XOP - AMZA Vs. XOP: Only One Winner But Second Place Gets Chicken Dinner

- A year back, we made a call on how AMZA and XOP would perform in different pricing environments.

- We examine what the pricing environment was and how the thesis played out.

- We update our thesis for the next 12 months.

Capital in markets is limited. While investors may like to buy everything that they admire, the reality is that they have to try and direct money at the best opportunities available at any given time. This was exactly our thinking when we covered InfraCap MLP ETF ( AMZA ) back in July 2021. We recognized the upside potential in midstream stocks, but at the same time we recommended a different play for those bullish on energy.

For reasons cited above though, we expect, Energy Select Sector SPDR ETF ( XLE ) and SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ) to deliver strong outperformance. Our relative outlook is provided below. We have based it on crude oil but you can extrapolate the same for Natural Gas prices. Note this is the outlook for the sector and we expect some upstream companies to outperform in all pricing environments. We remain very bullish on energy for the long term, but US midstream assets in general and AMZA in particular would be the last way for us to play that.

Source: Reasons Midstream Stocks Are Likely To Lag

Today we update that thesis and do so by comparing AMZA to the same ETF.

The Thesis Then

The thesis back in July 2021 was based on upstream stocks doing better than midstream stocks in all price environments that we could envision. We had presented the following table at the time. Now obviously it is pretty easy to see what kind of price environment we landed with.

Midstream Stocks Are Likely To Lag

Crude oil clearly went past even our high band and has comfortably averaged over $75 a barrel since that article was written. While we did not present this at the time, even Natural Gas averaged higher than our highest expectations. How did AMZA do against our suggested alternatives?

While AMZA performed well compared to the broader markets, it was crushed by both the recommended ETFs and it was not even close.

The Thesis Today

Our fundamental outlook for energy has changed slightly; we now expect Crude Oil prices to stay consistently in the third part ($75-$90) of the above shown table. There are three factors now that make us more bullish on midstream stocks.

- The first of these comes from steadily improving credit qualities of upstream companies. One of the issues that midstream companies have had between 2014 and 2021 is that a lot of it "tenants" have had poor balance sheet health. A period of consistently high oil and natural gas prices has fixed this. As a result, we think a significant revaluation of midstream companies is possible.

- The second aspect is the change in global fundamentals for energy resources has made it even more probable that US drilling for oil and natural gas will trend higher over the years to come. There are certainly hurdles in this regard and some of which are political in nature. But, within acreage already secured, especially in the Permian, we see room for higher production of both oil and natural gas in the years ahead. Midstream companies have always been a volume story first. This volume story is likely to improve materially in 2023 and 2024.

- The third aspect is that midstream companies should have substantially deleveraged over the next 12 months. Alongside that deleveraging we can expect a slow and steady increase in shareholder returns. This will come from distribution increases and share buybacks.

The combination of these factors makes it likely that midstream stocks can continue to deliver good performance even from here.

Midstream Vs Upstream

So as the above states, we are clearly bullish on midstream stocks, perhaps more now than we were about a year ago. However, the twist here is that the current pricing environment has swept fundamentals further in favor of upstream stocks, than midstream stocks. On a relative basis, we see three advantages for upstream stocks versus their midstream counterparts.

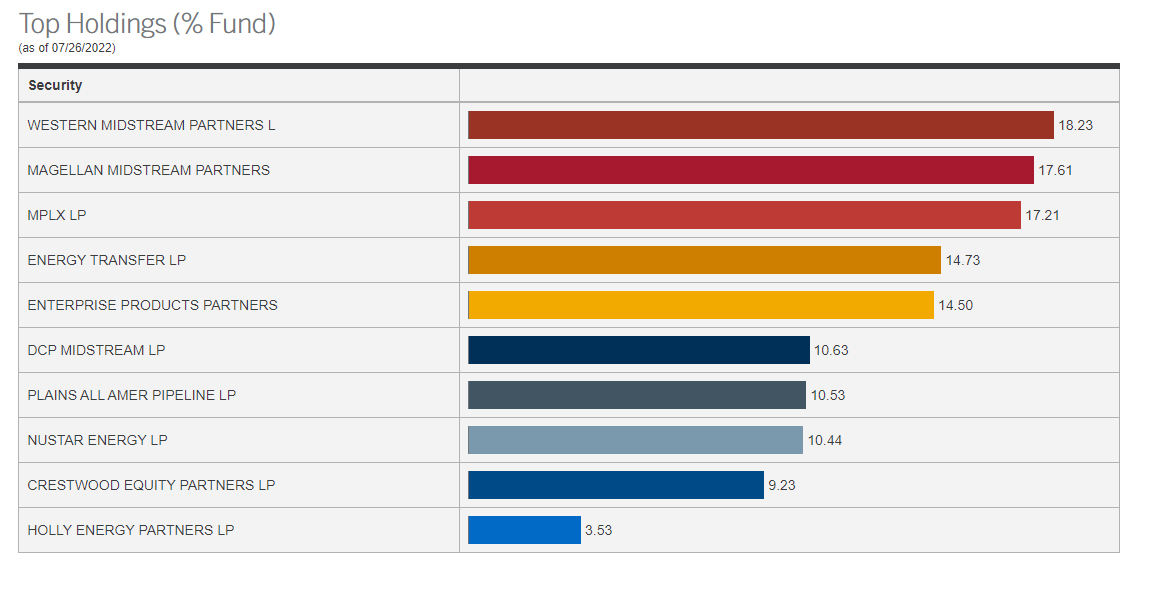

1) The first is the clear differential in valuations. While midstream stocks are cheap, the oil and natural gas producers are even cheaper. We can see this by comparing the valuations of some of the top holdings of AMZA and XOP.

Devon Energy Corporation ( DVN ) is trading at 4.25X EV to EBITDA and Pioneer Natural Resources Company ( PXD ) is flirting with the 4X mark. By comparison, Energy Transfer ( ET ) and Enterprise Products Partners LP ( EPD ) are 3 to 5.5x multiples wide.

{kind=link}

This is true for all of the top 10 holdings of AMZA vs XOP and we show a few more below.

Yes, both sectors are cheap but upstream stocks are in different ballpark at this point.

2) The second advantage is that the gusher of cash flow in 2022 has allowed faster deleveraging in upstream stocks than in midstream stocks. This again flows from the delta that oil and natural gas producers have to higher commodity prices.

3) Finally, we see a faster potential for upstream stocks to return cash to shareholders versus midstream stocks. We have already seen this in the form of special dividends from a few companies and increasing regular dividends as well. Buybacks are coming back in focus. This is especially true in the Canadian E&P universe where the balance sheets were already superior to the US shale plays to begin with.

Verdict

If we were to make a bet on the direction of AMZA 12 months out, it would definitely be on the higher side. We expect positive returns and even higher positive total returns which includes the hefty distribution. AMZA is of course leveraged, while XOP is not. Even then, we expect that XOP will deliver at least 10% outperformance in total returns versus AMZA over the next 12 months. We have also identified specific bullish plays within the E&P sectors and we think Crescent Point Energy Corp. ( CPG ) will deliver at least a 20% outperformance versus AMZA. We are maintaining our hold rating for AMZA and differing our buy ratings for XOP, CPG and DVN.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

AMZA Vs. XOP: Only One Winner, But Second Place Gets Chicken Dinner