AFMC - An Insider's Guide To The Banking Industry Amongst The Turmoil

2023-03-20 06:30:00 ET

Summary

- Why the 2 recent bank takeovers happened.

- Six actions to stop future takeovers from being needed.

- The current state of the banking industry and what happens next.

- Nine risks to look for in a bank investment assuming a likely recession.

Bank Failures in the Past

I was a career banker starting out as a government bank examiner. In 1992 I got a job with a bank and had several jobs including credit analysis and risk management. Most banks take risk management very seriously as it is essentially a risk management business. When I was an examiner, we always looked at interest rate risk. In the 1980s almost all S&Ls in the country and many banks would have been technically insolvent if they had to show unrealized losses on investments and loans. This was because the Federal Reserve raised the Fed Funds rate to over 20%, way way higher than the 4.50-4.75% of today. Many lost money for years until rates came down but they were allowed to survive if they had positive net worth.

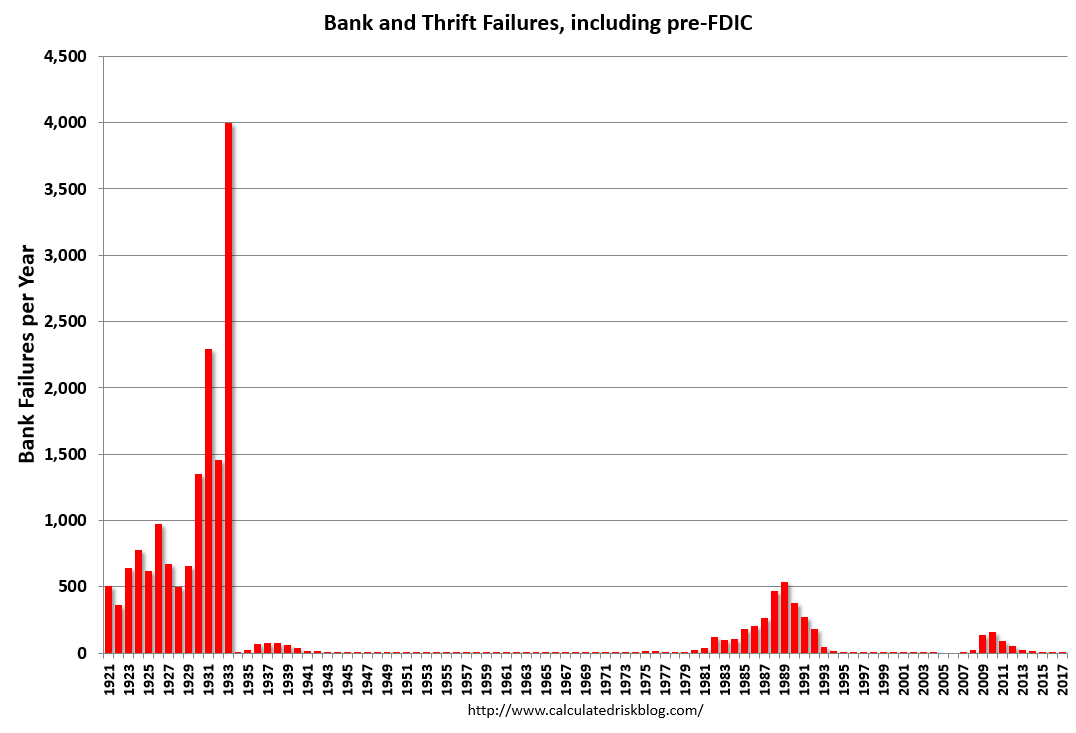

In and after the 2007-2009 recession a number of banks were taken over by the FDIC. Bank failures tend to lag a recession so the peak failure years were 2008 to 2012. In that time 465 banks or S&Ls were taken over. However, that paled versus the Great Depression and late 1980s/early 1990s as shown in the chart below.

{kind=link}

calculateriskblog.com

In the 2007-2009 recession and late 80s/early 90s in almost every case, the cause of the failure was bad loans. The only failures caused by a run on the bank I can recall was Lehman and Bear Stearns in 2008. Neither Lehman nor Bear Stearns were FDIC insured and Bear was actually sold to JPMorgan with help from the Federal Reserve.

What Just Happened?

So, what happened to cause the FDIC takeovers at Silicon Valley Bank ( SIVB ) and Signature Bank ( SBNY ), and the runs at Silvergate ( SI ) and First Republic ( FRC )? The first 3 were all non-traditional banks. They were heavily involved in riskier activities few other banks touch such as cryptocurrencies (SBNY and SI) and venture capital. Their deposit base also had a much higher percentage of deposits over $250,000 making most of them uninsured by the FDIC. Further, in the case of SI, SIVB and FRC they had an abnormally high amount of fixed rate investments or deposits.

The spark was the Federal Reserve raising the Fed Funds rate from 0% to the current 4.50-4.75% in less than a year to fight inflation. The reason it was so fast was the Fed took too long to get started. Once they did, they had to move quickly to make up for lost time. The result was one of the fastest Fed Funds increases ever. They were increasing by 75 basis points each time for a while when 25 basis points is more the norm. Clearly there were come banks not ready for this. What was more of a direct impact to banks is the Fed’s quantitative easing which raised longer term rates like those found in residential mortgage loans and investment securities.

As an examiner, I recall spending a lot of time looking at interest rate risk. We required all banks to have complex models showing what would happen to capital and earnings if interest rates shifted up or down by 300 basis points (a basis point is 0.01%). Why these banks were allowed to take on this much risk is now a subject of debate and will almost certainly result in changes by the regulators.

What made the situation worse than in the past is how fast large depositors can move money now in the age of the internet. No more physically lining up. A few mouse clicks gets it done.

Silvergate went first and lost almost all of its deposits within a month or so. It was not taken over by the FDIC because it simply sold its investments at a loss to cover the withdrawals. That left little net worth, but no takeover because they had handled the run. SIVB went next. Their run was much faster. They apparently decided not to sell or borrow against their huge investment portfolio. They could have done either. But selling underwater securities results in a big loss and borrowing against securities yielding under 2% with borrowings costing close to 5% results in a steady stream of future losses. They froze for a day or two and that was enough for the State of California and FDIC to decide to take them over.

The next was Signature Bank which was taken over by the State of New York and transferred to the FDIC. Unlike the others, Signature did not have an unusually large portfolio of fixed rate investments and its loan base was more diverse. It did have a rapid decline in deposits tied to crypto currency, which were about 15% of their deposits. It also like SIVB had close to 90% of its deposits over the $250,000 FDIC insurance threshold. It probably would not have had its net worth wiped out if it sold investments and loans to meet deposit withdrawals. In my opinion the takeover of Signature was not only unnecessary, it caused a panic in the market place. It’s one thing to take over a bank with huge unrecognized losses in its investment portfolio and a massive concentration to one risky industry, but Signature was neither. They had essentially no loan relationships with crypto firms, just their money.

After the Signature takeover, all hell broke loose and the government (FDIC, Federal Reserve, State regulators) and the banking industry realized something had to be done quickly to stop the panic.

First Republic was next. Unlike the others, FRC is a traditional bank that just happens to have an unusually large portfolio of fixed rate residential mortgage loans. These loans are usually some of the safest a bank has from a credit risk perspective. But it had two strikes against it. One is it is located in the same local market as SIVB and the locals were scared. The second was their large mortgage loan portfolio was underwater value-wise now that interest rates had gone up. Panicked local investors (scared by SIVB) started a run. The FDIC this time did not take it over. Doing so would have been disastrous as First Republic is a traditional bank and doing so would have risked a contagion to the entire industry. The FDIC quickly decided that all deposits would be insured, not just those over $250,000. When that didn’t do the trick, a cash infusion was decided on by the banking industry. They sent FRC $30 billion in deposits to hold them over until things stabilized. The Federal Reserve also opened a new lower cost funding window to all banks.

Something like that is what should have happened with SIVB and SBNY to begin with, especially SBNY. I was a Bank Examiner in the late 1980s and early 1990s, which you may recall from the chart above was one of the worst periods of bank failures. The rule of thumb back then is the cost to tax payers is 5X when you take a bank over versus infusing capital and keeping it alive. As a result, the taxpayers paid over $100 billion to bailout the FDIC in that period.

In the 2007-2009 recession, the government took a radically different approach and FDIC did not need to be bailed out. They infused cash into all banks, primarily the healthier ones. This program called TARP was very politically unpopular and heavily criticized by both political parties. Yet in my opinion, it was the most successful government program I have ever seen. So, before you think I have fallen off my rocker let me explain. Can you think of another government program that completely succeeded in its mission AND made money too? The TARP program did what it intended to do, stabilize the financial system and actually made money because the infusions were preferred stock that paid interest and few went unpaid.

There is absolutely no need at this time to infuse money into every bank. But, infusing money into banks facing a run, that don’t have a lot of bad loans, selectively is the best approach to stabilizing the situation and protecting taxpayers. This time the banks themselves did it. My hope is that the government takes that function if needed.

How To Stop Bank Runs Going Forward

Below are the steps I believe should be taken going forward to stop the current risks to the financial system from bank runs.

- The Federal reserve needs to pause raising interest rates or indicate they are close to an end. I expect them to do at their next meeting. Their objective was to slow the economy in order to bring inflation under control. Once things start breaking, a recession is usually imminent. Things are breaking. Recessions almost always cool inflation. The interest rate risk that impacted SIVB and FRC gets reduced once rates start coming down/

- A fund, much smaller than TARP, should be established by the Treasury Department, Fed or FDIC to selectively infuse money into otherwise healthy banks when experiencing a deposit run.

- Interest rate risk and liquidity contingency planning should become new priorities for banks and bank examiners.

- Regional banks the size of SIVB, FRC and SBNY should be subject to the same stress tests as the major banks.

- I expect FRC to be sold or recapitalized as the run they just had has likely put their capital level below the regulators comfort level. Also, the 11 bank consortium that pumped in deposits will want their money back.

- Other banks facing pressure on their stocks such as WAL and PACW need to be defended in any way necessary. These are traditional banks that didn’t take abnormal interest rate risk, and suffer mainly for their physical proximity to SIVB.

Items 3 and 4 are already being discussed and the Federal Reserve is meeting about interest rate this week.

The Banking Industry Financials

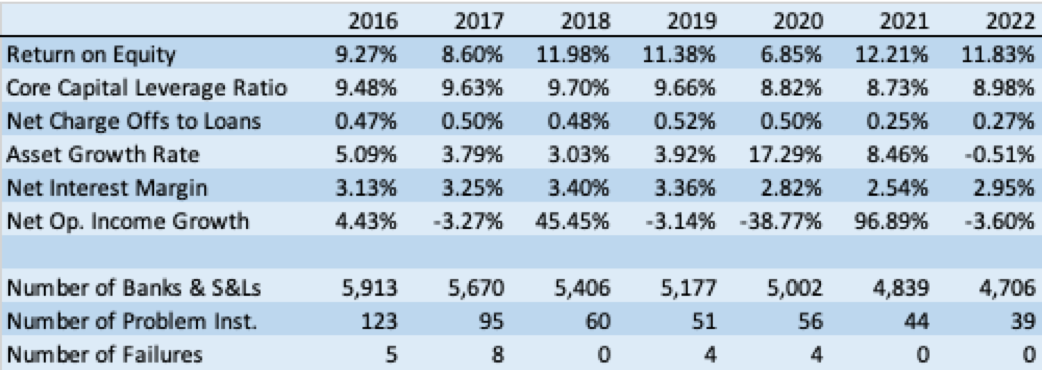

The chart below shows changes in the banking industry over the past 7 years.

{kind=link}

FDIC, author

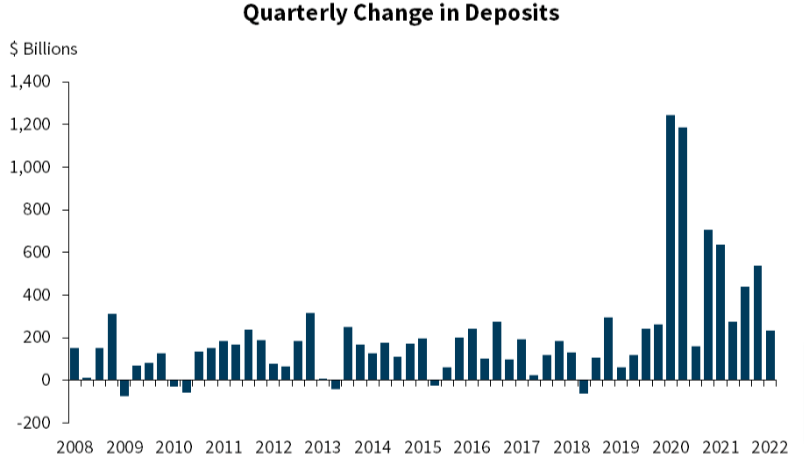

A number of things stand out in looking at this chart. The return on equity has increased in recent years. The year 2020 was an exception as banks built up a lot of loan loss provisions in anticipation of fallout from the Covid recession. The recession of 2020 turned out to be very short and excessive government stimulus far exceeded anything lost. The result was little damage and higher profits in 2021 and 2022 than they would have normally have had. The higher profits were due to asset growth and recovery of unneeded loss reserves. Charge off levels were normal in 2016 to 2020 but dropped considerably in 2021 and 2022 to historically low levels. This was also due to government stimulus, specifically PPP grants given directly to most smaller businesses and stimulus checks and higher unemployment insurance to individuals. There was unusually high asset growth in 2020. The chart below shows that was in part due to a surge in deposits resulting from all the government stimulus programs. New deposits get deployed into new assets. There have been few problem banks or bank failures in the last 7 years. It has been a strong period for banks until now.

{kind=link}

Finbold

What Happens Next For Banks

Outside of interest rate risk, the banking system is actually quite healthy with almost a record low level of bad loans and charge-offs. Bad loans have historically been the cause of most bank failures. Almost no banks have failed in recent years.

The banking industry also has much higher capital ratios than in the 2007-2009 recession. The ratio of capital to assets and capital to loans is much higher.

The largest banks are put through annual stress tests which includes liquidity.

The negative is I, and many others, expect a recession. The takeover of SIVB and SBNY, and the recent collapse of SI and FTX indicate things are breaking down. This usually happens right before or in the beginning of a recession. In a recession, the level of bad loans goes up. How many banks actually fail will depend on how bad the recession gets. I do not have a strong opinion on that, but expect a mild to moderate recession that drags on a while. I wrote an extensive article on this a few weeks ago.

What is particularly important is that any recessionary impact to banks is usually delayed. Remember at the top of this article I mentioned that most of the banks that failed due to the 2007-2009 recession failed in 2008-2012 with the peak being 2010. It takes a while for a loan to go bad after a recession starts. Most businesses and consumers have reserves they can use to keep paying for a while. Then there is a drawn out collection process before a loan is charged off or written down. Then there is the collateral repossession and sale process which can take well over a year if it is real estate.

What I am getting to is once the interest rate fueled bank runs stop, there should be a lull in the excitement. Banks are boring and that’s how they like it. But in 2024, if in a recession, we should see a much higher level of bad loans. It is usually difficult in normal times to see which banks have loose underwriting standards. It’s only in times of recession that as Warren Buffett famously said, we find out who is swimming naked. But there are some clues, these are below.

Risks to Look For in a Bank

If you are looking to invest in bank stocks here are some risks to look at, to account for the risks of a recession.

1. Level of risky assets – The riskiest primary loan types for banks in a recession are usually unsecured consumer loans including credit cards and construction and development loans. In this case I would add automobile loans due to a current price decline in the values of used cars. Look for concentrations in these areas.

2. Track record – Many of the largest banks were hit hard in the 2007-2009 recession, especially Citicorp, Bank of America, and Ally. Regional and community banks on average fared a little better but many did go under. I provided a list of how 102 community banks did in the 2007-2009 recession in this article.

3. Concentrations by industry - Banks that have a large amount of loans to a riskier industry such as oil and gas, venture capital (SVB Bank is an example there), and newer technology companies should be avoided. In real estate I recommend avoiding those with high concentrations to office buildings and retail buildings which both face large secular headwinds.

4. Current level of delinquencies - We have had a strong economic expansion for years, and most banks have few bad loans. Those that have a higher than average level indicate they are likely to be harder hit due to looser underwriting standards or riskier loan types.

5. Rapid Growth – Historically those banks growing the fastest are most at risk. They tend to take more risk or underprice to take loans away from competitors. Also, their loan portfolio has less age to it. Loans do better as they age. SIVB, SBNY and SI were all growing well in excess of the industry norm.

6. Capital level - Most banks have a significantly higher level of capital to assets than they did going into the 2007-2009 recession. This gives them a bigger cushion to absorb losses. An average level banks is around 9% capital to assets. Be careful with those significantly below that, though there are relatively few. Deduct intangible assets when looking at capital.

7. Geography - Banks in places like Texas, Oklahoma, Louisiana and the Dakotas will suffer if oil and gas prices drop and stay down a while, even if they have no direct loans to companies in that industry. California is highly tied to the tech industry, especially in the Bay area.

8. High Interest Rates on Assets – As of December 31, 2022, the average yield on banks earning assets was 4.54%. These assets include lower yielding investment securities. If the bank you are looking at has an average asset yield of over 5.50% they are probably making riskier loans. A higher rate is needed to compensate for higher risk.

9. Search FDIC Enforcement Actions – You can actually see what the FDIC and other regulatory agencies are doing at their websites. The FDIC’s is here FDIC: Previous Press Releases If you type the bank’s name into the search bar past FDIC activity comes up.

Takeaway

I expect the interest rate risk bank run crisis to die down assuming no policy mistakes by the government. They already have made some so that is not a given. The next phase is a surge in problem loans that usually occurs in a recession. It is difficult to tell which banks were loose with their underwriting but please look at my 9 factors for what we can look for. We’re still probably a year away from problem loans getting quite high, if they do at all. That means there will be a lull in the excitement. But if a recession appears imminent or upon us, look for lower earnings as banks build up their loss reserves. Earnings should also stall or fall as they were artificially inflated by excessive stimulus and loss reserve recoveries in 2021 and 2022. Earnings may also hurt by increased regulation.

Interestingly, media reporting has the big banks as the safest (including Barron’s cover this week). That was not the case in the 2007-2009 recession as Citi, Wachovia, Ally and Bank of America all struggled mightily. The largest banks are involved in riskier activities such as derivatives, international banking and credit cards. But they have much higher capital levels now and have been put through annual stress tests. They also have less interest rate risk than other banks. Further, they are also too big to fail, though that doesn’t help shareholders.

My overall recommendation for the industry is hold for investors and speculative buy for traders. Investors should weed out banks that are riskier based on my 9 factors to look for. Valuations have come down considerably and the stocks may rally in the near term as problem loans are still quite low once the bank runs stop. But we are facing the usual recessionary headwinds of significantly higher bad loans probably starting in the first half of 2024 and lower earnings going forward.

For further details see:

An Insider's Guide To The Banking Industry Amongst The Turmoil