AMPY - Amplify Energy: A Long-Term Winner On Valuation And Quality Assets

2023-08-23 04:19:54 ET

Summary

- Amplify Energy is a potential winner in the oil and gas industry due to its valuation and quality assets.

- AMPY has a solid asset base consisting of low-decline projects across the US, generating consistent cash flows and strong returns.

- Despite the rise of renewables, oil and gas continue to be reliable and accessible energy sources, making investments in AMPY stock appealing.

Investment Summary

Investing into oil and gas might not be exactly what has been hyped over the last few years as many renewable and solar companies saw their valuations skyrocket. But when the prices for those increased and ultimately for many of them also plummeted down, oil and gas companies continued chugging along and passed on massive amounts of earnings to shareholders. These are the real winners and I think that Amplify Energy ( AMPY ) could be one as well given the valuation and quality of the assets the company holds.

The company is included in the oil and gas exploration and production industry where it primarily focuses on engaging in both acquisitions and developments of oil and natural gas in the United States. The need for these resources is unlikely to diminish anytime soon and I think there is still a lot of value to be had there, and as a result, I will be rating AMPY a buy right now.

Still Very Oil And Gas Dependent

One of the major benefits of AMPY right now is the solid asset base they have consisting of solid and low-decline projects across the US.

Assets (Investor Presentation)

The productions are diversified and span across Texas and some parts of California too. The assets are long-lasting reserves and are likely to continue yielding AMPY solid returns over the coming several decades.

One of the major benefits of having such assets is the consistent cash flows they can generate from them. The 5-year average of FCF margins for AMPY is a very strong 25% which is far above the sector average of 6.23%. I think this should equate to a higher premium for the company and a p/FCF of around 6 - 7 should be applied for sure. With sector beating margins a premium is valid and the proven stability of it as well further adds to that argument. That would put a price target of around $14 - $16 for the company, indicating a significant upside from current prices.

Valuation Profile (Investor Presentation)

While it's a common perspective to view the future of oil and gas through a negative lens due to the ascendance of renewables, the narrative is more nuanced than a simple relegation of traditional energy sources. The landscape of energy generation is indeed transforming, with renewables gaining prominence and advocating for a cleaner and more sustainable future.

Energy Consumption (EIA)

Even as ambitious emission targets are set for 2050 , the practicality of completely eradicating oil and gas from the energy mix is complex. These resources continue to offer a reliable and accessible energy source, particularly in regions where alternative options are still developing. Furthermore, the extensive investment in oil and gas infrastructure, including refineries, pipelines, and distribution networks, underscores their role as integral components of our energy ecosystem. Despite the chart above having data until 2021, I think it quite clearly showcases the dependence the US has on both oil and gas to generate energy to support the massive grid they have. This is unlikely to shift in the short term and makes investments into AMPY still very appealing.

Quarterly Result

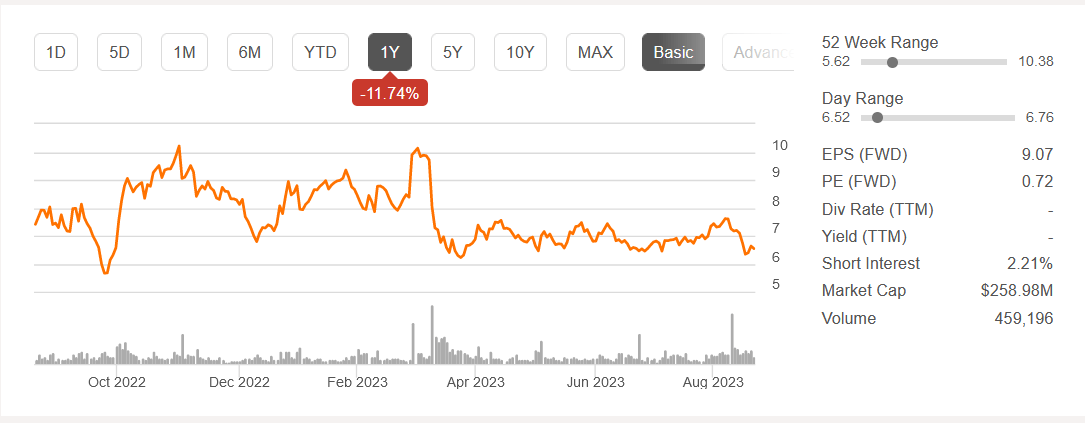

Looking at the results from the last quarter we can see that AMPY had some decent results actually as production levels were up around 9% on a YoY basis. Net cash generated during the quarter was $4.9 million and EPS came in at $0.24, a massive beat from the expected $0.13 for the quarter. This hasn't translated into a higher share price as AMPY posted strong results. Instead, the share price has remained in the same range and that leaves us with a solid opportunity still to capitalize and invest accordingly.

{kind=link}

On a QoQ basis, the FCF was down a fair bit to $6.1 million, but AMPY still has performed quite well maintaining solid margins. The company also reaffirmed its guidance for 2023 and the CEO briefly mentioned that some of the challenges placed on the company in the last 2 years are residing and more positive times seem to lie ahead. I think for upcoming quarters the most important factor to look out for will be an increase in the production levels of the company, this would indicate a more positive and demand market condition for AMPY which with solid operation performances will raise margins and the share price as well.

Risks

While the company has subtly alluded to the possibility of divestitures, it's intriguing to consider the alternative scenario where they veer in the opposite direction. Given the company's existing low leverage, a strategic shift towards initiating acquisitions could potentially trigger a downward trajectory in the stock's trading performance.

Should management opt for a divergent course by pursuing acquisitions, the implications on the stock's valuation could be noteworthy. Acquisitions entail not only financial implications but also strategic alignment and integration challenges. A misstep in this arena could reverberate through the stock's performance, leading to a lack of investor confidence and consequent price depreciation.

Asset Base (Investor Presentation)

Besides the mentioned risks with AMPY, I think another one worth considering is the fact that volatile commodity prices are likely to place slight pressure on AMPY to continue posting quarterly growth. I think it might be unlikely for them to do that all the time, but that is the nature of the oil and gas industry. As long as the asset base is solid then there is little to worry about in my opinion, which is the case with AMPY.

Valuation & Wrap Up

Investing in oil and natural gas is still very much a good opportunity for investors in my opinion. AMPY has showcased resilience and with a great margin of safety for investors, the company looks very appealing to start a position in. As we mentioned earlier, the company has a solid historical FCF margin thanks to the asset base they have developed.

{kind=link}

If we applied a 6 - 7x FCF multiple we are left with an upside of over 100%. Even if we don’t necessarily reach that, the potential still far outweighs the risks here in my opinion. For investors that seek to start a long-term position in an oil and gas company then making AMPY one seems highly advisable right now. Rating AMPY a buy right now.

For further details see:

Amplify Energy: A Long-Term Winner On Valuation And Quality Assets