AMWL - Amwell Looks To 2024 For Stabilization But Operating Losses Remain High

2023-11-08 11:46:16 ET

Summary

- American Well Corporation recently reported its Q3 2023 financial results, with a continued poor showing.

- The firm provides a telemedicine platform to healthcare system participants.

- Revenue continues to drop and operating losses remain extremely high, so my outlook on American Well Corporation is Bearish [Sell].

A Quick Take On American Well

American Well Corporation ( AMWL , " Amwell") reported its Q3 2023 financial results on November 1, 2023, missing revenue and consensus earnings estimates.

The firm provides a telehealth system for healthcare system participants in the U.S. and overseas.

I previously wrote about Amwell with a Sell outlook on reduced forward revenue guidance.

The company must reignite revenue growth while substantially reducing operating losses while serving an industry that is under significant cost pressures.

My outlook on AMWL remains Bearish [Sell] until we see a return to revenue growth and sharply reduced operating losses.

American Well Overview And Market

Massachusetts-based Amwell has developed the Amwell Platform, a telehealth system that enables healthcare service providers to deliver their services remotely.

The firm is led by Chairman and Co-CEO Ido Schoenberg, MD and President and Co-CEO Roy Schoenberg, MD, MPH.

Ido was previously co-founder of iMDSoft, and Roy was previously the founder of CareKey, an electronic health management software vendor.

Amwell has clients among health systems, health insurance plans, employers and retailers.

The firm’s primary offerings include:

-

Telehealth

-

Telestroke

-

Telepsychiatry

-

On-demand consultations

-

Scheduled consultations

-

Pre-packaged care modules & programs

-

EHR Integration

-

"Converge" with third-party and device integration support.

Amwell embeds its telehealth capabilities within large entity workflows and seeks new business via its direct sales and marketing efforts.

According to a 2023 market research report by MarketsAndMarkets, the global market for telehealth software and services was $87.8 billion in 2022 and is forecasted to reach $285.7 billion by 2027.

This represents a strong CAGR of 26.6% from 2022 to 2027.

The primary reasons for this expected growth are a sharp increase in the care and monitoring of chronically ill and elderly patients and improved telehealth monitoring devices and connectivity.

Healthcare providers continue to increase the number of specialty services they offer via remote means as they aim to improve care quality while increasing productivity and reducing costs.

The chart below shows the historical and projected growth rates in telehealth usage by global region:

MarketsAndMarkets

Major competitive or other industry participants include:

-

Doctor On Demand

-

Teladoc Health

-

MDLive

-

Philips

-

Medtronic

-

GE Healthcare

-

Cerner

-

Siemens Healthineers

-

GlobalMed

-

Chiron Health.

Amwell’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to decline in recent quarters; Operating income by quarter (red line) has flattened more recently but remains heavily negative:

Seeking Alpha

Gross profit margin by quarter (green line) has trended lower in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have moved materially higher:

Seeking Alpha

Earnings per share (Diluted) have remained heavily negative, as the chart shows here:

Seeking Alpha

(All data in the above charts is GAAP.)

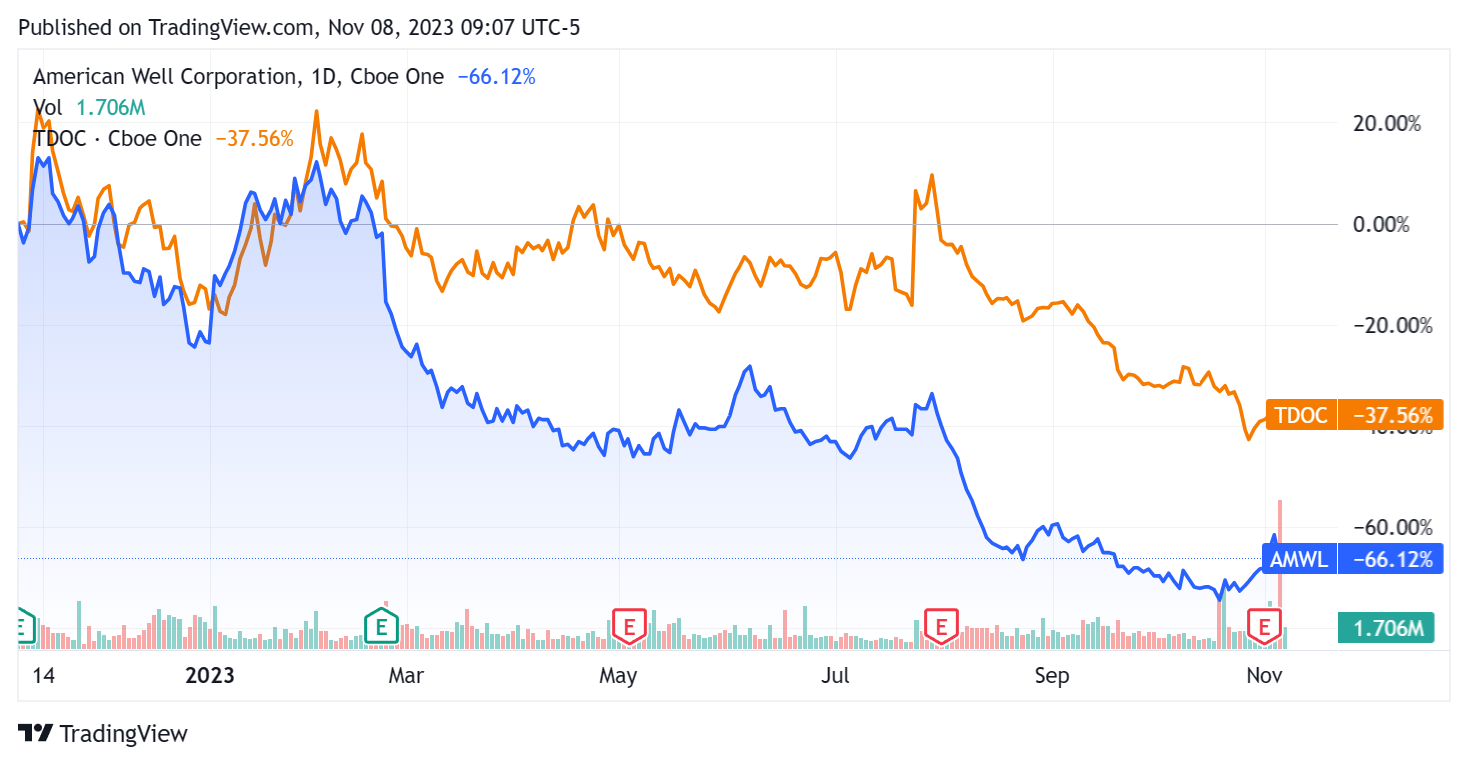

In the past 12 months, AMWL’s stock price has fallen 66.12% vs. that of Teladoc’s ( TDOC ) fall of 37.56%:

{kind=link}

For balance sheet results, the firm ended the quarter with $418.1 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash used was a whopping ($143.1 million), during which capital expenditures were $0.4 million. The company paid $84.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Amwell

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| NM |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.3 |

| Revenue Growth Rate |

| -1.2% |

| Net Income Margin |

| -257.0% |

| EBITDA % |

| -83.3% |

| Market Capitalization |

| $350,830,000 |

| Enterprise Value |

| -$37,340,000 |

| Operating Cash Flow |

| -$142,710,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.45 |

| Forward EPS Estimate |

| -$0.77 |

| Free Cash Flow Per Share |

| -$0.59 |

| SA Quant Score |

| Strong Sell - 1.30 |

(Source - Seeking Alpha.)

As a reference, a relevant partial public comparable would be Teladoc:

| Metric (Trailing Twelve Months) |

| Teladoc |

| American Well |

| Enterprise Value / Sales |

| 1.3 |

| NM |

| Enterprise Value / EBITDA |

| 145.9 |

| NM |

| Revenue Growth Rate |

| 11.0% |

| -1.2% |

| Net Income Margin |

| -155.1% |

| -257.0% |

| Operating Cash Flow |

| $285,490,000 |

| -$142,710,000 |

(Source - Seeking Alpha.)

Commentary On Amwell

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks highlighted success in reaching its client migration goals to its Converge platform.

The firm is also part of a "$180 million task order awarded to the Leidos Partnership for Defense Health. [DHA]"

This serves to increase the company's revenue visibility and expand its total addressable market, with the US government becoming one of the firm’s largest customers.

Total revenue for Q3 2023 fell by 10.5% year-over-year while gross profit margin dropped by 5.3%.

Selling and G&A expenses as a percentage of revenue dropped by 0.1% YoY, while operating losses were reduced by 9.0% but remained unsustainable at $64.5 million.

The company's balance sheet is solid, with $418 million in liquidity and no debt, but the firm is burning through a high amount of cash.

In the most recent conference call, analysts asked leadership about the government contract win and migration versus legacy dynamics.

Management replied that the government win would require initial deployment efforts, but that would be a boost to cash flow. It also positions the firm to pursue a contract with the Veterans Administration.

With sunsetting its legacy platform, management expects to see up to $10 million in cost savings and expects to complete migration by the end of 2023.

However, the legacy system is still currently a drag on the firm operationally and financially. Management believes clients on its new Converge platform will scale over time.

Looking ahead, the consensus topline revenue decline for 2023 is expected to be 6.5% versus 2022.

If achieved, this would represent a swing to revenue decline versus 2022’s growth rate of 9.6% over 2021.

Management is no doubt looking forward to 2024’s opportunities with the DHA contract, completion of sunsetting its legacy platform and lower prior-year comparables.

However, the company has much work to do to reignite revenue growth while substantially reducing operating losses in an industry that is under significant cost pressures.

My outlook on American Well Corporation remains Bearish [Sell] until we see a material improvement in its financial results.

For further details see:

Amwell Looks To 2024 For Stabilization But Operating Losses Remain High