AMGN - Amgen: Wonderful Stock At Decent Price

2023-12-19 08:10:00 ET

Summary

- Amgen is a biotech company with a strong track record of returning capital to shareholders and maintaining high profitability.

- The company has outperformed the S&P 500 and other pharmaceutical peers in terms of total returns over the past decade.

- It has a robust pipeline of drugs and, unlike some peers, is reasonably valued with a respectable and well-covered dividend.

Screening and evaluating short-term stock buys can take a lot of time and energy, especially if one is looking to make a quick profit within a year or less. That’s because nobody, not even Warren Buffett, can predict where stocks will go next month, let alone next week.

Investing gets easier for those who are not in a cash crunch and can therefore afford to play the long game. In this case, you want to look for long-term compounders that produce strong returns on capital. With these types of investments, the starting valuation, while still important, may not matter as much over the long run.

This brings me to Amgen ( AMGN ), which as a strong track record of returning capital to shareholders while maintain high profitability in its own right. I last covered AMGN here back in August, highlighting its solid operating fundamentals on the back of robust performing drugs.

The stock has given investors a 14.6% total return since then, far surpassing the 5% rise in the S&P 500 ( SPY ). In this piece, I provide an update and discuss why AMGN remains decently priced for long-term investors at the present valuation, so let’s get started!

Why AMGN?

Amgen is a leading biotech company that produces therapeutics in the fields of oncology, inflammation, neurology, and pulmonary diseases. It also has a burgeoning biosimilars practices with drugs that mimic the behavior of off-patent blockbuster drugs like AbbVie’s ( ABBV ) Humira and Genentech’s ( RHHBY ) Herceptin.

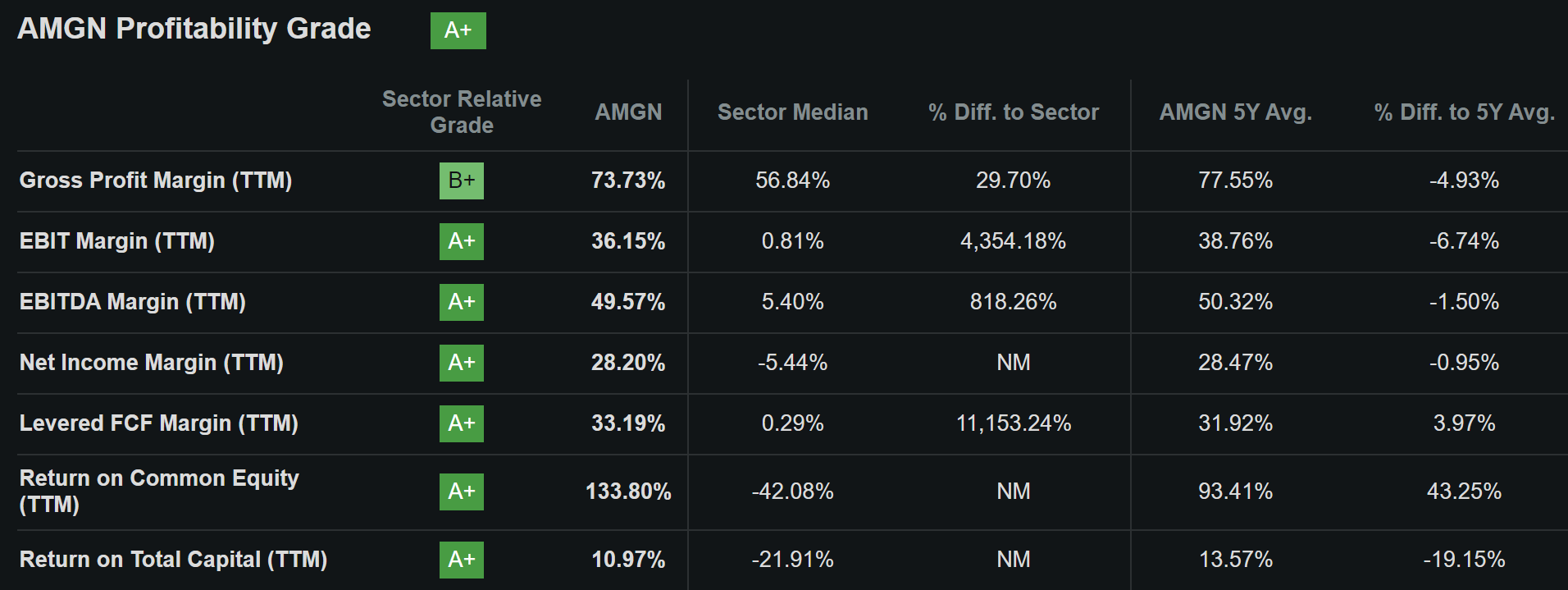

AMGN’s moat-worth drug franchises makes it a solid choice for those seeking stable and growing cash flows amidst economic uncertainty. That’s because healthcare is one of the most durable segments of the economy in the event of a recession. As shown below, AMGN has industry leading profitability with an A+ grade, driven by margins that are well in excess of the sector median. It also has a respectable 11% return on total capital and a 134% return on equity, due to its history of buying back shares.

{kind=link}

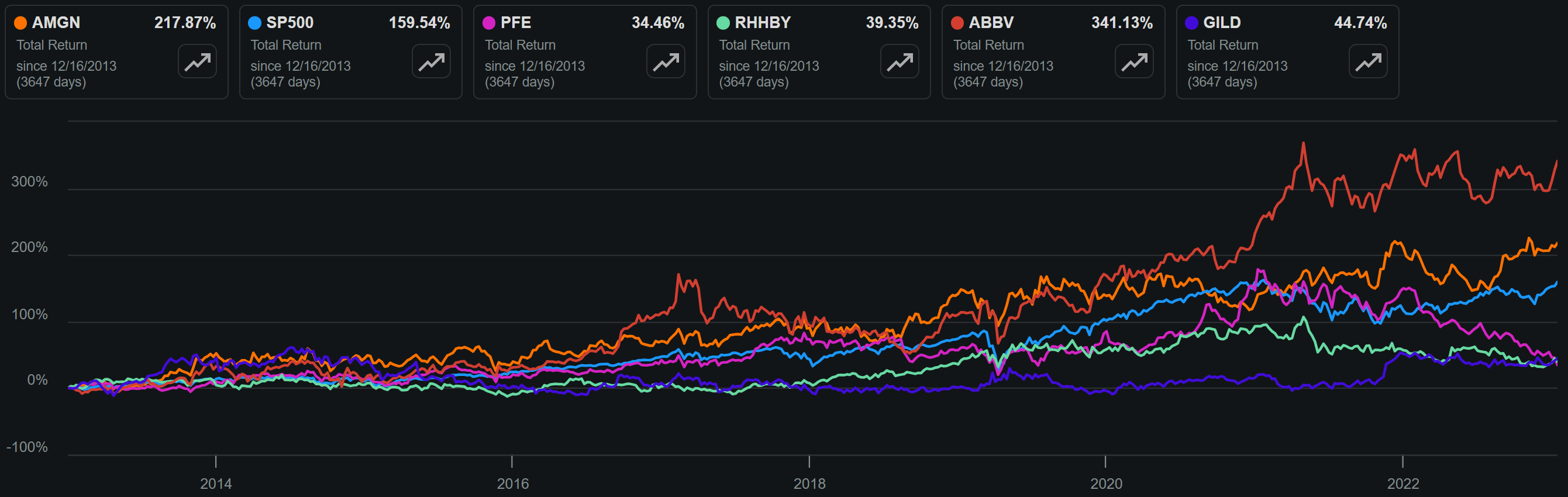

The high profitability combined with the aforementioned shareholder friendly nature of capital returns has resulted in impressive total returns for shareholders. As shown below, AMGN’s total return of 218% over the past decade has outperformed the S&P 500 as well as Pfizer ( PFE ), Roche (owner of close peer Genentech), and Gilead ( GILD ), while being outperformed by AbbVie due in large part to gains from their blockbuster drug, Humira.

AMGN vs. Peers' Total Return (Seeking Alpha)

{kind=link}

Meanwhile, AMGN has continued to generate growth since my last piece, with total revenue growing by 4% YoY to $6.9 billion during the third quarter. This was on the back of 11% volume growth, including double-digit volume growth from BLINCYTO (for treatment of lymphoblastic leukemia), EVENITY (osteoporosis), Repatha (cardiovascular disease), and Nplate (blood disorder). The strong Q3 results added to 3% total revenue growth for the first nine months of the year.

Looking ahead, AMGN has a robust pipeline that includes six potential first-in-class oncology assets , and three of these have earned Breakthrough Therapy designations from the FDA. Plus, in a nod to the success that Novo Nordisk ( NVO ) has seen with weight loss drug Ozempic, AMGN recently completed enrollment in its Phase 2 obesity study for its own drug, Maridebart cafraglutide.

Perhaps under-appreciated by the market is AMGN’s progress toward multi-specific drugs with AMG 193, as part of its acquisition of Nuevolution in 2019. Multi-specific drugs are an emerging therapeutic class that has the potential to revolutionize drug delivery. This is probably best described by the following note on the topic by PharmaFeatures :

For a long time, the pharmaceutical industry has relied on monolithic substances to deliver therapeutic outcomes. These substances would have to fulfill targeting criteria, pharmacokinetics and pharmacodynamics all on their own – not only did they have to deliver the desired effect, but they also had to deliver it to the right part of the body, for the right time. While this approach has yielded many successes, the rise of multi-specific drugs promises to revolutionize the number of substances we can use. Unlike traditional active ingredients, multispecific drugs can benefit from enhanced targeting and therapeutic impact – through the combination of diverse agents.

Of course, on top of most investors’ minds when it comes to AMGN is the recently closed acquisition of Horizon Therapeutics a couple months ago in the current fourth quarter. The closing of this deal combined with AMGN’s acquisition of ChemoCentryx last year significantly expands AMGN’s rare disease business and is expected to drive near-term growth.

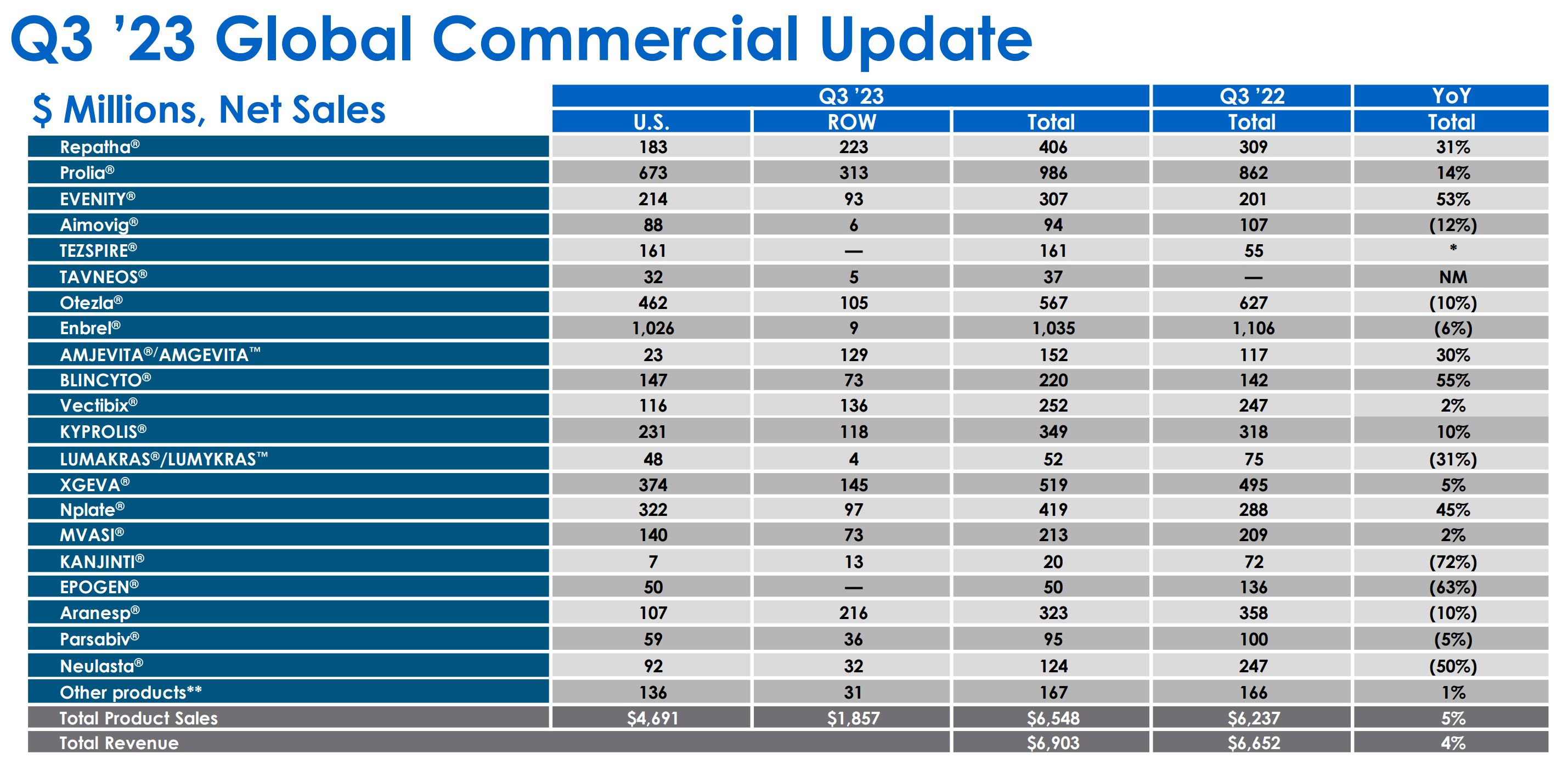

Notably, along with Horizon comes rare disease medicines Tavneos, Tepezza, KRYSTEXXA and UPLIZNA, which are early in their lifecycle, and are therefore expected to benefit from AMGN’s capabilities in process development, lifecycle management and manufacturing. These drugs are early enough in their lifecycles that they can offset AMGN’s upcoming loss of exclusivity in blockbuster drugs Enbrel, Prolia, and Otezla over the next few years.

As shown below, all three still generate robust sales ranging from $400 million to over $1 billion. While Prolia is seeing mid-teens revenue growth, Enbrel and Otezla are both starting to see their sales decline in the 6% to 10% range.

{kind=link}

Risks to AMGN include merger integration risks when it comes to Horizon Therapeutics, as there is always risk that incoming drugs may not add as much value to AMGN as previously anticipated. Also, AMGN’s legacy drugs like Enbrel and Otezla may have a faster than expected decline which may not be fully offset by newer drugs, and Medicare drug price negotiations will continue to be an overhang for the foreseeable future.

In addition, AMGN’s long-term debt balance is expected to land at $65 billion at the end of this year, an increase from $37 billion last year as a result of raising cash to pay for the Horizon acquisition. Fitch downgraded AMGN’s credit rating to BBB with stable outlook as a result of the acquisition. While AMGN ended Q3 with a safe net debt to TTM EBITDA ratio of 1.93x, I would expect for the leverage ratio to go higher over the next few quarters as Q4 would reflect the full balance sheet impact of the Horizon acquisition and it would take some time for Horizon’s newer drugs to significantly raise AMGN’s EBITDA.

Nonetheless, AMGN’s 3.3% dividend yield remains safe, as management implied confidence in the dividend payout with a 5.6% raise for the upcoming Q1 2024 payout. The forward dividend rate is also well-covered by a 46% payout ratio and comes with a 5-year dividend CAGR of 10%.

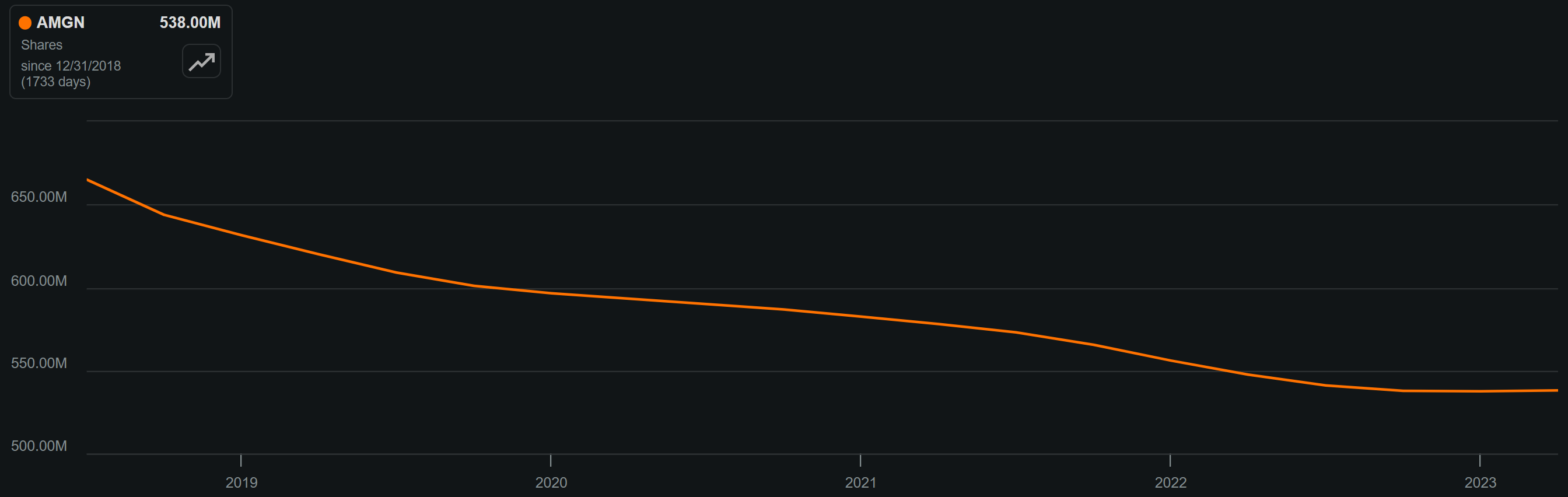

It’s also worth noting that AMGN has traditionally rewarded shareholders through share buybacks (which are more tax efficient) in addition to dividends. This includes a very robust 19% reduction in the share count over the past 5 years. While share buybacks have leveled off over the past 12 months, as shown below, I would expect for them to ramp up after debt gets paid down.

AMGN Shares Outstanding (Seeking Alpha)

{kind=link}

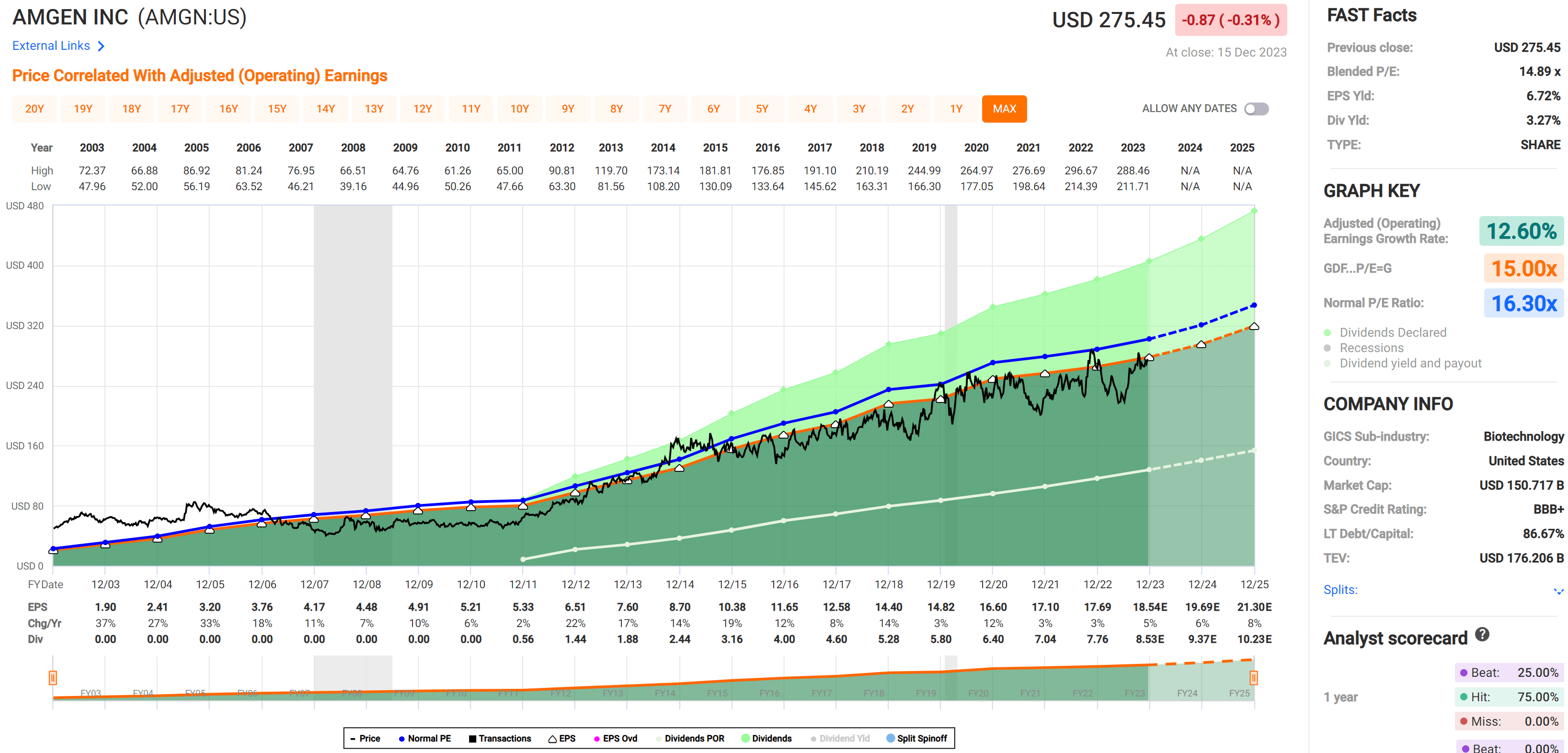

Turning to valuation, I no longer find AMGN to be a bargain at the current price of $275 with forward PE of 14.8, but I don’t find it to be expensive either. This is considering that AMGN trades below its normal PE of 16.3, its strong track record of shareholder returns, forward pipeline, and analyst expectations for 7-8% annual EPS growth over the next 2 years. These reasons put AMGN on better footing than peers like lower-valued Pfizer, and AMGN is far more reasonably valued than Eli Lilly ( LLY ) and Novo Nordisk which trade at forward PEs in the 36 to 86 range on weight loss drug optimism.

{kind=link}

Investor Takeaway

AMGN remains a strong player in the biopharmaceutical industry, with a diverse portfolio of drugs and a promising pipeline for continued growth. The company's acquisitions, including Nuevolution a few years ago and most recently, Horizon Therapeutics, have expanded its reach into new therapeutic areas and rare diseases, positioning it for long-term success.

Additionally, AMGN has a history of rewarding shareholders through dividends and share buybacks, making it an attractive investment option for investors seeking both growth potential and income. While AMGN is certainly no longer cheap, I continue to see value in the stock for long-term investors who prize the aforementioned attributes. As such, I maintain a 'Buy' rating on AMGN stock.

For further details see:

Amgen: Wonderful Stock At Decent Price