AMDUF - Amundi: High-Quality European Asset Management For Your Portfolio

Summary

- One of my ambitions for 2023 is to expand my EU coverage, in particular in France and the PIGS regions. Some of the companies found here meet my investment criteria.

- Amundi S.A. is one of those companies. This business is the merged asset management arms of the storied banks' Credit Agricole and Societe Generale.

- Amundi is a tricky proposition given its small history and the alternatives available on the market. But I believe the thesis I'm about to present you with is fair.

Dear readers/followers,

One of my ambitions for the year of 2023 is to increase your exposure - in reading, not necessarily in terms of investing (unless you choose to go this way) to European stocks, in particular not only Scandinavian or German (which is much of my coverage), but also French and the so-called PIGS countries.

One of the things I noticed in 2022 when revisiting how my articles and my investments performed, was that I had not given you enough "pushes" to look at these companies. And these companies, French ones included, are some of the best 2022 performers out there - and a part of the reason for my own outperformance. I will always try to be as transparent as possible, so because of this, I'm going to increase my coverage here. I also note that there, if I do not do this, is a dearth of coverage on these companies on SA. While this may not necessarily be a problem as such, it limits how potentially profitable you could be.

So - here we go.

Say "Hello" to Amundi ( OTCPK:AMDUF ), the largest asset manager in all of Europe.

Amundi - Asset manager with over $2T in Assets

So, I'm not going to pretend that my position in Amundi is massive. Unfortunately, it isn't. I know Amundi because a friend of mine had a wife who worked for the company, and I've spent some time researching it. When it dipped below €45 for the native stock, I pushed some money to work. And by some money, I mean less than $1,500, a watchlist position for my portfolio.

However, after recent outperformance, I'm doing a full-spectrum coverage on Amundi and adding it to my list of covered businesses. It deserves it.

Why?

{kind=link}

Amundi is the leading European asset manager. With its AUM, it's one of the 10 leading asset managers in the world. The company doesn't have that much of a history, being less than 15 years old in its current iteration. It contains the legacy assets of Crédit Agricole (Crédit Agricole Asset Management, CAAM) and Société Générale (Société Générale Asset Management, SGAM). It listed on Euronext in 2015, which gives it a traceable public history of around 7 years.

It's also still majority-owned by Credit Agricole.

What the company does is basically most things having to do with investment and asset management. It offers mutual funds both in equity and bonds as well as diversified management, structured products, and treasury management, as well as passive management. Amundi is an ETF issuer and an index fund manager, and also pushes real/alternative asset investment potentials, such as PE and real estate.

The company's target customers are retail and institutional investors. In its home country of France, Amundi is more widely known for its activities in the field of French employee savings schemes (épargne salariale). Amundi also has a well-respect R&D unit, which provides investing publications on global economic macro, as well as stock market developments.

The company isn't just France of course, but the company has offices in Asia and the US as well. It has around 100 million direct or indirect clients, and around 1,000 institutional customers.

{kind=link}

Amundi is A+ rated by Fitch , and it has a very solid dividend, generating more than 5-6% yield on an annual, current basis. The company has been growing organically as well as inorganically. The company acquired Pioneer investments, the asset management arm of Italian UniCredit for €3.5B, financed by debt issuance and a cap raise. This transaction added a quarter of a trillion euros to the company's AUM, and enabled Italian, German and Austrian expansion. The company also M&A'ed Sabadell - a relatively small Spanish player with around €22B under management, as well as Lyxor from SocGen for €825M, adding over €140B of assets, which also came with high expertise in ETF management and passive management.

So, the company has no issues growing - and it's been growing for years, adding business to what it already has. As with any management company like this, the company's core business and income are made up of asset management fees of various kinds - subscription fees, annual management fees, and other ancillary types of income and fees.

Like most asset management businesses, Amundi had a very good 2021. The tech froth of that year was simply "made" for fee-based businesses, with the insane amount of capital inflows we saw - and reverse again in 2022. Because of this, I tend to exclude these as non-recurring. Amundi saw a 19% EPS decline for the 2022E basis, but still respectably higher than in 2020. 3Q22 mostly confirms this trend for the ongoing fiscal, which we'll see closed fairly soon.

{kind=link}

Now, the company's relatively impressive trends in terms of cost flows come in spite of the market conditions, which for asset managers are extremely unfavorable compared to 2021. Interest rates that have been rising, the index evolution for the past 12 months, it's all pushing the company's trends downward - or as i like to consider it, more towards normalization.

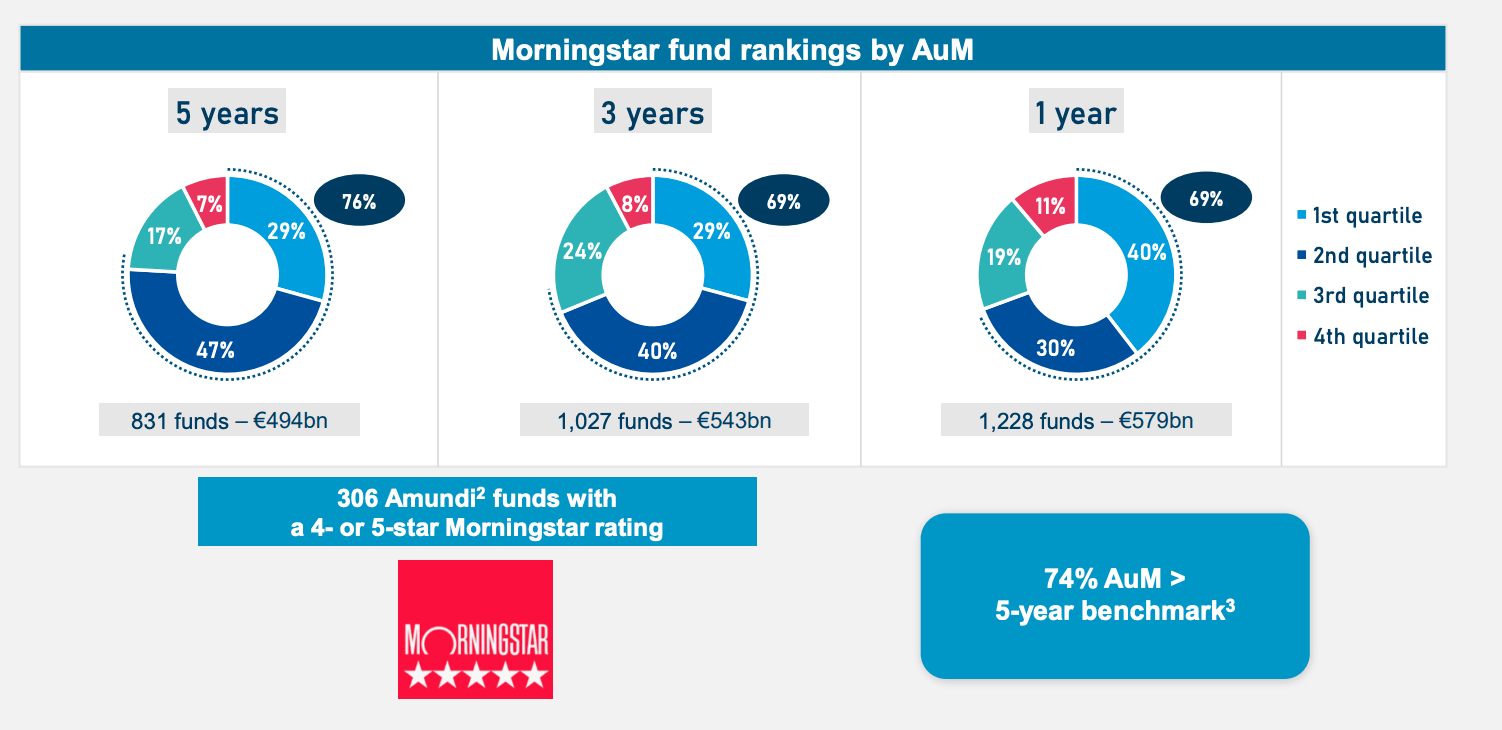

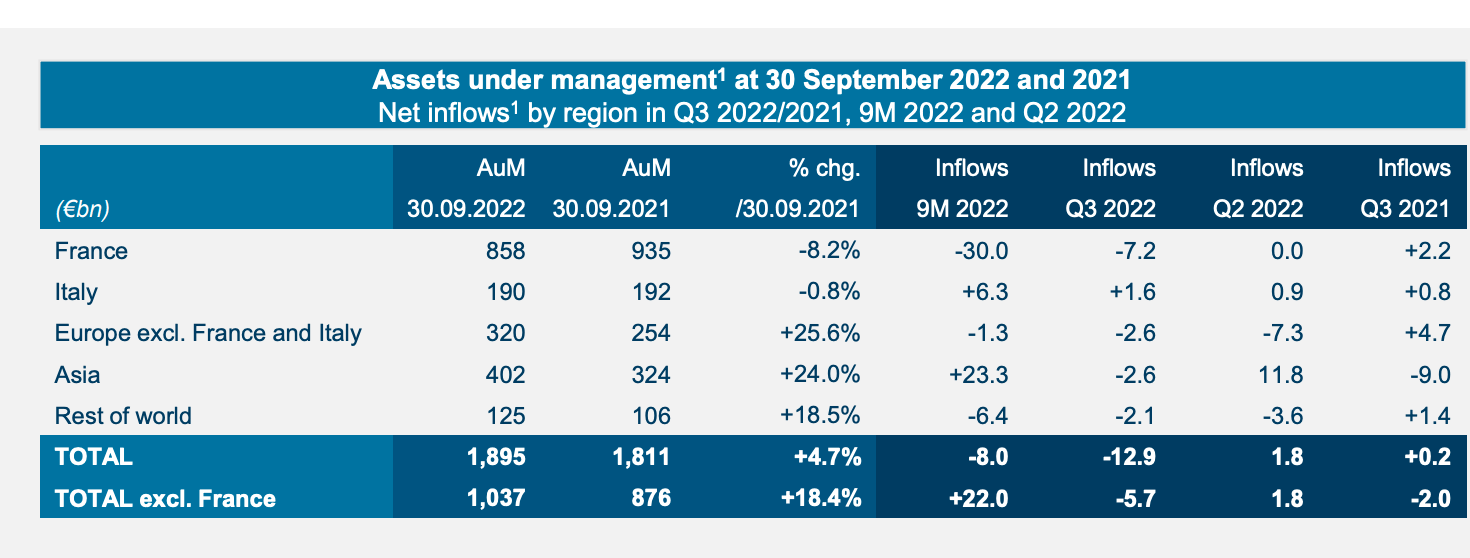

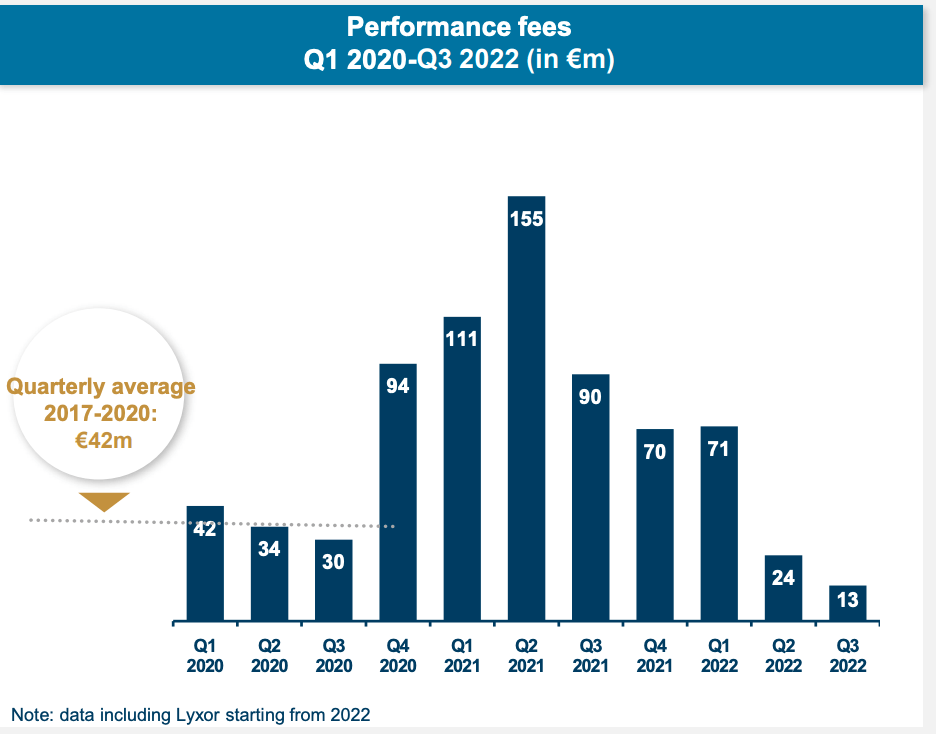

The company is currently seeing a decent amount of outflows, but an overall impressive resilience, considering the market we're in. The company's management fees continue to be solid. Net revenues are up 1.9% despite the strong comparative period. Performance fees though, are naturally in line with the market.

{kind=link}

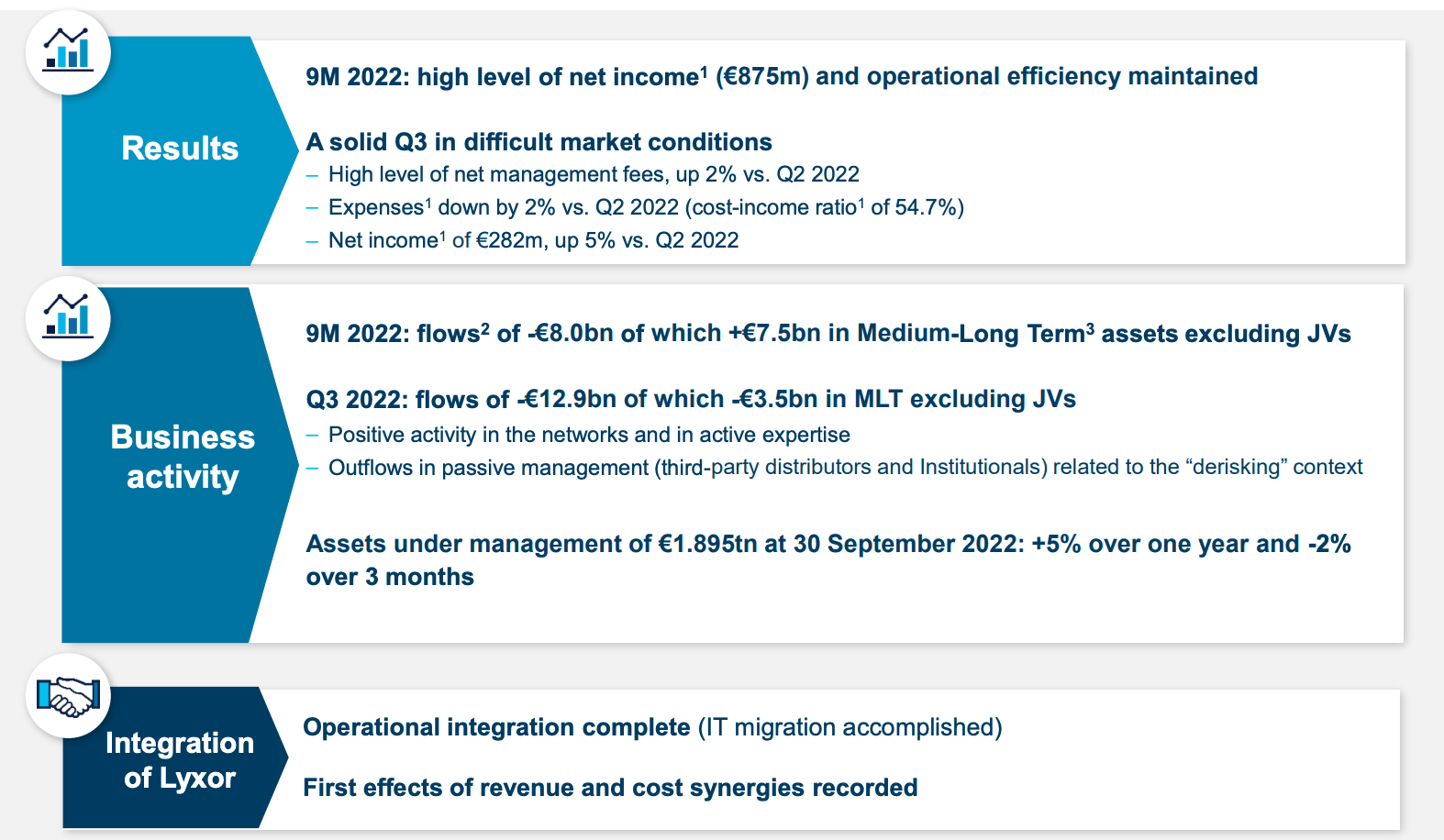

What I'm looking at when I currently check asset management businesses, is how the company is handling the changed nature of expense management, or rather, the expenses themselves. Amundi is impressive here, reporting a 1.7% like-for-like expense decline due to synergies from Lyxor, and significant expense control - and all of this is in spite of a negative FX from the dollar and Euro. On a sequential basis, the company's net income is up 4.7<% thanks to good cost control - on a YoY basis, due to performance fees on net income, the company's results are obviously down on a net basis.

A good summary of this business's current quarter and recent results is that the company is doing well despite high-level challenges and impacts. The company also managed to fully integrate Lyxor, and are seeing the results of this integration.

The risks and advantages of asset managers are fairly general no matter which one of the companies you're looking at. What is true for one of the top 10's is true for Amundi as well. Any massive EPS growth rate is not something you're going to find here, because asset manager earnings, especially in today's world with a relatively competitive asset management sector already. Essentially, the development of these companies usually reflects the underlying development of the market. In a relatively flat market, these companies perform fairly well and tend toward a 9-12x P/E - in better markets somewhat better.

What are things like today then?

Amundi's Valuation - not massively attractive, not terrible either

So, the right time to buy any asset manager is when there is a significant discount to its overall assets, to its peers, and to the historical valuation overall. We did have that time not terribly long ago when Amundi was trading at around 6-7x P/E - a great discount for a qualitative, A+ rated asset manager such as this. That's for the ADF by the way - the native and the peers for the native trade at closer to 9-15x. Peers for the company come in the form of Schwab ( SCHW ), BlackRock ( BLK ), State Street ( STT ), Franklin Resources ( BEN ), Nomura, and others.

We don't really have a discount in terms of P/E here though. While we're back to relatively normalized levels even without the massive boost we saw in EPS during 2021.

The range for the peers here goes from around 10x for companies like State Street, up to over 20x for Blackrock - so there's a fairly wide spread here, dependant on individual quality, the AUM, and the position in the market. In investments, we either have an upside based on earnings and dividend growth going forward, or we have an upside based on reversion, which we can see from either historical averages, or from peer averages. Preferably , we want a combination of these qualities. We had that back around 3-4 months ago, but we now have an upside that's strictly based on earnings and dividend growth.

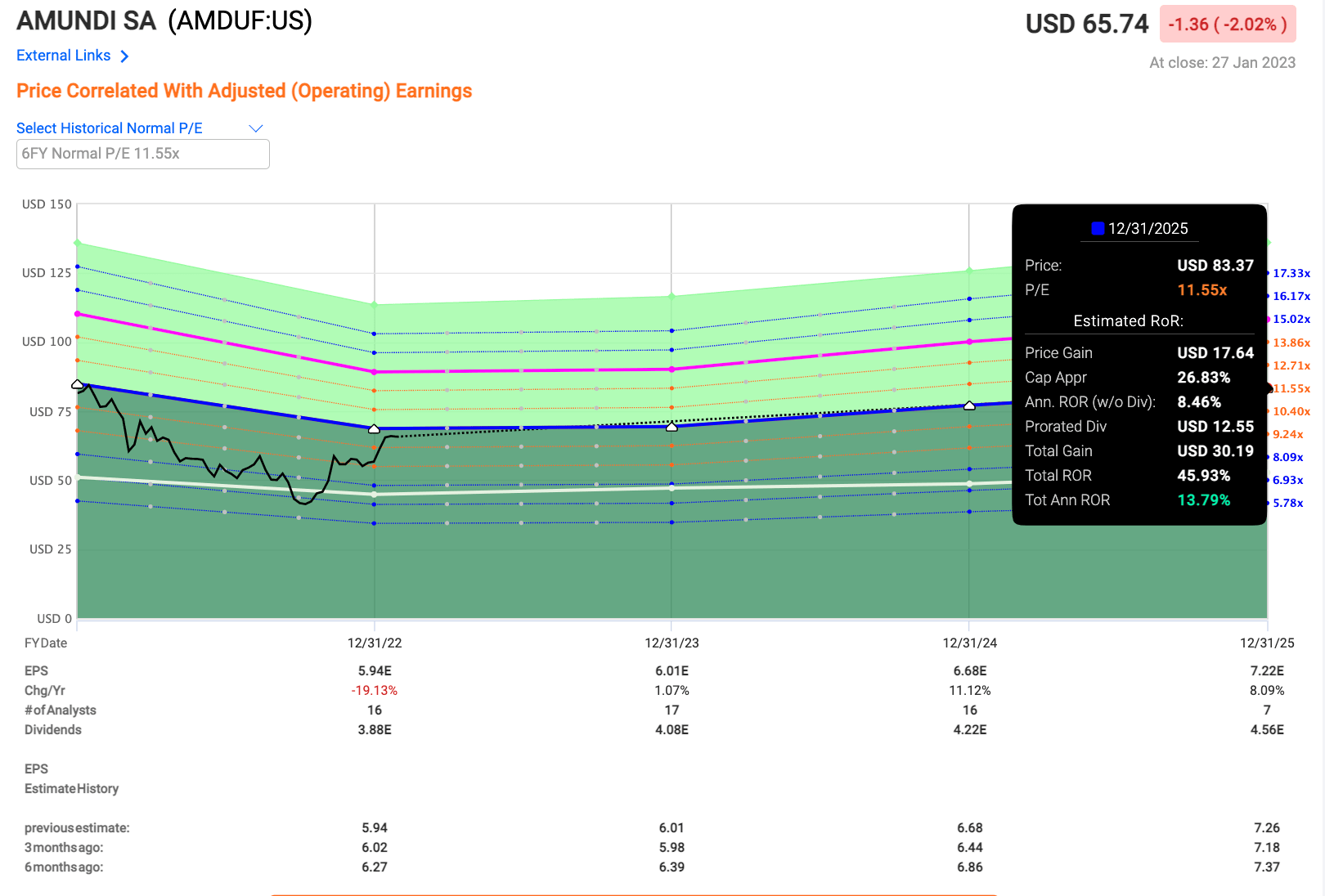

The company is currently trading at around 10-11x P/E normalized, which is close to its historical average of 11x. The expected forecasted average growth in the next 3-4 years is around 5-6% aper year for EPS and 5-9% for the dividend. A decent growth rate, but based on today's estimates, and based on an 11-12x P/E, which is really the highest you'd want to put Amundi at, would result in an RoR of around 13.8% annually - and that's as high as I would go here.

{kind=link}

Peer averages don't give us much help to consider this company higher either. For the native, we have 16 S&P Global analysts following the company. These give the company an average of €66 per share, which would suggest an upside of 10% here. I don't have much against this target, except that it's perhaps a bit optimistic - I would go a few euros lower to make sure that we're being conservative. There is a degree of volatility to this stock. The analyst range is from €59 to €78. I would tend toward the lower end of that range.

Now, the company has advantages. The yield is almost double that of a company like Blackrock or Schwab. This could suggest that the risk is significantly higher, which I consider being wrong in this case. Among its peers, it's also one of the best-rated asset managers in existence. I've invested in many of these peers, and I do own shares in Blackrock at the time of writing here.

However, we have little data on Amundi's forecast accuracy - only that analysts are perhaps a bit too exuberant about the targets, as they tend to be. For those reasons, I won't allow even a high, covered yield or a credit rating to influence me here.

So - my target for the company is €62/share. This comes to 11x P/E for the 2025E target period, representing a decent but not too exuberant growth. Anything above that will be a positive surprise - but you shouldn't be expecting it, because we're as uncertain about where the market is going from here as we are about the company's overall performance.

So, here is my thesis for this French asset manager.

Thesis

- Amundi is a French, world-class asset manager with over €2T in AUM, A+ rated with a yield of over 6% at a good valuation. The company, like any qualitative asset manager, is a play on overall market development and should be bought at a significant undervaluation.

- A valuation would consider to be relevant for the company here in order to increase my position is below €62/share. However, this must also be put into context with other investment opportunities available on the market today.

- I start coverage on Amundi with a "BUY", albeit one with a very limited overall upside.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company really can't be considered cheap here, but I still give the company a "BUY" with a small upside.

For further details see:

Amundi: High-Quality European Asset Management For Your Portfolio