AMPY - Amplify Energy: Q3 Results Suggest An Attractive Trajectory

2023-11-07 22:26:53 ET

Summary

- Amplify appears attractively valued, and there is room for the price to roughly double from here on comparative valuation grounds.

- Previously, capital allocation was a risk, but a proposal to sell a material asset (Bairoil) in H1 2024 is welcome.

- There is endemic risk in the energy sector from commodity pricing, but AMPY has reduced its debt load and has hedged out the majority of production to 2025.

- If a material sale occurs in 2024, it may provide a catalyst for the shares to re-rate.

Amplify Energy Corp. (AMPY) remains relatively attractive at current levels. Their Q3 2023 earnings announcement showed that they are a potential seller of assets and that they plan to invest in growing production of their Beta asset. They are also starting an internal energy services project (called Magnify) to bring down certain external costs.

Amplify's Bairoil marketing process is important as it signals a potentially sensible approach to asset allocation, which was a clear risk. Their operating performance was okay, and importantly full-year guidance was confirmed, which suggests a reasonable Q4.

Valuation

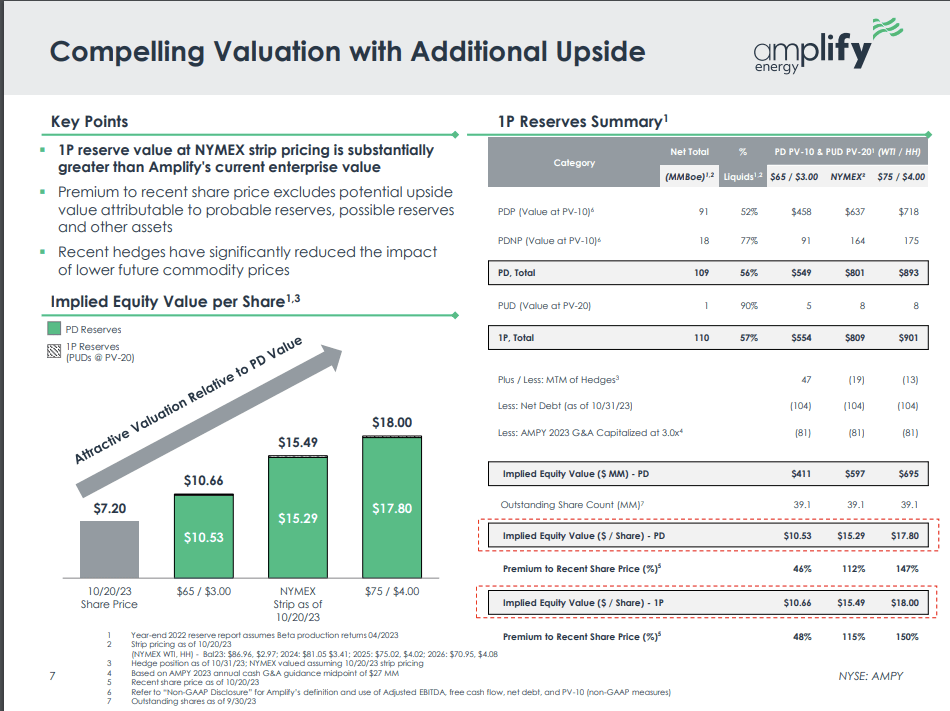

In terms of valuation, Amplify values their production at strip each quarter using an arguably somewhat promotional approach. In doing this they capitalize their G&A costs at a low 3x multiple (when 6x is likely more appropriate), but adjusting for that, strip pricing suggests the share price could trade close to $13/share.

In fact, that estimate is becoming more robust as they increasingly hedge out their production, in part as debt covenants require it.

Amplify's estimate of valuation (Amplify Q3 Investor Presentation)

{kind=link}

Disposal Possibility

Amplify intends to market its Bairoil assets for sale in the first quarter of next year. These are located in the Rockies, and Amplify believes another owner may be better positioned to operate these assets. It's a slightly odd announcement in that they have other assets they could sell more simply, such as an 8% working interest in Eagle Ford that would presumably be very easy to divest as it's more a financial holding, or indeed the whole company which is arguably a sub-scale producer.

Nonetheless, it is encouraging that Amplify is positioning itself as a seller, not a buyer. However, as a smaller producer, if Bairoil is sold then arguably there is even less operational leverage for the businesses' fixed costs. It may have been better for Amplify to launch a broader exploratory process rather than ring-fencing just Bairoil for sale, but still, the direction is welcome.

Bairoil could fetch around $200M looking at PV-10 values, so a sale could make the company debt-free. As of Q3 2023, net debt currently stands at $104M. If they were to achieve a fair price for the Bairoil asset and use the proceeds in a shareholder-friendly manner, then it could be a catalyst for the shares re-rating.

However, taxation on any sale could make the picture less rosy than it initially appears, though still likely positive for shareholders. One might also question why they are announcing the sale now but not starting the process until Q1 2024.

Hedging

Hedging is arguably becoming a positive for Amplify. They got punished by the market previously when they announced free cash flow targets but hadn't fully hedged their production, making their guidance potentially risky. However, now they are 50% to 80% hedged to FY2025, depending on the year and product, making their guidance of $200M of FCF for FY2023-2025 perhaps a little more robust, and it once again serves to highlight that they are perhaps attractively valued as their market cap is currently $240M i.e. a 20% more than 3 years of estimated free cash flow. If you don't think we're in a super-normal energy pricing period and don't think Amplify will waste cash then the company does look interesting today.

Comparative Valuation

The 'problem' though with energy investing currently is arguably a lot of the sector seems cheap, so here I'll compare the company with a few comparative ideas in the 'sector' more broadly.

For example, you have Blackstone Minerals on a 10% yield and 9x price to earnings. As a royalty company, the business model is arguably far more robust than Amplify's, but if Amplify were on 10x FCF of $50M-$70M that would imply a share price of $12/share-$18/share. Of course, that's a rich valuation, as I'd rather own a royalty business, which is more robust should energy prices decline (as they just take a fee off the top of prices and spend no capital), but it does suggest Amplify is attractively valued at the current price of $6.18/share.

Another way to look at things comparatively is a U.S. energy ETF currently has an 8x PE. Now, that's obviously a mixed bag of companies and business models compared to Amplify, but assuming Amplify's underlying earnings are around $50M-$60M that suggests a price of $10-$12/share. Again, a substantial margin of safety to the current valuation, even within the energy sector.

What's Holding Amplify Back?

It does seem Amplify is inexpensive and that's been true for a while. The removal of just about all risks related to the oil spill from 2021 has not caused the shares to fully re-rate.

The announcement that the company may sell assets could be a positive, if it occurs in H1 2024, but then does beg the question of what happens to the remainder of the company. It is interesting that the company fell on earnings, arguably Q3 numbers were soft, but full-year guidance remains intact.

Management's historic guidance has been somewhat subject to energy price swings, though arguably now with more hedging in place, the guidance is more robust. Maybe the market is still sounding out the degree to which it can trust guidance.

Conclusion

Amplify does seem to be relatively cheap and broadly doing the right things for shareholders. I don't have to work too hard to arrive at a valuation of around double the current share price. The question is what it might take to get there. Of course, where energy prices go from here is a major question, but the company is increasingly hedged into 2025.

Q3 results did suggest some appropriate capital allocation decisions from the company. There is arguably a lot of value in the energy sector at the moment, but if Amplify can sell its Bairoil assets at a reasonable price in H1 2024 and use the proceeds sensibly, such as, for example, becoming debt-free, and buying back shares, then 2024 could be a good year for shareholders. It would be even better if the M&A activity that appears to be picking up in the energy sector caused someone to make a bid for the company.

For further details see:

Amplify Energy: Q3 Results Suggest An Attractive Trajectory