AMPY - Amplify Energy: Better Hedged And Upcoming Catalysts

2024-01-02 08:09:56 ET

Summary

- Amplify Energy is sustaining production, controlling costs, and repaying its credit facility, but shares have fallen by 12%.

- The company has expanded its hedge book to mitigate risks associated with macroeconomic factors.

- Two potential catalysts for the company include monetizing Bairoil assets and increasing annual free cash flow.

Amplify Energy Corp. ( AMPY ) continues to operate the business well by sustaining production, controlling costs, repaying its revolving credit facility, and identifying potential asset sales. Although management has been executing, shares have fallen by approximately 12% since my initial writeup .

Part of that has to do with crude oil prices being down slightly and the weaker investor interest among smaller scale E&P operators. Typically small operators have weaker economies of scale and less diversified operations, where costs can eat into profitability, particularly in pricing downcycles. From a macro perspective, S&P Global Commodity Insights reported that production growth is "accelerating robustly, particularly in the United States." Certainly that would bring pricing pressure in 2024. Additionally, economic conditions also remain a point of concern, with recession risks still elevated , according to the NY Fed. Of course, these matters are outside Amplify Energy's control, so shareholders should be focused on what management is doing and allow macroeconomics provide the value dislocations, i.e., cheap stocks.

Amplify Energy provided another helpful investor presentation following Q3 2023 earnings. One important slide that caught my attention and should provide some consolation to shareholders was slide 15, as shown below:

Amplify Energy Presentation Slide 15 (Amplify Energy Q3 2023 Presentation)

{kind=link}

If you look back to March 2023, management had only hedged 30-40% and 5-10% of oil production in 2023 and 2024, respectively, but over recent quarters has management expanded its hedge book to cover 65-70% of oil pricing in 2024, 45-50% in 2025, and even 15-20% in 2026. The company has also verified in its securities filings that its hedge strategy is to cover at least 50-75% of commodity production. In any event, this hedge book helps mitigate the aforementioned macroeconomic risks.

Q3 2023 Update

This earnings report was another decent print. I think the biggest highlight from an operating perspective is that Beta is fully operationally and actually providing greater production than pre-shutdown levels: "Current production rates at Beta are back to pre-shutdown levels with additional wells scheduled to be returned to production. We anticipate having higher gross production rates compared to the pre shutdown period before effects of new development drilling planned for 2024."

Otherwise, Q3 2023 production volume was relatively stable with oil being slightly up and NGLs and natural gas slightly down. The first nine months ended Sept. 2023 had flat average net production from 20.6 MBoe/d last year to 20.4 MBoe/d this year. As we all know, oil and gas prices have come down in the past year, so that's translated to reduced revenue. Turning to operating expenses, when excluding oil & gas hedging gains and losses and pipeline incident expenses, total operating expenses were very roughly flat year-over-year for both the three and nine month reporting periods. So management is doing an excellent job with cost discipline and is regularly taking action to control expenses within its fields.

Lastly, Q3 net interest expenses increased from $4 million last year to $4.5 million this year, primarily due to higher interest rates and the amortization and write-off of deferred issuance costs. This line is also largely immaterial, but as management actively repays its credit facility, not only do interest payments go away, but it provides the company with financial flexibility and the ability to eventually provide capital return. Over the last three years, management has made considerable progress and now were within shooting distance of the company turning to a net cash position.

Two Catalysts

Management has outlined varied catalysts for shareholders quite plainly on slide 4 of their investor presentation. I believe all of these action items are sound to maximize shareholder value, so let's have a look:

Amplify Energy Presentation Slide 4 (Amplify Energy Q3 2023 Presentation)

{kind=link}

With that, there are two catalysts in particular that I think have relatively greater potential to materially re-rate shares higher over the next year.

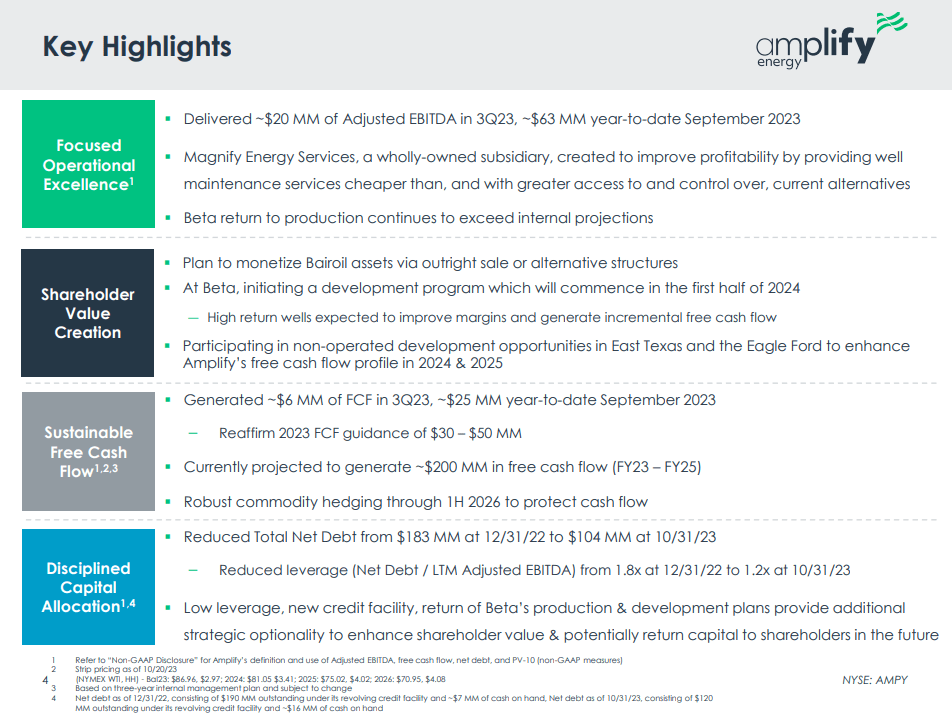

- Plan to monetize Bairoil assets via outright sale or alternative structures

- Currently projected to generated ~$200 mm in free cash flow (FY23-FY25)

Speaking to the first bullet, this asset only represents approximately 14% of annualized production, yet has 22 years of reserve to production life. So it's a valuable asset, but a relatively small piece of the overall business. Ultimately management would look for larger operators that can achieve synergies where a sale makes the most sense. Within their investor deck, management outlined a PD PV-10 valuation of $200 million, for what that's worth. Management spoke to this transaction on the Q3 earnings call , and that additional detail would be provided in Q1.

Lastly, I guess I’d say we’re under no real pressure to sell the asset, so we will only transact if the value exceeds what we believe to be the hold value. We think we’ll run a thorough process with our investment bank adviser but we’ll have more to announce upon that next year, following the first quarter when we initiate the process.

Being a slow declining asset and with energy prices still at reasonably favorable levels, I think there's good potential for this asset. Executing the transaction at a reasonable multiple would definitely garner a positive response from the market. Moreover, proceeds would be used to help accelerate its debt payment schedule and help eliminate the remainder.

Regarding the second bullet, this catalyst itself is straightforward. The business is generating around $30-50 million in annualized free cash flow today, defined as adjusted EBITDA less interest expense and capex. Granted there are some real operating costs that are removed by the adjusted EBITDA figure (which I described in my prior writeup), they are not significant enough to raise a yellow flag in my book. To account for this however, I think simply adding back certain costs or applying a haircut to their guided FCF will still produce a realistic result. For example, annualized stock based compensation is nearly $5 million, and this is appropriate to deduct from FCF. Tax expenses can be more tricky from year to year given the potential for asset sales and writeoffs that can provide tax shields. But eventually, sustained profitability will probably bring the business closer to the statutory corporate tax rate of 21%, which could be material. That said, depreciation and other expenses can provide significant help on effective tax rates and cash taxes.

Nonetheless, management is guiding that annualized free cash flow will step up from $40 million at midpoint in 2023 to $80 million at midpoint for 2024 and 2025. At face value, that will also help toward eliminating the remainder of its debt, not even factoring the potential asset sale.

Now we can work around management's assumptions and create our own. If we forecast that management will achieve its annual free cash flow target, then we can update their definition (i.e. cash from operations less capex, taxes, and share based compensation) or within the range of $60 million. Against its enterprise value of $345 million, that's still only priced at 5.75x cash flow. We could put together a valuation matrix, but my point is that either management has to either A) be directionally wrong in their forecasting or B) energy prices would have to collapse for shares to be unattractive here. Of course, there's room for upside or downside but it seems achievable.

Bottom Line

Thus far, AMPY shares have underperformed the broader market, but that's not surprising given the way energy prices have trended over the last nine months. Shareholders may also being shying away from AMPY given its small production scale relative to alternatives in the market, not even factoring all of the potential macro and technical trading factors. That said, management is clearly making progress on the business, has outlined catalysts, and has given investors the option to accumulate good value in plain sight. Thank you for reading and please comment below.

For further details see:

Amplify Energy: Better Hedged And Upcoming Catalysts