AMKR - Amkor Technology: Well Positioned And Fairly Valued

2023-08-11 12:37:03 ET

Summary

- Amkor Technology, Inc. remains a reasonably valued semiconductor company with strong earnings.

- Having exposure to the semiconductor market is a good move for investors, and AMKR offers good exposure.

- AMKR specializes in outsourced solutions for semiconductor packaging and testing, benefiting from rapid technological advancements.

Investment Rundown

Despite the runs up across the semiconductor for companies' share prices, Amkor Technology, Inc. ( AMKR ) remains one of the more reasonably valued ones still. The company has a p/e of just 18 and still generates strong earnings. I think it has become quite clear to most investors that the semiconductor market does extrude some volatility as it remains cyclical. The ebbs and flows of the demand for it shifts and therefore do the top and bottom lines for companies like AMKR. What becomes crucial is finding the companies which are well-positioned and ready to capitalize when the cycle rebounds and growth accelerates.

Having some exposure to the semiconductor in some way or another seems like a good move for most investors. Maintaining a diversified portfolio is crucial to hedge against otherwise strong volatility. Having a position in AMKR seems to offer good exposure to the market and I will be rating it a buy as a result.

Company Segments

AMKR specializes in delivering outsourced solutions for semiconductor packaging and testing needs across the United States but also internationally. The company's core focus lies in offering a comprehensive suite of turnkey packaging and test services that cater to the intricacies of the semiconductor industry's demands.

In an industry characterized by rapid technological advancements and evolving market dynamics, AMKR's role as an outsourced service provider is pivotal. Semiconductor manufacturers benefit from the company's specialized expertise and state-of-the-art facilities, which allows them to focus on their core competencies without compromising on the quality and reliability of their products.

{kind=link}

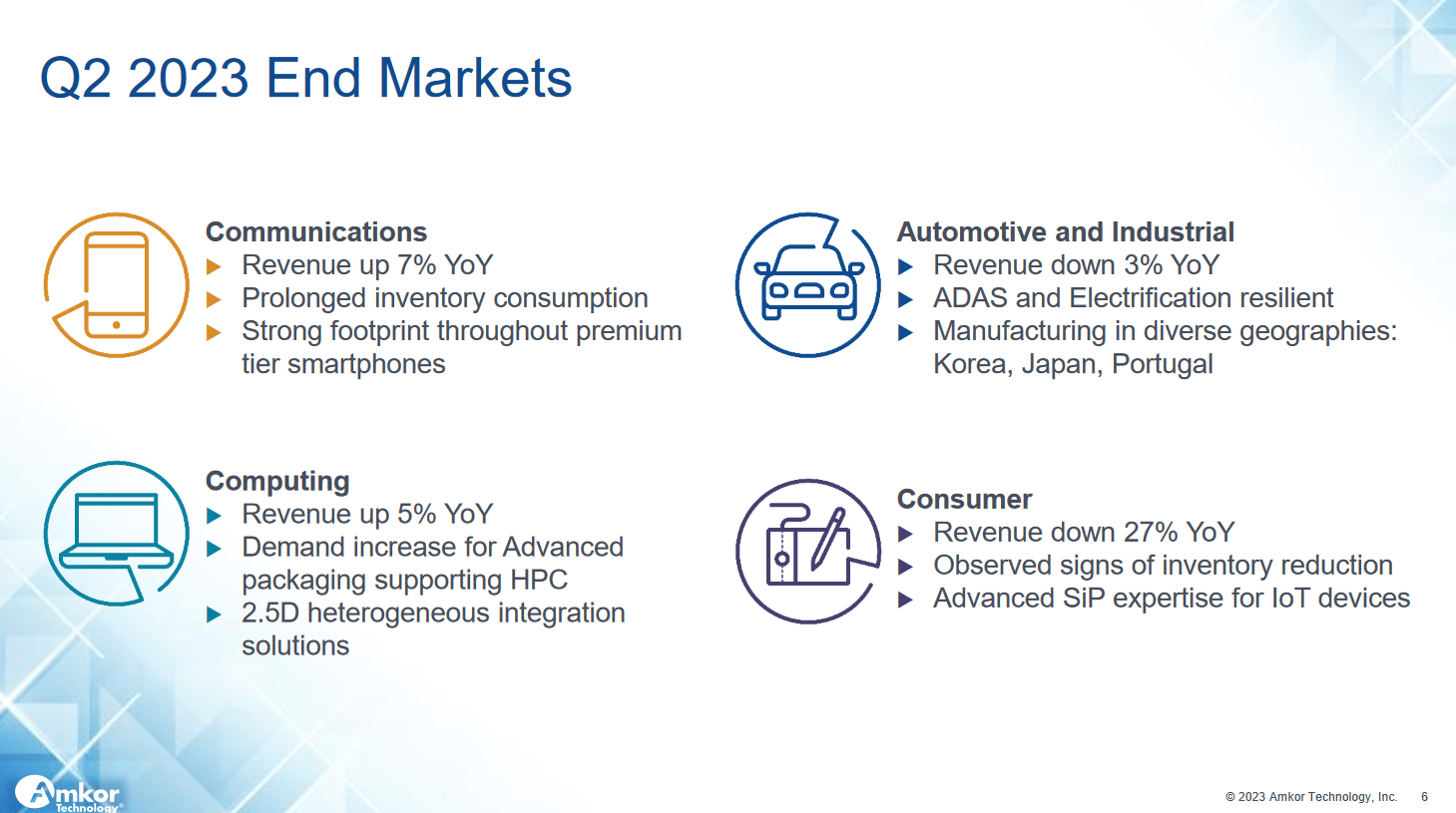

From the last quarter, there was varied demand across the end markets that AMKR has. Most notable was a 27% decrease YoY in the consumer market. Leading causes for this decrease seem to be signs of inventory reductions as companies want to have a larger operation where they aren't too reliant on assets and inventory. That does create a more flexible position to operate from but does result in companies like AMKR having results as we say in Q2, significant YoY declines. But what is important to note is that once the market rebounds then the growth is quick and impressive.

Growth Rates (Seeking Alpha)

Just looking at the historical growth of the company they have managed to achieve a 9.27% annual growth for the revenues in the last 10 years, But what is reassuring to see is that EPS has grown at 21% during that period, indicating that AMKR has made solid margin progress at the same time.

Net Margins (Macrotrends)

During peaks of the cycle margins are high, and during “valleys” of it the margins are low. Seems quite obvious, but looking at the chart above here for the net margins of AMKR it seems we are heading towards a floor. If we see preservation of margins around the 8% - 9% range then I think we are in for a good buying opportunity. I am willing to take that bet as I am rating it a buy. Further reassurance to this stance will come from the Q3 and Q4 report where my main focus will be the margins. I don’t doubt AMRKs ability to grow revenues by expanding into new markets, but retaining margins is a different challenge.

Risks

The company's financial performance is currently grappling with the effects of a pronounced downturn in the semiconductor market. This downward trajectory is conspicuously reflected in its earnings, which have encountered a substantial slump. The intricacies of the semiconductor landscape, often influenced by cyclical trends and market forces, have cast a shadow on the company's income streams.

Margin Growth (Investor Presentation)

Accompanying the earnings slump, the company has encountered a constriction in its profit margins. This has resulted in a decline of 96% year-on-year decline in EPS, bringing it down to $0.26. This financial figure underscores the challenges the company is navigating in a landscape fraught with volatility and shifting dynamics. As the market slumps the earnings for the company significantly decrease to reflect this new sentiment and market condition.

But as I think is clear with companies in a cyclical market, adding to a position when they are looking like their worst is often the best time. There might be more pain ahead, but the QoQ above here showcases a recovery that I don’t think is only because of seasonality, desiring Q1 being one of the toughest months to operate in.

Financials

Financially, I think AMKR still looks very healthy and I don’t think they will have any significant challenges paying down the debt. The balance sheet is so strong it makes me question again why AMKR is trading where it does.

Assets (Balance Sheet)

They have gathered up over $800 million in cash, there is a display of decrease from where AMKR was at the year-end of 2022. But that isn't to say AMKR is in any way in bad shape. The company has $975 million in long-term debt which has decreased by over 10% since the last quarter. That means AMKR could almost cover all debts just from the cash. For me, this is a key point to look at as it indicates they are likely very capable of investing heavily into new revenue streams or making acquisitions, both practices hopefully leading to better earnings.

Final Words

For AMKR the focus lies right now on preserving margins I think. The company seems to be maintaining it rather well and even showed consequently growth in the latest quarter. The varied end markets that AMKR are displaying varied trends with some decreasing significantly, whilst others growing still. I think that AMKR is valued at a great price that it makes sense to begin a position and start capitalizing on the massive demand for the semiconductor industry. Based on earnings, AMKR is valued at 20% below the sector and based on sales 62% below the sector. That leaves me with a very satisfying discount, resulting in me rating AMKR a buy right now.

For further details see:

Amkor Technology: Well Positioned And Fairly Valued