AMDUF - Amundi: The 2024 Outlook And My 'Hold' Rating

2024-01-11 14:20:03 ET

Summary

- Amundi, one of the largest asset managers in Europe, has not performed as well as the market, but still has value for conservative investors.

- The company reported positive inflows and impressive profitability in Q3 2023, with a focus on passive investing and expansion in Asia.

- The primary risks to Amundi include the captive distribution model and competition from index and fund investing, but the company also has upside potential with its strong client base and consolidation in Europe.

Dear readers/followers,

You may recall that I started covering and investing in a slew of new French and other European companies back in early 2023. One of those companies that I started to cover was Amundi ( AMDUF ) at the time, and still one of the largest asset managers in all of the European sphere.

I'll say straight away that Amundi hasn't done as well as the market. My position is up around 13%, and that was only due to the grace of investing at an undervaluation, specifically October/November of last year and only in small amounts - but overall, my thesis that Amundi is a great business that does deserve a fair bit of your attention is still a thesis I stand behind here.

In this article, I'll update the thesis for the coming year, and I'll look at what we can expect from Amundi going forward into 2024, once the company reports 4Q, and once the company decides on the coming dividend.

Amundi remains a tricky proposition given its small history and the alternatives available on the market - but I still believe it has value to the conservative investor, and I don't believe the valuation to be as prohibitive as some may consider here.

So, this particular piece is an update to the last article, which you can find here.

Revisiting Amundi and what upside the company has for 2024

As I said in my very first article on Amundi - which I wrote in early 2023 - I do and have had a position in the company for a while, just not a big one, unfortunately. It's a watchlist position, initially €1,500 that has gone to about three times that. A respectable amount of capital for many, but in the context of my own investments, not so much.

I wish, given how the company has performed, that I could claim larger exposure here, to what is Europe's leading asset management business. Because even as we look at it in the 3Q23 period , Amundi remains one of the ten largest asset managers on the entire planet.

Essentially, Amundi is the legacy asset management assets of Credit Agricole and SocGen, two of France's largest banks. It was IPO'ed in 2015, which now means it's looking at its 9th year of being in business.

Also, the company still has a majority stakeholding by Credit Agricole ( CRARY ), which is never a negative thing, given how high quality that particular bank is - also a bank I own shares in, as it happens.

I went "HOLD" in my last article in April, and did not provide a new update when the company dipped - but if you followed my price target and thesis for the company, you would have noticed that the implied upside there was enough to warrant a "BUY" rating change.

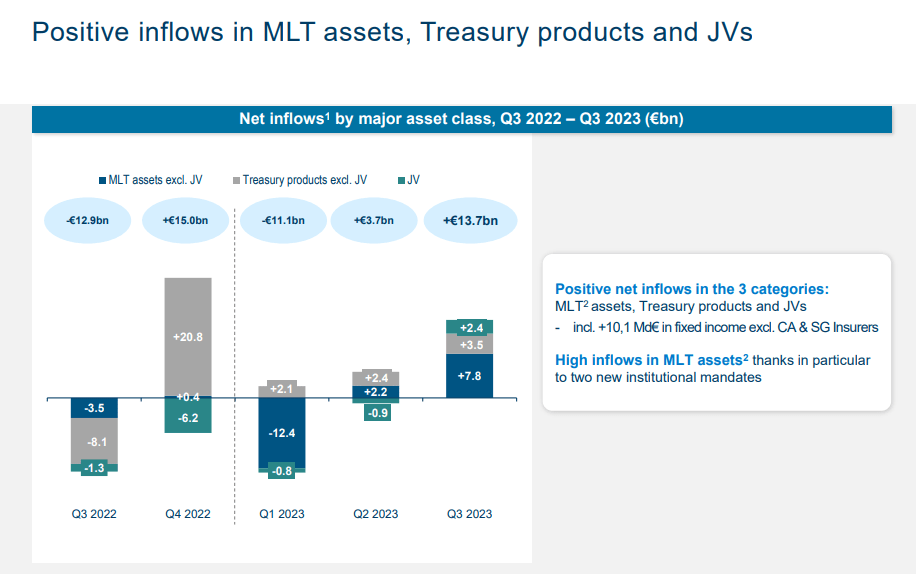

We have 3Q23 results, and those were good. The ~€2T AUM asset manager managed a €14B positive inflows in retail, institutional, and JV's, with another €6B inflows in active management of fixed income, coming to a YoY 4% AUM growth which is impressive, given the backdrop of high-risk aversion we had going for us during that particular time.

Amundi also managed a very high and impressive overall profitability during this time, generating €290M worth of quarterly net income, which again is an upward trajectory thanks to an excellent diversification in top-line sales and good operational efficiency.

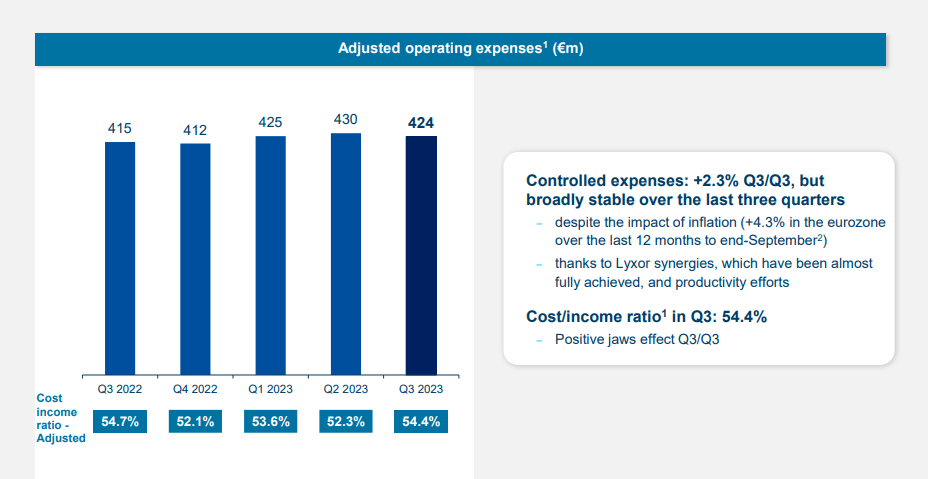

The primary measure of that efficiency is the C/I or the cost/income ratio. Amundi is at 54.4% which isn't market-leading, but quite excellent for this company. The company's priorities continue to be passive investing like indexes and ETFs, and inflows there were up, with solid inflow in China and Asia as well.

Amundi markets itself, in conjunction with its December 2023 meeting, as a "Fixed Income Powerhouse".

The European asset management markets were characterized mostly by risk aversion during the middle and end of last year. Treasury products were responsible for much of the modest inflows, with continued outflow from active management and similar products, as investors grow more and more averse to risk and as the interest rates push passive products higher.

{kind=link}

The company is also seeing significant expansion successes in Asia, with Amundi now being the #1st place asset manager in all of India, a country unlike large parts of the remainder of the world seeing a GDP growth expectation at 6% for 2024, compared to 1.2% for the G20 nations. Amundi has a strong part with the first-place bank in India, with 22,000 branches and 480M clients with a 23% market share in retail banking. This makes Amundi the go-to partner for Indian asset management as well, and as an Amundi shareholder, you'd do well to remember, and keep an eye on this.

While there is a general instability in the market as a result of macro conditions, Amundi retains an impressive level of overall revenues. The levels of outflows and performance for the quarter also means that Amundi saw a tailwind of low levels of performance fees for the quarter, and manages good cost control, despite an overall inflationary environment that we're actually currently in.

{kind=link}

This also resulted in impressive levels of net income - down slightly, but still with an overall characteristic stable level of net income despite ongoing market fluctuation. That's generally what we want to see - asset managers that manage good net income from shareholders even when the market goes down.

To date, as of 3Q, the company has seen over €900M of net income, and will likely generate upwards of €1.2B on the annum, thanks to the ongoing stability of the management fee margin. A slight improvement to C/I is also good here, but I'd still like to see Amundi getting below that 52% C/I (though it's unlikely to happen, as Asset management companies have different reward structures that are more cost-intensive than your typical retail bank.

However, the overall outlook for Amundi remains a positive one, as I see it. Thanks to company diversification, I expect Amundi can adapt well to a myriad of market conditions and institutional mandates and the stability, year-in and year-out of the company's income is something I look very closely at here, and with a great deal of positivity toward.

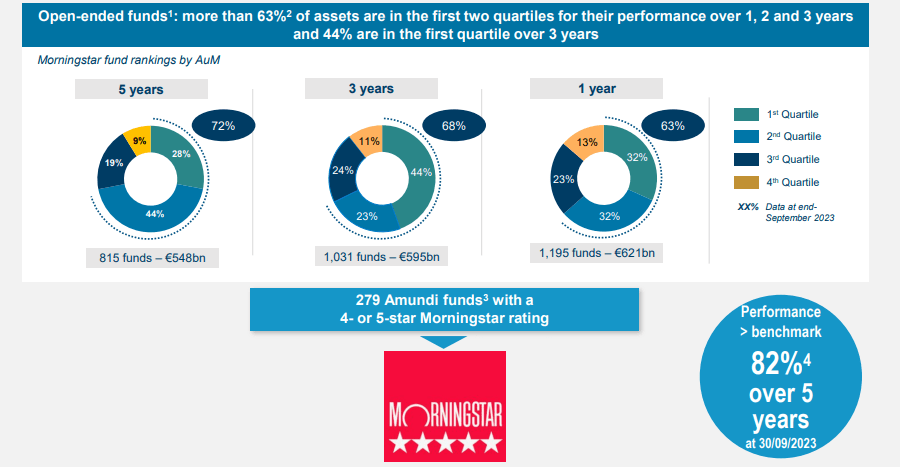

Morningstar, meanwhile, has a lot of positive things to say about Amundi's funds.

{kind=link}

Here are the risks and upsides to Amundi as a business, and as an investment.

Risks & Upsides to Amundi

The primary risks to Amundi, aside from the global macro environment and what effects this can contribute to an asset manager, is the entire company model. What is known in industry vernacular as the captive distribution model is likely to come under ever-increasing pressure not only from regulators but from investors as well as they're trying to get the "bang for their buck". This will eventually, as I see it, dilute most non-scalable asset managers back to niche or boutique positions, and it might not hold up in the longer term in terms of performance. And if this is the case, and Amundi starts performing sub-par it's only a question of time until the share price and valuation starts doing the same.

It's no secret, after all, that the entire business model of the asset manager has taken a massive hit from the rise of global index and fund investing - this is unlikely to change. But this risk also isn't unique to Amundi, it goes for all asset managers.

However, that same model also leads to the upside for Amundi - meaning that the company has plenty of so-called sticky clients with very good margins and income visibility, for as long as they continue. Also, Amundi using its deep knowledge and network of bank branches, has the advantage of having easy access to customers and a massive share in retail investments in France and other geographies - upwards of 40% in France alone.

The company also isn't in any danger of being outscored - Amundi is the leading consolidator of asset managers in Europe, and will likely lead this charge, not suffer from it.

Those are the primary ups and downsides that I see.

Amundi - The valuation

Amundi's valuation is now again tricky. The best thing to do is to buy the company when it's below €50/share - though this is rare. In my earlier article, I made a case for the company not being a "BUY" unless it traded at €57/share or below. I'm sticking to this target here, despite seeing Amundi as a qualitative business.

There simply are many other great businesses out there that do not cost you this much - even with the quality and fundamentals that Amundi does offer you.

The upside at this valuation, given a growth estimate of 4-5%, is very limited. If the company keeps its 11-12x P/E ratio, then you can expect to annualize perhaps 10-12%, inclusive of that impressive 6.5% dividend that currently remains well-covered.

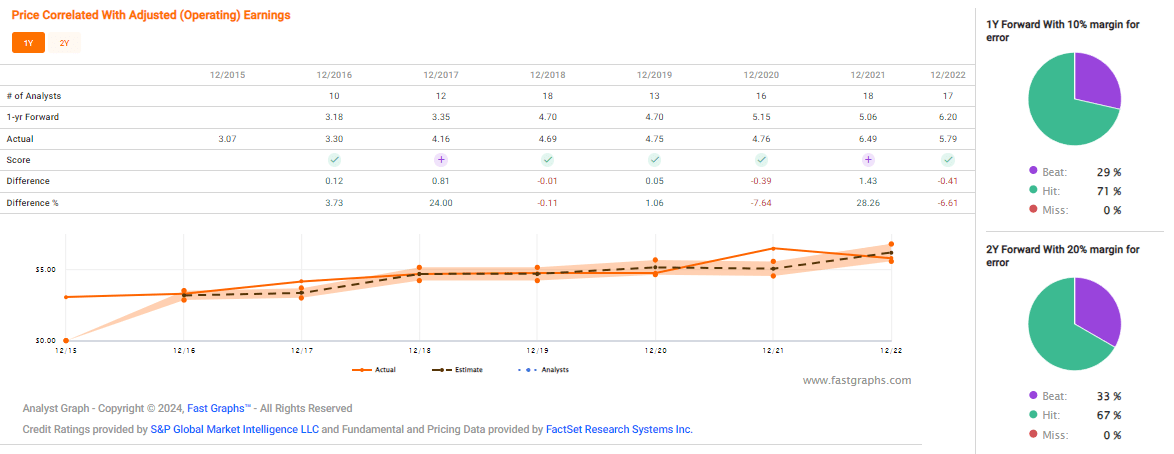

The problem is, that there are dozens of financial companies available with good yields and far better upsides to this, and you do not need to invest in Amundi to get it, even if the company's forecast accuracy ratios and historicals are nothing short of absolutely stellar.

{kind=link}

Those numbers you see there, coupled with the operational and income stability, coupled in turn with the dividend of almost 7% is why Amundi is a far better investment at the right price than you may actually believe. Also why, if the company drops below €55-€57, I will be there to scoop up shares.

And I believe any conservative investor with an eye for valuation could be there to look at the company at that time as well.

So while I am a "HOLD" as things currently stand, with the company over €60/share - I'm clear about my targets if those fundamentals turn, and I'll be happy to add more when that happens.

Here is my current thesis for Amundi.

Thesis

- Amundi is a French, world-class asset manager with over €1.9T in AUM, A+ rated with a yield of over 6.7% at a good valuation. The company, like any qualitative asset manager, is a play on overall market development and should be bought at a significant undervaluation.

- A valuation that would consider being relevant for the company here in order to increase my position is below €57/share. However, this must also be put into context with other investment opportunities available on the market today - and that is why I am keeping my target to that €57, from over €60/share previously.

- I start my 2024E coverage on Amundi with a "HOLD," and the price target you see at €57/share.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Now, I'm only at 3 out of 5 targets, which means I'm at a "HOLD" at this time.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Amundi: The 2024 Outlook And My 'Hold' Rating