AMPY - Amplify Energy: 5x FCF Calls For Significant Upside

2023-03-30 04:39:31 ET

Summary

- Amplify Energy obtained a net settlement payment of $85 million.

- Balance sheet is now healthy being significantly deleveraged to <1x.

- Total executive compensation of $4.8 million annually remains conservative at ~7% of free cash flow.

- A forward free cash flow multiple of 5x limits downside.

- However, there are a few risk factors.

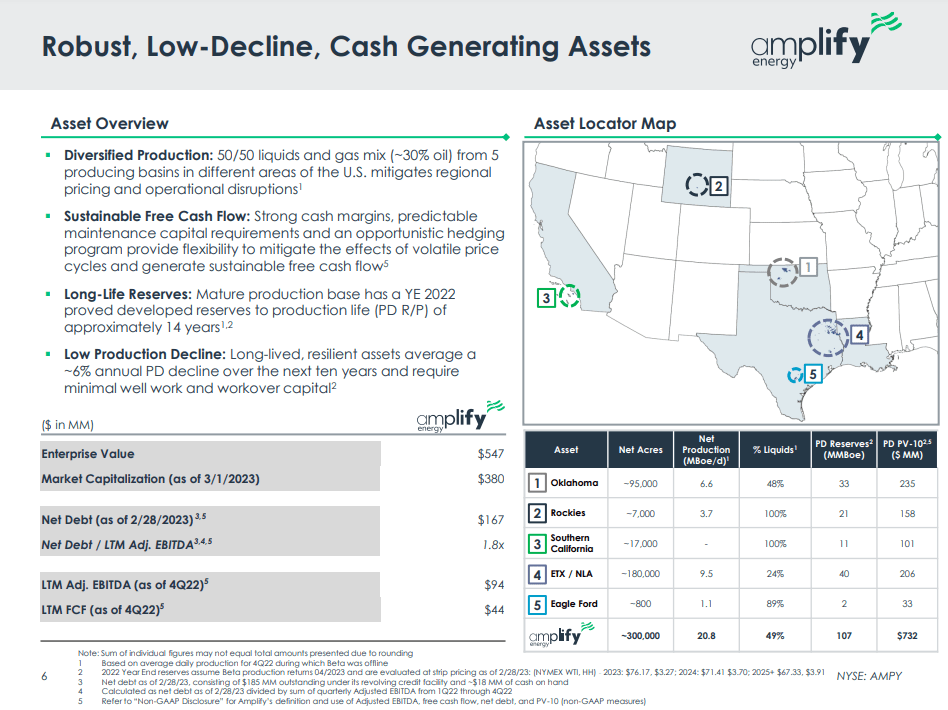

Amplify Energy Corp. ( AMPY ) is an upstream oil & gas play with a proven reserve base of 42% natural gas, 39% oil, and 19% NGLs. Its upstream properties are based out of Oklahoma, the Rockies (Bairoil), East Texas/North Louisiana, and Eagle Ford. In 2022, total revenue from production was slightly more oil than natural gas. Management estimates a reserve-to-production ratio between 14-16 years, as disclosed in their Q4 2022 investor deck .

Amplify Energy Q4 2022 Investor Deck (Amplify Energy Investor Relations)

{kind=link}

This ratio is nuanced given the relationship between production and reserves, i.e., higher production reduces reserve life, but in general, this timeline is arguably quite good in terms of sustainable production. The company also has a midstream pipeline asset in the federal waters offshore Southern California, known as Beta, which was shuttered due to a pipeline incident and plans to restart in the coming weeks.

Settlement Payment & Optionality

Without rehashing the Beta pipeline incident, the ultimate outcome was that although AMPY incurred minor expenses, there was ultimately a favorable net settlement payout of $85 million . As disclosed in the company's Q4 financials, the company was quite heavily leveraged, carrying a $190 million on its revolving credit facility. However, in the Q4 earnings call, management disclosed that as of February 28th, total debt declined to $185 million and cash on hand reached $18 million, resulting in net debt of $167 million. When factoring in the net settlement payment, cash liquidity increases to $103 million and net debt declines to only $82 million. That's a significant improvement in balance sheet health and massive deleveraging event. In effect, between Q4 2022, total debt to assets was about 41%, but if we hypothetically reduce debt by the settlement amount, total debt to assets declines to ~28%. Alternatively, net debt to adjusted EBITDA will improve from over 2x to less than 1x by the end of Q1 2023.

That said, management has not fully disclosed their approach on how the proceeds will be used, i.e., debt reduction, M&A, capital return, etc.

The credit facility interest rate was ~5.36%, so debt reduction would carry a significant return for shareholders, but it would reduce credit risk and potentially be re-rated higher. However, the company could also increase shareholder value with one of the following options:

- retiring shares with an implied free cash flow yield of 16.5+%,

- identify a cheap and strategic bolt-on acquisition to increase scale,

- putting the company up for sale.

My hope is that management will lean into options 1 and 2, while still maintaining enough cash liquidity for a rainy day. However, I'm sure some shareholders would lean for a complete sale of the company to a larger operator, as that more or less guarantees a premium/gain for shareholders.

The Case For Buybacks

Management disclosed that Beta should restart in early April 2023, or within the next couple of weeks. For context, with Beta being shut down, AMPY still generated $93.8 million in adjusted EBITDA and free cash flow of $43 million (defined as adjusted EBITDA less interest and capex). However, we should further reduce this free cash flow amount by share-based compensation [SBC] of $3 million, or $40 million of FCF. A more conservative free cash flow calculation would just be cash from operations less capex and SBC, which would result in $26.7 million.

All that said, the company is essentially operating at trough performance. With Beta coming back online, management guided that adjusted EBITDA and free cash flow would ramp and reach full production in 2023. The 2023 FCF guide was $30 to $50 million, with a 2023-2025 cumulative FCF guide of $180 million. Regardless of how we break that out, annual free cash flow will average about $70 million in 2024 and 2025. If we factor in SBC of about $3-5 million, FCF will be $65-67 million. In other words, total executive compensation between cash payment and non-cash SBC represents only 7% of annualized FCF.

The current market cap is about $261 million. If we add on the net debt of $82 million provides us with an enterprise value of $343 million. Against our revised free cash flow of $65-67 million, we have a free cash flow yield ranging between 19-20%. Now, if we want to be more cautious, we should also think about the delta between management's free cash flow guide and the conservative approach outlined above. All in, TTM FCF was $26.7 million and if we tack on the $30 million of guided improvement, we should be looking at about $56.7 million as a low bar for FY24 and/or FY25, which still offers a 16.5% FCF yield.

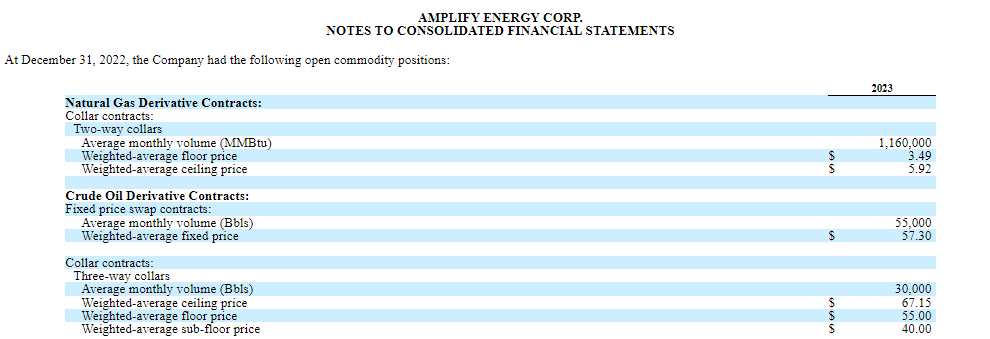

What's the absolute worst case scenario in terms of cash flow? Well, management guided that those results will come to fruition at oil and gas strip prices as of February 28, 2023. At the time of this writing, WTI crude oil prices and natural gas prices have fallen by 6% and 24%, respectively, since February 28 closing prices. About 30-40% of oil pricing is hedged and gas is 65-75% hedged for 2023, both of which roll down significantly to 5-10% and 5-15% in 2024.

Amplify Energy Corp. Hedges (AMPY 2022 Form 10-K Filing)

{kind=link}

Management indicated free cash flow should improve as hedges roll off. That said, however, a significant decline in strip pricing would more than offset hedge protection, especially given the short-duration of the hedge book. Of course, management can add to their 2024 book, but hedging is not free either. So in general, investors should be hoping for oil and gas prices to stabilize and/or increase for sustained operating performance. Higher pricing can also make up for material production shortfalls. Case in point, nearly all Beta production was lost, yet revenue increased largely due to higher selling prices.

Perhaps A Cheap Acquisition

Shareholders have arguably signaled that the possibility of an acquisition is a risk, especially after dumping shares following the language from the Q4 earnings call .

Our improved liquidity and leverage profile, the return of production of Beta and the significant free cash flow from our diversified asset base provides us with flexibility as we consider our strategic path forward and evaluate potential capital return options. In conjunction with that effort, the management team and Board working to evaluate strategic opportunities that could further enhance Amplify's shareholder value.

In general, investors fear destructive acquisitions. However, I've seen E&Ps execute roll up strategies by acquiring small bolt-on acquisitions at reasonable or below-industry valuations. One recent example was Earthstone Energy ( ESTE ), which executed its M&A strategy and generated a handsome return for shareholders. Between pre-pandemic and today, the company's valuation more than doubled within the span of a few years, and was a massive multi-bagger when measured from peak to trough.

In truth, I think investors are mistaken blindly selling their stock by concerning themselves with the potential for a value-destructive acquisition. We also have to remember that management now has time . They are not backed against a wall with their lenders, are steadily deleveraging, and have ample liquidity.

Furthermore, oil and gas prices are largely unpredictable given the numerous complexities of global supply and demand, which include E&P investment, (fickle) production discipline, economic boom/busts, OPEC, government policy, etc. In general, I think the biggest battle is between the lack of investment into oil & gas constraining supply and the ongoing risk of an economic downturn that would impact future demand.

For now, bears remain in control, which is certainly negative for AMPY's existing cash flows, but it could also present management with an opportunity to acquire a smaller operator at a discount. At today's prices? I think it would be difficult to find an acquisition that would produce the FCF yields outlined above. But if oil reprices meaningfully lower, i.e., in the event of a recession, then management could pick up an under levered operator for $0.50 on the dollar looking through the cycle. Just because broader oil & gas M&A activity is slow today, doesn't mean that it cannot or shouldn't happen in the future.

Business For Sale

Of course, AMPY could put itself up for sale to be acquired by a medium or larger scale operator that has greater access to capital and cheaper financing. What is there not to like? Arguably, the largest operators probably won't have an appetite for AMPY's small operation, as it wouldn't move the needle on performance. Deloitte also outlined that oil & gas M&A activity has slowed considerably, with deals representing only 3% of aggregated industry market capitalization. Why? The goal has been dividends and buybacks.

That said, I think there are oil & gas companies that are strategic and can identify a great opportunity when they see one. Again, AMPY has a reasonably healthy reserve to production life, could identify more proven reserves, carries a healthy balance sheet, will reach a net cash position by FY24, and sports a double-digit FCF yield. Even with a premium takeout consideration, another operator could finance the deal with a mixture of cash, debt, and/or equity and pencil out a handsome return for their shareholders.

Risk Factors

There are several potential risks that could negatively impact AMPY:

- Oil and gas prices continue trending lower.

- Further guidance reductions, i.e., higher than expected costs.

- Management overpays in an M&A deal, i.e., dilutive offering.

- Capex is allocated to lower return assets, i.e., gas heavy projects.

Bottom Line

AMPY stock may not be an inherently safe investment; however, with such a bottom-of-the-barrel enterprise valuation, I think the risk of permanent capital impairment is quite low. The company is now in a strong position, has multiple options for capital allocation, and management should proceed carefully to maximize shareholder value. Like my other successful oil and gas investments, this company appears to fit the bill. How do you think AMPY will perform? Let me know what you think in the comments section below. As always, thank you for reading.

For further details see:

Amplify Energy: 5x FCF Calls For Significant Upside