AMSSY - ams-OSRAM: Plenty To Like About Austrian Quality Despite Underperformance

2023-05-31 10:15:33 ET

Summary

- I maintain a small position in ams-OSRAM due to its long-term potential, expecting a 150% return on investment within 2-3 years.

- Despite underperformance and a difficult market environment, ams-OSRAM is investing in growth, such as its industry-first 8" LED front-end facility in Malaysia.

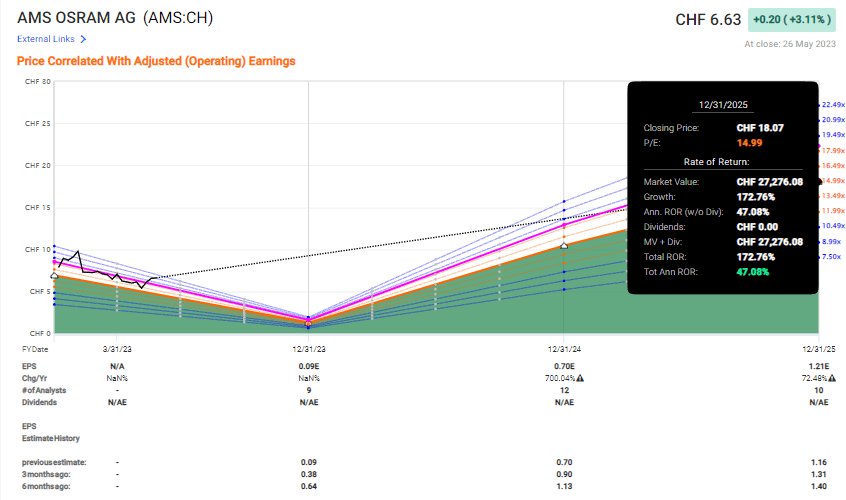

- I recommend a "BUY" rating for ams-OSRAM with a long-term price target of 15-18 CHF per share, but it may take until 2025 to reach these heights.

Dear readers/followers,

I'm relatively clear when I invest - my investments are based on theses that may take years to play out. It's relatively rare that I change my mind mid-way through and instead of adding more, start rotating or selling off what I believe to be a "diamond in the rough" or a seed waiting to bud into a flower, so to speak. Such is the case with ams-OSRAM ( AMSSY ). While the company continues to underperform, I remain convinced by the company's longer-term upside.

The company known as ams-OSRAM is one of the smallest positions that I maintain out of expecting it to revert to a massive upside. I believe that if you're early in a company, and you know your business, you can see the signs of a company really being in a position to deliver alpha - eventually. This is not a guarantee, and I've made mistakes here. That is why my position is small.

However, let me show you once again, using the latest-quarter results, why I'm still maintaining my position and considering adding more to this company.

ams-OSRAM AG - What we like about this company and its upside.

ams-OSRAM has certainly underperformed - and that's never a good thing. As some investments I've made will show you, it sometimes takes years to see those triple-digit RoR's. And that's what I expect from this business. This is the sort of company where I expect realistically an upside of over 150% based on an EPS expansion of several hundred percent in 2024 and beyond, compared to the levels of 2023.

Remember, this is a component of the well-known Voestalpine AG, which at one time decided to become a European Fab/Semi operator. This was several decades ago, and while the company has been seeing significant changes for the past 20 years, we haven't seen the business really take off just yet. The company has improved , that is for sure - but we've not yet seen the share price do the same.

This is despite the company's history being relatively impressive over the past 10 years.

AMS-Osram IR (AMS-Osram IR)

Building a quality fab/semi company takes time. And it's not as though the company is not profitable. If it wasn't consistently profitable, then I would not be investing in the business. The company's upside is there, going forward. This is further confirmed by the simple fact that ams-OSRAM has been able to outperform other peers in the semi Industry by factors and multiples of several X over the past seven years at the very least. It's just that the last few years, or the years since 2017-2018, have been volatile to put it very mildly. Since about that time, we've seen a massive decline in overall share price, currently putting us below 7 CHF per share. The company's native listing is on the Swiss stock market.

1Q23 is in, and that's what we look at to see what we have going for us, and why the company has underperformed.

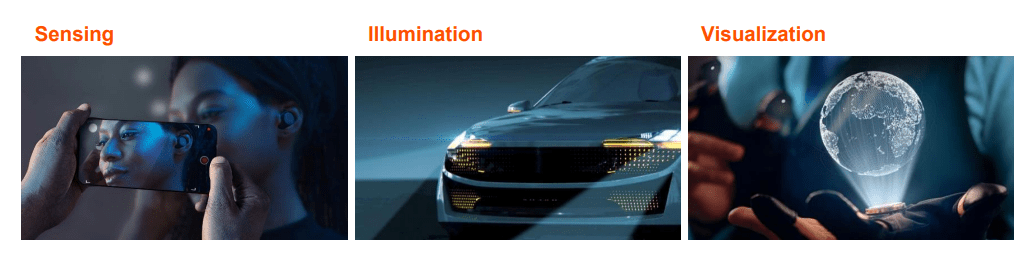

Osram is, as you might recall, a company in several key segments, with the clear goal of market leadership in optical solutions . This includes the fields of sensing, illumination, and visualization.

{kind=link}

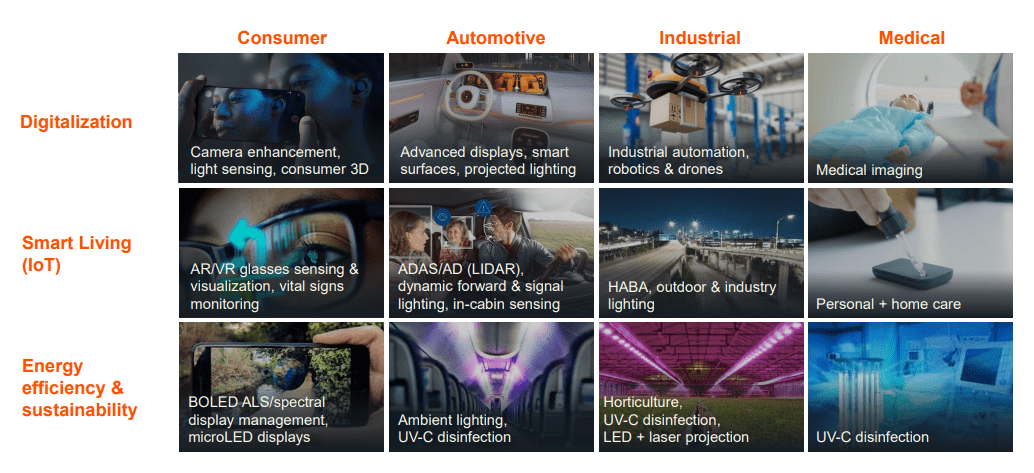

Specifically, the company seeks to dominate Emitters, optical components, various light, and image sensors and Emitter driver IC's, Sensor interfaces, and processors - and this includes algorithms. The company is relatively exposed to automotive, which explains some of its recent volatility. The 2022 mix was 41% automotive, 24% consumer, and 35% industrial/medical.

If you believe in the changing world with digitization, smart living, and energy efficiency, you should believe in OSRAM, because it works these segments and is a respectable leader, or among the leaders in many of those sub-segments.

{kind=link}

Automotive will continue to require qualitative emitters and components not only for exterior/interior lighting, but signaling, monitoring, automated driving, and gestures, but really it doesn't need to be automotive. Anything smartphone, wearable, AR/VR and other devices will require these components, or already require them today. The demand will not go away - only expand.

{kind=link}

The company did not have a great 1Q23. Whenever a company describes a quarter as " in line with guidance reflecting the difficult market environment and macro-economic trends", you know that is a way of saying that "we have negative results YoY/in some other way".

In OSRAM's case, it subdued market activity and demand situation across areas, which result in asset underutilization and negative profit. A vicious cycle that requires the situation to change before any improvement can be seen. The company reported a moderate sequential decline in automotive semis, which is a key segment for OSRAM - alongside a very muted consumer business overall, due to end-market weakness that has been ongoing for some time now. This was coupled with a lower infrastructure market , which in turn impacted LED Industrials, outdoor trends, horticulture lighting, and other trends which drove results further into the negative.

There were some light spots. Not many, but they exist. Some stabilization was there in other key industrial end markets. Other than, that the company managed its last communicated disposals according to plan, though calling this any sort of significant advantage might be a bit of a stretch. The company is merely doing what it set out to do. Any business or organization that cannot do this needs to be evaluated.

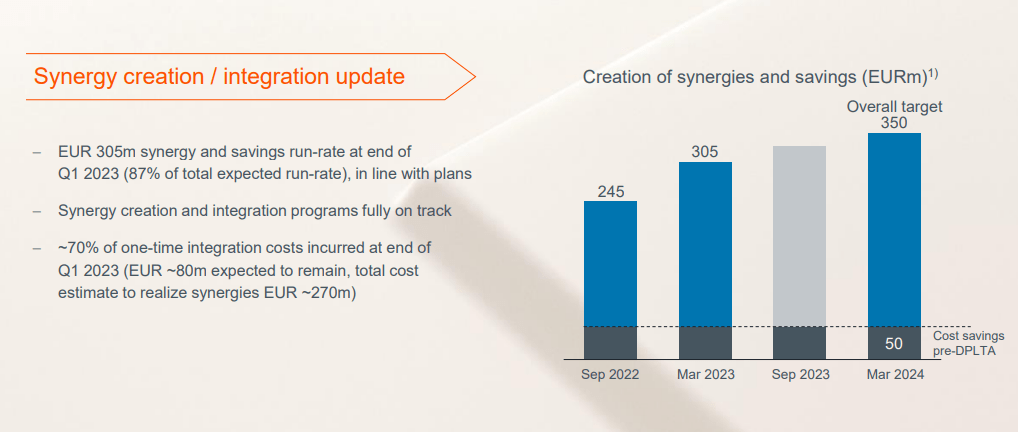

Furthermore, company synergies are somewhat on track, and perhaps most important, we're seeing a meaningful increase of CapEx driven towards investment in 8" LED front-end Fab.

This development brings the total disposal proceeds to €0.6B since 2021 and marks almost the end of the company here, with the company now able to call it a "successful completion of portfolio realignment". Savings targets are, in fact, intact for the time being.

{kind=link}

The company's defenders would say that ams-OSRAM is still really pushing capital into investment, including its industry-first 8" LED front-end facility, located in Malaysia. This has resulted in a significant increase in CapEx, now at 11% of total revenues for the company. This is starting to resemble a Telco, but this high percentage is giving results.

1Q23 saw the completion of the building, including the build-out of support infrastructure and planned equipment deliveries, to drive substantial CapEx - and the remaining construction is on schedule. The company expects 023 CapEx spending to end slightly below €1B. This means that we're unlikely to see significant profitability improvements in 2023 because it's expected to be peak CapEx.

That means that we're still in a very good position, if we have that sort of patience, to buy ams-OSRAM at a very cheap price. The company is unable due to combined industry pressure and negative trends coupled with peak CapEx, to deliver anything close to impressive or representative long-term results. By that, I mean representative of the longer-term potential of the company, which is significantly higher than what we see here.

Net results were still positive, though just barely. 1Q23 results came in at 0.02 CHF per share, compared to 0.39 CHF/share YoY, showcasing just how extreme things currently are. However, I believe there is light at the end of the tunnel - and for 2024E to be the year when the company will start to turn things around. We'll be past peak CapEx and set for some of these investments to start paying off.

This coupled with market reversal and normalization, will see ams-OSRAM bring about better results.

And this leads me to the following valuation assumption.

ams-OSRAM - continues to show value but in the very long term

Investing in this sort of company is never easy. It's based on a significant reversal, which might not come this year. Many expected the reversal to come this year and were disappointed when it did not. That is why we have analyst price target trends where analysts used to have a 20 CHF PT at this time last year, only for this year to see the PT drop to an average of 8 CHF, with a low of 5.1 CHF, compared to 13.8 CHF last year.

Does that mean that the company is worth only roughly a third of it was a year ago?

No, of course, I do not believe that. I believe the market is making the classic mistake of mistaking a growth and investment stage for a permanent downturn. I view ams-OSRAM as a long-term significant potential, despite only 4 out of 13 analysts being at a "BUY" rating here.

Investing in this company will take time, but in case of normalization in accordance with its growth and reversal estimates, will see you reach a RoR of 150%+ within less than 3 years. And that is based on a 15x P/E, not the company's historical average of over 20x P/E.

{kind=link}

The company isn't really in any worrying sort of debt situation, despite a group leverage of 2.5x to adjusted EBITDA, because it holds a very well-laddered maturity structure, and over €1B of undrawn credit, including however, a higher-interest €800M revolver. Still, 95%+ of debt is fixed.

For guidance, I tend to agree with the company. The company is expecting no more than 3-6% OM on revenue of less than a billion. This reflects ongoing subdued demand, seasonals, and underutilization of assets as well as deconsolidation. However, there is an expectation of a slowly improving situation in 2H23, which should allow for the beginning of a ramp-up in 2024, catalyzing in 2025 in the return you see above.

A risky prospect, to be sure. That is why my position in the company is relatively small. However, the company is fundamentally safe, as I see it, and its position in the value chain and supply chain in its fields gives it a good potential going forward. And sometimes, that is enough for me to invest in - if the implied payout is enough.

This is one of the riskier plays I currently engage in, and if you're an income investor/retiree, I would not suggest that this investment is suitable for you. If you have cash and are willing to wait 2-3 years for a payout of over 150% in the semi sector, then this is an investment you could make, though I'd make it one of a basket of attractive potentials.

That's how I'd play this one, at least.

Here's my continued thesis for the company.

Thesis

- ams-OSRAM is a market-leading play on key sectors and MLED trends that will play significant roles in the next 5-20 years of the semi, electronics, and IT development. I view the company as being well-positioned for longer-term growth and outperformance, but not a short-term one.

- The key is to buy this company significantly below normalized discount multiples, and that is currently possible with the shares below 7 CHF.

- I view the company as a "BUY" with a long-term PT of 15-18 CHF per share, but it needs to be noted that it will take a long time for the company to reach these heights. At least, I believe it will take until 2025E, at this time I'm writing this article.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company does not fulfill my dividend criteria, but every other criterion I have. This makes it a "BUY" to me at this time, but one that requires you to understand what you're getting into.

For further details see:

ams-OSRAM: Plenty To Like About Austrian Quality Despite Underperformance