AMDUF - Amundi: Scope Of Partnerships Impacting AUM

2023-06-09 08:21:58 ET

Summary

- UniCredit is reportedly reducing Amundi funds. Analysts suggest that UniCredit's relationship is deteriorating, making a renewal of their agreement difficult.

- We provided a comps analysis with Allianz, and we prefer the German insurance company (higher profits, lower valuation, and GEO diversification).

- At a similar P/E estimate, we decided to start Amundi coverage with a neutral rating.

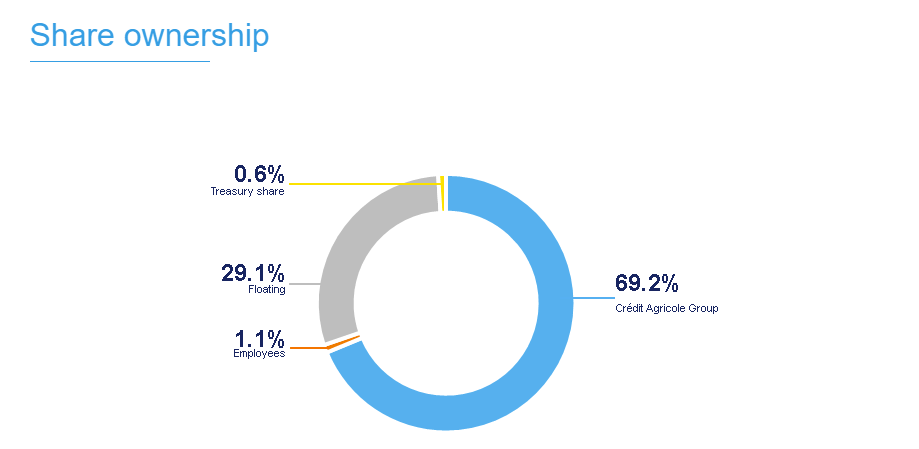

Here at the Lab, today we decided to provide a comprehensive deep-dive into Amundi (AMDUF) with a comps analysis with the PIMCO/Allianz division. We have a good overview of the asset management field and it is important to report that Amundi's main shareholder is Crédit Agricole Group with an equity stake of 69.2% (Fig 1). As a reminder, we have a long-standing buy rating on the French bank, and our latest publication was emblematically titled: " Dividend Yield At 10% Means It's A Buy ".

{kind=link}

Fig 1

Amundi SA is an asset management France-based company that offers its services to B2B and B2C thanks to a wide range of products in order to assist its clientele in their investment decision. Its services offering involves all asset classes (fixed income, equities, private markets, and structure products) and the company is currently active in the EU (with a key market share in its home market), but also in APAC and the Americas.

Before providing a comps analysis, Amundi was all over the news for the potential UniCredit reduction in funds. In detail, UniCredit ( buy-rated by our team ) is linked to a commercial agreement with Amundi. In 2016, Crédit Agricole bought Pioneer for €3.54 billion and the two groups signed a ten-year alliance on AUM distribution products in Italy, Germany, and Austria. The alliance will expire in 2027. However, according to Reuters , the Italian bank is starting to reduce Amundi funds to its total assets under management. The agreement signed would provide that Amundi's funds represent a pre-established share of the bank's total AUM. Although the quota has been set at around 80%, Unicredit would have started to reduce Amundi's products below this threshold by agreeing to pay small penalties. In particular, UniCredit launched a strategy to reconstitute its own asset management division with Azimut (AZIHF) (AZIHY). UniCredit's CEO is also working with other partners such as Fidelity, BlackRock, and JPM to offer clients more personalized funds. Here at the Lab, we see three potential scenarios:

- We believe that Amundi will try to renegotiate its partnership well in advance of the 2027 deadline to avoid a divorce and change the overall terms and scope of the partnership (this is our base case scenario);

- The second option is that UniCredit will identify a new industrial operator and this is negative for Amundi because the new partner could be Azimut. If this happens, as a worst-case scenario, in the short-term horizon, we see a limited impact given the fact that the contract will expire in 4 years. We believe that UniCredit could retrieve around €100 billion of AUM, but not before 2030 at the earliest losing at max €60 million in net profit;

- More ambitious is the third hypothesis in which UniCredit could reach an agreement with Amundi to transfer its former Pioneer assets (around €150 billion) in an ad hoc vehicle of which the bank would acquire control. UniCredit has the highest capital ratios in the European banking system, but we believe that will prefer shareholders' remuneration over dilutive M&A. If this happens, as a best-case scenario, Amundi Italian AUM assets could benefit from an M&A premium (as a reminder, in 2026, this deal was valued at €3.5 billion which represents Amundi's 35% of its current market cap).

{kind=link}

Fig 2

Here at the Lab, we are pricing the first scenario; and even if we subtract UniCredit €150 billion fund (which is unrealistic in the medium-term horizon), Amundi would lose approximately 7.7% of its entire AUM and might represent a minus €85/90 million in net profit loss.

{kind=link}

Fig 3

Q1 results and our comps analysis

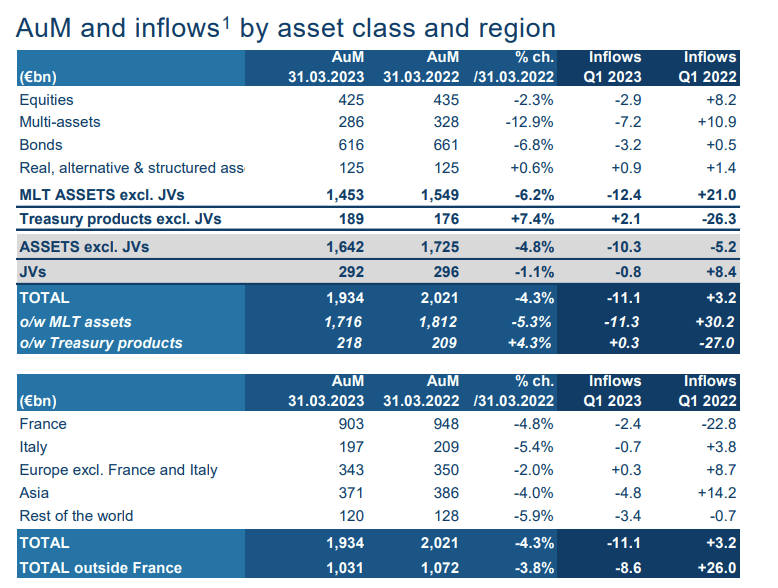

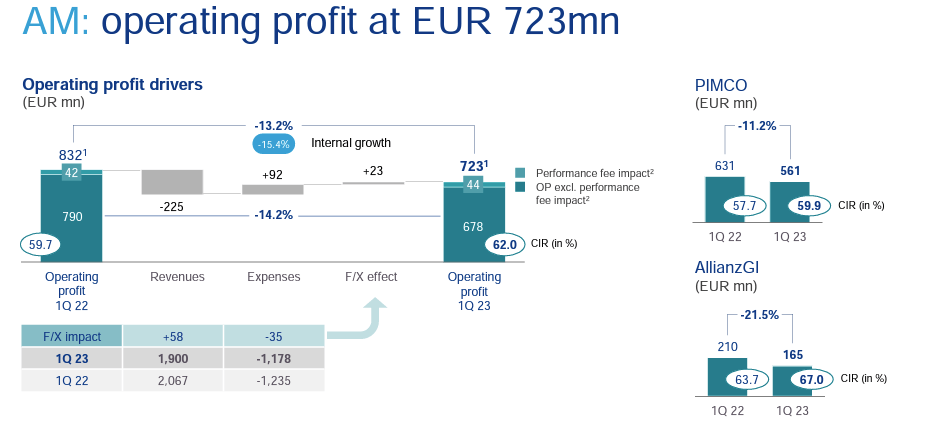

Looking at the recent Q1 results, Amundi's net profit reached €300 million with a cost/income ratio of 53.6%. Total net inflows amounted to minus €11.1 billion. Assets under management decreased by -4.3% in one year, but increased by +1.6% compared to 2022-end, reaching €1.93 trillion. The strong performance of the retail business was more than offset by outflows from MLT assets in very low-margin segments, as well as outflows in China, where the asset management sector still experiences net redemptions in MLT assets. Looking at Allianz ([[ALIZF]], [[ALIZY]]) versus Amundi, we highlight the following:

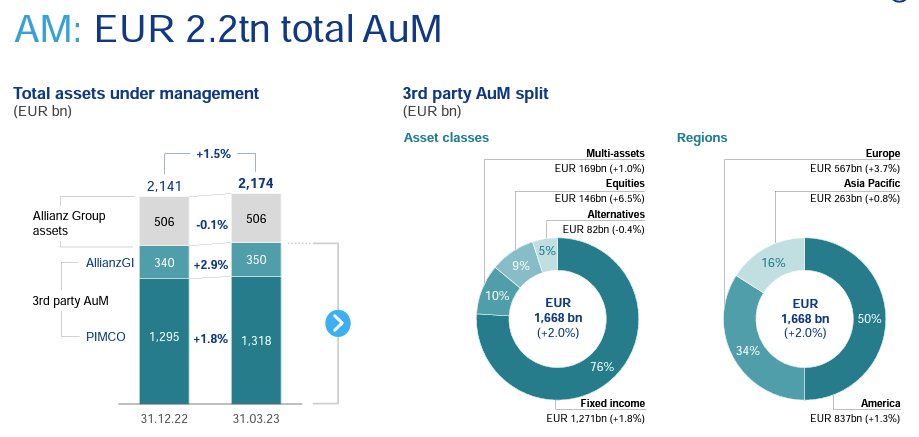

- AuM: Allianz has assets for €2.2tn including also third-party AUM (Fig 5) versus Amundi at €1.93 trillion (Fig 3);

- Cost/Income ratio: Allianz is at 61.2% versus Amundi at 53.6% (Fig 4);

- On a GEO level, Allianz AUM flow is more diversified than Amundi where the EU accounts for 74% of its assets. Allianz GEO split is America €837 billion (50%), Asia Pacific €263 billion (16%), and Europe €567 billion (34%);

- AuM operating profit: €723 million for Allianz while Amundi (with a similar AuM) is at €390 million (Fig 3 vs Fig 6).

{kind=link}

Fig 4

{kind=link}

Fig 5

{kind=link}

Fig 6

Conclusion and valuation

Amundi is currently trading at an 8.84x P/E while Allianz is at 8.75x. The German company is also benefitting from secular growth trends in the combined ratio evolution as well as on higher reinvestment yield. Even though Amundi has better cost discipline, Allianz scored better in GEO diversification, AUM flow, and abs profit. We suggest to our readers check our previous publication called: " Allianz - Solid 2023 Start " . Regarding Amundi, the valuation seems fair and we decided to remain neutral with a 12-month target price of €55 per share. Our target price is also based on a DCF valuation, using a 12.5% WACC and 1% long-term growth rate assumptions. At €55 per share, Amundi would trade at a 10x 2024E Price Earning multiple and we believe is at a premium valuation not only with Allianz but also with Legal & General , which also offers a better dividend yield (>8% vs 7.5%). Downside risks include partnerships renegotiation (UniCredit is a threat), dependency on bank networks, AUM flows, higher competition, and regulatory risk complexity.

For further details see:

Amundi: Scope Of Partnerships Impacting AUM