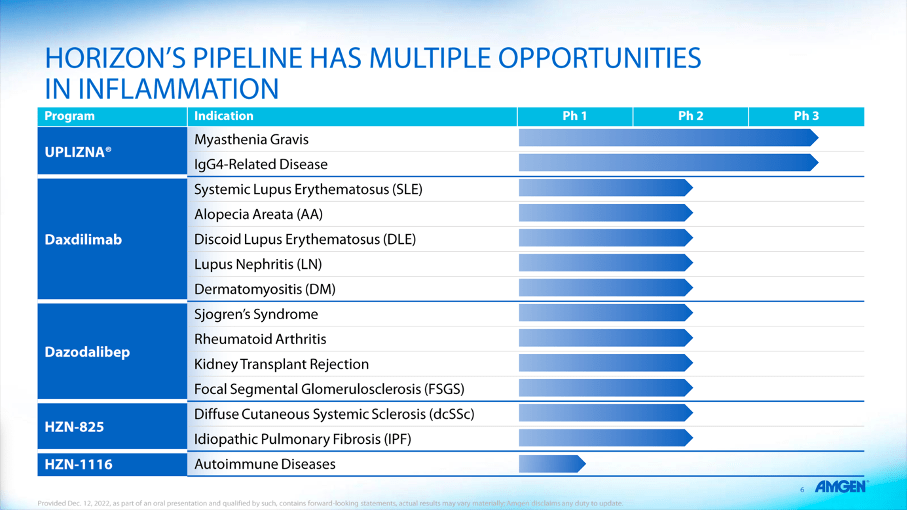

And when talking about potential growth in the years to come, we can focus especially on the acquisition of Horizon Therapeutics. Aside from $1.4 billion in non-GAAP operating cash the business is generating annually right now and the expected $500 million in annual cost synergies, Horizon Therapeutics is expected to contribute to growth in the years to come. First, we can mention the pipeline of Horizon Therapeutics with about 20 development programs and several potential drugs being in stage II and two already being in stage III.

Amgen Horizon Therapeutics Acquisition

{kind=link}

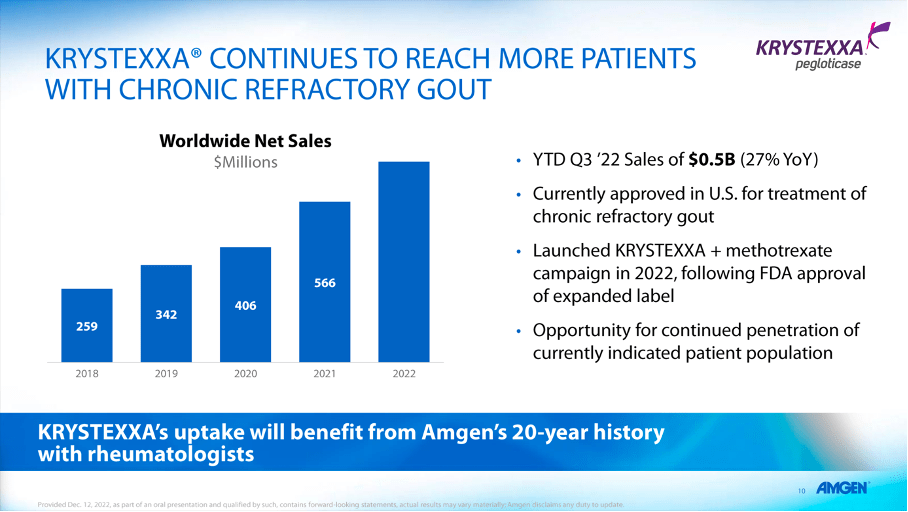

Horizon Therapeutics is not only bringing new potential drugs to the table but is already generating revenue due to several very successful drugs. One of them is Krystexxa which reported $716 million in sales in fiscal 2022 and is growing with a high pace.

Amgen Horizon Therapeutics Acquisition

{kind=link}

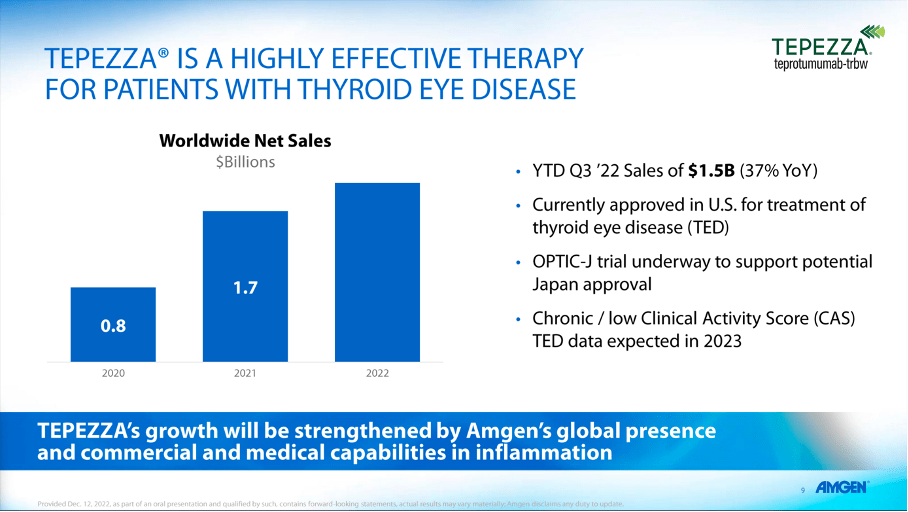

Another drug worth mentioning is Tepezza, which generated almost $2 billion in sales in fiscal 2022 and grew 18% year-over-year.

Amgen Horizon Therapeutics Acquisition

{kind=link}

A third drug worth mentioning is Uplizna, which generated $155 million in sales in fiscal 2022 and grew revenue 154% compared to the previous year. Horizon Therapeutics is expecting peak sales of at least $1 billion.

Intrinsic Value Calculation

Similar to many other biopharmaceutical companies, Amgen is still trading for rather low valuation multiples. When looking at the price-earnings ratio of 19, Amgen might seem rather expensive, but it is still below the average P/E ratio of 22.87. When looking at the more important price-free-cash-flow ratio instead, Amgen is trading only for 14 times free cash flow - in line with the 10-year average P/FCF ratio of 14.46. Additionally, using adjusted earnings per share, Amgen trade only 13 times earnings.

As always, I will calculate an intrinsic value for the stock by using a discount cash flow calculation. As basis we can take the free cash flow of the last four quarters, which was $8,785 million and in-line with the company's guidance for revenue and earnings per share (as well as capital expenditures being similar), we can assume free cash flow being similar in 2023 as in 2022. And when calculating with 539 million outstanding shares as well as a 10% discount rate, Amgen must grow its free cash flow about 3% to be fairly valued right now.

In my last article I calculated with 5% growth and considering the lower capital expenditures from 2024 going forward as well as the acquisition of Horizon Therapeutics contributing to the bottom line as well, I would assume 5% growth seems like a realistic assumption. When calculating with these assumptions, we get an intrinsic value of $325.97 for Amgen.

Conclusion

While Amgen still seems undervalued and a good buy from a valuation standpoint, I would be a little more cautious right now. As mentioned above, the extremely high debt levels and Amgen being highly leveraged (in my opinion) is making me cautious about Amgen as an investment and I don't know if the stock should be bought right now. As I explained in my last article (and other previous articles), Amgen certainly is a great business and recession-resilient, but I am not willing to accept such high debt levels. And the discount Amgen is currently trading for is certainly reasonable and when including the high debt levels into the equation, the stock price can be called fair and reasonable.

For further details see:

Amgen: Questioning The Horizon Therapeutics Acquisition