AMZA - AMJ: MLP ETN Beats All MLP ETFs

2023-11-20 10:04:22 ET

Summary

- MLPs are performing well despite lower energy prices.

- Midstream companies have low linkage to energy prices and benefit from capex discipline.

- The future looks bright for MLPs with expected record levels of US energy production and sector consolidation.

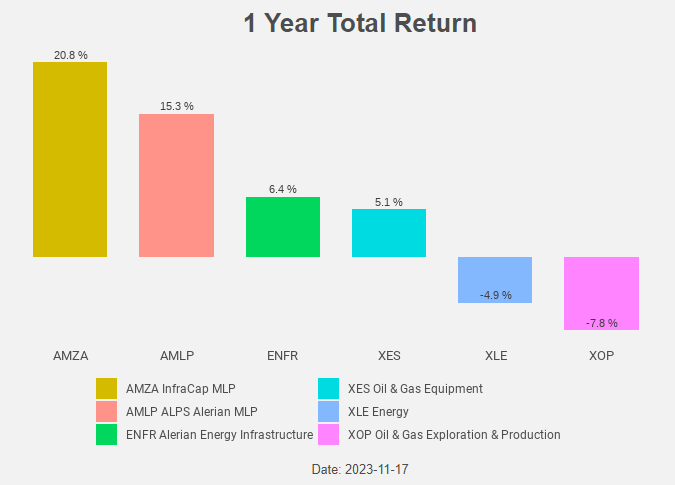

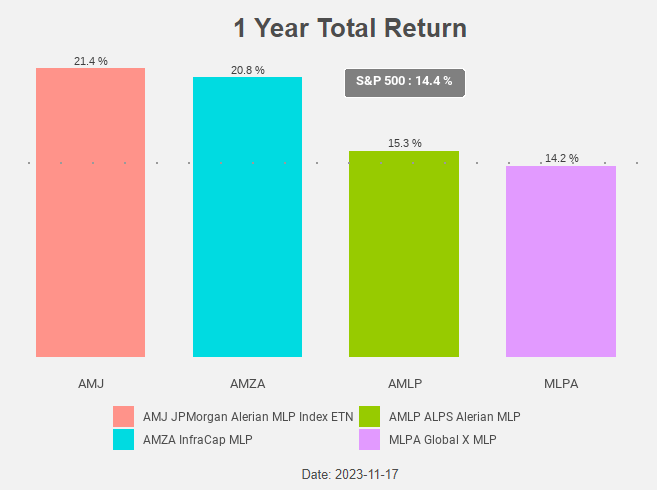

- AMJ is the best performing MLP ETF/ETN over the last twelve months.

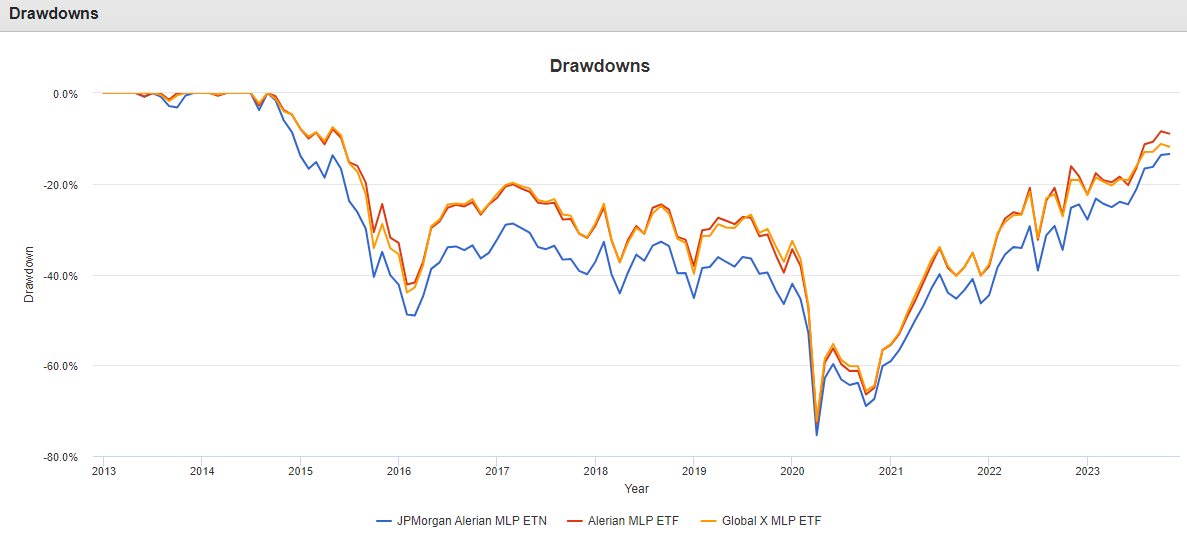

Despite lower energy prices, MLPs keep performing well. In previous articles we already made the case for MLPs in general and the ALPS Alerian MLP ETF ( AMLP ) and the more risky InfraCap MLP ETF ( AMZA ) in particular. Today we take a look at an MLP ETN: the JPMorgan Alerian MLP ETN ( AMJ ). AMJ is the best performing MLP ETF/ETN over the last twelve months.

Despite lower energy prices, MLPs are performing well

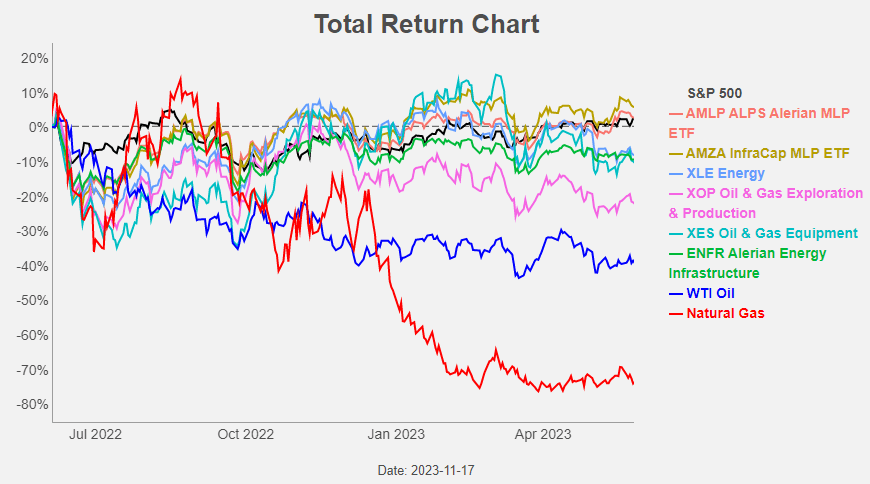

Oil and gas prices were in a down market between June 2022 and May of this year. This negatively impact energy ETFs like the SPDR S&P Oil & Gas Equipment & Services ETF ( XES ), the SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ) and Energy Select Sector SPDR ETF ( XLE ). MLP ETFs like AMLP and AMZA still managed to book a positive total return over that period.

{kind=link}

Over the past 12 months MLPs are also outperforming other energy ETFs, with the best performance for the higher beta AMZA.

{kind=link}

Midstream companies have indeed low linkage to energy prices. They get paid by the volumes they are transporting through their pipelines no matter what the price of oil is at that moment or how volatile the oil price is.

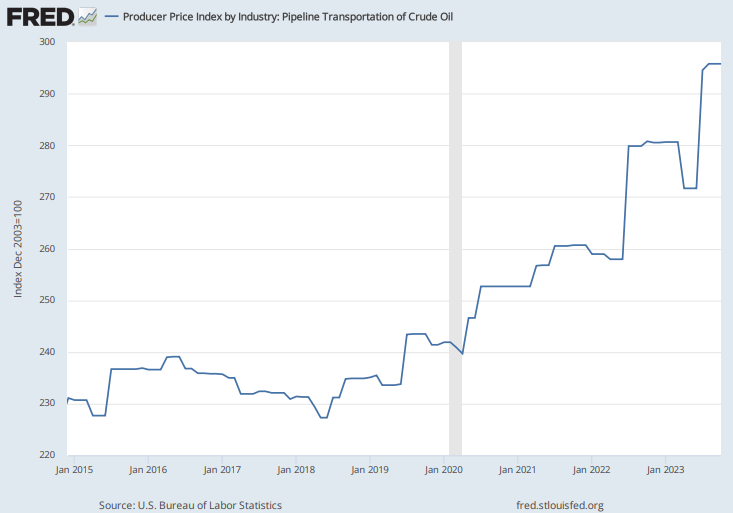

Capex discipline is not only present in the exploration and production part of the energy sector, but also in midstream. And this supports the pipeline transportation prices midstream MLPs can charge their customers.

Figure 3: Producer Price Index by Industry: Pipeline Transportation of Crude Oil (FRED)

{kind=link}

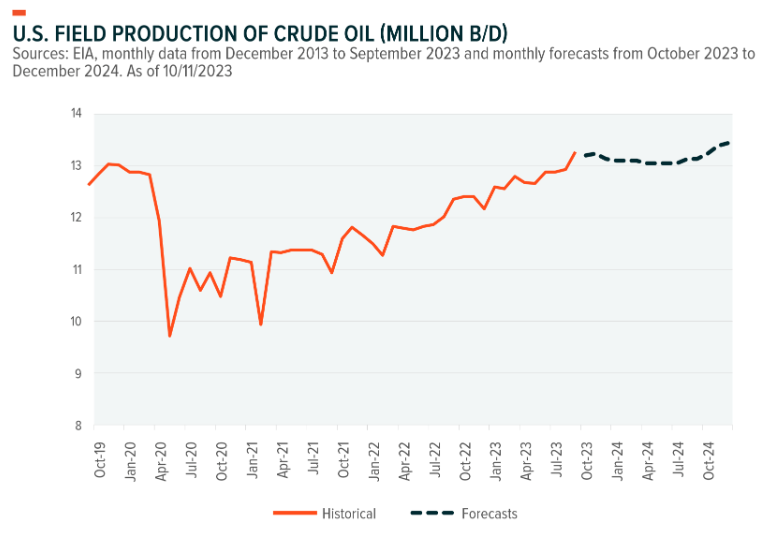

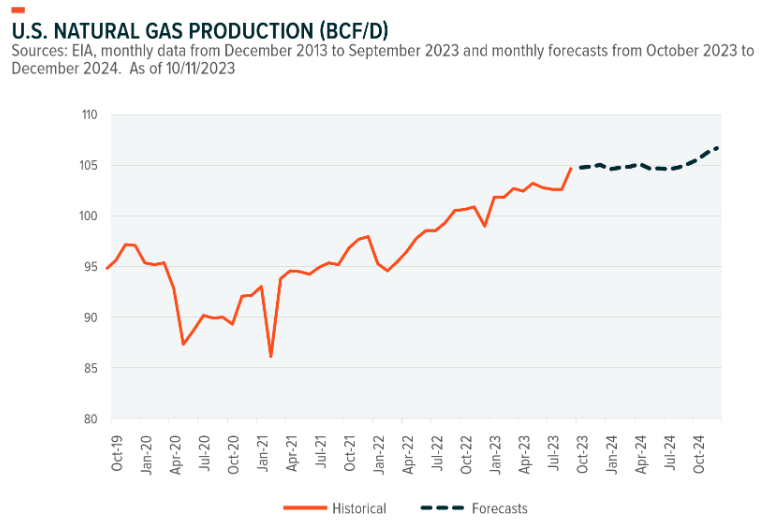

The future is looking bright not only for prices, but also for volumes. The EIA expects U.S. oil production averaging almost 13 million barrels a day (Mb/d) in 2023 and 13.1 Mb/d in 2024, compared to an average production of 11.9 Mb/d in 2022. The EIA also forecasts U.S. natural gas production to average almost 104 billion cubic feet per day (Bcf/d) in 2023 and around 105 Bcf/d in 2024, compared to an average production of 98 Bcf/d in 2022. These record levels of US energy production are a boon for MLPs.

{kind=link}

{kind=link}

Another factor contributing to the nice MLP performance is the consolidation that is taking place in the sector. Energy Transfer LP ( ET ) acquired Crestwood Equity Partners LP and Oneok ( OKE ) bought Magellan Midstream Partners.

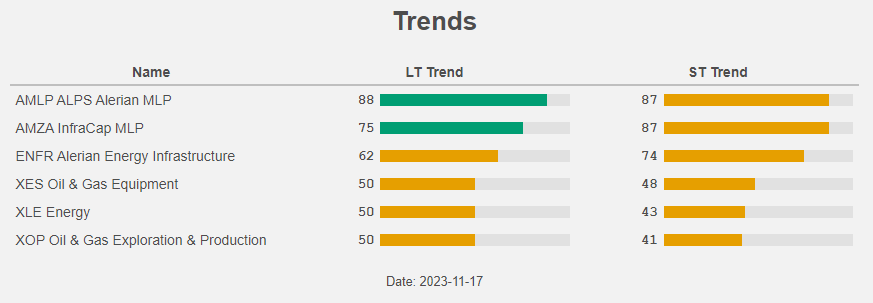

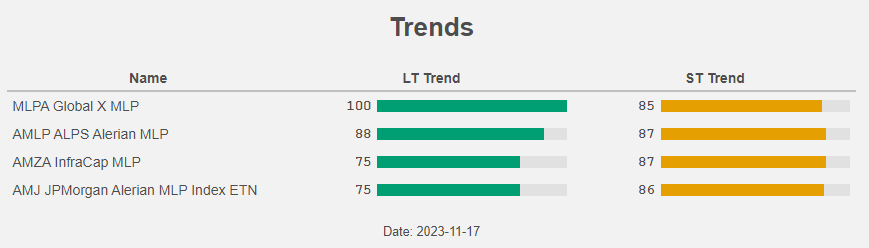

MLP ETFs are the only energy ETFs in a long term uptrend.

{kind=link}

JPMorgan Alerian MLP ETN

The best performing MLP ETF/ETN over the last twelve months is AMJ.

{kind=link}

AMJ is not an ETF but an exchange traded note ((ETN)). This implies that investors in AMJ are exposed to the credit risk of JPMorgan Chase & Co ( JPM ). Unlike (most) ETFs, ETNs have a maturity date. In the case of AMJ the maturity date is May 24th 2024. AMJ has a market cap of $3 billion and we expect JP Morgan to launch a new MLP ETN around AMJ’s maturity.

AMJ is linked to the Alerian MLP Index and pays a variable quarterly coupon linked to the cash distributions paid on the MLPs in the index, less accrued tracking fees. The tracking fee is 0.85% per year.

The Alerian MLP Index (AMZ) is a gauge of energy infrastructure Master Limited Partnerships (MLPs). The index is capped, float-adjusted, and capitalization-weighted. The constituents earn the majority of their cash flow from midstream activities involving energy commodities.

The Alerian MLP Index (AMZ) includes MLPs that span the entire energy value chain and the Alerian MLP Infrastructure Index (AMZI) represents midstream MLPs exclusively. AMZI is the underlying index for the AMLP and AMZA. AMZ is the underlying index for AMJ.

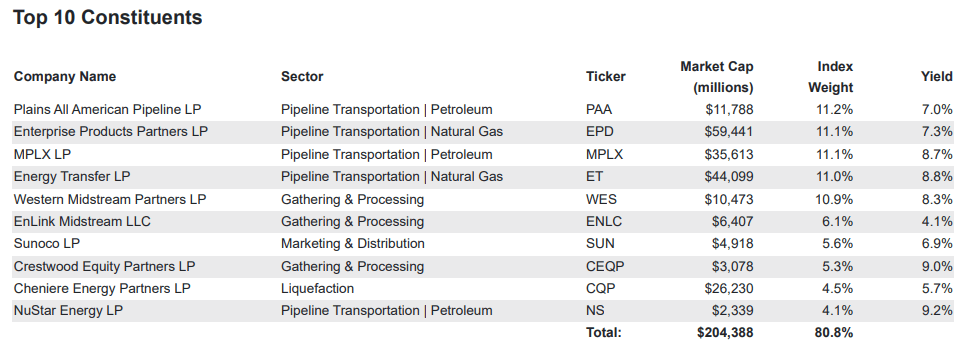

The sector weightings confirm indeed that the entire value chain is included in the Alerian MLP Index.

Figure 8: Sector allocation (VettaFi)

The biggest names in the index are all transportation MLPs.

{kind=link}

The risk of dividend cuts is low

In the past MLPs performed badly when they (had to) cut dividends. This was the case in 2015 and during the oil crash in the Covid crisis.

{kind=link}

Currently, balance sheets are in good shape, free cash flow generation is high and the risk of dividend cuts is low. Thanks to the capex discipline, free cash flow yields are high and MLPs are shifting their attention towards returning capital to shareholders.

Figure 11: FCF yield (Invesco)

And balance sheets are indeed in good shape and are expected to improve further.

Figure 12: Debt/EBITDA (Invesco)

The distribution coverage (distributable cash flow divided by distributions paid to shareholders) has increased in recent years and is expected to remain at the current levels.

Figure 13: Distribution coverage (Invesco)

Valuation

The strong free cash flow generation and the expected juicy dividends and buybacks are great news for midstream investors, but what about the valuation?

The midstream EV-to-EBITDA remains well below their long-term average.

Figure 14: EV/EBITDA ( Invesco)

And when we compare energy infrastructure companies to other income oriented sectors, like bonds, REITs and utilities, they come out on top.

Figure 15: Dividend yield (VettaFi)

MLPs do not only score good points on valuation, but also on momentum. All MLP ETFs/ETNs are in a long term uptrend.

{kind=link}

Conclusion

Capex discipline in the midstream energy sector keeps leading to higher transportation costs. This results in strong free cash flow generation and higher dividends and buybacks for MLPs.

In the past MLPs performed badly when they (had to) cut dividends. Currently, balance sheets are in good shape and the risk of dividend cuts is low.

The valuation of MLPs remains cheap and this could support further M&A activity.

We like MLP ETFs like AMLP and AMZA and the same can be said of the MLP ETN AMJ, the best performing MLP ETF/ETN over the past 12 months.

For further details see:

AMJ: MLP ETN Beats All MLP ETFs