AMSSY - ams-OSRAM Is A Turnaround Candidate Shares Could Double Or Even Multiply

2023-09-25 09:00:36 ET

Summary

- ams-OSRAM has been on a downward trajectory ever since the Austrian sensor company ams acquired the German lighting company Osram Licht in 2020.

- A new CEO and a new business strategy could be the starting point for a turnaround to a smaller, but more profitable company.

- If things go well and according to plan, shares could double or multiply over the next 1-3 years.

(Note: All amounts in the article are in EUR. At the current exchange rate, 1 EUR is around 1.06 USD. Although ams-OSRAM is headquartered in Austria, the primary listing is on the SWISS Stock Exchange, and the company publishes financial information in EUR. I am following that practice throughout the article. )

Investment Thesis

The combined ams-OSRAM ( OTCPK:AMSSY ) goes back to 2020 when the Austrian sensor company ams bought the significantly larger German lighting company Osram Licht AG, which was twice its size.

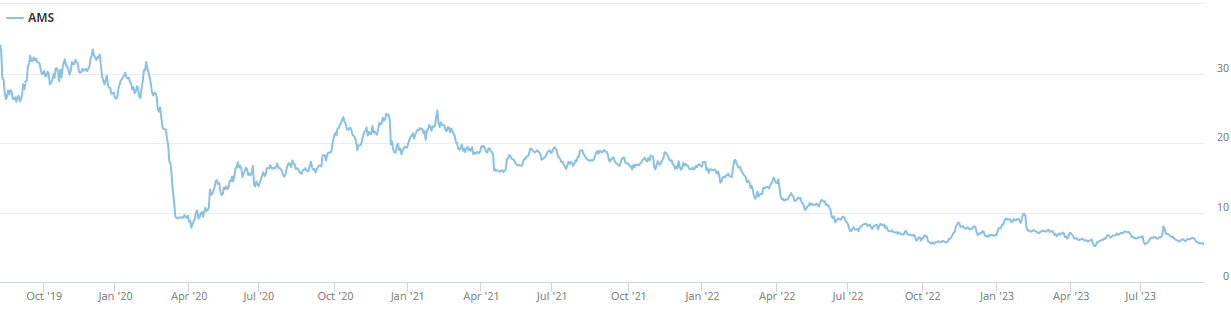

ams had become big as a supplier for Apple (NASDAQ: AAPL ) and the iPhone. The share price had gone up 4x between 2017 and 2018. In August 2019, when the first offer for Osram Licht was announced, it was still over 30 CHF. It is around 5.5 CHF now.

ams-OSRAM share price in CHF (Source: SWIS Stock Exchange))

{kind=link}

The integration did not go well. The ams CEO Alexander Everke wanted to create a European champion for sensor and light technology. The desire to reduce the dependency on the consumer electronics sector, and specifically the largest ams customer Apple, also played a role in the decision.

Instead, the company has faced one headwind after the other, from execution issues to deteriorating market conditions, and reduced business from Apple. The stock is down more than 80 percent three years after the takeover.

However, I think now ams-OSRAM deserves a closer look as many things are changing and in motion.

After a new supervisory board was installed in 2022 (more on that later), Everke had to go in March this year, and a new CEO, Aldo Kamper , joined. Kamper previously was the CEO of the German auto parts manufacturer Leoni AG, but he is an OSRAM veteran and spent most of his career there in various senior leadership roles.

Kamper announced a new strategy in July. The goal is to shrink the company and make it more profitable by focusing on areas where ams-OSRAM has technology leadership and a significant addressable market, which are LEDs and sensor chips for the automotive sector, industry, and medical technology. The profitability target is an EBIT margin of 15%. Discounting goodwill write-offs the EBIT margin in Q2 2023 was just 5.9%. After losing around 20 percent of the current revenue, going forward sales should grow with a CAGR of 6-10%.

If it works, I think the share price could at least double in a timeframe of one to three years. ams-OSRAM is a speculative Buy, in my view. I am on purpose saying speculative as there is an obvious execution risk. However, the share price is currently low, and despite the problems, ams-OSRAM is profitable in its operational business. Based on the adjusted EPS for Q2 2023, which does not include a one-time write-down of 1.32bn goodwill, the P/E ratio is just 11.9. Therefore, shares are not expensive, and if the new CEO delivers on the new strategy, there is a lot of room upward.

Company Overview

The takeover of Osram Licht by the much smaller ams had its fair share of drama . Osram Licht was not a willing takeover target, the influential German IG Metall union even asked key shareholders not to agree. Eventually, ams was successful, but in 2020 it had to do a capital increase and took on considerable debt.

In hindsight, it swallowed more than it could chew. Also, Osram was not in such good shape at the time. In 2019 revenue declined by 13.1%, margins almost halved and the business was barely FCF positive (17mn euros on revenue of 3.4bn).

ams on the other side had a significantly higher profit margin in 2019 than Osram (31% compared to 8.9%) and increased its revenue in 2019 by 32% (between 2016 and 2019 revenue multiplied 4x). However, a lot of this was driven by business from Apple, especially 3D sensors for facial recognition. This created a significant dependency and customer concentration risk, and in 2021 the company lost the 3D sensor business with Apple.

ams-OSRAM has disposed of several Osram Licht businesses but generated only around 600mn euros from this – a fraction of the purchase price.

The company now has two business segments: 1) Semiconductors and 2) Lamps & Systems (short: L&S). The Semiconductors segment is the larger one by far. In Q2 2023 it contributed 71% to the revenue, and only 29% came from the L&S segment. The exposure to semiconductors is even larger than those numbers, as the company also produces specialty lamps for semiconductor manufacturing – a business that showed slow traction in the quarter as you would expect given the current slowdown in most semiconductor segments.

ams-OSRAM has strong market positions in LEDs (where it is a technology leader in micro-LEDs) and light sensors. According to a recent investor presentation , it is #2 worldwide in those segments, not far behind Nichia from Japan in LEDs and the Swiss STMicroelectronics (NYSE: STM ) in light sensors. ams-OSRAM claims to be the market leader in traditional auto lamps and bulbs, but that business is neither especially high-tech nor is it growing.

From an industry segment perspective, more than 80% are from Automotive (51%), Industrial and Medical (31%). The rest (18%) is from the Consumer segment.

Products range from lasers for Lidar, LED lighting, sensors for robotics, CT scanning, etc. to specialty sensors (like driver monitoring) and UV light disinfection.

Micro-LEDs are a disruptive technology where ams-OSRAM is a leader. The company focuses on the very small 10x10 µm size and is investing over 1bn in its manufacturing plant in Malaysia . This could also lead again to a larger cooperation with Apple , which is itself investing heavily in micro-LEDs to decrease its reliance on Samsung for display technology.

In one area, the takeover of Osram Licht has been successful for ams: reducing customer concentration risk. The Top 3 customers are now responsible for only 18% of revenues and the Top 10 for 32%. The company also has a balanced geographical sales distribution with APAC accounting for 47% of revenue, EMEA for 31%, and the Americas for 22%.

Q2 2023 results

2022 was a disappointing year for ams-OSRAM. Revenue declined by 4% and the year ended with a net loss of 444mn euros, after a net loss of 31mn in 2021. Key drivers were impairment losses on goodwill and property, plant, and equipment. Q1 2023 was not much better. Revenue declined again by 21% QoQ and 26% YoY. The quarter ended with a net loss of 90mn euros.

In Q2 2023 revenue declined again QoQ by 8% to 851mn. YoY the decline was 28%. Part of this is due to the divestment of Osram Licht assets. However, as the total proceeds from those divestments since 2021 are only 600mn, I assume it is the smaller part.

A bright spot is that the EBIT margin increased QoQ from 5.4% in Q1 to 5.9%. YoY the margin decreased significantly though; it was 8% last year. A reassessment of the long-term business outlook led to a non-cash impairment on goodwill of 1.31bn, so the quarter ended with a huge loss of 1.34bn euros. Without that impairment, the net result though was positive at 31mn, a significant improvement both QoQ and YoY. In Q1 2023 the net result was 6mn and in Q2 2022 the net result was negative at -54mn.

The operating cash flow also improved significantly to 232mn. In Q2 2022 it was just 100mn. FCF was negative though at -31mn due to CAPEX expenses driven by upgrades to manufacturing facilities in Austria, Germany, and Malaysia where ams-OSRAM is building an industry-first 8-inch LED facility. ams-OSRAM says it intends to return to the long-term CAPEX target of 10% of revenue in 2025, but at least until then, we should expect CAPEX to be elevated. The company has recently been awarded a 300mn research and development grant in the context of the European Union IPCEI (Important Projects of Common European Interest) program, which should help.

A new supervisory board, a new CEO, and a new strategy

It is remarkable that the previous CEO Alexander Everke could hold on for so long, if you look at the 90%+ share price decline over the last years and the dismal financial results, with practically every reporting period ending with a disappointment.

I think the reason why he had to go is simply because the supervisory board was changed last year. There is a new chairwoman, Margarete Haase, and a new deputy chairman, Wolfgang Leitner. I have to admit that I do not know much about Haase, but I am very familiar with Wolfgang Leitner . Leitner has stellar credentials, having led the Austrian machinery builder and plant engineering company Andritz ( OTCPK:ADRZF , OTCPK:ADRZY ) as CEO for over 20 years until 2022. In that time revenue multiplied 30x, and so did the share price – making Leitner a billionaire on the way.

Leitner lives in the Austrian city of Graz (Andritz is also the name of a district of Graz), which is just a few kilometers away from the ams-OSRAM headquarters, whereas Everke was criticized for running the company from his Portugal vacation home – a good change in my view.

This is obviously subjective, but for me, the involvement of Leitner is a key reason to think ams-OSRAM can execute the turnaround.

At the beginning of April 2023, Aldo Kamper became the new CEO. In July he announced a new strategy and updated business model. The main goal is to make ams-OSRAM smaller, but more profitable.

Strategy update

The company will focus on LED and sensor chips for the automotive sector, industry, and medical technology. Less profitable businesses with sales of 300 to 400 million euros will be discontinued. Interestingly this includes prisms and lenses for smartphones and computers, so the ams part in particular is likely to be affected.

The smartphone components business made ams successful thanks to its largest customer Apple, but it will only play a minor role in the future. As a consequence, ams-OSRAM wrote off 1.3bn euros on the goodwill of less successful business areas in Q2 2023.

The new strategy has two key objectives: 1) increased profitability with an EBIT margin of 15% from 2026 onwards; 2) annual revenue growth of 6-10% (after the exit from 300-400mn euros of non-core semiconductor business in 2023).

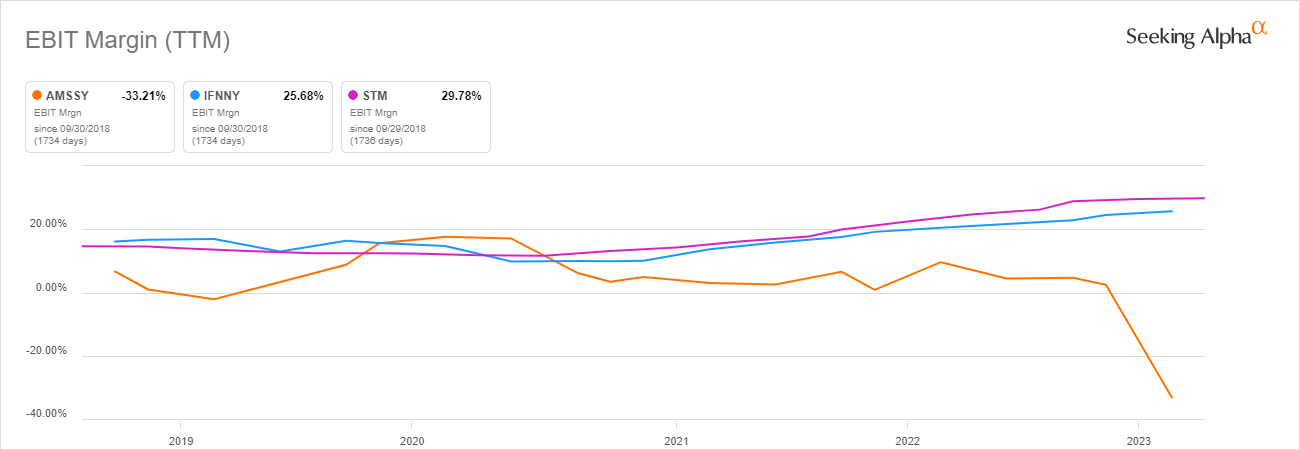

Both things should be doable, in my view. The 15% EBIT margin would bring ams-OSRAM not even up to where its peers are, for example, STMicroelectronics and Infineon ( OTCQX:IFNNY ). And ams, before the ill-advised takeover of Osram, had been there already.

ams-OSRAM EBIT margin vs. peers (Source: Seeking Alpha)

{kind=link}

It also looks like ams-OSRAM will benefit from Apple’s push into microLED displays . If this happens, it should take care of a large part of the revenue growth. On the flip side, ams-OSRAM is investing 1bn euros in its Malaysian LED production facility. So, if neither the cooperation with Apple nor something similar materializes, this will be a problem.

Another promising sign is that the German federal government and the State of Bavaria awarded ams-OSRAM a research and development subsidy of 300mn euros for its Regensburg location. The money will go towards research and development of innovative optoelectronic semiconductors and their production processes, for example, Lidar sensors for autonomous driving and UV-C LEDs for purifying air and disinfecting it with light.

Balance sheet

One thing investors will need to watch is debt. Even after disposals of non-core Osram assets of around 600mn since 2021, ams-OSRAM net debt at the end of June 2023 was still 2,034bn, giving the company a leverage of 2.9x net debt/adjusted EBITDA. I would consider this not good but acceptable. A slight concern is that two bonds with a combined volume of more than 1bn euros will expire in 2025. They were issued in 2020 for the Osram Licht takeover and although their coupons are quite high (6% for the EUR bond , and 7% for the USD bond ), they trade around 94%. Unless we see improvements by 2025, ams-OSRAM could face higher refinancing costs.(Note – the Austrian Erste Bank ( OTCPK:EBKDY ) publishes a regular Corporate Credit Monitor Austria , which can be very useful. You can find more information here. In general, their view is similar to mine: ams-OSRAM is financially solid, but there is a restructuring risk which could result in further increasing refinancing costs compared to peers.)

The company had cash and cash equivalents of 841mn, so the liquidity situation is solid. The write-down of 1.32bn and subsequent loss have reduced the shareholder equity to 1.25bn euros. The equity ratio (equity/total balance sheet) is now 17.7%, down from 32% at the end of 2022. The number certainly could be better. As a way of comparison, German peer Infineon, (which is significantly larger though than ams-OSRAM) reported a ratio of 51.75% in its last half-year report .

Risks

The biggest risk to the investment thesis is execution. Will the new CEO deliver? I am positive and have started building a position in ams-OSRAM. But success is far from assured, and there are also macroeconomic risks that can be an impediment to the execution of the new strategy, or prolong the timeline.

As we have seen, the company is very dependent on the semiconductor business in general, and with more than half of revenue coming from the Automotive segment, negative (or positive) developments in this segment will have a significant impact.

Another thing to watch is the micro-LED progress and especially any good or bad news regarding the cooperation with Apple.

My approach is to build up a sizeable position at the current low share price and then monitor closely. If there is bad news, I intend to exit even if it means a loss.

The next checkpoint will be end of October when ams-OSRAM announces Q3 2023 results.

Conclusion

ams-OSRAM has been a disappointment for investors since 2018. The misguided takeover of Osram Licht in 2020 has accelerated the downward trend and shares are now down more than 90% from their peak.

The new CEO and supervisory board have abandoned the plans for ams-OSRAM to become a large European player in the field of sensors and light technology. However, the execution of the now less ambitious goals could again create shareholder value.

The current lows could be the right time for entry – when things are still looking bad, but there is a sliver of light on the horizon. The investment is not without risk though and investors should be prepared to get out quickly if the company does not deliver again.

For further details see:

ams-OSRAM Is A Turnaround Candidate, Shares Could Double Or Even Multiply