MFC - An Update On Legal & General: It's Still Attractive

Summary

- I've written about Legal & General Group Plc a few times in the past, and own a small stake in the UK-based insurance company, which is mostly in the L&H segment.

- To call the stock historically stable in terms of price would be going too far. There's plenty of volatility to Legal & General Group Plc, and the company has outperformed broader markets.

- However, at the right valuation, most qualitative companies become buyable, and Legal & General Group Plc is qualitative in my book.

- Here's my 2023 update on Legal & General Group Plc.

Dear readers/followers,

I've been following Legal & General Group Plc ( LGGNF ) a few times over the past few years, both privately on our marketplace iREIT on Alpha, but also on the general Seeking Alpha site. Part of the argument for investing in Legal & General is the impressive yield that the company pays. Provided that you don't overpay, this yield provides a very nice cushion against volatility and should, at least in theory, prevent you from losing money or underperforming the market too badly.

So it was during the past few months, though I bought my shares in Legal & General Group Plc at generally attractive prices, that it has given us returns of 4.23%, in a time when the market is down over 2% - hence, outperformance - if a small one.

Seeking Alpha Legal & General Group (Seeking Alpha Legal & General Group)

In this article, I'm updating my general case for and against the company for 2023. Legal & General is perhaps not the most qualitative of insurance stocks - but it's conservative and safe all the same.

Let's look at what's in store for this year.

Legal & General Group - The case for investing in 2023

Legal & General Group Plc, hereafter called L&G, is a British-based multinational financial service and asset management company. The company has been through substantial changes and corporate adjustments for the past couple of years, which has resulted in the company having both investment management with lifetime mortgages, pensions, annuities, and life insurance. LGIM, the company's investment management arm, is the 10th-largest in the world and the second-largest in all of Europe.

L&G is the biggest provider of life insurance in the UK. After leaving non-core markets, the company's focus is organic growth in life insurance and products, as well as growth in the investment business, with a focus on the U.S., UK, China, and Japan, as well as providing insurance coverage in India.

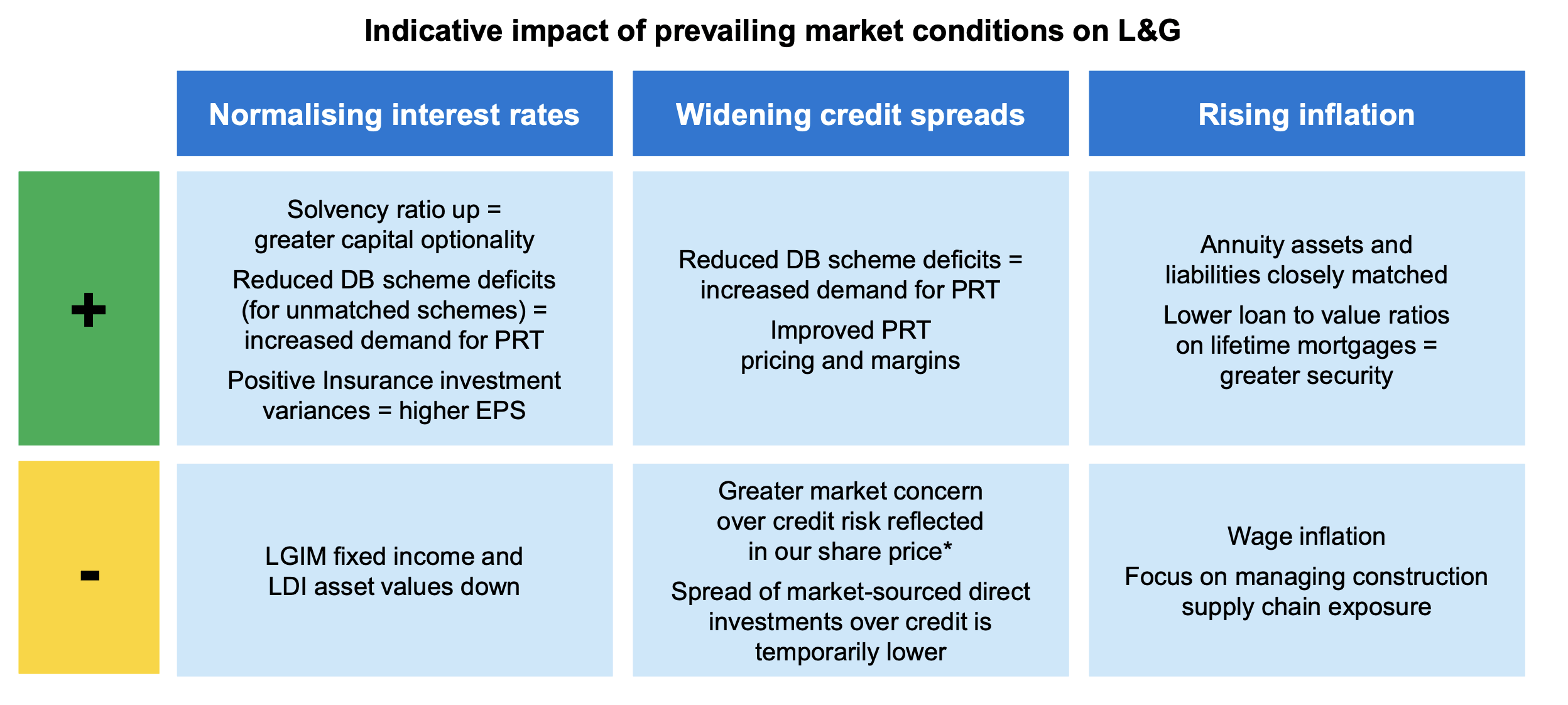

The company's business idea is to maximize the synergies between these various operations, using its various segments to increase its assets while de-risking its pension assets. This has become much more difficult as interest rates fell, and is becoming somewhat easier now that rates are on the rise, and as it has moved away from equity investments.

The company is now one of the major players in lifetime mortgages, with a market share of nearly 25% in the UK. Additionally, the company continues to grow in individual annuities.

As I've said, the company's challenges like any finance company, related to low interest, will likely fade as the interest rates reverse, which they are currently doing. This will, and has resulted in interest-related income growth. This will not eliminate, and likely not completely weigh up performance-based returns in a down-market cycle, but it will cushion the blow and lend some stability to earnings results. The danger is fund outflows due to the bear market, which would enhance the poor performance here.

The company is, in part, a play on how strong synergies the company can develop between its retirement/investment/capital arms, its insurance operations, and other areas while managing the highly competitive home markets in the UK.

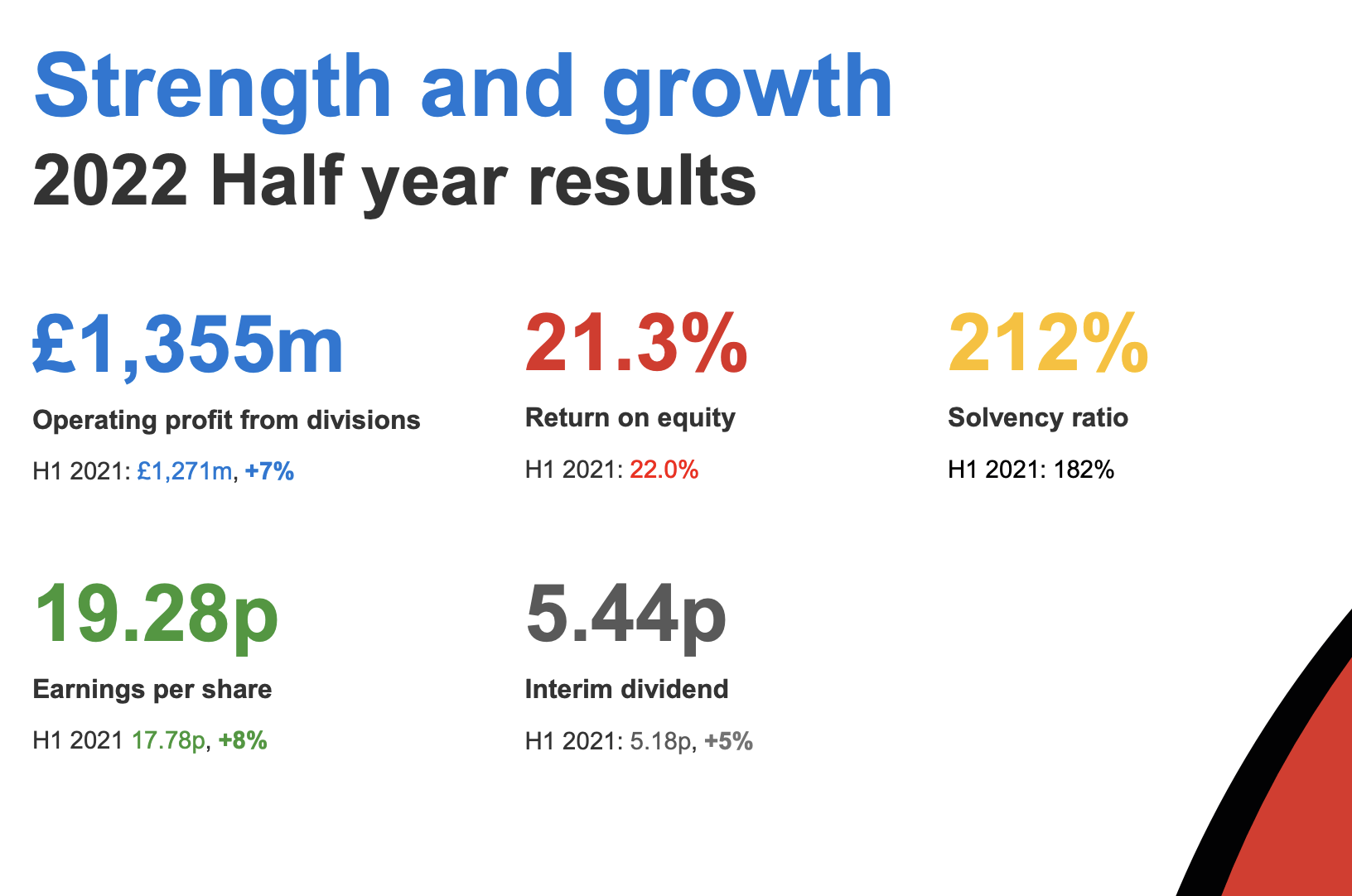

The latest results for L&G are the half-year results. Like many companies in Europe in this segment, L&G keeps quarterly result reports to a minimum, leaving us analysts to work with the half-year numbers and work from estimates, forecasts, models, and guesswork outside of this.

Company results for the half-year period were nonetheless solid. The company grew operating profit, earnings, dividend, a good RoE, and excellent solvency for the type of operation that L&G is.

{kind=link}

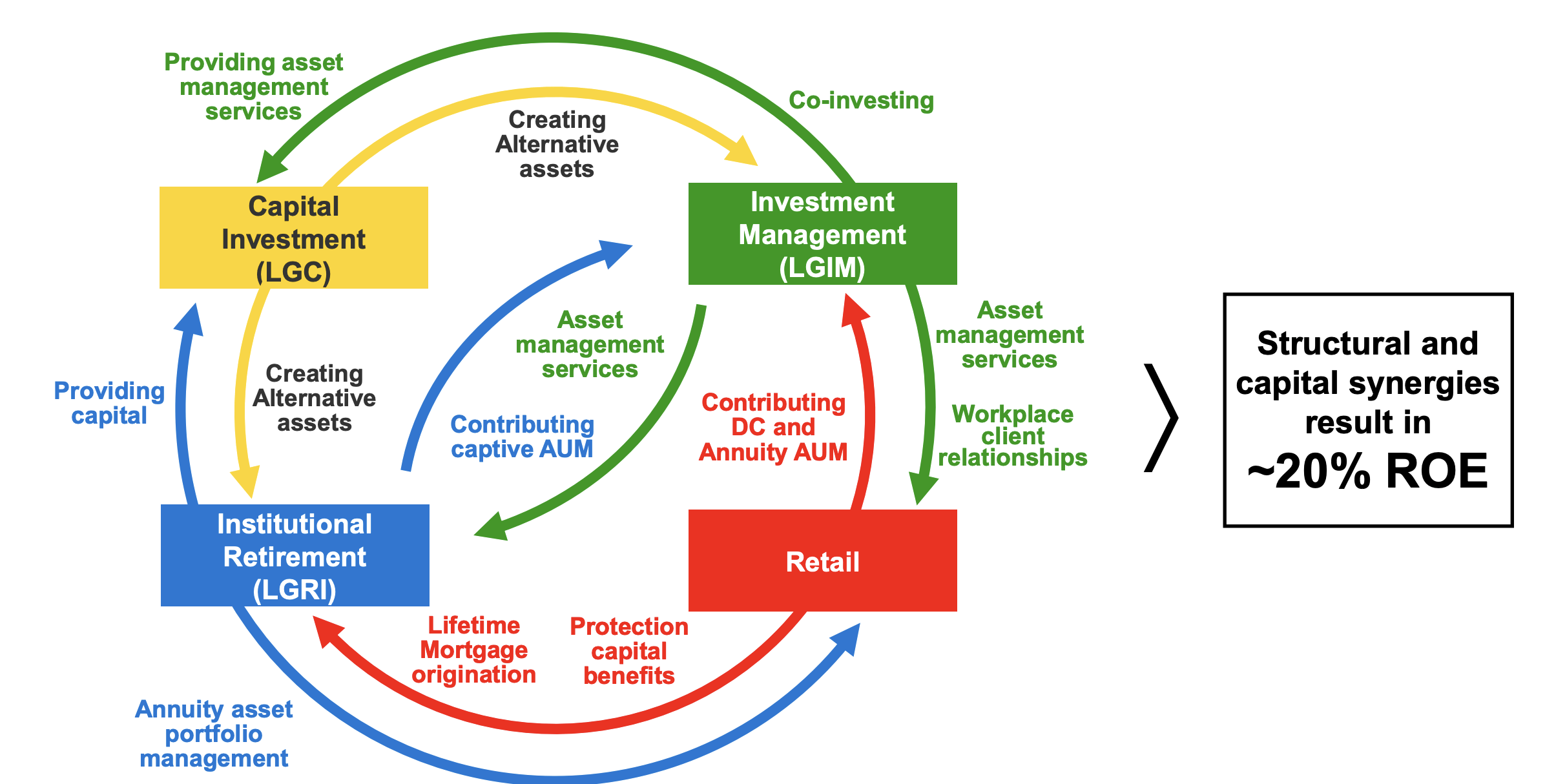

Currently L&G consists of four appealing divisions - asset origination, management, Retirement solution, and Retirement & Protection solutions, where the former solutions work with Risk transfers and multi-national management.

The company works in the full "cycle," which gives L&G access to impressive synergies from the various segments, flowing from asset management, to providing capital, to working with various originations, to the creation of assets, to Retail.

{kind=link}

The company, aside from being a play on synergies, is a play on fundamentals across the western world, including the aging demographics, the globalization of management, investing in welfare reforms, and if you like, addressing climate change and ESG topics through all of the company's divisions. There's really no fundamental argument to be made against the company being able to manage today's market and how the current trends develop.

{kind=link}

L&G, as I see it, is very much a macro sort of play. While micro and national trends will see some impacts across the company's various sectors, this is mostly about macro here, with a wide variety of coverage across multiple fields in various protection, mortgage services, savings, and retirement. Risks include, as with most insurance players, things like write-downs and poor shorter-term performance as well as longer-term due to the volatility. The company's 5-year performance for shareholders can actually be called "poor." Returns are negative, and shareholders have actually lost 10% of their invested capital, despite what can be called great results.

So valuation is absolutely key when buying - also, it's worth knowing that in buying L&G, you're essentially buying into the UK, which is something I'm very careful about since the company left the EU. Far from being a net positive, so far things have gone decidedly negative for the nation, both economically, in terms of imports/exports, and in terms of the UK as the basis for production/manufacture and London as a financial service center.

In addition, the company's reliance on the UK as a market for more than 85% of its current pre-tax profits isn't exactly an advantage. Other companies, including Allianz ( OTCPK:ALIZY ) and Munich Re ( OTCPK:MURGY ) or AXA ( OTCQX:AXAHY ), have home-market advantages, but lower overall exposure to one national market.

That is why my exposure to L&G is still relatively limited, while I have a much larger position in all of the above-mentioned companies.

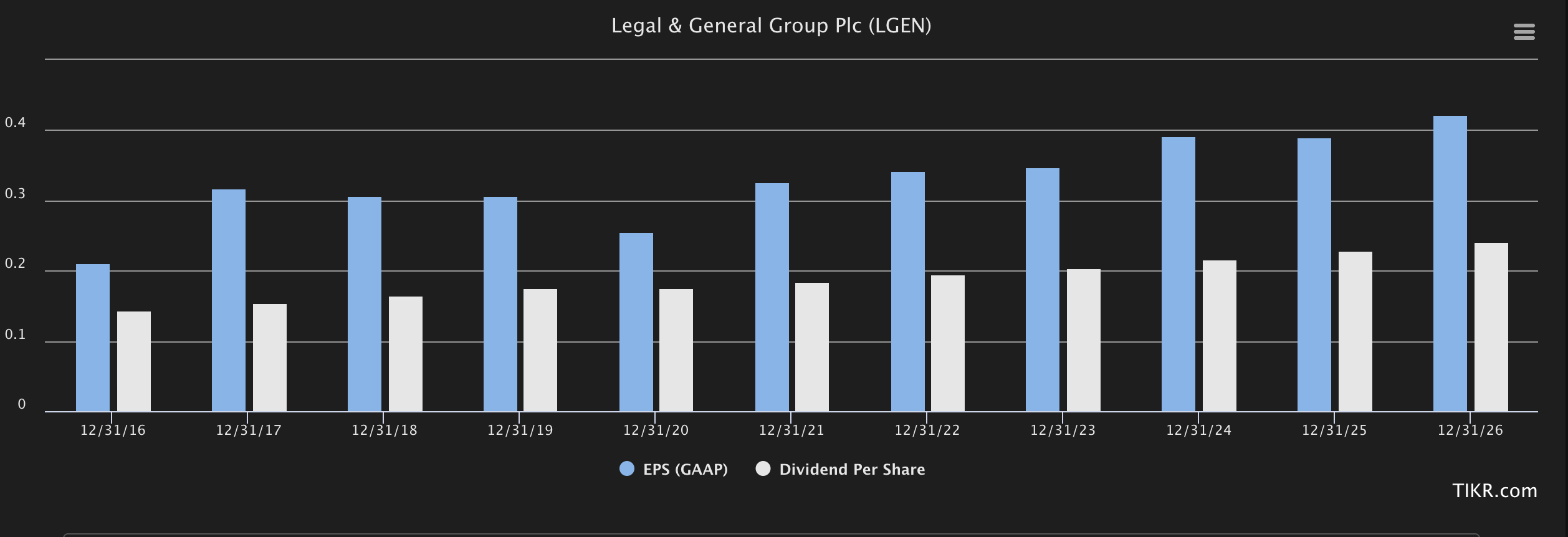

However, I want to clearly state that recent trends are very much positive. I also see further upside based on the company's expected growth for the next few years. While somewhat lumpy, the company's expected earnings nonetheless show a growth trajectory, with dividends growing right alongside it.

Legal & General Profit/Dividend (TIKR.com)

{kind=link}

And while other risks like its Russia exposure might have some potential to drive earnings and revenues lower, I view these as temporary, due to the company's high UK exposure. The UK might not be the massively growing economy and safe haven of finance it once was, but it's still an economic powerhouse that can be relied upon in many areas, with a large population that requires the services the UK offers. And while the GBP is far from a reserve currency, it nonetheless maintains an attractive status across the world.

These macro trends are what I look at for L&G. And in terms of higher-level results, I see very few worries. L&G is well-capitalized, and its hits both analysts and its own targets. The company's solvency is up over 20% in less than half a year, and despite market trends, its annuity portfolios have seen no defaults, with 100% of scheduled cash flows paid.

Let's look at what this does with the company's valuation, and where we should expect it to trade for 2023.

Legal & General Valuation - still attractive, despite small outperformance

The company's native share trades at £2.6 per share. The average targets from the 16 analysts from S&P Global following the stock come to a range of £2.4 on the low side to £4 on the high side, with 10 of these analysts currently considering the company an attractive, potential "BUY." The average from this range is around £3.12, implying an attractive upside of 20.4% despite outperforming when the company traded closer to £2.1 back when I loaded up the second time in September.

It should not be a surprise to you, based on recent dips, that I retain my stance that's generally more aligned with the bullish view on L&G. However, I'm still not as bullish as some analysts are.

Until the recent drop when the company dipped from $18-$21/share for the ADR, I held a fairly somber view of the company's prospect, assuming an 8-12% annualized RoR at best.

If we look at the company's closest overall peers, L&G still remains undervalued. The competition includes Manulife ( MFC ), Swiss Re, Metlife ( MET ), and other insurance players - and in terms of overall P/E, none of the company's peers here trades at lower multiples than L&G, which is currently at a native NTM P/E of 7.62x. The closest would be China Life, at 7.68x, and Manulife at 7.71x. I don't know China life all that well, but I would also consider Manulife undervalued.

The appeal of L&G remains its high and covered yield, as well as its potential for climbing higher towards the £3 mark to align more closely with its non-UK peers, most of which trade at double digits, and some of which trade over 18x.

Because of the UK risk, I don't believe such normalization and trends to be entirely possible here - but I do believe the company can go higher. Much as in my previous article, I'm bullish - just not "as" bullish as most of my colleagues.

Looking at Embedded value for the company at a WACC of 9% comes to around £3.1/share, bringing the company again, to an undervaluation here of around 15-20% depending on the exact level of valuation. I've impaired the valuation a bit more to account for somewhat higher costs and market risks. However, NAV remains perhaps the more interesting segment. I was previously unwilling to go higher than 10x natively for L&G, and I remain this. This now comes to around £3.05 normalized.

I'm still ready here to clearly state that the company is undervalued in every metric here. Every single metric we're looking at is giving us an upside either on historical metrics, peer metrics, analyst averages, or NAV averages, of at least 10% and as high as 22% - and this is conservative.

So, I still think that L&G is one of the better-valued insurance plays out there in Europe. It's not as though "cheap insurance" is rare here, though - there are plenty of companies that trade at low multiples compared to where they could be.

However, with Allianz climbing above €220, AXA stabilizing as well, and Europe overall seeing more positives, we can state here that the relative appeal of L&G has in fact increased. Legal & General is a great investment at this valuation.

This is my current thesis for the company.

Thesis

- Legal and General is a great UK-focused insurance and retirement protection/asset management shop, one of the largest on earth, and one of the most significant in all of the United Kingdom. At the right valuation, this company becomes a strong contender for being able to generate 6-8% simply from the company's well-covered dividend, together with more upside from normalization.

- We've seen the company drop to appealing levels over the past few months, and even with the normalization since September, the company remains attractive at below £2.5/share.

- I rate L&G a "BUY" with an adjusted PT of £3/share for the native.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Legal & General Group Plc fulfills all of my fundamental requirements at this time, and it's therefore a "BUY."

For further details see:

An Update On Legal & General: It's Still Attractive