AMRX - Amneal Pharmaceuticals: Risk Still Persists

Summary

- The inability to efficiently market new drugs might put significant pressure on AMRX's margins, which can lead to a substantial stock price correction.

- As the business has been expanding its drug portfolio, in the upcoming years, profitability might improve significantly.

- I believe the upside is significant but the downside risk still persists.

With its primary operations in the United States, India, and Ireland, the company produces generic and branded specialty pharmaceutical products. Amneal Pharmaceuticals ( AMRX ) is a holding company that holds about 49.6% stake in Amneal's business (the promotor group owns the remaining 50.4% stake).

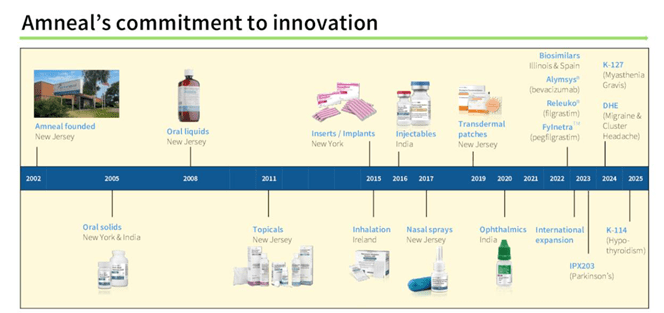

In the year 2021, to expand its drug portfolio, the company acquired controlling stakes in various pharmaceutical companies such as Saol, Puniska, Kashiv, and AvKARE, which produce various specific and generic drugs; the acquisition is expected to strengthen the business model along with improve the business performance in the upcoming years.

Furthermore, management tends to focus on high-value, complex drug formulations, which give higher profitability and a longer life cycle. Also, to develop high barrier-to-entry generic drugs, the company markets over 250 products covering an extensive range of products.

In its specialty segment, the company focuses on central nervous disorders , such as Parkinson's disease, through its patented drugs, such as Rytary. Also, through its AvKARE segment, the company provides medical and surgical products to government agencies.

As the business has expanded its drug portfolio, profitability will improve significantly in the upcoming years. Still, higher debt and loss-making operations might bring significant concerns to the business model. I believe the upside is significant but the downside risk still persists.

Historical performance

revenue growth (macrotrends.net )

Over the last ten years, revenue has seen substantial growth, starting from $581 million in 2012; the revenue has reached $2 billion; such significant growth is attributed to continuous innovation and acquisition. Although the revenue has seen substantial improvement, net profits have been significantly volatile over the underlying period; such volatile earnings are attributed to fluctuations in product margins along with various charges such as research and development impairment charges. Also, despite profitable business operations, the company has been relying on equity dilutions for business operations and expansion; as a result, the total share count has increased from over 66 million to about 151 million during the same period.

Furthermore, as a result of merger with impex in 2018 , revenue and debt levels increased significantly, and higher interest on increased debt levels has been affecting margins significantly.

CFO (macrotrends.net )

Also, Cash flow from operations seems attractive; over the years, the company has able to increased cash flows despite subdued earnings. Except the year 2019, Amneal has produced huge cash flows; which provides significant stability to the Amneal's business model.

{kind=link}

Also, historically Amneal has brought innovative products to its drug portfolio, which has been a major growth driver for cash flows. It seems that management is focused on expanding business operations, which can bear fruit in the upcoming years.

Strength in the business model

Amneal is focused primarily on obtaining generic drug 180-day exclusivity, which gives high-profit margins over a limited period; from such operations, the company could protect its margins and earn higher returns. Also, the company spends a significant amount on research and development, which can help the company bring innovative products to sustain margins.

{kind=link}

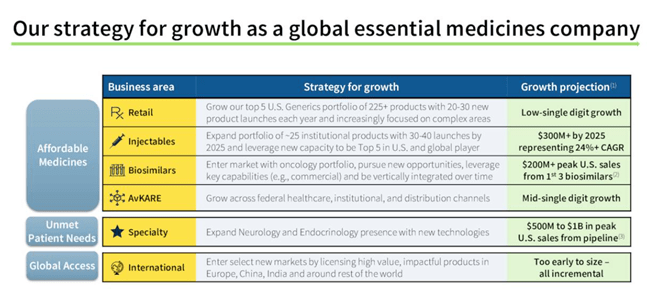

As the company has been taking various initiatives to expand its product portfolio by focusing on drugs with a large total addressable market, revenue might increase significantly in the next few years. As per the growth projection by the management, the company has a significant opportunity to expand its operations.

Risk factors

As a significant percentage of revenue comes from the top three customers, loss of customers might bring significant concerns to the business. Also, the company operates majorly in the generic segment which is known for high completion and low returns; inability to bring innovative products or exclusive products might affect the revenue and profitability.

litigation charges (quarterly report)

Over the years, the company has been facing various litigation charges, in the last nine months, the company has incurred over $173 million in antitrust litigation charge; such a high charge can affect the cash flows significantly.

debt (quarterly report)

Also, over $2.5 billion of long-term debt will mature by 2025; any weakness in the business performance due to high litigation charges, low-profit margins and loss-making newly acquired subsidiaries might affect the refinancing procedure, which can cause a substantial drop in the stock price.

Recent development

quarterly result (quarterly report)

In the recent quarter, revenue has increased from $528 million in the same quarter last year to about $545 million by now, primarily due to solid performance in all three segments. Despite such a stunning performance, the company has posted a loss due to higher research impairment charges and interest burden. Also, in the last nine months, the losses reached $125 million due to the higher litigation charges; but due to increased payables, cash flow turned positive. Investors must consider that a positive CFO is related to increased payables, not core business operations.

{kind=link}

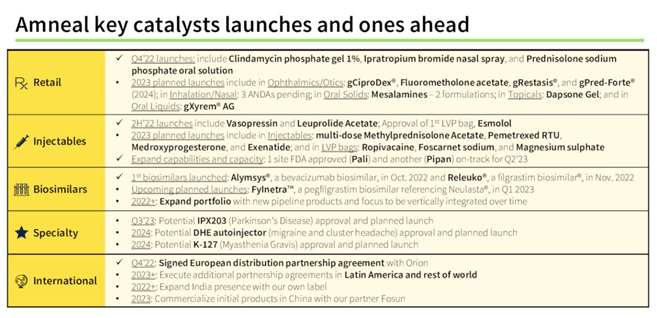

Although the business has been facing significant backdrops, the management is focused on driving revenue growth of various segments, which can be a value-creating decision. These newly launched drugs might bring substantial cash flows to the business. As the company has filed for new drug approvals, business performance might improve upon the launch of these drugs.

share price (Ycharts )

Since 2018, the stock has posted over 89% of its value and has been trading for about $2.1 per share; such a significant drop came after its merger with Impex; the company started facing significant trouble maintaining its margins along with increased debt load.

Currently, the company is trading for $640 million, whereas it has over $2.7 billion in net debt and over $1.4 billion in current assets; As the company has been losing money, higher debt might affect its financial position. Also, the inability to efficiently market new drugs might put significant pressure on margins, which can lead to a substantial stock price correction.

Based on its current market valuation, the stock seems cheap, but because of its higher debt and loss-making acquired businesses, it becomes difficult to predict the company's future; therefore, I assign Hold ratings to the stock.

For further details see:

Amneal Pharmaceuticals: Risk Still Persists