AMSSY - ams-OSRAM: The Pain Continues But There Is Light In 2025-2027

2023-09-18 17:57:00 ET

Summary

- ams-OSRAM is a company with poor fundamentals but potential profitability in the future.

- The company is focusing on sensors and interfaces, which are in a significant sector.

- The valuation of ams-OSRAM is currently low, making it a potential investment opportunity for long-term growth - but with a high risk that needs to be looked at.

Dear readers/followers,

ams-OSRAM ( AMSSY ) has been a fairly terrible investment so far - thankfully not as large as it could have been. This company is an Austrian player in sensors for microelectronics, low power, sensitivity, and multi-sensor applications. On a business-idea sort of level, this company is a superb player with a good upside - but the valuation and share price trends would imply disagreement here. This is an update to my previous article/coverage, posted here on SA .

Why?

We'll look at the continued issues with the company and see if we can identify any new issues that make this company one to avoid going forward. But overall, I would say that my original thesis from December of last year is still relevant here, and that's the thesis I'll be revisiting for the company.

ams-OSRAM - Fundamentals look terrible, but profitability seems clear

So, ams-OSRAM actually looks fairly terrible from a purely fundamental level. If we look at the company from a purely business model sort of perspective, it probably shouldn't be high on anyone's list at all.

ams-OSRAM business (GuruFocus)

{kind=link}

his particular one arose out of the fairly well-known steel company Voestalpine AG when the company decided to diversify operations into fabs and semi-operations.

The first partner for the company was American Microsystems Inc., with whom the company cooperated. The resulting fab was chosen to be the top fab in 1992, and it was the first semi-company to go public back in 1993, with an IPO on the Vienna stock exchange. Since that particular partner, the company has been through a long multitude of mergers, and structural shifts, and doing the equivalent for a company of "finding itself". This is not a profitable sort of thing, usually, because it involves significant transformation and related costs - no different for ams-OSRAM. But there are two sides to this story.

On a factual revenue basis, the company since GFC has seen significant growth .

ams-OSRAM IR (ams-OSRAM IR)

This is of course not the same as profit - but I would argue the company is slowly finding where it "wants" to go. The company has in fact outperformed most peers in this metric, by several multiples.

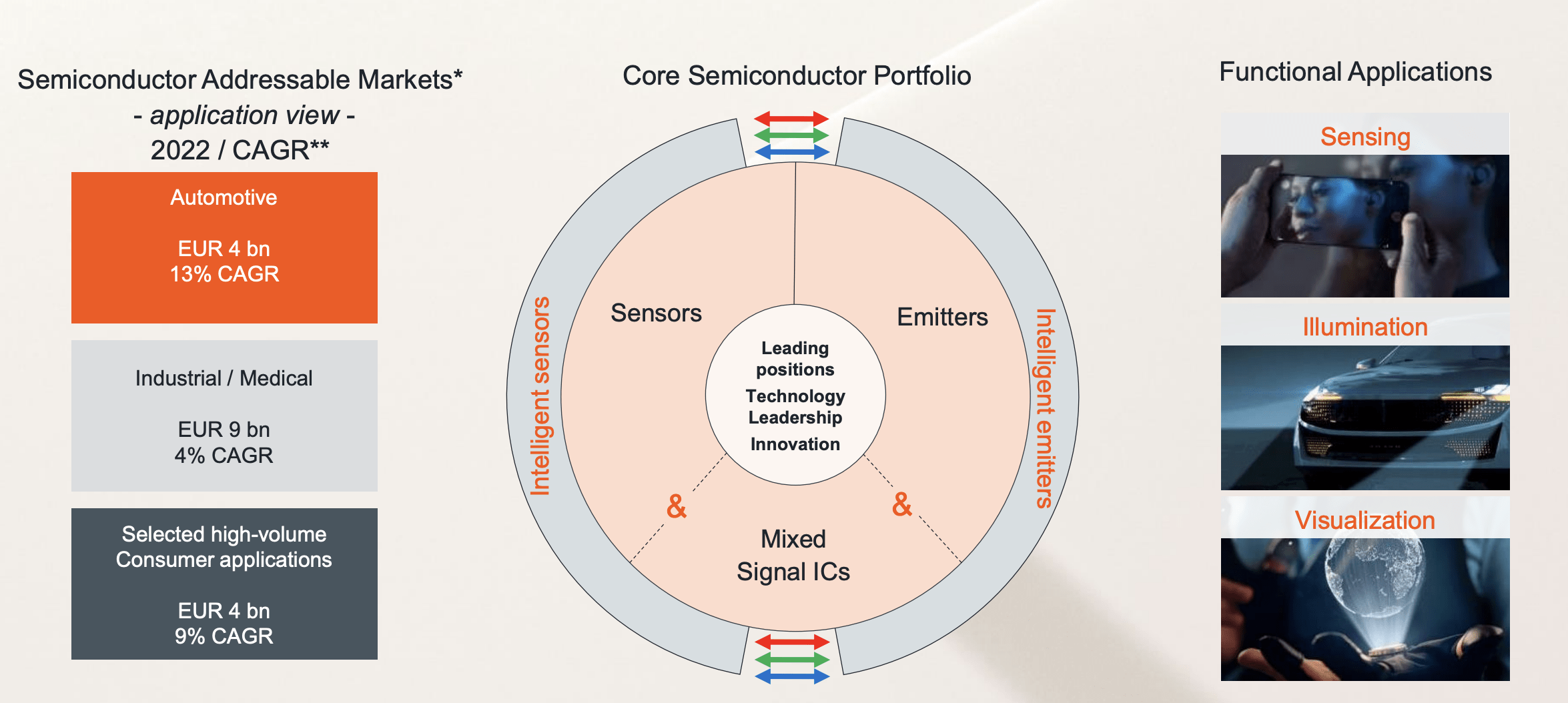

Its current focus, and what's arisen out of over a decade of trying to find its way, is a focus on sensors and interfaces based on analog and mixed-signal semi-design. This is primarily sensors, illumination, and visualization. If you know anything about anything in the industrial and the modern world, you'll realize that this is a significant sector. Osram's expertise is a good thing here. These products are used in consumer and specialized solutions across multiple sectors.

ams-OSRAM IR (ams-OSRAM IR)

My questions with regard to this company have always centered around profitability and fundamentals, both current and on a forward-looking basis. Because if we can confidently state that the company is going there, then the investment thesis writes itself. We have a European market leader in a highly important sector - that's an investment for me, provided that the company is cheap.

However, the problem remains that the company keeps updating and adjusting its business model. Its latest iteration keeps talking about a focus on profitability and monetizing the innovation that it has. The company's current argument is laying the foundation for double-digit revenue growth with a 15% adjusted EBIT margin by the fiscal year of 2026E.

How?

By focusing on:

- Semi-portfolio with a target of intelligent sensors and emitters

- Exit Non-core semi-businesses

- Pursue consumer markets where the company can differentiate, while continuing to push capex into microLED.

- At the same time, adjust the current semi-portfolio and structure to this new business model, with streamlining down from 3 to 2 units and heightened responsibility, with €150M worth of savings by 2025E.

The problem with these ambitions is, that the company should have done this years ago. Many of these ambitions beg the question "Haven't you been doing this already?".

I don't want to be too fundamentally negative on the business. Because the company's targeted sectors are attractive , and the potential in both the sectors and in Osram products, are confirmed.

{kind=link}

What's also confirmed are the secular megatrends that are likely to drive continued growth for the company. I'm talking digitalization, I'm talking smart living and efficiency in energy - all of those trends are likely to see innovation-based investing and sourcing across consumer, automotive, industrial, and medical sectors.

But when a company spends much of its material focusing on where specific sectors are going, instead of where its own results in those sectors are going , you know you're on thin ice and you know what you want to focus on.

ams-OSRAM has advantages. It's a near market leader or market leader in 3 segments. I'm talking about things like LED, where it's #2 with a 13% market share. I'm talking Light Sensors, where it's at a 25% market share behind only STMicroelectronics ( STM ) - the problem comparing obviously being, that STM is a very profitable business. It's also the market leader in traditional auto lamps/bulbs, where it has its own market model. (Source: ams-OSRAM IR).

Automotive is the major contributor to OSRAM. 51% of the current mix is automotive, which means that this is what the company is trying to change going forward and improve the mix.

But, I have never seen material so filled with macro expectations and focus on markets rather than their own results. And the reason is very clear for this. ams-OSRAM is not currently generating anything close to acceptable results, and there also isn't any clear indication for a 1-year upswing in the foundational trends, that would improve company results. These are the company's own words (Source: ams-OSRAM IR).

Why?

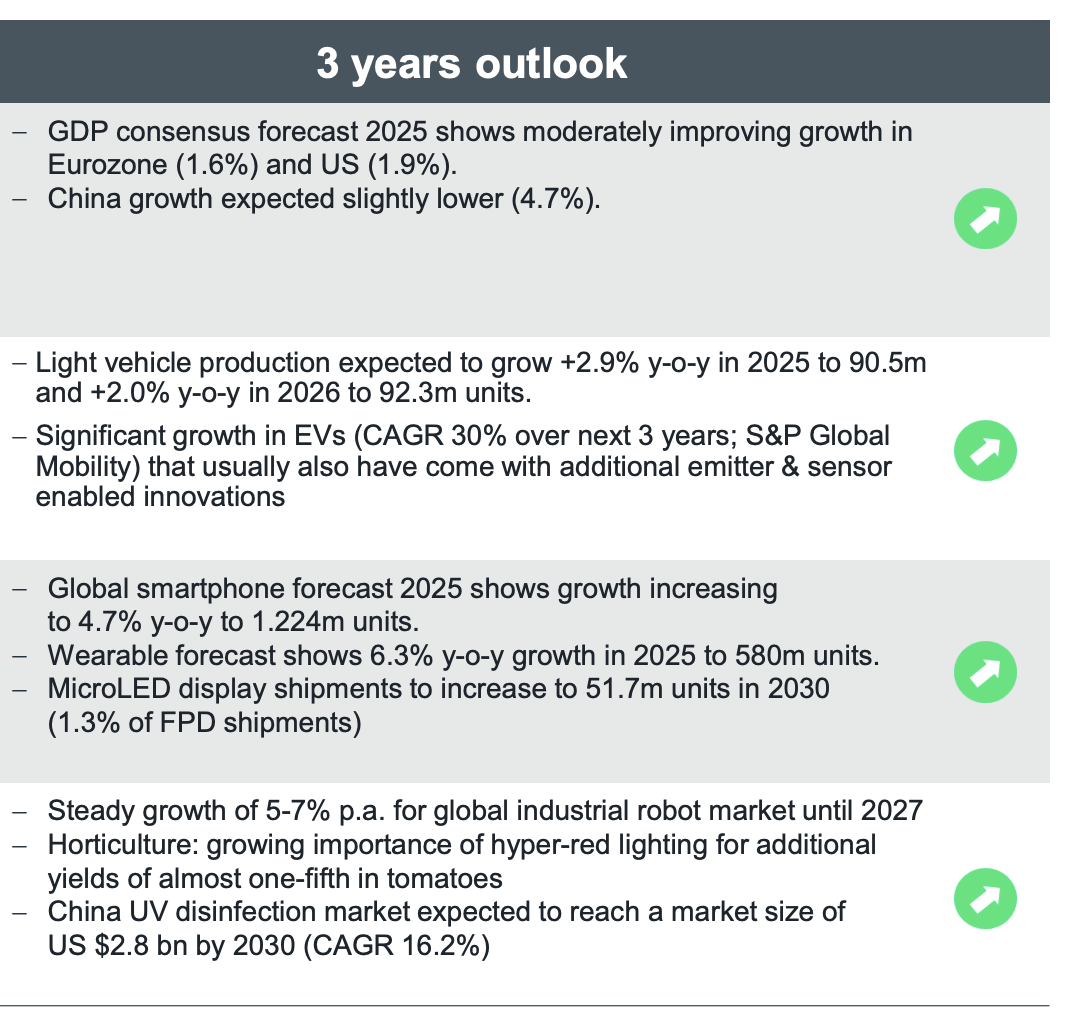

A combination of macro factors, including inflation, weak GDPs, semi-forecasts, negative global smartphone forecasts, wearable forecasts, and industrial forecasts are all either showing negative or flat trends. Automotive is the only thing that's up, and that only partially.

However, the company believes that in 3 years, by 2026E, things will look different.

{kind=link}

A fair characterization of what the company is currently doing is therefore essentially preparing for the future , where the company expects both revenue growth and a double-digit EBIT margin.

Do not misunderstand me. ams-OSRAM is generating sales - quite a bit of them: over €850M for 2Q23, with an adjusted EBIT margin of 5.9%. That means the company is actually profitable here. The business also expanded margins, but the short-term guidance is not a positive one - and FY2024E also brings with it potential for decline, but focus on improving profitability.

{kind=link}

The current performance is and seems likely to continue to be lackluster. This includes the fact that ams-OSRAM lowered its official guidance, but has continued to lag even that lowered guidance. Much of the company's potential is forward-facing. We're talking about things like the microLED opportunity - but smartphone sectors are likely to remain under pressure. I am personally a firm believer in both social media and smartphone fatigue, and I'm noticing trends where people are disconnecting from social media, and lapsing longer between smartphone cycles than before, representing anecdotal proof, if nothing else. I personally have no hurry whatsoever to replace my phone - and probably won't until it no longer works or the battery lasts less than 18 hours. I have social media, but I do not use it and haven't for several years at this point - but who knows, I may be an exception.

Automotive is likely to remain in a position where it can give the company profit - but the real gamechanger I see for the company is when we go into what could happen in the next 4-20 years, with many of the technologies the company actively pursues going into more of an interesting position.

Let's see what the valuation says about the company here.

ams-OSRAM valuation - what there is to like about it here.

I do own shares in the company - but only at a small stake so far. I mean to size up my position, and my current rating is "BUY". I don't intend to change my PT here, but as with every investment, it needs to be put into context for your personal investment goals, as well as what other alternatives are available on the market today.

And there, ams-OSRAM does not measure up all that well.

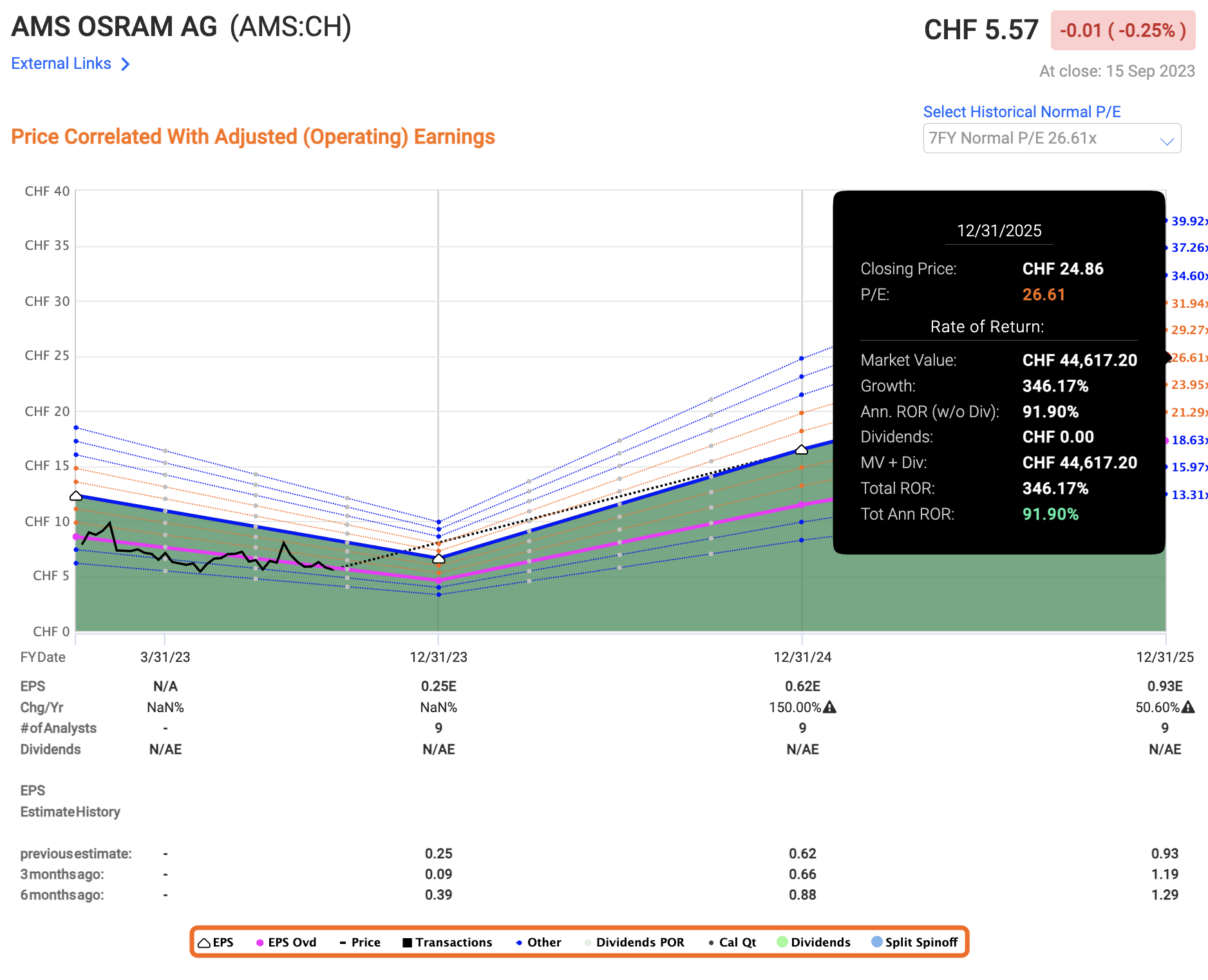

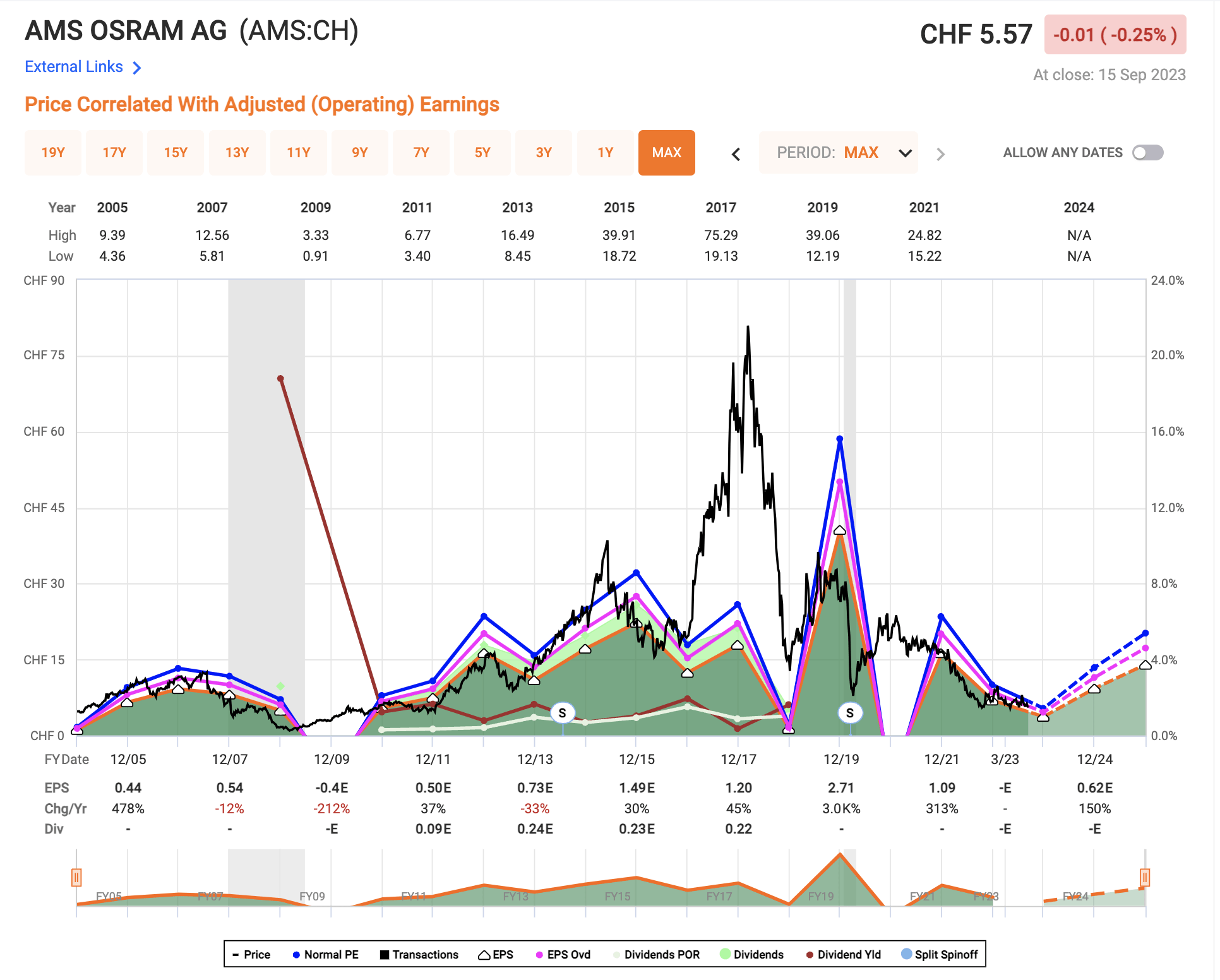

The company trades natively under the AMS symbol - and if you do look up the current estimates, your RoR is 350% based on 2025E 26x P/E based on the 5-year normalized premium.

ams-OSRAM upside (F.A.S.T graphs)

{kind=link}

Great, right?

No, not really. It's not quite that simple. The company is BB-rated (that's BB-), has no yield, and has an absolutely abysmal forecast accuracy with more than 50% misses even with a 10-20% margin of error. Some of the recent misses are as much as 100%+ (Source: FactSet).

My stance is that the company will eventually turn around. When it does, I believe the current share price is one we'll look back on and wish we could have again. But the lack of visibility of when is what's difficult here, and what makes this an investment only for the most risk-tolerant and long-term of investors out there.

The current estimates essentially include not just reversal in basic segments such as smartphone and automotive, but also movement in microLED.

Based on how poorly the company's historical trends have actually looked, I would be extremely careful about paying too much heed to forecasts here.

ams-OSRAM earnings trends (F.A.S.T Graphs)

{kind=link}

Investment is, as I see it, only possible if you have a 5-20 year timeframe, and you're certain you don't need the capital. This company does have a very impressive history across all of its segments. But most of that is legacy - and this isn't necessarily indicative for the future/on a forward basis.

I would estimate ams-OSRAM at a very low forward P/E, still expecting an upside. The long-term value may indeed be well above 15 CHF per share , but it will take time. For now, I say 7 CHF per share or below, and to not add too much and to make sure the investment meets your criteria.

Still, by staying invested in a company like this when it's possible we see an upside as the one the company expects, that is how fortunes can be made. Many of my articles are on growing fortunes you already have. This is a company that based on what can happen, can actually make you rich. A 4-7x is possible here. And that is worth illumining and focusing on, even if at the same time I caution you what also could happen, and how poor returns your capital could generate.

I own a stake, and it's small - for my portfolio - but it may be large for yours. I do not add new shares at this time, but I may going forward. Here is my current thesis for ams-OSRAM.

Thesis

- ams-OSRAM is a market-leading play on key sectors and MLED trends that will play significant roles in the next 5-20 years of semi, electronics, and IT development. I view the company as being well-positioned for longer-term growth and outperformance, but not a short-term one.

- The key is to buy this company significantly below normalized discount multiples, and that is currently possible with shares below 7 CHF.

- I view the company as a "BUY" with a long-term PT of 15-18 CHF per share, but it needs to be noted that it will take a long time for the company to reach these heights.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

For further details see:

ams-OSRAM: The Pain Continues, But There Is Light In 2025-2027