AMLP - AMLP: A Good Inflation Hedge With Lower Volatility Than Most Energy Investments

2023-10-24 06:59:36 ET

Summary

- The U.S. energy landscape is bullish for midstream assets given rising gas production and exports.

- As a "hard asset", midstream infrastructure also offers a good inflation hedge.

- The Alerian MLP ETF offers diversified exposure to U.S. midstream MLPs without the administrative burden of a K-1.

- The ETF's yield will become more attractive as interest rates eventually peak.

Investment thesis

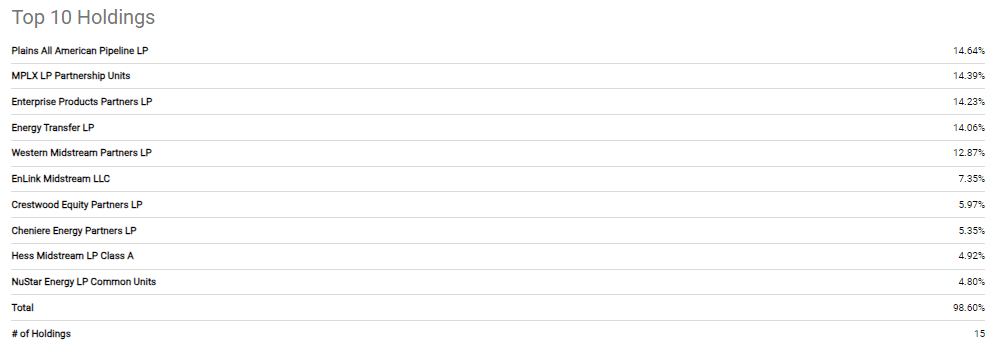

If you believe energy prices and inflation will be higher for longer but prefer to avoid the volatility of upstream oil and gas equities, the Alerian MLP ETF ( AMLP ) may be an investment vehicle to consider - especially if you value income. AMLP offers diversified exposure to the common units of the master limited partnerships (or MLPs) that own much of the U.S. midstream infrastructure. Currently, Plains All American Pipeline ( PAA ), Enterprise Products Partners ( EPD ) and MPLX ( MPLX ) are the top three holdings.

But why invest in midstream MLPs? Three reasons:

- The MLP units are claims on "hard assets" critical to the energy sector - oil and gas pipelines, processing facilities, storage terminals and even LNG export infrastructure;

- Not only are hard assets an inflation hedge, but domestic U.S. politics makes it difficult to construct new pipelines; this makes the existing infrastructure even more valuable by eliminating competitive threats;

- Midstream players have less volatile cash flows compared to upstream producers; this allows MLPs to maintain stable distributions that are valued by income investors.

That said, if you purchase the units of PAA, EPD or MPLX directly, you will achieve a better yield because the fees charged by AMLP are rather high. However, besides the diversification benefit, the ETF also provides a "wrapper" around the K-1 forms issued by individual MLPs. While receiving a K-1 isn't the end of the world, many investors prefer to avoid the tax complexity.

AMLP may be particularly attractive if you think the Fed is approaching the end of its tightening cycle and we are headed into financial repression, i.e., lower, artificially managed interest rates while inflation has not fully receded. Historically, just as other high-yield investments, MLPs have underperformed when interest rates were high. However, this time, perhaps because it is still recovering from the pandemic sell-off, AMLP has held up surprisingly well. If the Fed "pivots" in the face of rising fiscal deficits, I would expect AMLP to eventually re-rate higher.

The bull case for midstream assets

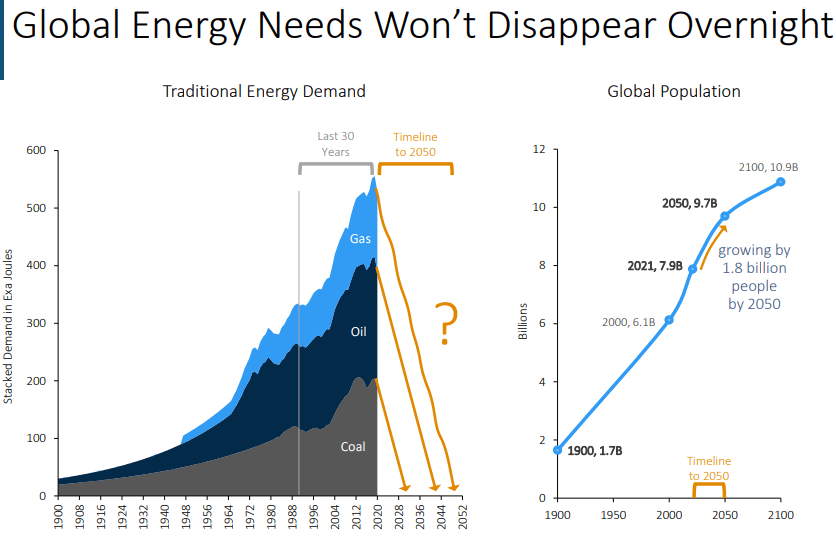

Midstream assets ought to do well in an inflationary regime because they are "hard assets" and also represent critical infrastructure - there is no substitute. The only threat could be a rapid transition to renewables but that is simply not realistic as pointed out by EPD in a recent presentation:

{kind=link}

Further, as U.S. shale is maturing , upstream production is getting more gassy and this puts more pressure on the midstream segment:

Enterprise Products Partners Presentation

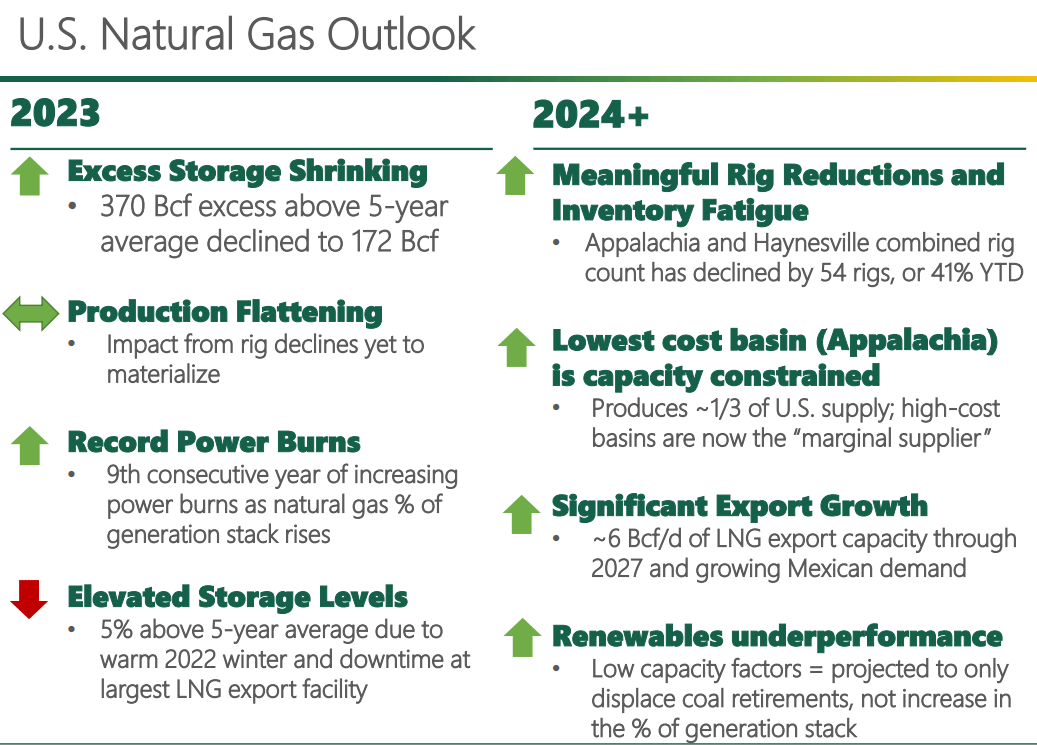

As the Permian's gas output is growing, it is good to remember that Appalachia is already constrained by offtake capacity:

{kind=link}

This promises for an interesting dynamic. Both U.S. LNG export capacity and upstream gas production are growing, but the midstream capacity that links the two is lagging behind. I think this is good for the owners of the existing infrastructure.

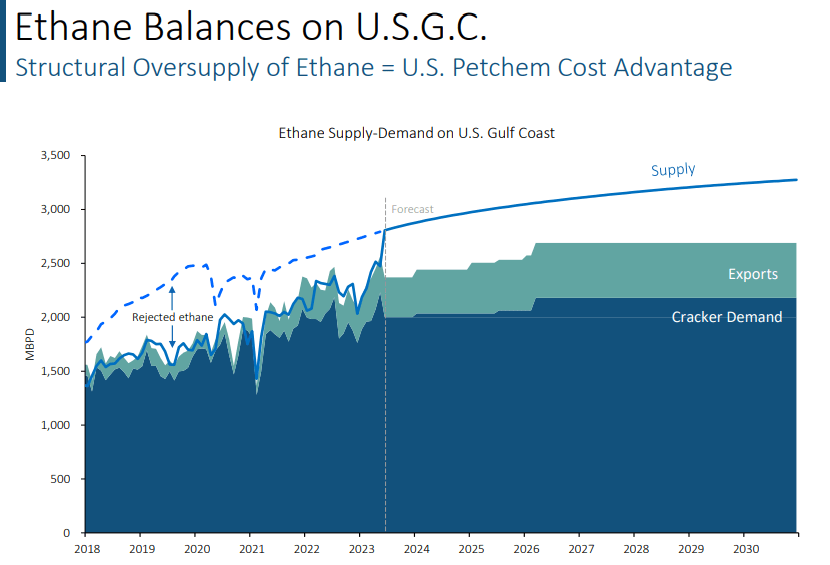

In fact, the midstream bull thesis extends beyond energy to petrochemicals as well:

{kind=link}

The U.S. has excess ethane (which, after getting cracked into ethylene is a basic petchem building block) and managing the oversupply will put further premium on storage and export terminals along the U.S. Gulf Coast.

What is a master limited partnership?

While some midstream companies are organized as C-corps (similar to most traded stocks), others are MLPs or publicly traded partnerships. Unlike C-corps, MLPs are passthrough entities from federal income tax perspective, which theoretically results in a lower cost of capital.

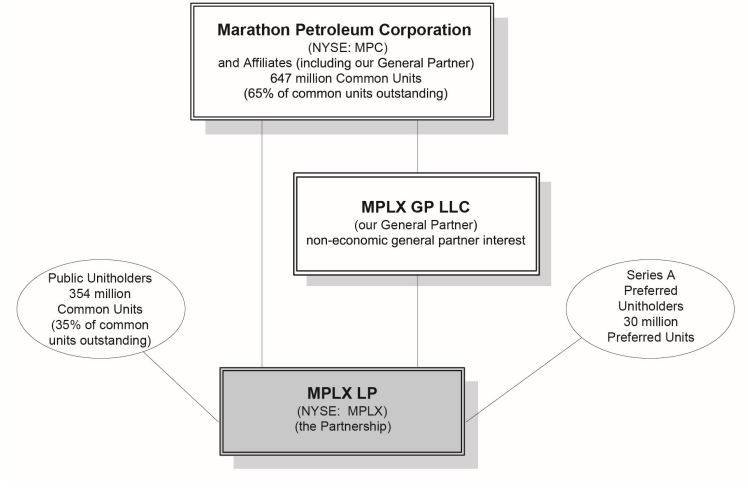

A good example of how an MLP works is MPLX, which is controlled by Marathon Petroleum Corporation ( MPC ):

{kind=link}

MPC is the GP (general partner) in the MLP that is responsible for the commercial decisions. In this case, MPC isn't only the GP, but also owns 65% of the common units - the common unit holders are basically the "limited partners." In MPLX's case, only 35% of the common units are owned by investors and traded publicly, but there is no reason why that percentage can't be different. MLPs can also have preferred units.

While not all MLPs are linked to a corporation, in the MPC-MPLX setup the MLP gets a lot of revenue from the sponsor, i.e., MPLX provides its infrastructure for MPC's use. This usually happens under long-term agreements with minimum payment obligations to shift risk away from the MLP to the sponsor. The GPs may also frequently have "incentive distribution rights" which act similarly to carried interest and increase the GP's returns after certain return hurdles are reached by the common unit holders.

As the GP controls the MLP from a commercial perspective, the partnership agreement has certain safeguards to protect the common unit holders. Usually all available cash above some minimal level has to be distributed quarterly. Unlike a REIT, the distribution requirement is not tax-driven. However, similarly to a REIT, an MLP must derive at least 90% of its income from "qualifying activities" (operating midstream energy infrastructure is of course a qualifying activity).

The MLP structure limits the upside for the common units, but the idea is that there is also protection on the downside - and, mostly, the entire setup is intended to facilitate cash distributions in a tax-advantaged way.

Who invests in MLPs?

MLPs target U.S. retail investors. Unlike stock dividends, some of the MLP distribution is considered a "return of capital" and decreases the cost basis of the units. This can have the effect of deferring tax on distributions until the investors sell their units.

For other market participants, the MLP structure may not make as much sense :

- For tax-exempt investors such as many institutional investors, the MLP income is considered "unrelated business taxable income" or a "nuisance"; this also applies to individuals who own MLPs in a non-taxable IRA although a small amount of MLP income is allowable;

- Non-U.S. investors in MLPs will face a significant administrative burden; they will be considered engaged in a "U.S. trade or business" (as they are "partners" in an active business) which means they need to file a U.S. federal tax return - quite a pain if you don't have to do it otherwise; because of this, the IRS also requires the MLPs to withhold tax from the distributions to non-U.S. persons.

- Finally, regulated investment companies such as mutual funds may face further restrictions on the maximum they can allocate to MLPs and risk losing their tax-exempt status if they aren't in compliance.

MLPs have generally been losing popularity. One culprit is perhaps the reduction of the U.S. corporate tax rate from 35% to 21% back in 2017, which diminished the tax advantage. However, even prior to that some industry players such as Kinder Morgan ( KMI ) unrolled their MLPs. In the KMI example one concern was the increasing incentive distribution right payment that resulted in the MLP paying out more cash to KMI than to the common unit holders; the MLP structure was also said to constrain growth.

In any case, besides Kinder Morgan, there are a number of other midstream players organized as C-corps; you don't have to invest in MLPs to gain exposure to the sector.

What are AMLP's largest holdings?

The quality of an ETF is as good as the underlying investments:

{kind=link}

After PAA, MPLX and EPD, the next largest holdings are Energy Transfer ( ET ), Western Midstream Partners ( WES ) and EnLink Midstream ( ENLC ). These top six holdings make up about 75% of the ETF.

Currently Seeking Alpha analysts rate each of these MLPs as a "buy":

{kind=link}

Distributions have been slowly growing since the pandemic:

The coverage ratios are good:

Cash flow multiples are considerably below their pre-pandemic levels:

Individually, AMLP's holdings appear to be reasonably good investments.

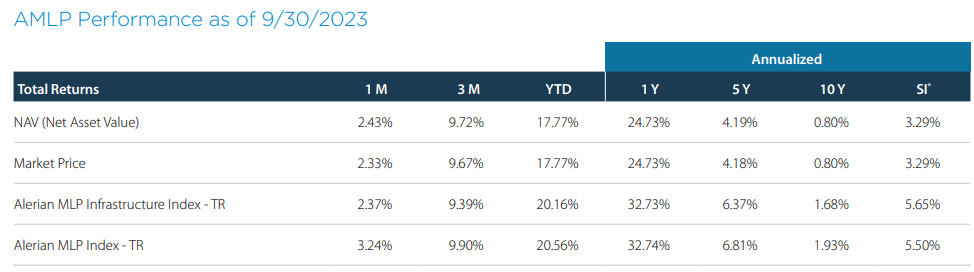

How has AMLP performed historically?

Distributions fell in Q1 2020 and reached their low point in Q1 2021; since then, they have been steadily increasing. Minor quarter-to-quarter fluctuations are probably associated with special distributions:

Seeking Alpha

AMLP is less volatile than an upstream ETF such as the SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ) and drawdowns have been more muted:

AMLP did experience big drawdowns in 2014 and during the pandemic, though; that still weighs down on the long-term historical returns:

{kind=link}

The 0.85% fee charged by the ETF isn't low either, but that is probably the price if you really want to avoid the K-1s:

Unlike direct investments in MLPs, income and losses from the Fund’s investments in MLPs will not directly flow through to the personal tax returns of shareholders. The Fund will report distributions from its investments, including MLPs, made to shareholders annually on Form 1099. Shareholders will not, solely by virtue of their status as Fund shareholders, be treated as engaged in the business conducted by the underlying MLPs for federal or state income tax purposes or for purposes of the tax on unrelated business income of tax-exempt organizations.

Source: AMLP Prospectus

It is worth pointing out that a competing ETF from Global X ( MLPA ) with a similar no K-1 benefit charges a lower fee of 0.47%. The two ETFs track closely each other although MLPA has slightly underperformed AMLP:

The MLPA yield is also a bit lower. Ultimately, AMLP and MLPA cover similar investments, but the holding percentages are different.

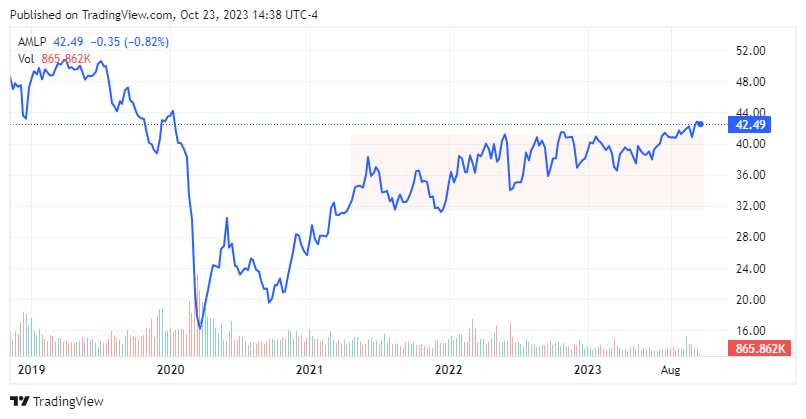

Is AMLP a buy, sell or a hold?

I started buying AMLP back in 2020 and my average cost basis is currently about $26. Right now, I would probably wait for some correction before I put new money in although AMLP recently seems to have broken above its post-pandemic "range":

{kind=link}

I rate AMLP a "hold" which is exactly what I personally am doing.

For further details see:

AMLP: A Good Inflation Hedge With Lower Volatility Than Most Energy Investments