MDT - An Approach To Investing In A Recession: Let Mr. Market Come To You

2023-04-30 02:29:58 ET

Summary

- Recession can be scary but recessionary investing can also be rewarding because such periods can create the perfect hunting ground for bargain hunters.

- High-quality, investment-grade companies that have paid growing dividends for decades can continue to provide returns even in economically distressed times.

- Not all dividend payers are created the same. Use these two criteria to sieve out companies that performed well in the Great Financial Crisis.

- Great companies may not be great investments. Safe companies may not be great investments. Valuation still matters for investments to pan out profitably.

- Keep these companies on your watchlist and wait for Mr. Market to offer up buying opportunities.

Introduction

Recession.

It is something almost everyone talks about for the past few months. Some called it the most anticipated recession ever. If a recession is coming, surely investors need to be prepared for it, no?

Investors have to be prepared psychologically because "recession" is a word that strikes fear in many investors since in a recessionary period companies' margins and earnings typically compress and along with those their share prices too. At the same time, the negativity spells an opportunity for value investors who will be out bargain-hunting.

It is one thing for value investors to recognize the opportunities a recession brings. It is another to select companies that do well in a recessionary environment.

And these companies should preferably be dividend payers. Dividend-paying companies' contribution to investors' portfolio returns should not be understated. Based on a Morgan Stanley's research , more than 40% of the total returns over the last 91 years from 1930 to 2021 came from dividends. According to another study from Morgan Stanley ,

With the right mix of stocks, dividends can provide cumulative growth as the earnings can be reinvested back into the portfolio or be used to buy additional dividend-paying shares- a tried and true investing tactic that becomes even more favorable amid economic uncertainty .

Investors should not be overly fearful of recessions. After all, recessions do not last forever. Peter Lynch recently quipped on CNBC ,

We had thirteen recessions since World War 2; we had thirteen recoveries!

In my opinion, investors should have a portion of their portfolio in companies that have demonstrated their ability to do well over long periods of time. Typically, companies that manage to pay dividends and grow these dividends consistently over decades will be a good starting point since these businesses have to be producing increasing revenues and earnings to allow them to pay an increasing dividend through all kinds of economic conditions, and the Dividend Aristocrats is where I choose to start my search.

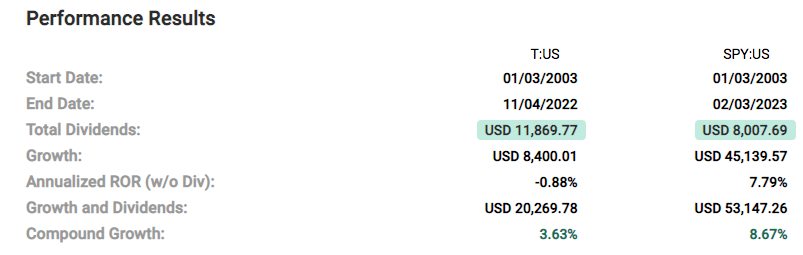

A caveat before I continue: Simply being in business for a long time while paying a dividend is insufficiently telling of a good business. Even Dividend Aristocrats are not guaranteed winners. AT&T (T) is proof of that. Even disregarding the period after which T cut the dividend, T would have been a much poorer investment than simply putting money in an index fund like SPY .

{kind=link}

Having gotten that out of the way, let's take a look at some companies that did perform well through economically challenging times in the past and held up well.

The Approach And The 27 Initial Candidates

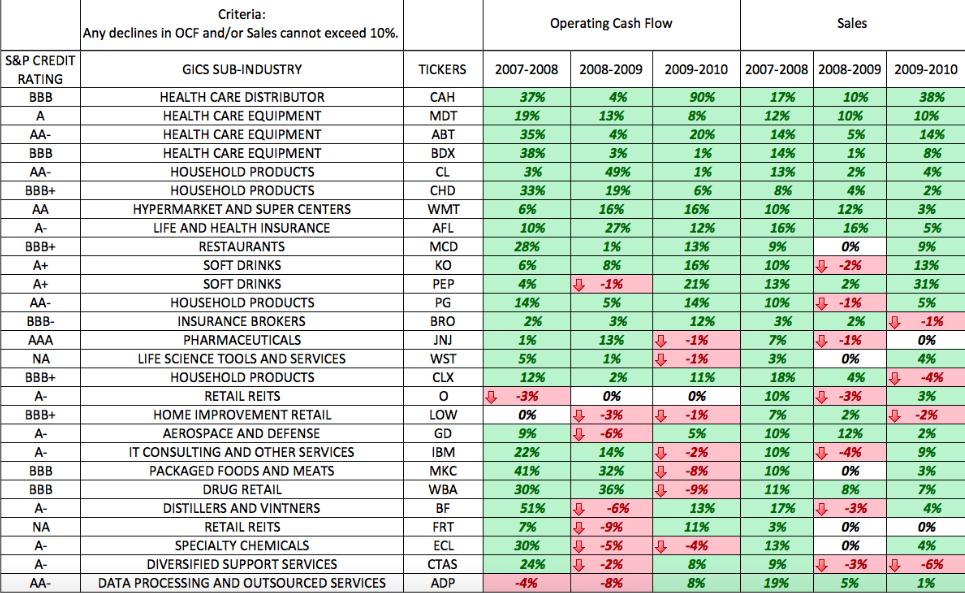

I used the following criteria to sieve out these 27 companies:

- They have to be Dividend Aristocrats

- During the period of the Great Recession, and immediately after (2009 to 2010), the companies' operating cash flow cannot decline beyond 9%.

- During the period of the Great Recession, and immediately after (2009 to 2010), the companies' sales cannot decline beyond 9%.

As evident from the table below, 27 of the 66 dividend aristocrats made the initial cut.

Author's compilation of data from Fast Graph

{kind=link}

The first criterion, dividend aristocrats that have paid dividends for more than 25 years and have proven their mettle, is obviously not rigorous enough. The stress test of the second and third criteria, which examine the companies' performance during the Great Financial Crisis, will surface the best from this list.

Criterion 2: Sales

Revenue is the money a company brings in from its normal business operations. It is an important indicator of the growing demand (or lack thereof) of a company's products and services. As the purpose of this article is to surface companies that can do well in a recession, it will be prudent to study companies that can continue to grow revenue (or at least experience a smaller decline than most) in spite of an economically challenging environment.

Criterion 3: Operating Cash Flow

Looking at sales alone is insufficient since companies can grow sales at the expense of profit. And sales do not represent cash flow, which the latter is an indicator of liquidity. A key to surviving tough times is to have the liquidity to sustain business operations without needing to borrow.

Operating cash flow, therefore, provides clarity on the real situation of a business. If a company is unable to generate enough cash from its primary business operations, it will run into liquidity problems and will need to find other sources of cash flow like financing, and in the high interest rate environment that we are in this will not be desirable. The higher interest repayments will reduce the company's net working capital, and hamper its ability to expand operations or to take advantage of opportunities.

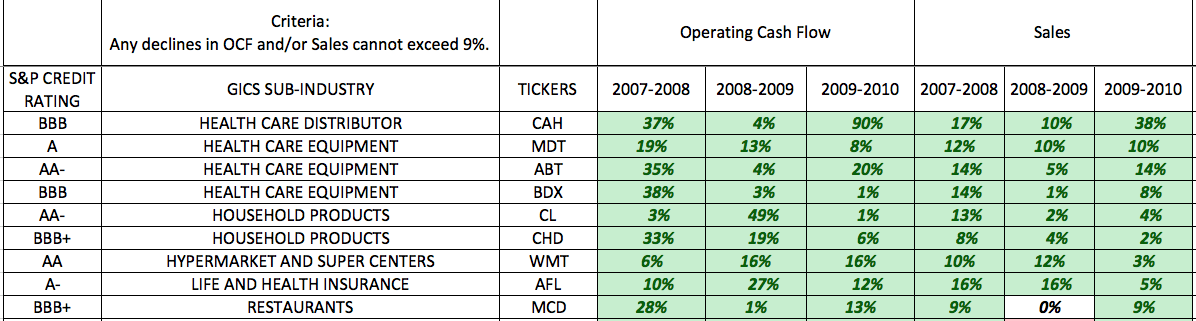

Based on criteria 2 and 3, the initial list of 27 was further narrowed down to 9 for the most risk-averse and conservative investors.

The Top Nine Candidates

The following nine companies did not experience any decline in both operating cash flow and sales when examined through the lens of the three time periods of 2007-2008, 2008-2009, and 2009-2010. The worst performer was McDonald's (MCD) which posted 0% revenue growth from 2008 to 2009 but it made the cut as there was no decline in sales growth.

Author's compilation of data from Fast Graph

{kind=link}

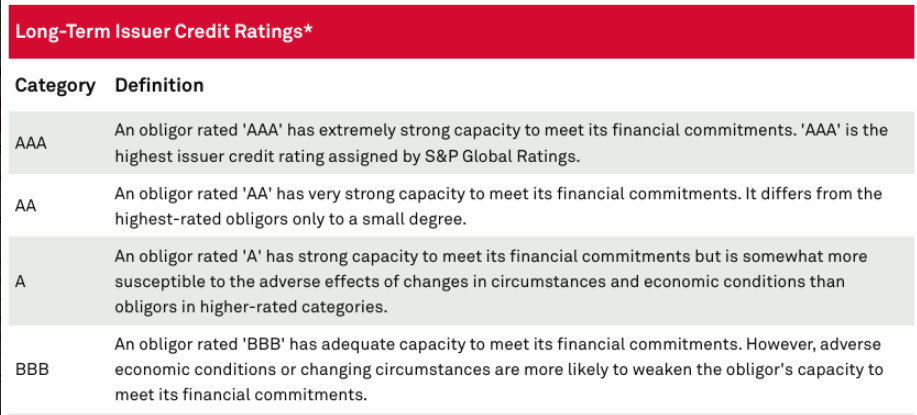

Unsurprisingly, most of these companies are found in defensive sectors such as healthcare and consumer staples. With investment-grade ratings spanning from BBB to AA , these are definitely safe stocks to hold with low probability of default.

S&P Global Credit Rating Description

{kind=link}

It is important to draw the distinction between "safe stocks" and "great investments" . Safe stocks are probably safe from going out of business but they may not be great investments if purchased at prices that do not offer a margin of safety. More on this later.

Valuation And Buy-Hold Decision

Everyone knows what Warren Buffett said about buying stocks at a great value,

Price is what you pay. Value is what you get.

It matters little if these candidates are the safest companies in the world if they are overpriced and overvalued because buying overvalued assets not only means there is no margin of safety, it means investors cannot fully participate in the growth of these companies.

Based on my valuation, all these companies are currently either overvalued or at best fairly valued . Depending on your approach, if you really like a company, it is your prerogative to start a position in it even if it is overvalued, fully ready to dollar-cost-average down as you build up your position.

That is not my approach. I will prefer to wait for Mr. Market to offer wonderful businesses to me at amazing prices (or at least fair prices) before I consider parting with my hard-earned money. I will however place the companies I like on my watchlist and set a price alert.

In the following segment, just for illustrative purposes, I will be providing a brief overview of four of the top nine candidates (arranged in no particular order), one from each defensive sub-sector, complete with links to relevant information for you to conduct your own due diligence on the companies you like to own or to add to.

I will cover Cardinal Health (CAH) from the Healthcare Distributor sub-sector, Medtronic (MDT) from the Healthcare Equipment sub-sector, and Colgate-Palmolive (CL) from the Household Product sub-sector, and McDonald's from the Restaurants sub-sector.

If there is a particular company from this list of nine that you would like me to do a deep-dive on, indicate your interest in this poll , and I may just do that if there is sufficient interest.

Let's go.

A Brief Overview Of Four Of The Top Nine Candidates

1. Cardinal Health

From the 2022 10K , CAH describes itself as

... a globally integrated healthcare services and products company providing customized solutions for hospitals, healthcare systems, pharmacies, ambulatory surgery centers, clinical laboratories, physician offices and patients in the home. We provide pharmaceuticals and medical products and cost-effective solutions that enhance supply chain efficiency. We connect patients, providers, payers, pharmacists and manufacturers for integrated care coordination and better patient management. We manage our business and report our financial results in two segments: Pharmaceutical and Medical .

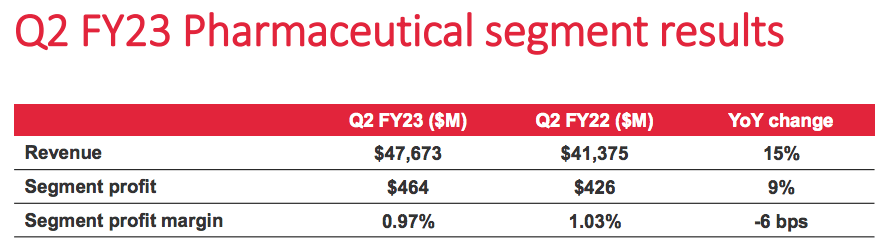

The Pharmaceutical segment has a 15% boost in revenue from 2022 to 2023. Profits came mainly from improved sales under the brand and specialty products, and from the generics program. However, due to increased costs from supply chain headwinds, the year-on-year profit margin was done by 6 basis points.

Q2 2023 Investor Presentation Slide Page 5

{kind=link}

CEO Jason Hollar was particularly pleased with the results from this segment at the Q2 2023 earnings call,

At an enterprise level, we continue to see benefits below the operating line from our capital deployment actions and favorable capital structure. With the first half of fiscal 2023 behind us, we are pleased to raise our full year EPS guidance and outlook for the Pharmaceutical segment .

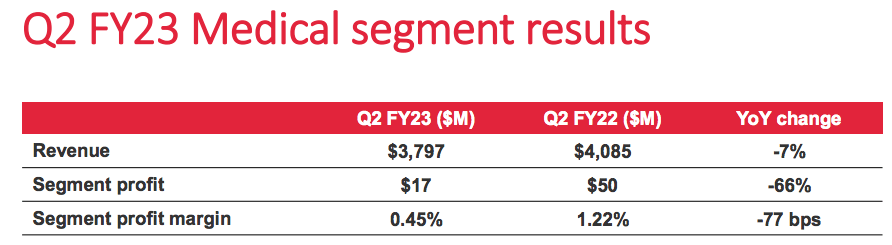

The results from the Medical segment are a little mixed. This segment did not perform as well on a year-on-year basis due to a combination of lower products and distribution volumes, and impact from rising inflationary.

Q2 2023 Investor Presentation Slide Page 6

{kind=link}

Nevertheless, Q2 2023 revenue result was an improvement over Q1 2023, bringing the $3.778 billion in sales up slightly to $3.797 billion in Q2 2023.

The guidance for this segment is understandably more bearish. CFO Trish English expects the revenue from this segment to decline anywhere between 3% to 6%, and the profit to range from flat to a loss of 20%.

Risk and Valuation

CAH had not performed well in recent years due in part to the uncertainty surrounding its role in the opioid crisis. After the settlement with the US government, that matter is largely behind them and investors are able to have more investment clarity.

Author's probability estimates

{kind=link}

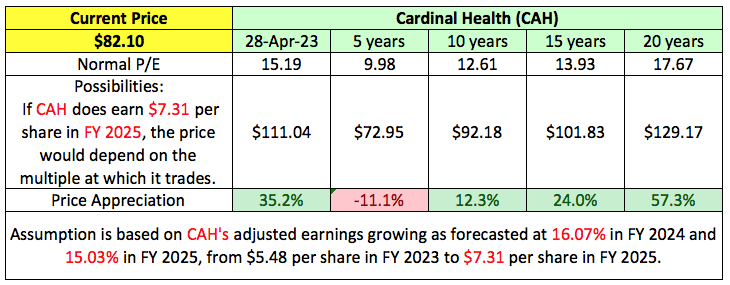

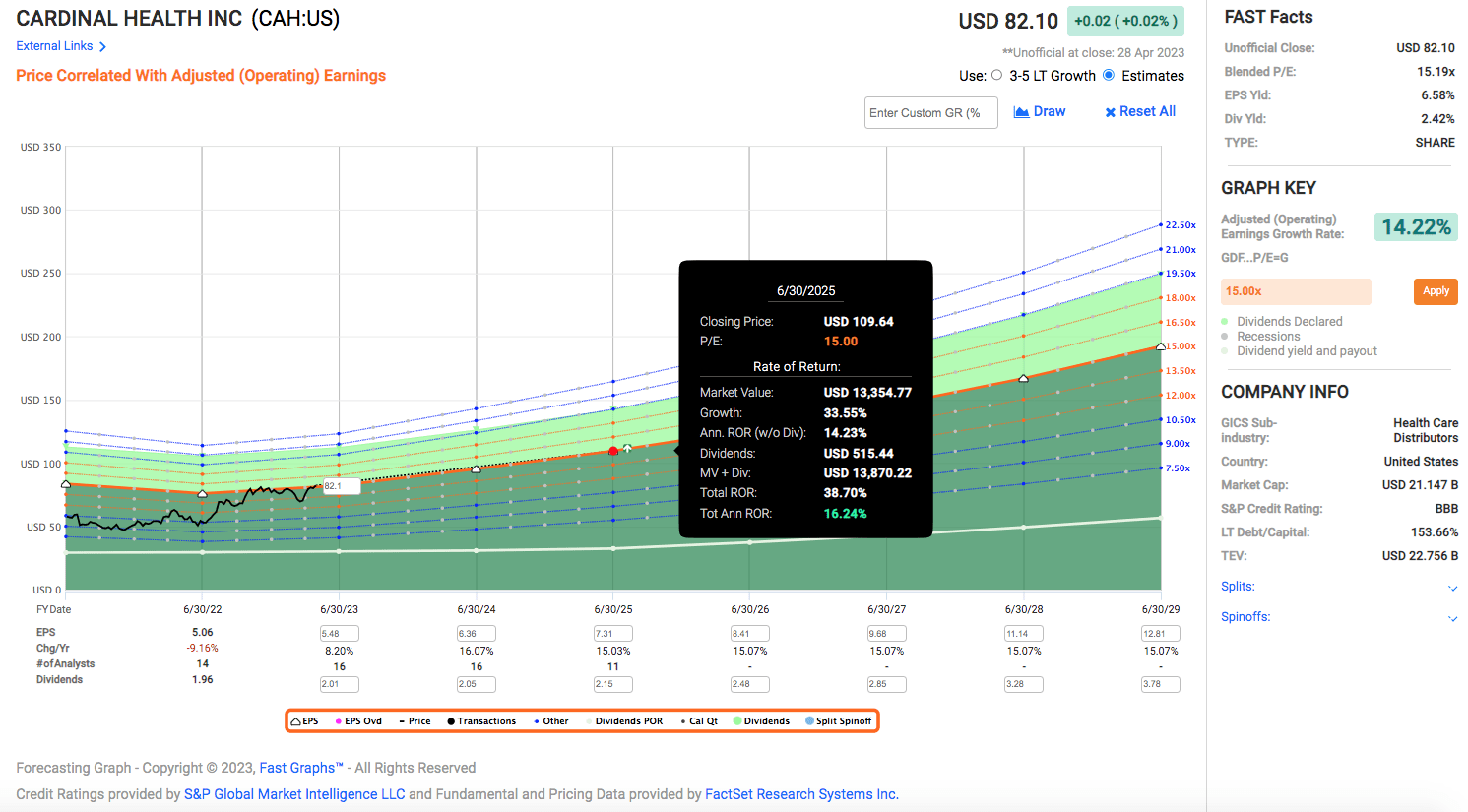

At the current price of $82.10, CAH is fairly priced but definitely not a screaming buy. If analysts' earnings forecasts are spot on, CAH could provide an annual rate of return of 16.24% in 2 years.

{kind=link}

Takeaway

A 16.24% annualized rate of return sounds great but CAH has a dangerously high long-term debt-to-capital ratio of 153.66%. Despite it being a BBB credit-rated company that pays a 2.42% dividend, I will prefer a larger margin of safety before opening a position in CAH.

2. Medtronic

According to the company's 2022 10K ,

Medtronic... is the leading global healthcare technology company... Our Mission - to alleviate pain, restore health, and extend life - empowers insight-driven care and better outcomes for our world... We have four operating and reportable segments that primarily develop, manufacture, distribute, and sell device-based medical therapies and services: the Cardiovascular Portfolio, the Medical Surgical Portfolio, the Neuroscience Portfolio, and the Diabetes Operating Unit.

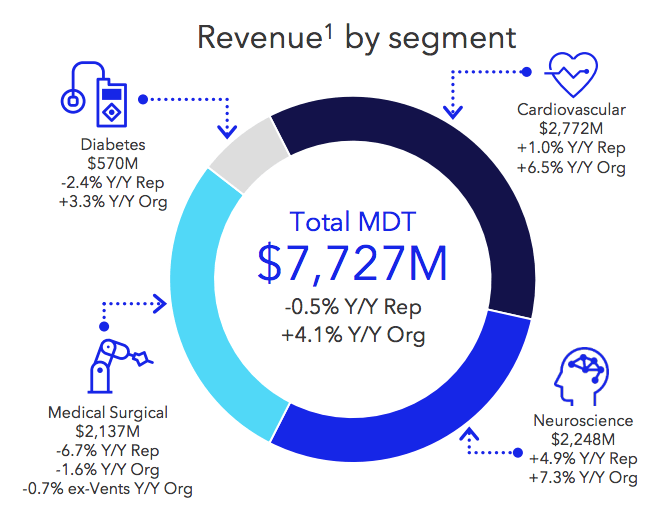

CFO Karen Parkhill sounded positive at Q3 2023 earnings call and gave the following upbeat guidance for the full year,

Given our top and bottom line beat in the third quarter, we are raising our full year revenue growth and EPS outlook. On the top line, we expect our fourth quarter organic revenue growth to be in the range of 4.5% to 5%, which is unchanged from what was implied by our second half guidance that I gave last quarter... We continue to expect Cardiovascular to be up 5.5% to 6%, Medical Surgical to grow 2.5% to 3%, neuroscience to increase 6.5% to 7% and Diabetes to decline in the low single digits, all on an organic basis... Given our third quarter $0.03 beat, we raised the lower end of our fiscal '23 non-GAAP diluted EPS guidance by $0.03 to the new range of $5.28 to $5.30

Medtronic March 2023 Investor Handout

{kind=link}

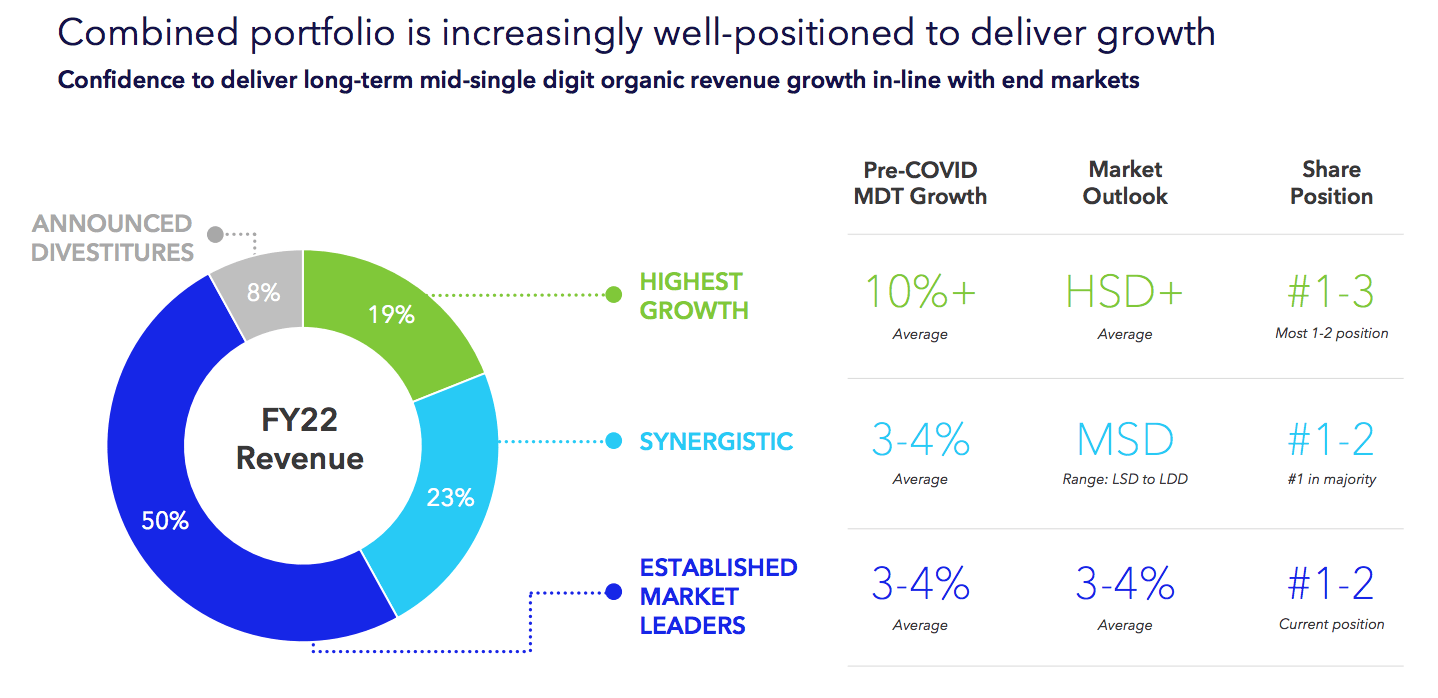

Beyond these 4 reportable segments, CEO Geoff Martha shared his thinking about MDT's portfolio. He sees the businesses in three groups: highest growth , synergistic and established market leaders ( 50% of the total revenue ) .

Medtronic March 2023 Investor Handout

{kind=link}

On the Established Market Leaders:

These business units, which include the cardiac rhythm and spine, and Surgical Innovations businesses, are expected to grow at an average of 3-4%.

On the Highest Growth Business:

The high-growth units include Structural Heart, Cardiac Ablation Solutions, Surgical Robotics, Neurovascular, and Diabetes. Collectively, these businesses contribute 20% of MDT's revenue and are expected to grow in the high single digits. MDT has been investing heavily in these businesses to position these to make up an even larger part of the company's revenue.

On the Synergistic Business:

These units include Cardiac Diagnostics, which sales of LINQ II grew double-digits, and Neuromodulation, which grew 12% in pain stim, and GI Genius which uses artificial intelligence to help physicians detect polyps during colonoscopies, grew in the high single digits on the back of strong demand.

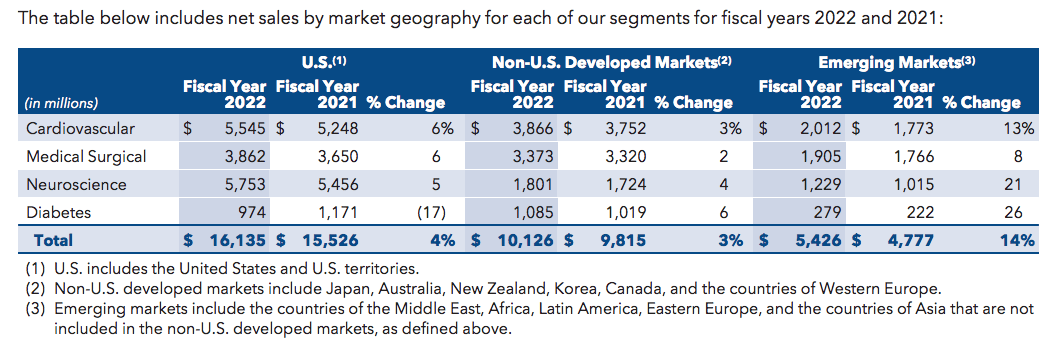

Despite having a strong, market leadership position in almost every group (highest growth, synergistic and established market leaders), MDT continues to grow its sales in the developed and mature US and non-US markets.

{kind=link}

But the real growth area lies in the emerging markets with a strong 14% growth from FY 2021 to FY 2022.

Risks and Valuation

In Q3 2023, outside of China, revenue grew 17% . The headwind from China comes in the form of volume-based procurement ( VBP ) which brought the 17% figure down to 5%, and the negative impact will continue into FY 2024. The CEO gave more color to this headwind,

I mean we think that 80% of our portfolio... could be impacted by VBP. ... we're 50% of the way through. And the remaining 30%, we will get in FY '24 . We don't think the remaining 20% will be impacted certain things that are nuanced or under the radar screen. And what we're doing here is taking out some of our selling and marketing costs in China to offset the lower prices... So the (Chinese) government is living up to the volume commitments from those VBPs at these lower prices . The discounts have gotten lower as they have gone on... we will reset our business and grow from there. And so, FY '24 will be another year where China is a bit of a headwind .

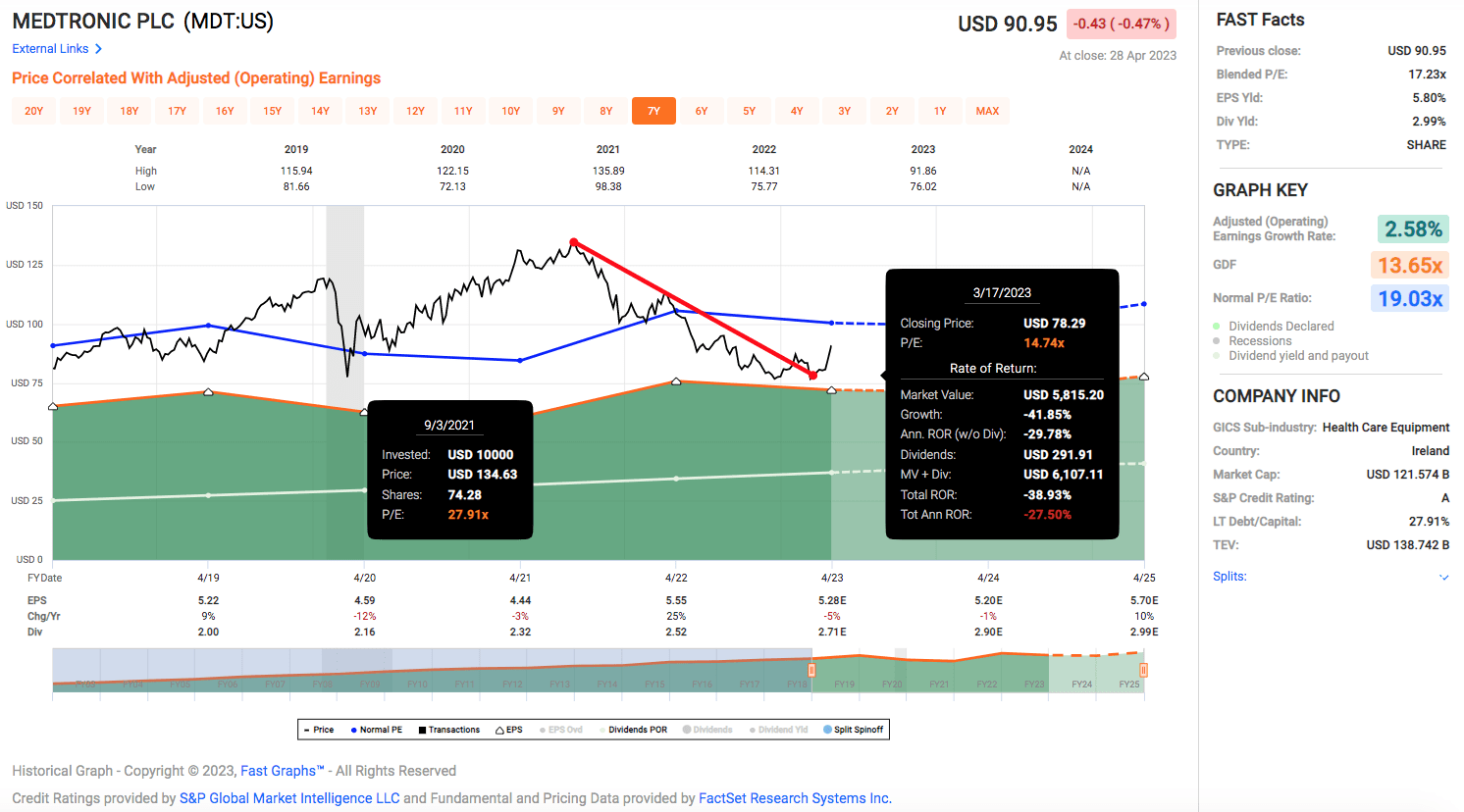

Due to various issues like the Ukraine war, supply chain disruptions affecting especially the Surgical Innovation business, and now VBP in China, MDT has not been doing well these past two years. The stock price collapsed more than 41% from $134 in Sep 2021 to $78 in March 2023, before recovering on the back of the improving Q3 2023 results to $90.95.

{kind=link}

Volume-based Procurement is meant to make healthcare more affordable for Chinese citizens in China, or as this whitepaper puts it,

VBP aims to lower the price of medical consumables by tendering the market volume of cities, provinces, or the country to manufacturers at the lowest price... VBP is expected to reduce revenue for medical device companies with an increase in the number of tenders at the provincial and national levels... medical device suppliers need to be ready for high-price cuts or risk losing their market share gradually.

In short, VBP means med-tech products being sold have experienced huge price cuts.

{kind=link}

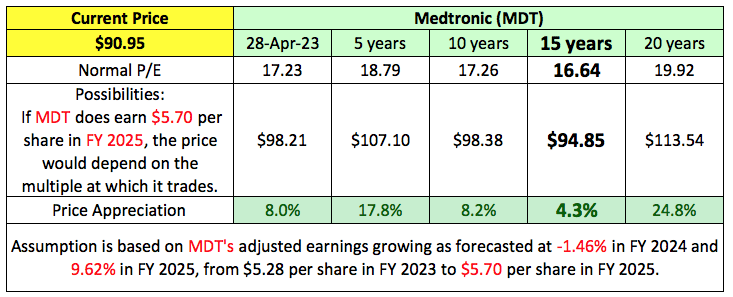

In lieu of the lingering issues around VBP, I will personally assign a more conservative multiple to MDT. Rather than the 20-year normal P/E of 19.92, I think a P/E of around 15-16 is more appropriate.

Author's probability estimates

{kind=link}

Investors should remember that even a premium market leader like MDT had periods when it traded in the lower P/E range of 10-12 for years from 2009 to 2012. And at a P/E of 16.64, if the company manages to grow adjusted operating earnings as forecast, it could potentially have a mere 4.3% in share price appreciation, a lackluster result.

{kind=link}

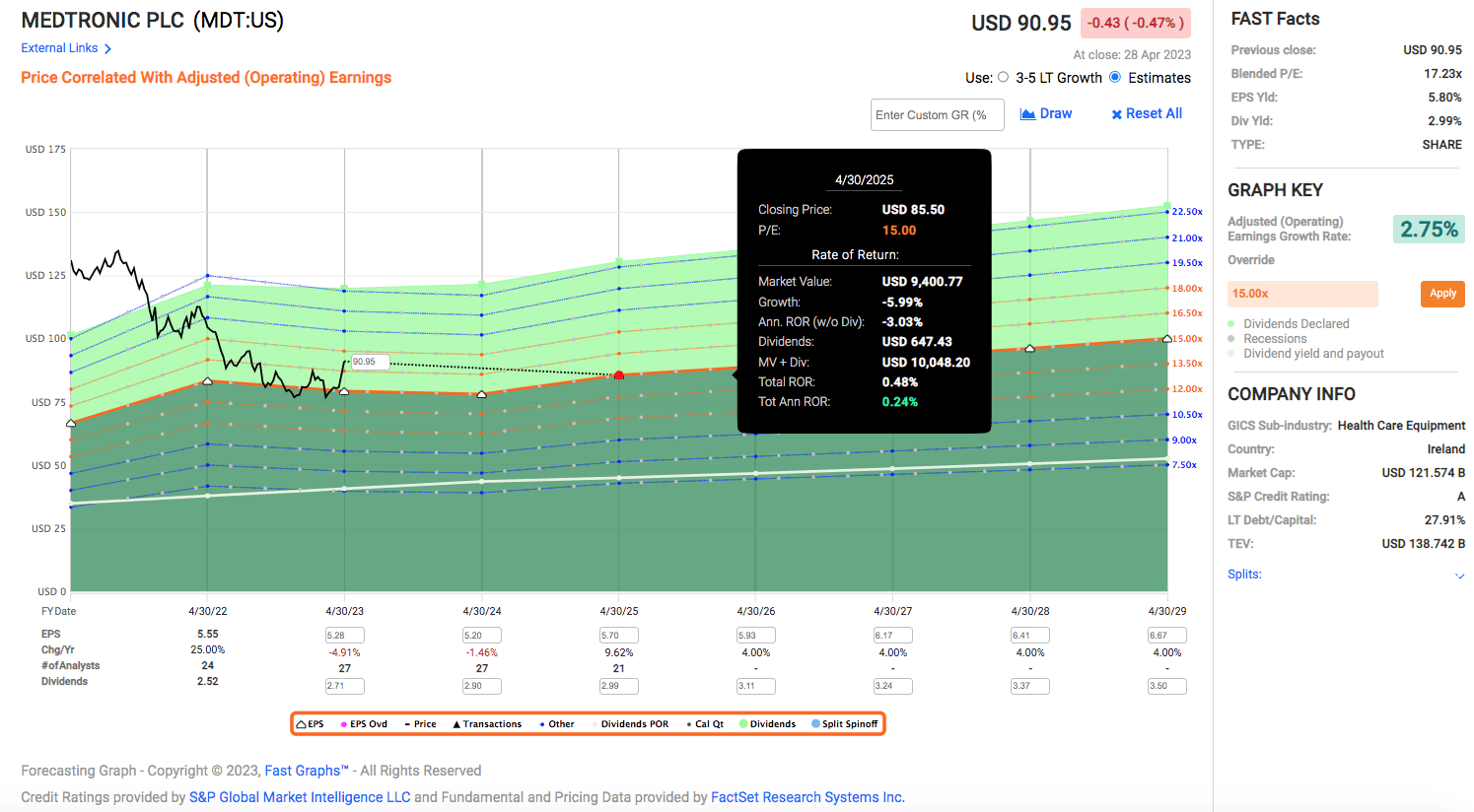

After the price recovery in the recent few weeks, MDT moved out from being slightly undervalued in March to being fully valued currently. There is no margin of safety to invest in MDT now. Assuming a P/E multiple of 15 and MDT generates the expected average growth rate of 2.75% (FactSet analysts' 2-year earnings forecasts are 92% accurate) from now till 2025, after accounting for dividends, an investment now will only break even.

Takeaway

Despite MDT being an A-rated company with a low long-term-debt-to-capital ratio of 27.91%, paying a 2.99% dividend yield, and it being a market leader in almost every area it operates in, the combination of near-term headwinds and the price at which it is trading at now does not offer any margin of safety for an investor seeking a safe investment.

The next two companies really do not need any introduction. Everyone knows Colgate-Palmolive and McDonald's. Most of us will have at least one product in our house that comes from CL. Most of us would have eaten something from McDonald's at least once in our life. I believe that companies (or brands) like CL and MCD are so well known and loved that it is part of the reason why they are perennially trading at premium valuations that do not commensurate with their fundamentals like earnings growth rate.

As a value investor, I would often invest in smaller, less well-known companies with excellent track records and future growth potential, and proceed to wait for the rest of the market to realize their true worth. If you are interested, do check out my research on STAAR Surgical (STAA), Diodes (DIOD) and BJ's Wholesale (BJ). Since my latest publication of each of these companies, BJ has returned 34.8%, DIOD has returned 21.29%, and STAA has returned 19.77% .

Now, let's take a quick look at CL and MCD and their valuations.

3. Colgate-Palmolive

CL reports its revenue in two product segments that are organized into four groups ( Oral , Personal and Home Care ; and Pet Nutrition ).

The largest revenue contributor comes from Oral Care, generating 43% of CL 2022 total sales.

{kind=link}

The second-largest revenue contributor comes from the Pet Nutrition segment making up 21% of total sales.

{kind=link}

The last two segments are Personal Care (19% of net sales) and Home Care (17% of net sales).

CL sells its products in over 200 countries, which is pretty much the entire world, which does make one wonder where else would future growth come from.

2022 Annual Report

For such mature companies like CL, they can try to grow sales through acquisitions (like the Filorga acquisition in 2019 ) or they can boost earnings per share through a combination of margin improvement and share buybacks.

Clearly, those efforts have not yielded much result for CL. Overall, revenue and gross profit basically remained flat since 2013.

{kind=link}

Due to supply chain issues and rising costs of materials, margins have gotten worse in the last three years.

Morningstar Operating Performance

{kind=link}

Risks and Valuation

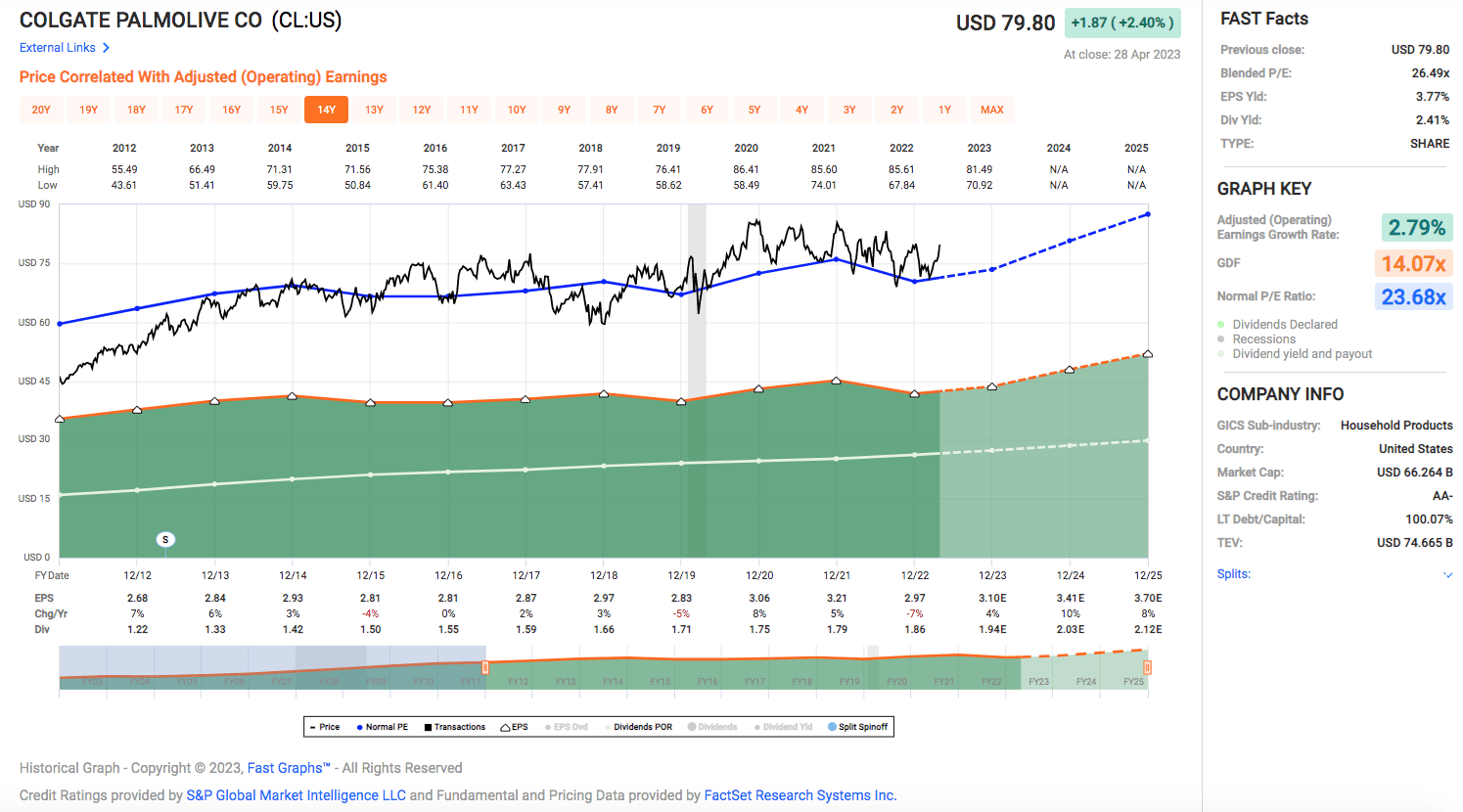

As mentioned earlier, CL is a company that could manage only a 2.79% "growth" in adjusted operating earnings from 2012 to 2023, yet investors seemed willing to pay a premium of more than 20 times earnings for the shares of an almost zero-growth company when there are many better options out there.

{kind=link}

FactSet analysts expect the company to grow adjusted operating earnings at an average rate of 7.18% for the next three years. However, purchasing shares at the current price of $79.80 at a blended P/E of 26.49 offers no margin of safety.

{kind=link}

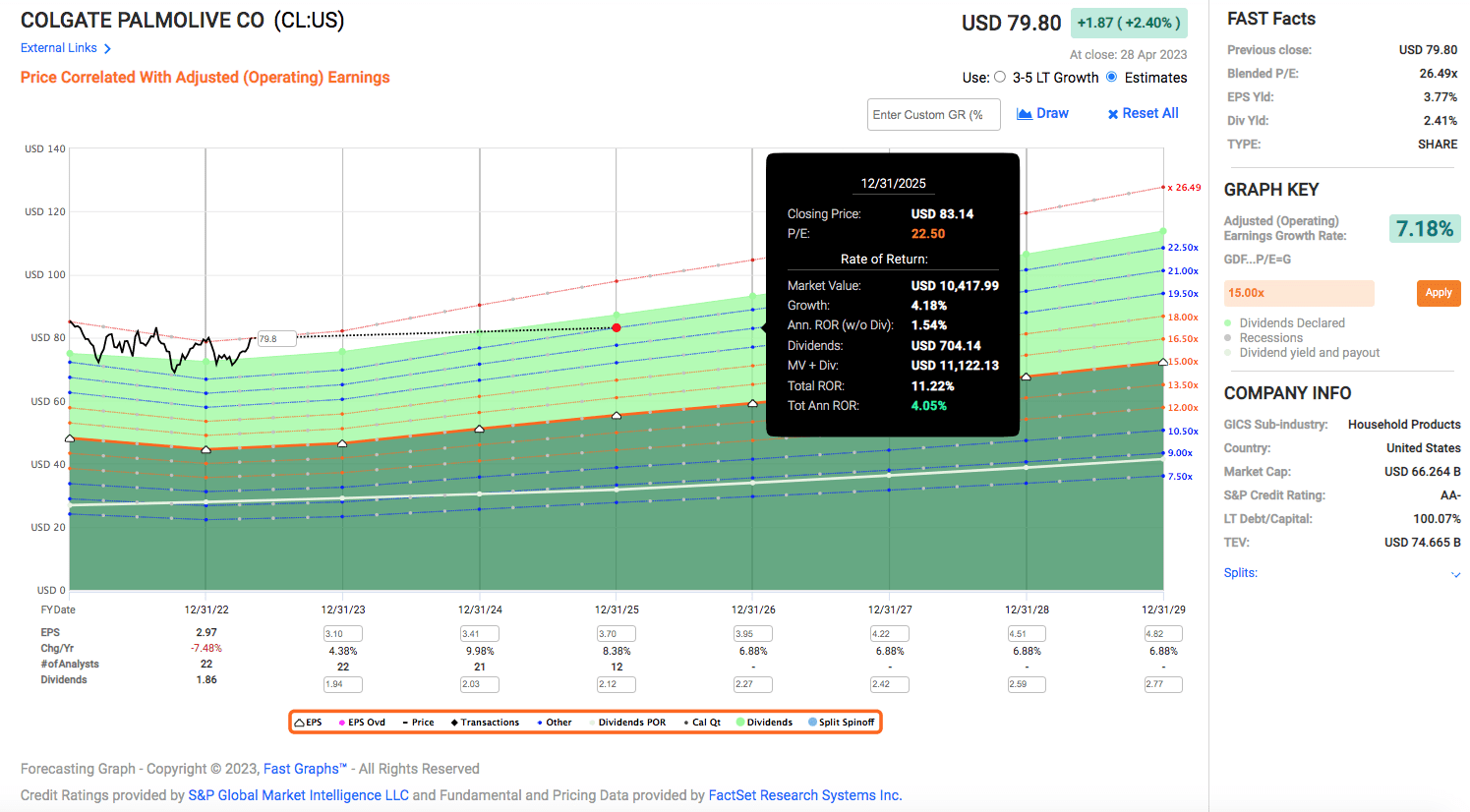

If CL trades back to a valuation close to its own long-term market valuation of around 22-23, even if CL does grow earnings at 7.18%, an investor will only get a 4.05% return as buying CL shares when they are overvalued denies him the chance to fully participate in the company's growth.

That represents an unfavorable risk-and-reward scenario because even an investment in the 3-year US Treasury note at 3.7% can provide better returns without the risk of capital loss.

Author's probability estimates

{kind=link}

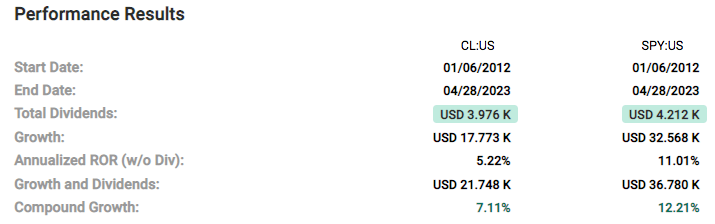

I get it that CL is a AA- rated company that sells products that almost everyone on Earth has used and will probably keep using. I get it that CL could be a great business but I stop short of saying it is a safe investment. An investment in SPY in the same time frame will yield a much higher return than a similar investment in CL.

{kind=link}

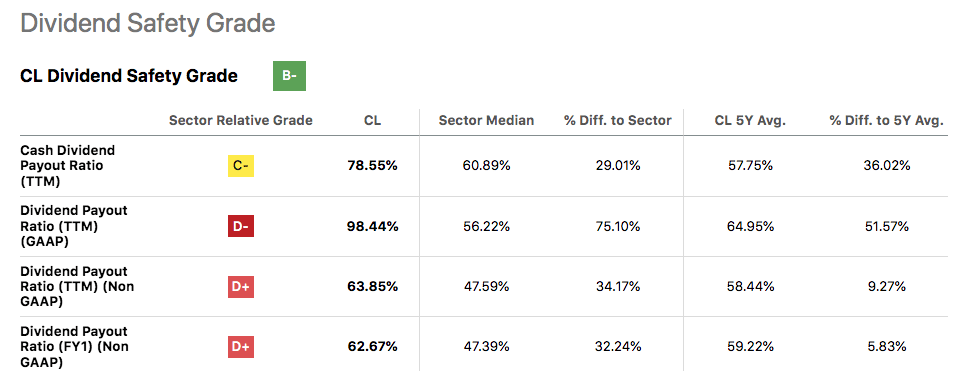

CL also has a dangerously high long-term debt-to-capital ratio of 100.07%. Although Seeking Alpha gave CL a solid Dividend Safety grade of B-, I am more concerned about its dividend payout ratio. The Dividend Payout Ratio as measured as a percentage of GAAP earnings has increased from the 5-year average of 64.95% to 98.44%.

Seeking Alpha Dividend Safety Grade

{kind=link}

Takeaway

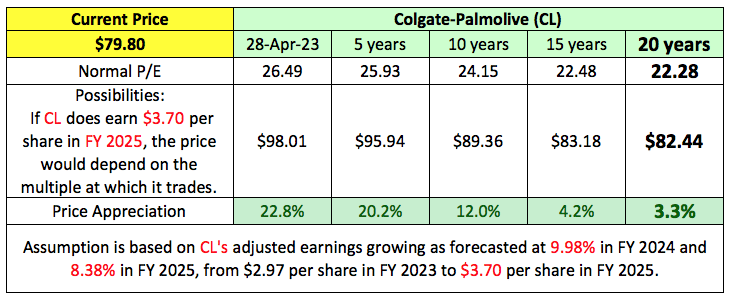

Despite CL being an AA-rated company that pays a respectable 2.41% yield in dividends, it has a very high long-term-debt-to-capital ratio that exceeded 100%. The price at which it is trading at now does not offer any margin of safety for an investor seeking a safe investment. Plus, if all an investor can hope for while taking on the risk of owning equity is just to get a 3.3% return in the form of share price appreciation, I will say let's wait for a better entry.

4. McDonald's

The last on the list of nine that I will cover is MCD. The ubiquitous presence of McDonald's restaurants in countries all over the world is a testament to the success and popularity of the fast food chain.

According to the 2022 10K ,

Of the 40,275 McDonald's restaurants at year-end 2022, approximately 95% were franchised...

The Company is primarily a franchisor and believes franchising is paramount to delivering great-tasting food, locally relevant customer experiences and driving profitability...

The Company's revenues consist of sales by Company-operated restaurants and fees from restaurants operated by franchisees... These fees, along with occupancy and operating rights, are stipulated in franchise/license agreements that generally have 20-year terms.

The Company's Other revenues are comprised of fees paid by franchisees to recover a portion of costs incurred by the Company for various technology platforms, revenues from brand licensing arrangements to market and sell consumer packaged goods using the McDonald's brand and, for periods prior to its sale on April 1, 2022, third-party revenues for the Company's Dynamic Yield business.

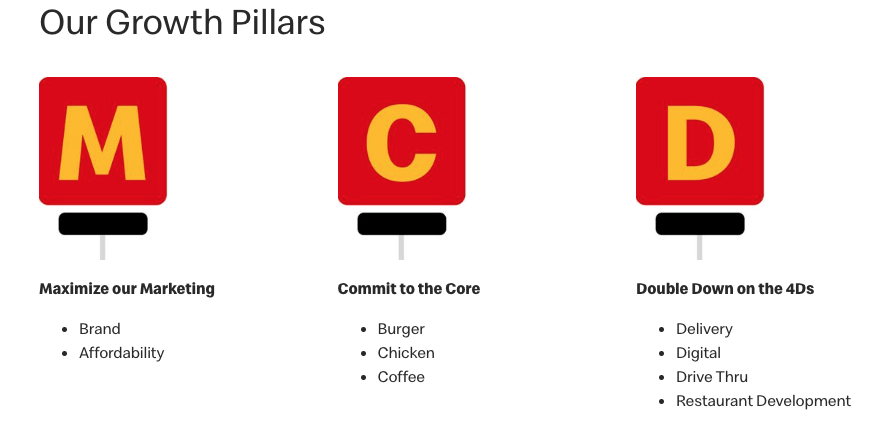

Despite having an international presence in over 100 countries, MCD still aims to grow. In 2020, MCD launched " Accelerating the Arches " a new growth strategy that builds on its traditional strengths and articulates new areas of opportunity. In 2023 , MCD added a fourth "D" to the strategy - Restaurant Development - "to fully capture the increased demand" that came as a result of the

Accelerating the Arches Growth Strategy

{kind=link}

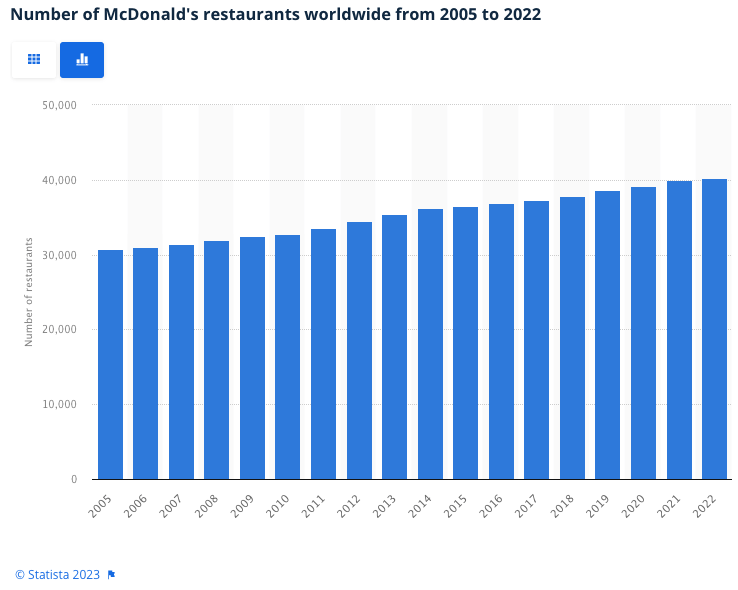

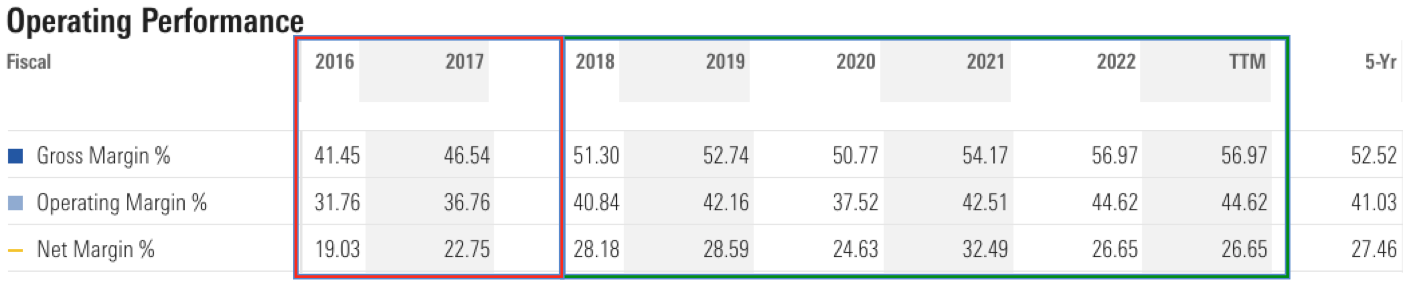

MCD has been desperately trying to find growth areas. Like CL, it is getting harder to increase revenue. Although the number of MCD restaurants has been increasing every year, that is not the case with revenue or profit.

{kind=link}

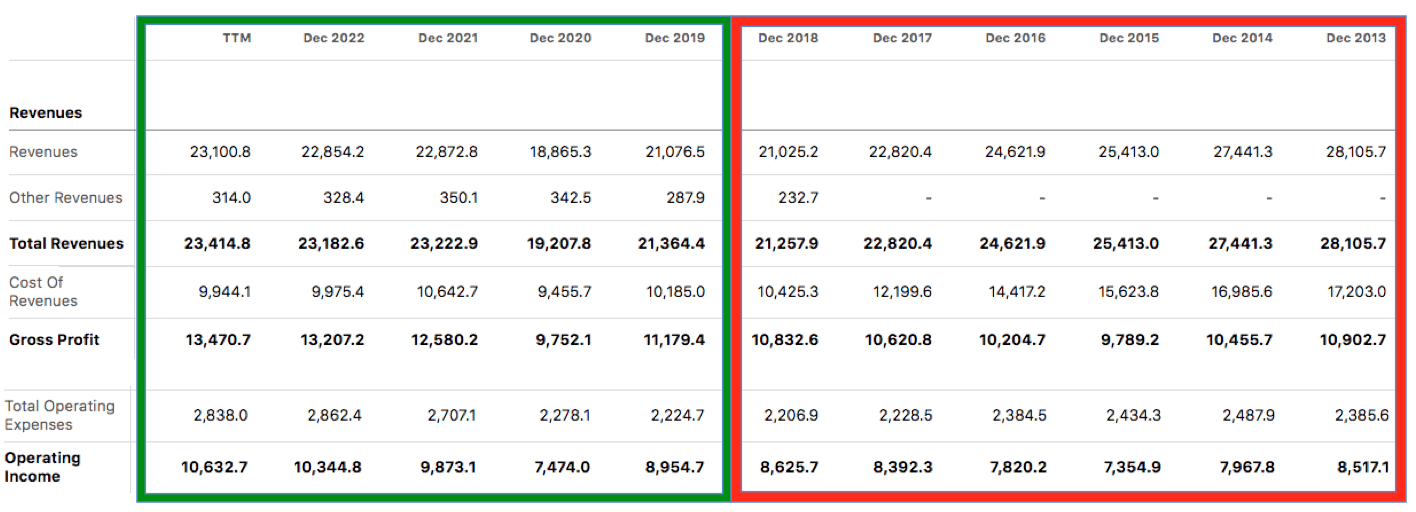

Revenue actually fell from 2013 to 2018 while gross profit plateaued.

{kind=link}

There has been some improvement since 2019. Revenue is showing some growth though the latest figure still falls short of the revenue generated in 2013. MCD manages to bring in more profits and operating income, although the increase when compared to the figures 10 years ago is unimpressive.

{kind=link}

Management did well to improve margins overall in the past five years, but there is only so much profit that can be squeezed out of a smaller revenue base.

Risk and Valuation

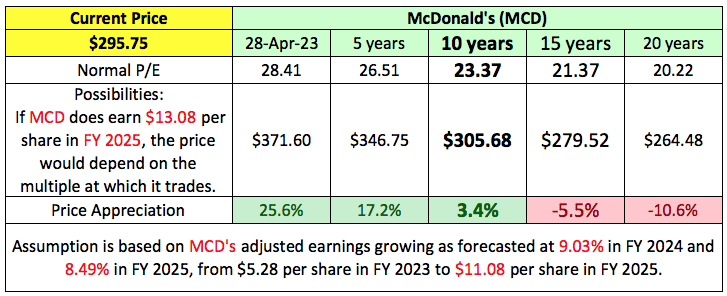

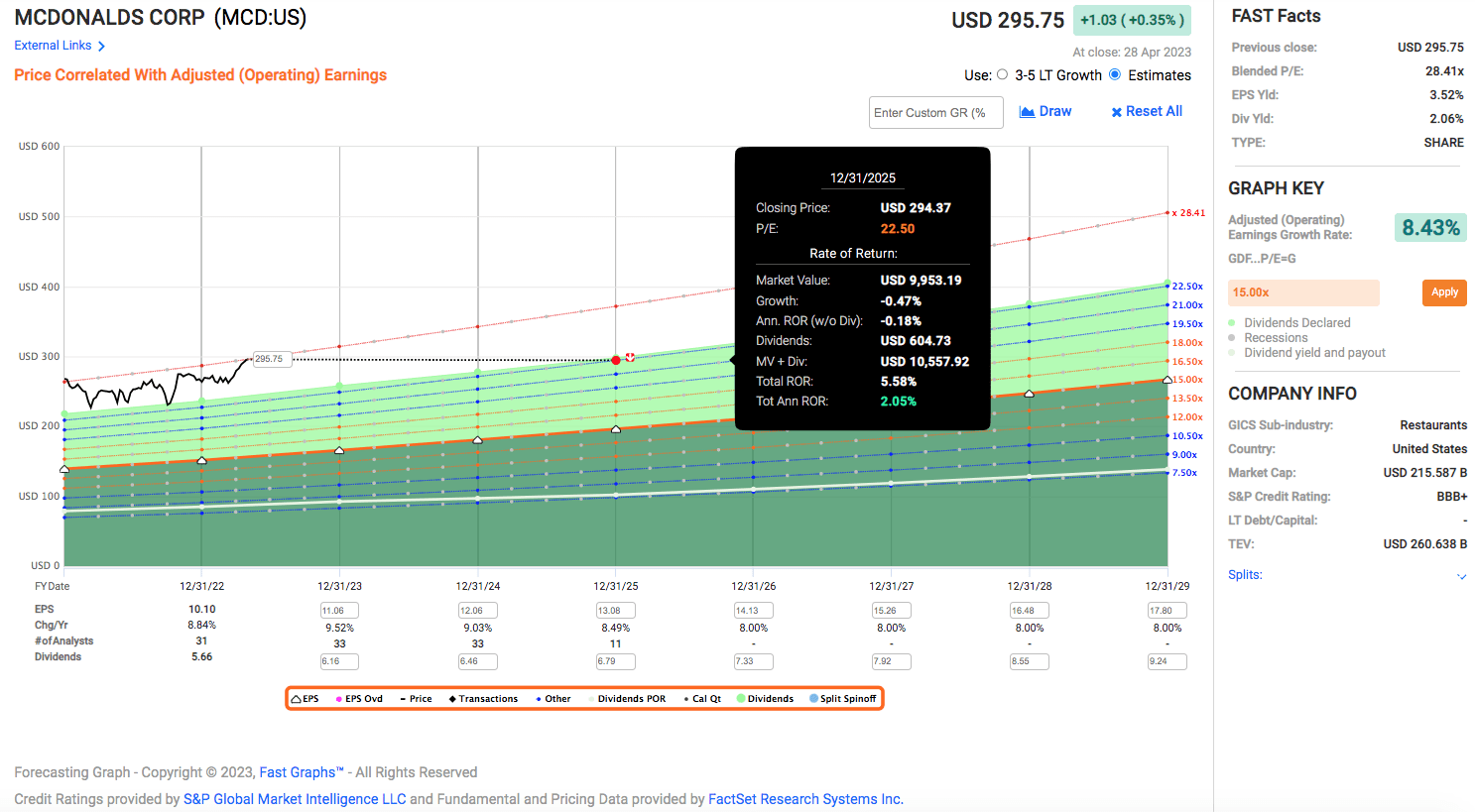

MCD is currently trading at a very high blended P/E of 28.41. For the most part of 2002 to 2015, MCD traded at a multiple of under 20 times earnings. If MCD were to trade at a blended P/E of 21 or lower, even if it can hit its earnings growth forecast of 8.42% a year to arrive at $11.08 per share in 2025, this investment will suffer a significant capital loss.

Author's probability estimates

{kind=link}

In order to show double-digit growth in price appreciation, the stock has to continue to trade at a premium valuation while meeting or exceeding its earnings growth forecast.

MCD's adjusted operating earnings are forecast to grow at a rate of 8.43% per year. However, because it is trading at a multiple far higher than its 20-year normal multiple, there is a much higher probability that the stock will revert closer to its long-term multiple of 20. When that happens, an investment in MCD now will barely break even by 2025. This means that investors who invest in MCD now may not be able to fully participate in this 8.43% growth in earnings even if the forecast growth figures are accurate.

{kind=link}

Takeaway

MCD is a BBB-rated company. It pays an above-average dividend yield of 2.04% respectable 2.41% yield in dividends. However, as it is trading at a premium valuation that is far higher than even its normal market multiple, there is no margin of safety.

Conclusion

Warren Buffett once said,

Risks to us... relates to several possibilities. One is the risk of permanent capital loss, and the other risk is just an inadequate return on the kind of capital we put in.

I believe that the companies surfaced above are recession-proof investments, meaning these companies can do better than many others in an economically poor environment. Investments in these nine companies should not result in capital loss.

However, finding the right stocks to buy that meet one's criteria is just the first step. Buying these stocks at the right price is just as important because great companies do not equate to safe investments if the investments in them are at a price and valuation that does not offer any margin of safety. That is neither prudent nor safe.

In times like this when investors are readying themselves for the most anticipated recession of all times, it is important that they do not blindly pour money into supposedly "safe" investments like Dividend Aristocrats just because they want to weather the storm. I love having Dividend Aristocrats in my portfolio as much as the next dividend investor - but only when the price is right.

Therefore, these 9 companies are on my watchlist, and if Mr. Market offers me an opportunity to buy them at a deep discount to skew the risk-and-reward in my favor, I will rub my hands with glee and take out my wallet. Until then, I appropriate Charlie Munger's "sit-on-your-ass" investing methodology.

Sit tight. Be patient. Let Mr. Market come to you with a better price.

For further details see:

An Approach To Investing In A Recession: Let Mr. Market Come To You