AMPY - Amplify Energy: Beneficial FCF Guidance May Enhance The Valuation

2023-08-15 13:30:23 ET

Summary

- AMPY delivered impressive FCF expectations and refinanced its balance sheet with a new credit agreement.

- The company has reserves expected to last for a long time and already delivers positive FCF.

- Amplify Energy Corp. appears undervalued, with a discounted future net cash flow significantly higher than its current market capitalization.

Amplify Energy Corp. ( AMPY ) delivered impressive FCF expectations for 2023, and successfully refinanced the balance sheet with a new credit agreement. Taking into account the optimism of management, I believe that future FCF and the debt obtained will be sufficient to finance future acquisition and capital expenditures. I do not like the current exposure to a few clients and the incidence in California, however I believe that the company appears quite undervalued.

Amplify Energy

Amplify Energy is an independent energy company engaged in the exploration, development, and acquisition of oil and natural gas projects. Its activities are conducted within a single operating segment. The company's assets, projects, and properties are concentrated in Oklahoma, federal waters of Southern California, East Texas, and Eagle Ford.

In my view, the most interesting thing about Amplify Energy Corp. is that reserves are expected to last for a long time, close to 14 years. Besides, the company already delivers positive FCF with predictable maintenance capital requirements and a diversified production profile.

Source: IR Presentation

In total, management reports close to 110 MMBoe with net production close to 21.2 MBoe per day and a total of 5 assets geographically diversified.

Source: IR Presentation

Amplify does not have the exploration or extraction tools, the transport, or related services in storage and internal movement within the work camps. These are provided by independent contractors who maintain relationships with the managers of each of their facilities.

Its three main clients are concentrated, at around 50% of the company's sales. They include Sinclair Corporation, Koch Energy Services, and Southwest Energy Lp. The contracts are based on the fulfillment of the demand for them, and are renewed monthly. Hence, the relationships are not guaranteed in the long term. The joint loss of these customers could seriously affect the company's operating flow.

Due to the nature of this type of market, it is important to achieve the sale of the company's total production due to fluctuations in prices, the need to cover operating costs with direct liquidity flows, and the volatility of demand.

With all that mentioned about clients and the work with independent contractors, I believe that Amplify Energy Corp. comes as an interesting play when we assess the valuation of the reserves. In a recent presentation, management noted that the discounted future net cash flow discounted at 10% stands at close to $1.64 billion. It is significantly higher than the current market capitalization of less than $300 million. With this in mind, I suspected that the upside potential in the stock price could be significant.

Amplify defines PV-10 as the present value of estimated future cash inflows from proved oil and natural gas reserves that are calculated using the unweighted arithmetic average first-day-of-the-month prices for the prior 12 months, less future development and operating costs, discounted at 10% per annum to reflect the timing of future cash flows. Source: IR Presentation

Source: IR Presentation Source: Ycharts

Beneficial Guidance And Expectations

In a recent presentation, Amplify Energy reaffirmed its 2023 FCF guidance close to $30-$50 million, and expects to generate 2024 and 2025 FCF close to $200 million with a production of close to 7.3-7.9 million barrels per day of oil and a total of 20-22 MBoe per day.

Source: IR Presentation Source: IR Presentation

I believe that the expectation of market analysts is quite beneficial, and it is worth having a look at it. Market analysts expect 2034 net sales close to $314 million, with 2034 EBITDA of $86.5 million, EBIT of about $51.4 million, and 2034 net income close to $45.2 million with EPS of $1.17.

Source: marketscreener.com

Balance Sheet

As of June 30, 2023, the company reported cash and cash equivalents close to $1 million, accounts receivable of about $63 million, prepaid expenses and other current assets close to $23 million, and total current assets worth close to $89 million.

The ratio of current assets/current liabilities is lower than 1x, however the net debt/FCF ratio and the net debt/EBITDA stand at a good level, so I would not expect a liquidity crisis any time soon.

Property and equipment stands at close to $345 million, with restricted investments of $15 million, deferred tax assets close to $259 million, and total assets of $715 million. The asset/liability ratio is close to 2x, so I would say that the balance sheet is solid.

Source: 10-Q

I would not be worried about the total amount of debt because it is small. Besides, management made significant reductions in 2022 and 2023. Right now, the net debt/LTM Adjusted EBITDA stands at close to 1.2x.

Source: IR Presentation

With accounts payable close to $23 million, the company also reported revenues payable of $21 million, accrued liabilities worth $55 million, and long-term debt close to $120 million. Finally, with asset retirement obligations of $118 million, total liabilities stood at $357 million.

Source: 10-Q

FCF Assessment

Due to international market conditions, highly influenced by changes within this industry due to the war between Russia and Ukraine, reflected in a considerable price increase in fuels and gases for heating and consumption, the company had a significant increase in sales in the last year. This growth is projected to continue throughout 2023 and 2024 although without presenting margins of the same magnitude as in 2022. Under my cash flow model, I assumed that Amplify Energy may not suffer a decrease in the oil price in the near term.

Amplify was affected by an incidence regarding its distribution lines in the coast of California. Based on this, the company has developed a strategic plan to cover these costs and renew these lines. Although they have reached an agreement on time for the payment of a few million dollars for the repair of these pipes, in my view, the numbers are still insufficient.

In my view, successful fulfillment of this strategy is fundamental for the company, and the projections for the moment give positive results, together with the increase in FCF registered recently. In any case, this incidence significantly diminishes the recognition and credibility of the company, with which access to forms of financing may be affected.

With that, I do not expect that higher costs will lead to significant FCF margin decreases. Management provided full explanation about these matters in the last annual report:

On February 2, 2022, the Unified Command announced that response and monitoring efforts have officially concluded for the Incident, and Unified Command would stand down as of such date. We currently estimate that the total costs we have incurred or will incur with respect to the Incident related to actual and projected response and remediation expenses incurred under the direction of the Unified Command and estimates for certain legal fees to be approximately $160.0 million to $170.0 million. Source: 10-k

Accordingly, our assumptions and estimates may change in future periods based on future events and total costs may materially increase; therefore, we can provide no assurance that we will not have to accrue significant additional costs in future periods with respect to the Incident. Source: 10-k

Management successfully received new financing from debt holders, which would most likely interest equity investors. Taking into account the incidence in California, the fact that Amplify Energy could negotiate new debt agreements is quite beneficial. With this in mind, I do not think that the company suffered such reputational damage.

The aggregate principal amount of loans outstanding under the New Credit Facility as of July 31, 2023, was $120.0 million. Source: 10-Q

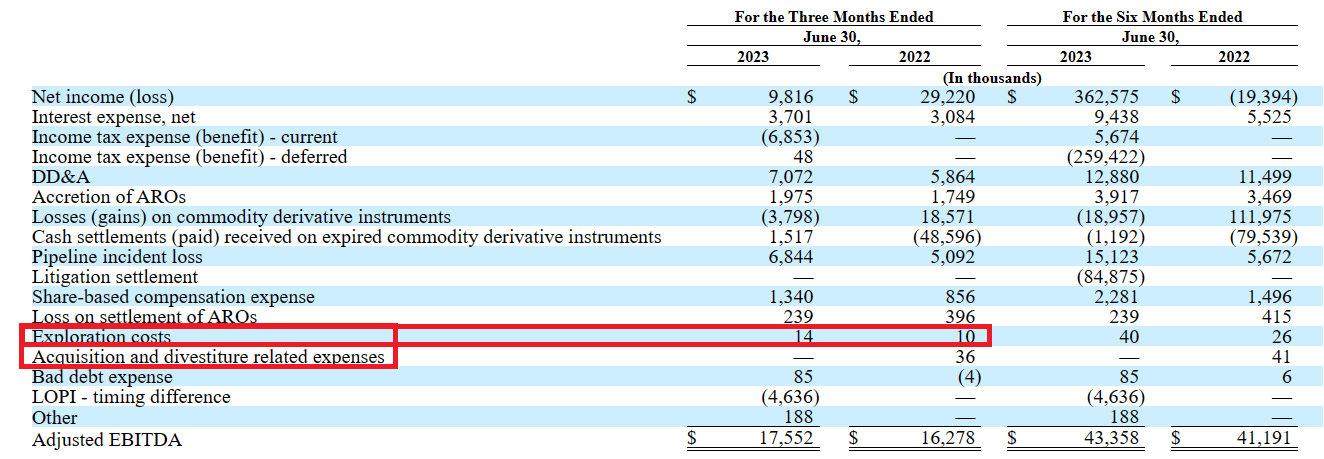

With that about the new debt and the words from management, I am quite optimistic about the future of Amplify Energy Corp. In my view, if the current CFO and the debt financing are sufficient to finance future capital expenditures and acquisitions, we may also expect FCF growth. I believe that acquisitions may also lead to an increase in the amount of reserves. In this regard, it is also worth noting that exploration costs and acquisition related expenses increased in the quarter ended June 30, 2023 and the six months ended June 30, 2023 as compared to the figures reported in the same period in 2022.

Based on our current oil and natural gas price expectations, we believe our cash flows provided by operating activities and availability under our New Credit Facility will provide us with the financial flexibility necessary to meet our cash requirements, including normal operating needs, and to pursue our currently planned development activities. Source: 10-Q

{kind=link}

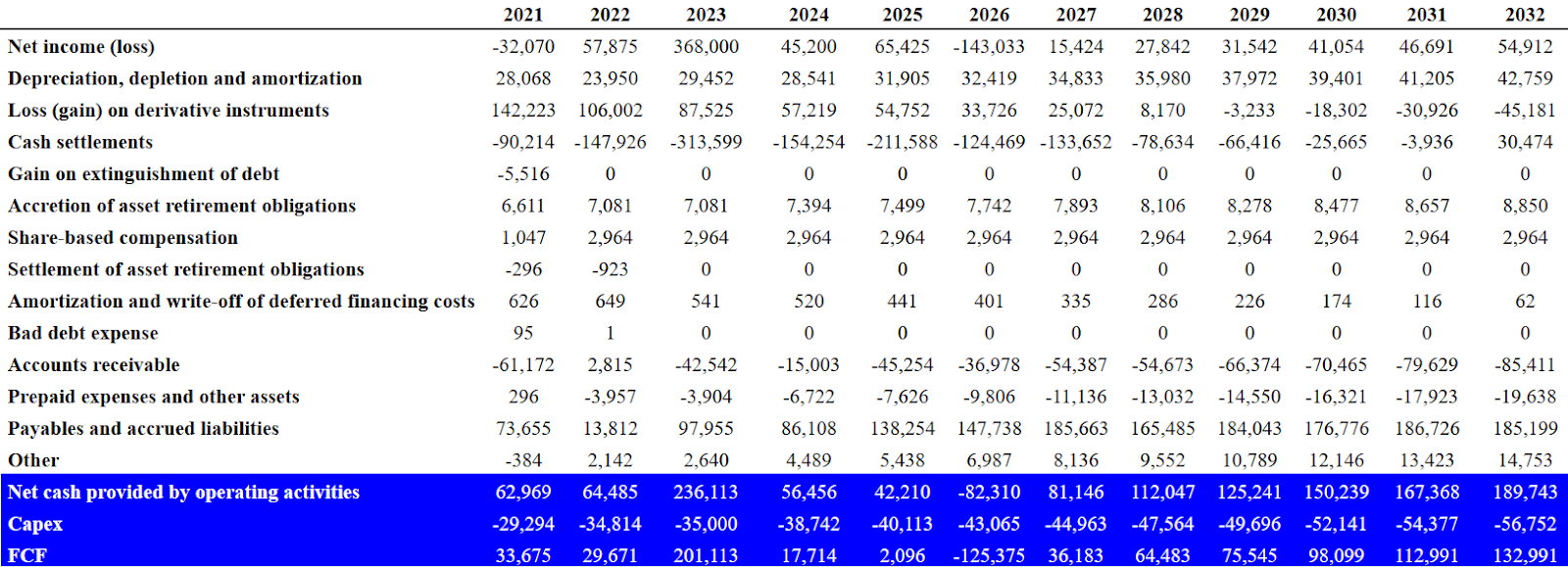

My numbers included stable and positive net income from 2023 to 2032, with increases in D&A and stable stock-based compensation. The results also included positive FCF in most years from 2023 to 2032. I believe that my numbers are conservative.

The model included 2032 net income close to $54 million, with 2032 depreciation, depletion, and amortization close to $42 million, cash settlements worth $30 million, accretion of asset retirement obligations worth $8 million, and share-based compensation close to $2 million.

Also, with changes in accounts receivable of -$86 million, changes in prepaid expenses and other assets of -$20 million, and changes in payables and accrued liabilities of $185 million, the CFO would be about $189 million. Finally, if we assume 2032 capex close to -$57 million, 2032 FCF would be about $132 million.

{kind=link}

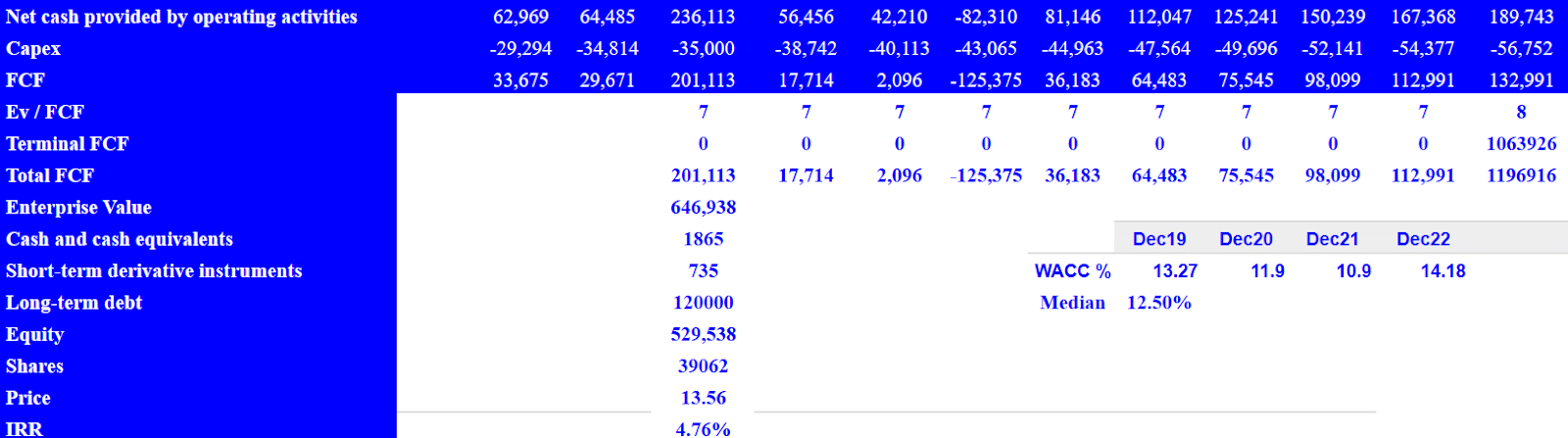

Now, with an EV/FCF of 8x, the implied enterprise value would be close to $646 million. In the past, the company traded at 7x 5 Years Median FCF, so I would say that the terminal EV/FCF assumed is reasonable.

Source: Ycharts

If we add cash and cash equivalents of $1 million and long-term debt close to $120 million, the implied equity would be $529 million, and the fair price would stand at $13-$14 per share. Hence, we would be talking about an IRR of 4.76%.

{kind=link}

Competitors

Competition in this area is high, and is given by the search for new opportunities as well as hiring insured personnel or companies that provide services within the extraction areas. This competition is also transferred to the one with the capital available within the market. Since their competitors are companies with greater resources, the cost of access to capital can be much lower for them. In this sense, the ability that Amplify has to locate opportunities for the acquisition and development of projects and the ability to carry out these transactions directly are a fundamental factor in the competitive framework of the company, exposed to higher costs and sales conditions with lower margins than its competitors.

Risks

First, the incidence in California creates a series of risk conditions for the company, which have to do with the ability to cover costs, exposure to scrutiny and legal disputes, access to credit lines or the capital market, and the suspension of operations in the pipelines. In addition, the concentration of attention and efforts to correct the operating and recognition costs of this incidence can generate distractions in other areas of development of the company.

Similarly, Amplify is exposed to conditions of the energy markets, such as price volatility, speculation about reserves, and general economic conditions. This factor also applies to the calculation of available reserves and the current hedging strategy, which may not offer the liquidity results estimated by the company's management. The inability to undertake operations in other areas with liquefied and natural gas reserves may seriously alter Amplify's infrastructure.

Conclusion

Even considering the incidence in California, Amplify Energy Corp. successfully refinanced its balance sheet in July 2023, which I think could bring a lot of optimism to the market. In my view, equity holders may buy more shares as soon as they see that debt holders do not seem worried about the future operations of Amplify Energy. With stable FCF margins, predictable production, and a diversified list of assets, I think that Amplify Energy will most likely be able to finance future acquisitions and capex thanks to cash flow from operations and the debt obtained. Even taking into account certain risks from concentration of clients or failed hedging strategies, Amplify Energy does look significantly undervalued.

For further details see:

Amplify Energy: Beneficial FCF Guidance May Enhance The Valuation