AMKR - Amkor Technology: Recent Price Action Provides An Entry Opportunity

2023-09-27 14:15:49 ET

Summary

- The recent price drop due to insider selling presents a buying opportunity because it is not tied to the company's performance.

- The company is globally diversified and expanding, with a new manufacturing facility under construction in Vietnam and potential for a new facility in the US.

- Amkor has strengthened substantially in the last 5 years, leading to its inclusion in the SOX index.

- Commodification of the OSAT industry, high fixed costs, and key customer risk must be considered.

Investment Thesis

Amkor Technology ( AMKR ) is the leading OSAT company technologically, and second largest by revenue. The company provides packaging and testing services for communication devices, automotive and industrial, consumer devices, and computing. Amkor is globally diversified and expanding. Recent price drops due to insider selling (more on why this is not a concern later) present a buying opportunity.

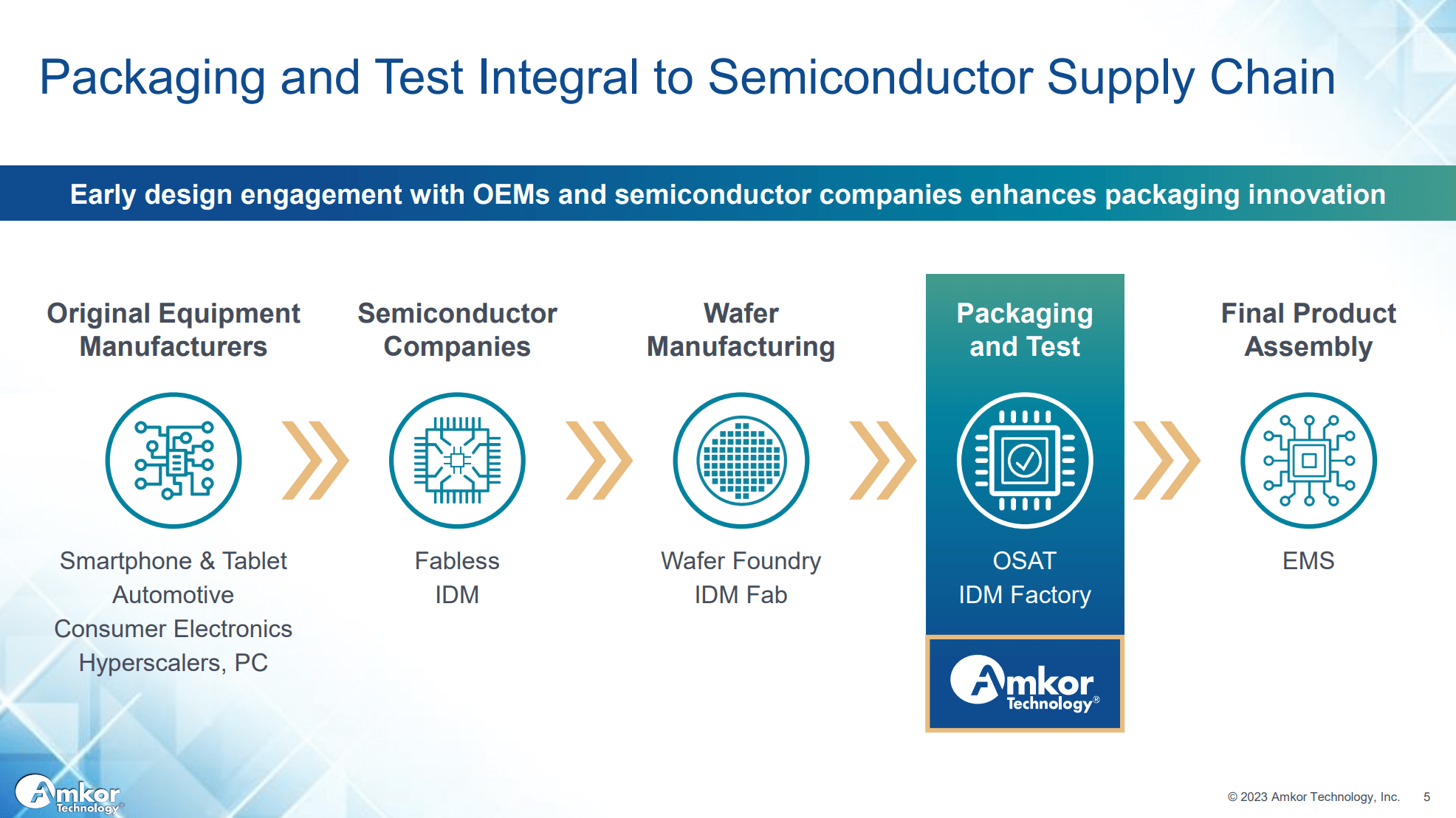

Semiconductor supply chain (Amkor 2023 Technology Presentation)

{kind=link}

About the Company

As a member of the Outsourced Semiconductor Assembly and Testing industry (OSAT), Amkor derives most of its revenue from packaging (88% in FY22) while the remaining 12% comes from testing services. Packaging encompasses processing completed wafers (produced at a foundry) into finished chips. This includes dicing the wafers, creating the package that protects the wafer, and all electrical routing and connectors that let the chip talk to the outside. Testing, as the name implies, verifies the chip works as intended.

Amkor focuses on four key markets: phones and tablets represented 41% of sales, automotive and industrial was 23%, consumer devices were 20%, and computing (data center, storage, etc.) was 16%. As the OSAT technology leader, most of their revenue came from advanced services (74%) that target leading edge nodes. The other 26% of revenue came from mainstream services targeting larger chips.

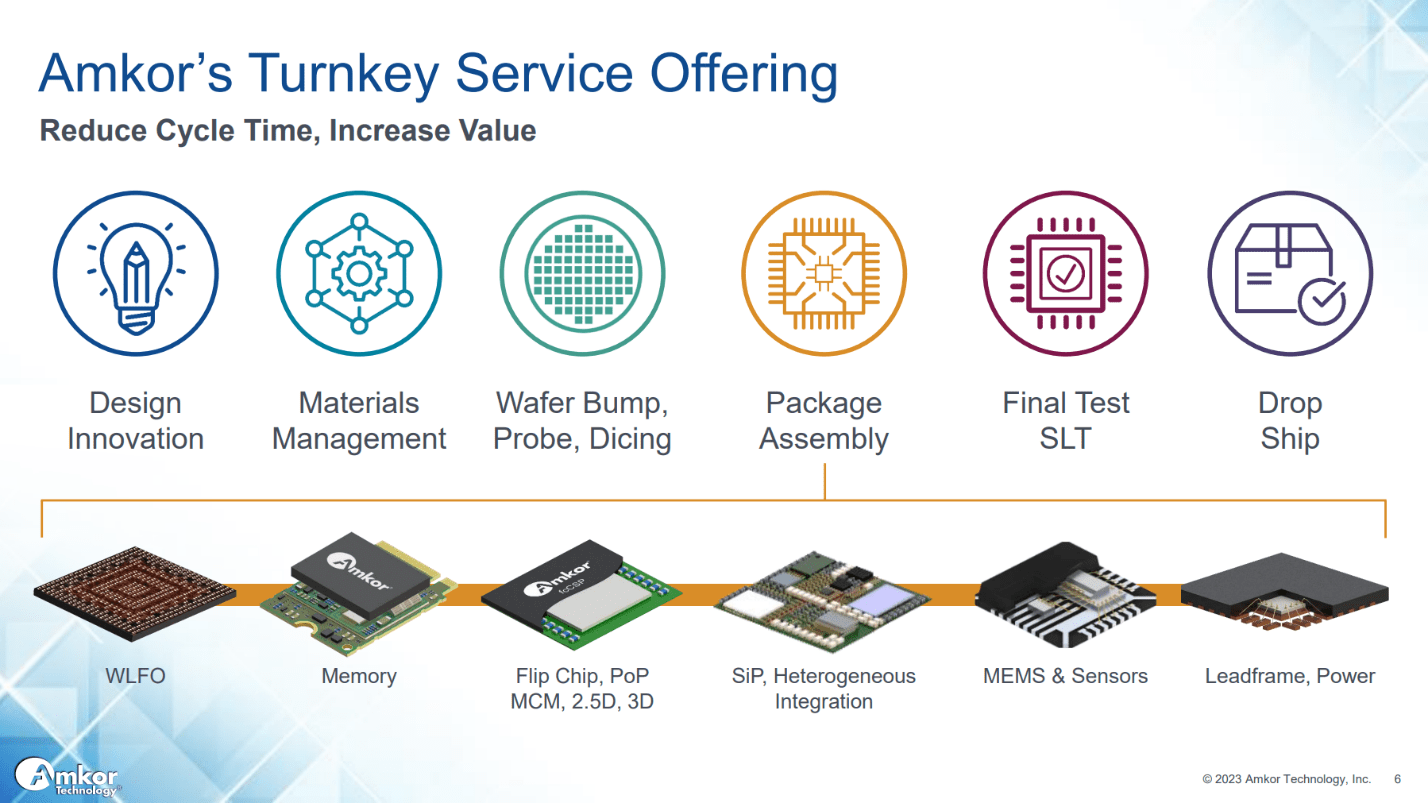

Packaging services chain (Amkor 2023 Technology Presentation)

{kind=link}

Amkor is focused on serving growing segments of the market. Automotive and silicon carbide chips are widely expected to be the fastest growing segments of the semiconductor industry for the foreseeable future. Amkor is the #1 automotive OSAT with over 40 years of experience. They are also expanding their manufacturing capabilities for silicon carbide which is used in power applications (EVs, inverters).

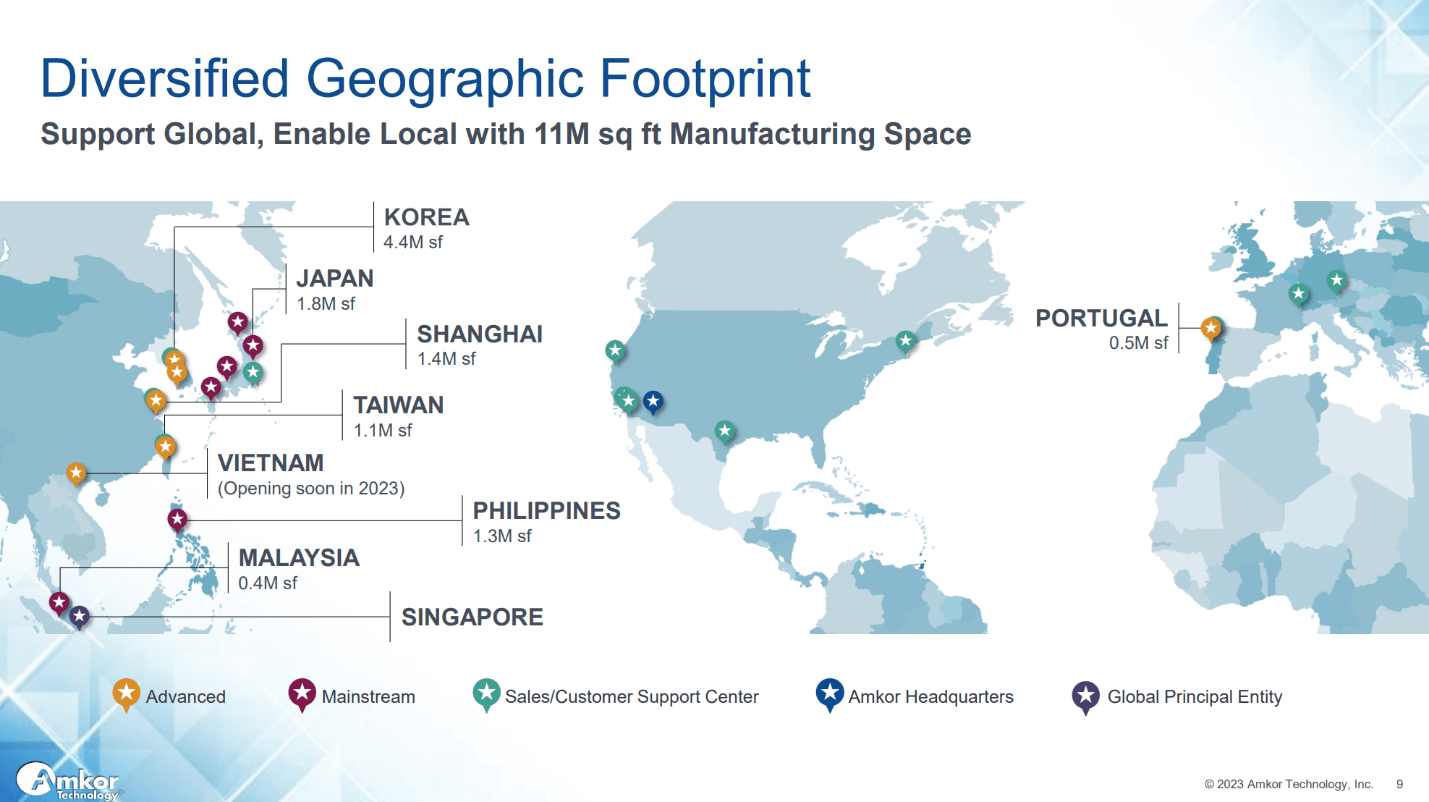

Amkor has a global manufacturing presence that is rapidly expanding. They have a new facility under construction in Vietnam that is expected to begin production later this year. They are also looking to create their first US based manufacturing facility to take advantage of the CHIPs act. In February a partnership with Global Foundries ((GF)) was announced where Amkor would provide OSAT services out of their Portugal site to enable a 100% US/EU supply chain for Global Foundry’s customers. On the Q1 earnings call , the CEO said that customers are looking to secure capacity at different locations in order to derisk their supply chains. This will help drive demand at the new Vietnam facility.

Amkor’s geographic footprint (Amkor 2023 Technology Presentation)

{kind=link}

Amkor seeks to be the OSAT technology leader, but they do not have the most advanced technology. Large foundries such as TSMC ( TSM ), Intel ( INTC ), and Samsung ( SSNLF ) provide full turn-key manufacturing including packaging and testing. New packaging methods such as chiplets are currently restricted to large foundries due to the high capital costs associated with their production. Amkor’s CEO believes that chiplets will eventually move into the OSAT industry once the technology matures and the costs associated with their production come down.

Financial Analysis

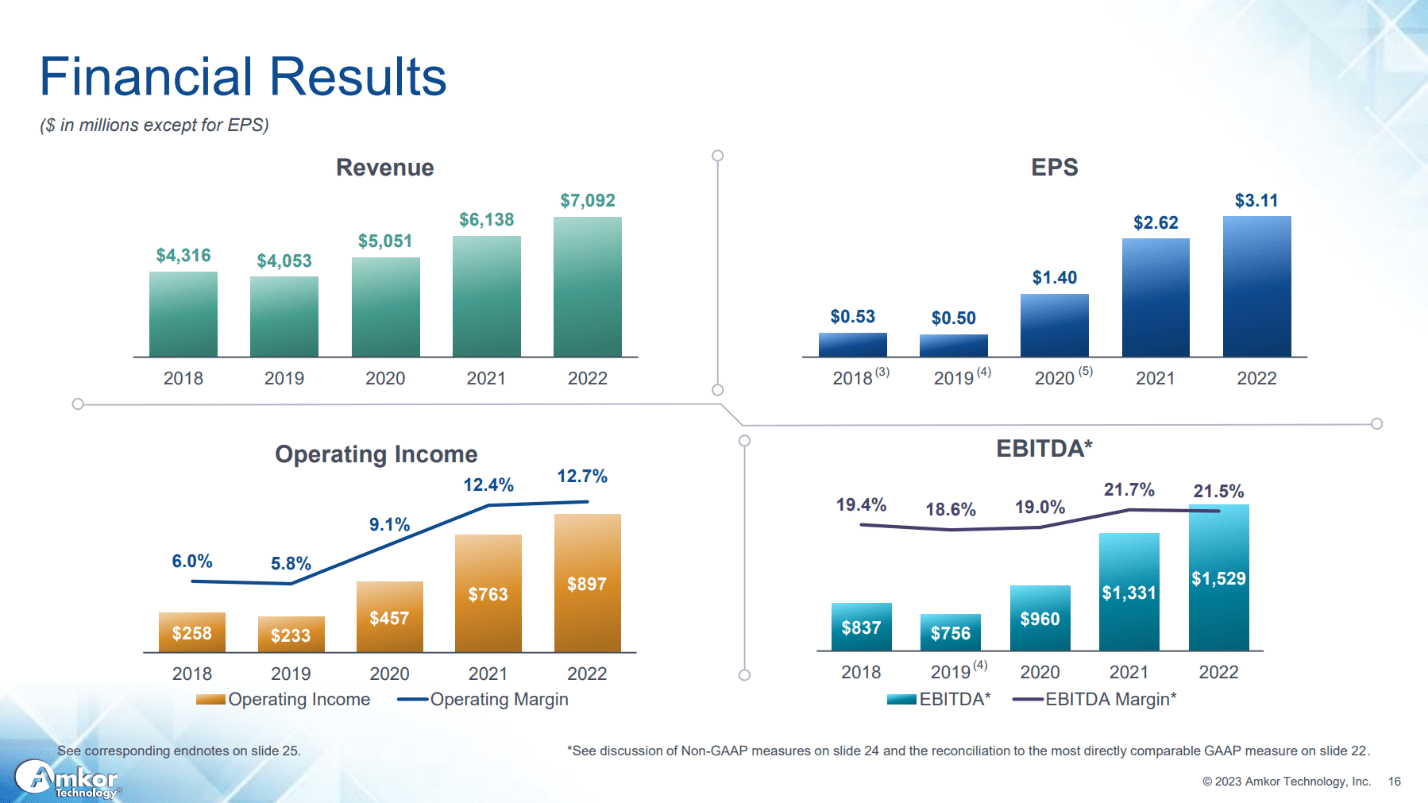

Amkor has steadily improved their performance in the last 5 years. Revenue has increased 64%, EPS has increased 487%, and EBITDA has increased 83%. Prior to 2018 the company saw no growth and its stock price had traded sideways since the dotcom crash. Because of their greatly improved performance, Amkor was added to the PHLX Semiconductor Sector Index ( SOX ) on September 18th.

Financial results for the last 5 years (Amkor 2023 Technology Presentation)

{kind=link}

No Pricing Power and Low Margins

Competition in the OSAT industry is fierce and margins here are more in line with traditional manufacturing than semiconductor manufacturing. The business has become commodified. The operating margin for Q2 was 12.8% and there is little room to push prices up. In fact, there is downward pressure on pricing. In their 10-Q report , Amkor states: “Prices for packaging and testing services have generally declined over time, and sometimes prices can change significantly in relatively short periods of time. We expect downward pressure on average selling prices for our packaging and testing services to continue in the future, and this pressure may intensify during downturns in business.”

For Q2, the cost of sales was 87.2% of revenue. Breaking this down, material costs represented 53.6% of revenue, labor was 10.9%, and other manufacturing expenses were 22.7%. Looking at this breakdown, there is little chance for business efficiency improvements leading to better margins.

Amkor also has high capex spending relative to their revenue. In 2022 they spent $908M on capex while revenues totaled $7.1B. This leads to high fixed costs and depreciation in excess of $150M per quarter. As a result, profitability is directly tied to factory utilization. They do not provide utilization percentages in their 10-Q or 10-K, but the CEO has stated usage rates on earnings calls when asked. 2022 was their most profitable year, for Q3 FY22 they said that utilization was at 85%. Sales are currently being impacted due to the cyclical downturn in semiconductors. The CEO stated that Q3 FY23 (next quarter) utilization will be sub-70% and it is expected that to be the trough in utilization.

Amkor also faces risks due to uncommitted demand. From their 10-Q : “Generally, our customers do not commit to purchase any significant amount of packaging or test services or to provide us with binding forecasts of demand for packaging and test services for any future period, in material amount. In addition, … our customers often reduce, cancel or delay their purchases of packaging and test services for a variety of reasons… This makes it difficult for us to forecast out capacity utilization and net sales in future periods.”

By focusing on high demand areas, the company has avoided the worst of the recent downturn . For the first half of the year revenue is down 6% compared to the approximately 20% decline for the semiconductor industry overall. However, the risk will always remain since customers are not required to reserve capacity and there are no penalties for pushout or cancellation.

Concentrated Customer Base

Amkor’s customer base is highly concentrated. In Q2 the top 10 customers represented 66% of revenue. In their 2022 10-K , they disclosed that their top customer was 20.6% of revenue and the second largest was 10.1% of revenue. I believe Apple is their largest customer because they have disclosed that their communications business serves Android and iOS devices.

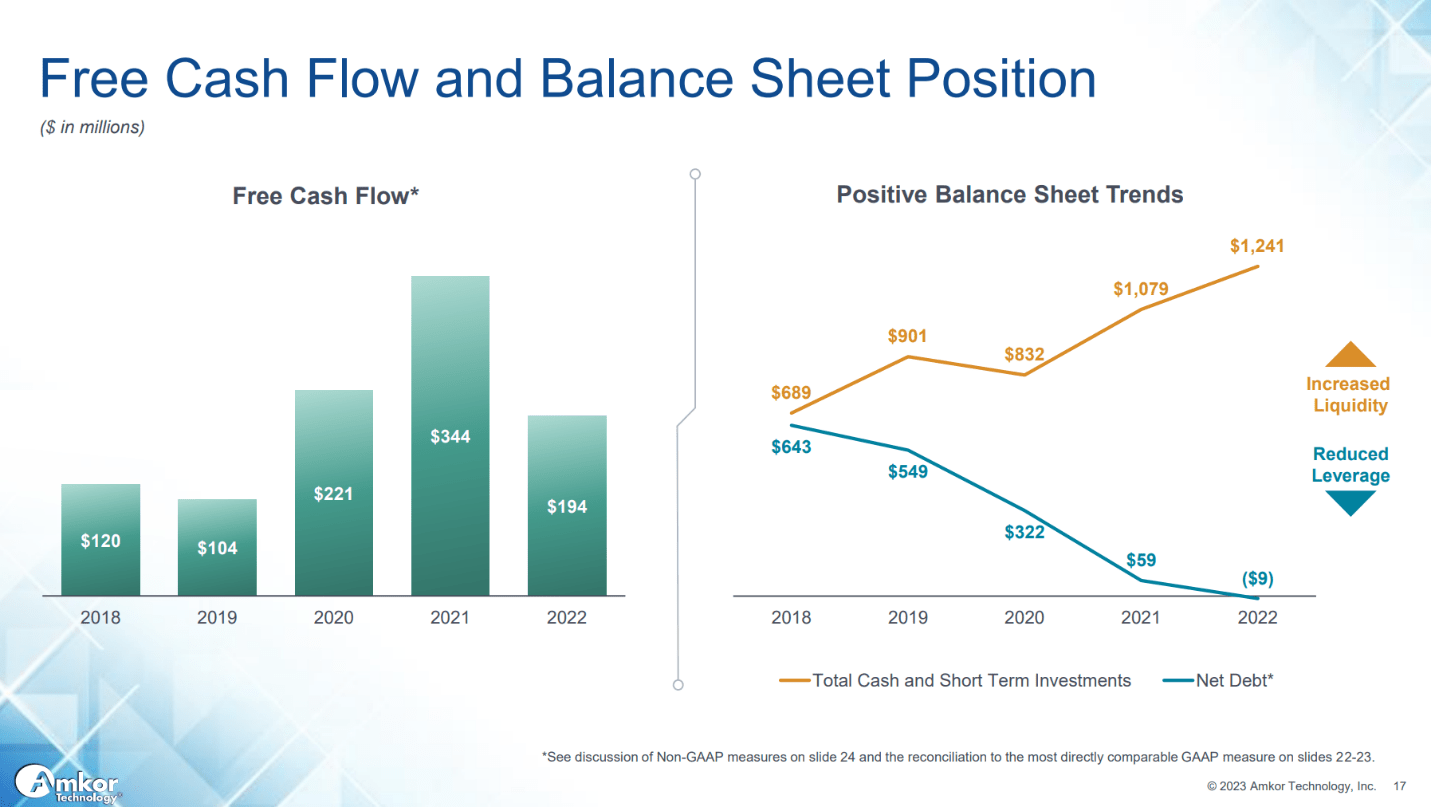

Balance Sheet

The balance sheet has improved substantially over the last 5 years as financial performance has improved. Amkor was debt-burdened for a long time, but as of last quarter their net debt is negative; they have more cash and short-term investments than long-term debt. The deleveraging comes from a mix of debt payoff (current long-term debt is $975.5M), a doubling in cash on hand to 800M, and an increase in short-term investments to $400M from zero.

The capital heavy business model has seen increasing rates of capex and depreciation over time. Capex typically exceeds depreciation and has resulted in an increasing book value per share over time. Currently the book value is $15.19 per share which yields a P/B just under 1.5.

Cash flow generation and balance sheet improvement (Amkor 2023 Technology Presentation)

{kind=link}

Q2 Results and Outlook

Q2 results were weaker than prior years. This is mostly driven by reduced utilization because of cyclical demand contraction in the semiconductor market. The company generated a net income of $64M on $1458M of revenue with an operating income margin of 5.2% for $0.26 EPS. Depreciation was $158M and capex was $184M as the company continued to expand its manufacturing footprint.

Management expects utilization to trough in Q3. Revenue is still expected to be higher in the quarter, between $1.725-$1.825 billion, driven by increased demand for advanced packaging for premium phones (probably iPhone). Margins are not likely to increase; net income is guided between $90M-$130M and EPS will be $0.36-$0.53.

Besides strong phone revenues, management also expected strong automotive demand in the quarter. Q3 runs from July to September. The UAW strike didn’t begin until September 15th so it is unlikely to impact Q3 revenue, but an extended strike could hurt sales in Q4 if it persists too long.

Valuation

Amkor is a tricky company to value because its performance is inconsistent between quarters. The variance is caused by differences in capex which have varied from $98M to $333M per quarter over the last 11 quarters. Their revenue is also tied to utilization which varies based on customer demand that is not locked in. Because of the variability, valuation models such as discounted cash flow cannot be used.

To estimate the fair value of the stock the only practical method I see are comparisons between current and historic metrics. Amkor has a 5 year average P/E GAAP ((FWD)) of 22.81, this would imply a fair value of $34.55. Their 5 year average P/E GAAP ((TTM)) is 15.31 which implies a fair value of $35.93.

Charting shows two preferred price ranges between $24-$26 (orange lines) and $28-$30 (cyan lines). The midpoint of each range provides a factor of safety equal to 12% and 30% respectively. Charting produces more a more conservative upper limit, and I would consider selling above $30.

Amkor charting (Webull, Markup by Author)

{kind=link}

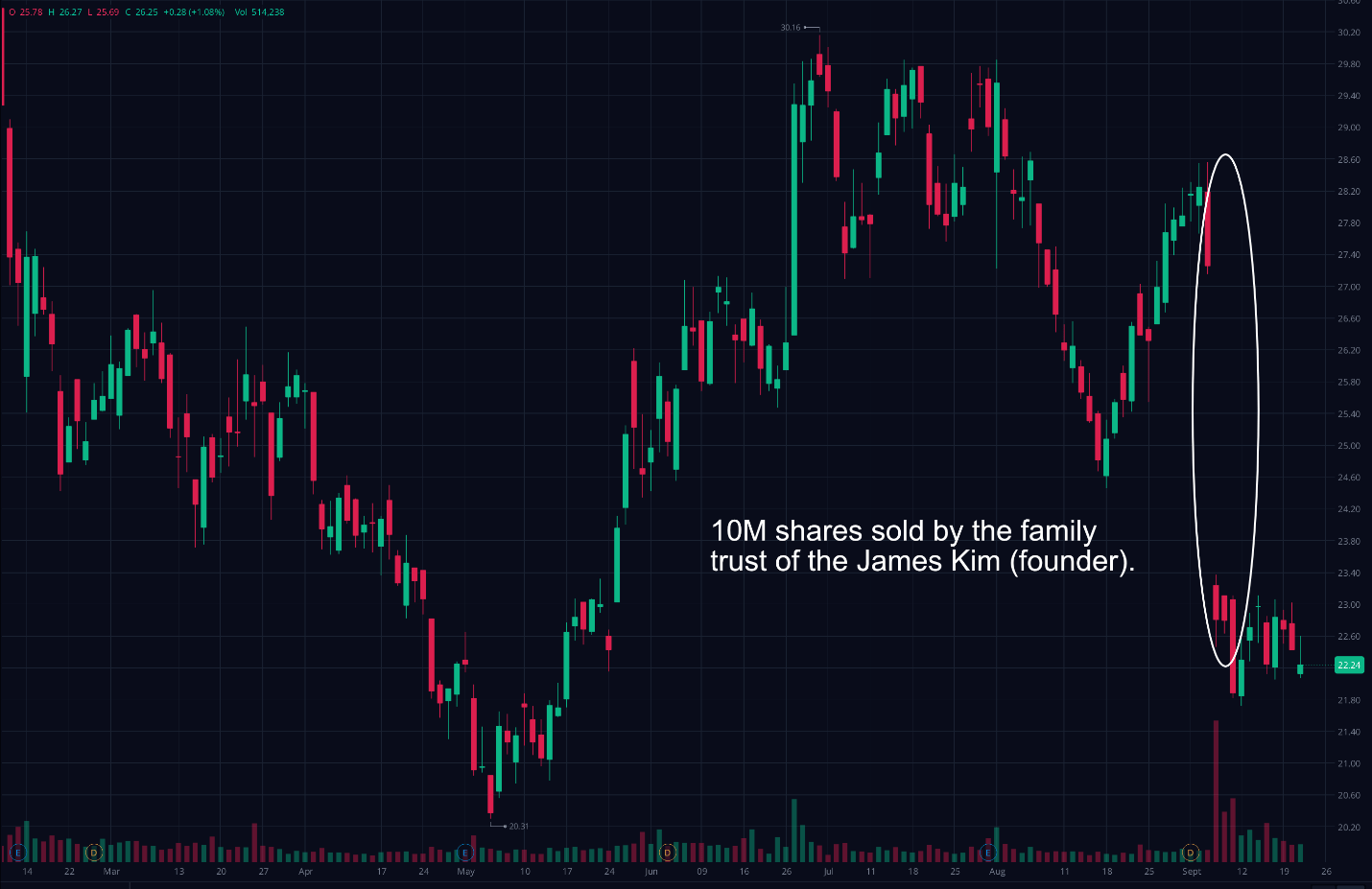

Share Price Tumble

On September 6th it was announced that the family trust for James Kim—the founder of Amkor— sold 10 million shares for $24 per share. Amkor had no role in the sale, and the newly released shares are nondilutive, though they increase the free float. The Kim family agreed to a 1 year lock-up prohibiting the sale of more shares.

Amkor stock chart (Webull, Markup by Author)

{kind=link}

The share price dropped almost instantaneously on the news. Amkor has a free float share count of only 113.1M of 245.7M shares outstanding and the Kim family holds over 50% of the shares either directly or via trust holdings. The newly available shares represent 8.8% of the free float.

Since nothing about the company changed, only the ownership makeup, the stock price could recover to where it was previously. On the other hand, it will require a significant number of existing and new shareholders to take up the expanded free float. Based on the past two weeks it appears digestion of the new shares won’t be quick because the stock price has continued to trend down.

Risks & Conclusion

The risks Amkor faces should be weighed with the chance for gain. Amkor’s client list is concentrated, they don’t have long-term commitments, and the business is commodified. Losing a single large client could be the difference between profitability and loss. High fixed expenses related to their factories and low margins make cost cutting unlikely in the event of demand loss. Finally, the UAW strike could lessen the demand for automotive components which directly impacts Amkor as the largest automotive OSAT.

Amkor is well positioned in the OSAT industry and stands to benefit from accelerated growth in automotive electronics in addition to standard semiconductor growth. The new facility in Vietnam, expansion of existing facilities across Asia and Europe, and the potential for a new site in the United States will provide additional capacity for Amkor to serve its existing clients and acquire new clients. Additionally, I do not believe they would expand capacity so heavily if they did not believe it would lead to future revenue growth. Finally, the share price drop presents an opportunity to buy the dip because it is an external event. Therefore, I rate the stock a speculative buy.

For further details see:

Amkor Technology: Recent Price Action Provides An Entry Opportunity