AMPY - Amplify Energy: Improved Projected Free Cash Flow Despite New Hedges

2023-10-28 07:12:52 ET

Summary

- Amplify added a significant amount of hedges over the next few years due to requirements from its new credit facility.

- It has hedged most of its natural gas production, leaving it with limited upside potential from natural gas prices.

- Amplify does have more upside potential from oil prices and prices for NGLs still.

- Amplify's 2024 to 2026 hedges have an estimated negative $11 million value at the current strip.

- It is still projected to generate $220 million in free cash flow between 2023 and 2025 at the current strip.

Amplify Energy (AMPY) added a significant amount of hedges over the next few years in conjunction with its new credit facility . It previously only had a modest amount of hedges for 2024, but now has hedged the majority of its expected production in 2024 and 2025.

These new hedges were added when commodity prices were slightly weaker, so at current strip Amplify is projected to end up with $11 million in hedging losses between 2024 and 2026, compared to $1 million in hedging losses based on its prior hedging position. Amplify's exposure to upside in natural gas prices is also significantly limited, although it retains more exposure to oil pricing upside.

Despite these hedges Amplify is expected to generate $220 million in free cash flow between 2023 and 2025 at current strip prices. This would result in it having around $45 million in net cash at the end of 2025 after factoring in its required sinking fund payments for Beta decommissioning responsibilities.

I am maintaining my estimate of Amplify's value at $11 per share based on long-term $75 WTI oil and $3.75 NYMEX gas. My near-term free cash flow estimates for Amplify has improved a bit compared to my earlier projections , but that is balanced out by its reduced ability (due to hedges) to benefit from any spikes in commodity prices.

Notes On Hedges

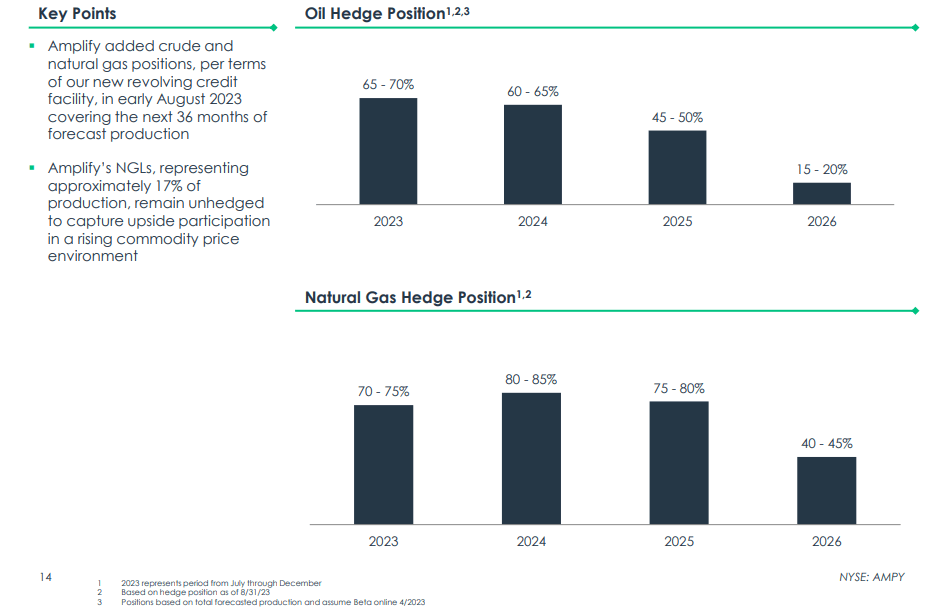

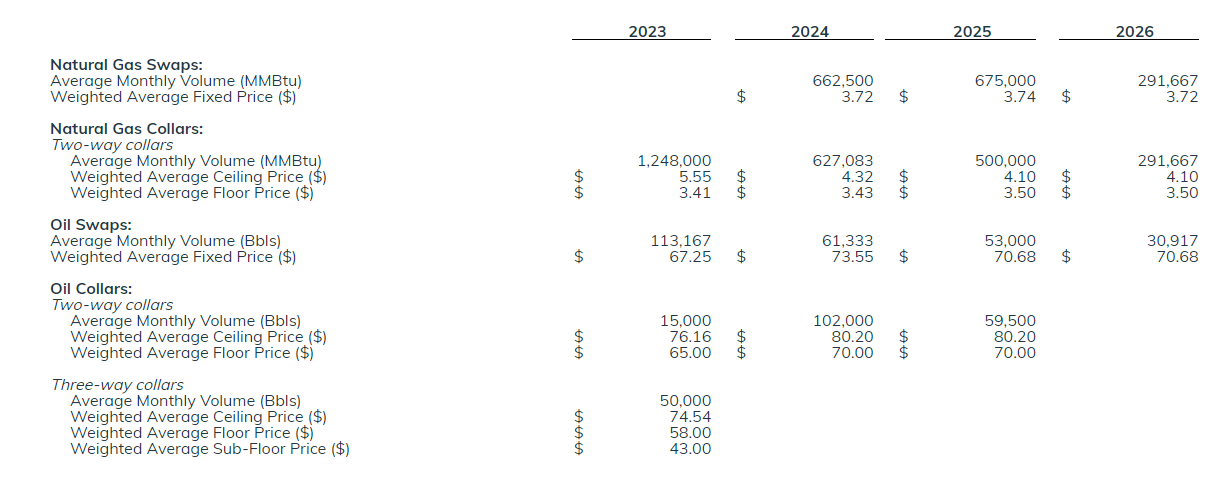

Amplify Energy is required to hedge a significant amount of its forecasted proved developed producing production volumes as a result of its credit facility agreement. It is required to hedge 75+% of its forecasted PDP production volumes (oil and natural gas) for the first 24 months starting August 2023, and 50% of its forecasted PDP production volumes for the 12 month period starting August 2025.

This has resulted in Amplify having around 60% to 65% of its expected 2024 oil production hedged along with 45% to 50% of its expected 2025 oil production hedged. Amplify has more of its natural gas production hedged (close to 80% in 2024 and 2025) while its NGLs are unhedged.

{kind=link}

At current strip prices, Amplify's hedges are generally a bit under water. From Q4 2023 onwards, Amplify's hedges have approximately negative $18 million in estimated value at current strip prices. This includes $7 million in projected hedging losses in Q4 2023, $3 million in projected hedging losses in 2024, $6 million in projected hedging losses in 2025 and $2 million in projected hedging losses in 2026 at current strip.

{kind=link}

The hedges increase the chances that Amplify Energy can continue to generate positive cash flow and pay down its debt, but the hedges also reduce its upside exposure if commodity prices improve. Amplify has a reasonable amount of exposure to oil price upside, but won't really benefit that much from an increase in natural gas prices (from current strip) over the next couple years.

Free Cash Flow And Valuation

Amplify previously mentioned that it expected $200 million in free cash flow during 2023 to 2025, but the improvement in oil prices (with oil prices typically being a few dollars higher than its assumptions) should allow it to generate closer to $220 million in free cash flow during this period. This is based on current strip prices and is inclusive of the impact of Amplify's added hedges. Amplify should thus be able to end 2025 with around $45 million in cash on hand after factoring in the sinking fund payments for Beta's decommissioning obligations. These payments do not appear to be included in Amplify's free cash flow calculations as they are labeled as additions to restricted investments.

I am maintaining my estimated value for Amplify at $11 per share in a long-term $75 WTI oil and $3.75 NYMEX gas environment.

Conclusion

Amplify Energy was forced to add a significant amount of hedges over the next few years as part of its new credit facility agreement. This has left it hedged on most of its projected natural gas production in 2024 and 2025 and over 40% of its projected natural gas production for 2026. Amplify is less hedged on its projected oil production and is unhedged on its production of NGLs, so those commodities are where Amplify's potential upside will come from.

At current strip, Amplify is expected to generate around $220 million in free cash flow between 2023 to 2025, giving it a decent net cash position by the end of 2025.

Amplify's value is estimated at $11 per share at long-term $75 WTI oil and $3.75 NYMEX gas. It may be able to generate over $5.50 per share in free cash flow between 2023 to 2025 at current strip, despite the negative value of its hedges.

For further details see:

Amplify Energy: Improved Projected Free Cash Flow Despite New Hedges