ALNPF - ANA Holdings: A Challenging Airline Recovery Profile

2023-08-15 15:32:39 ET

Summary

- All Nippon Airways (ANA) reported revenue growth of 33% and cost growth of 19% in its most recent quarterly report.

- The international cargo business saw a decline in capacity and unit revenue, leading to a 60% decrease in revenues.

- ANA faces risks from weak cargo and mail revenues, as well as potential softening in unit revenues for passenger services.

The investment thesis for airlines remains a challenging one as higher input costs have limited the ability for airlines to meaningfully reduce unit costs. North American carriers have been spearheading the recovery with strong demand in the domestic market. The recovery sequence, however, at this point also makes it interesting to look at airlines in other regions. Asian airlines have been subject to COVID measures for a long time, limiting their ability to recover. With those measures easing or even completely lifted, we see revival of demand on routes to and from Asia as well as on the domestic markets in Asian countries. In this report, I will be discussing the most recent results for All Nippon Airways.

Revenue Growth Outpaces Cost Growth

{kind=link}

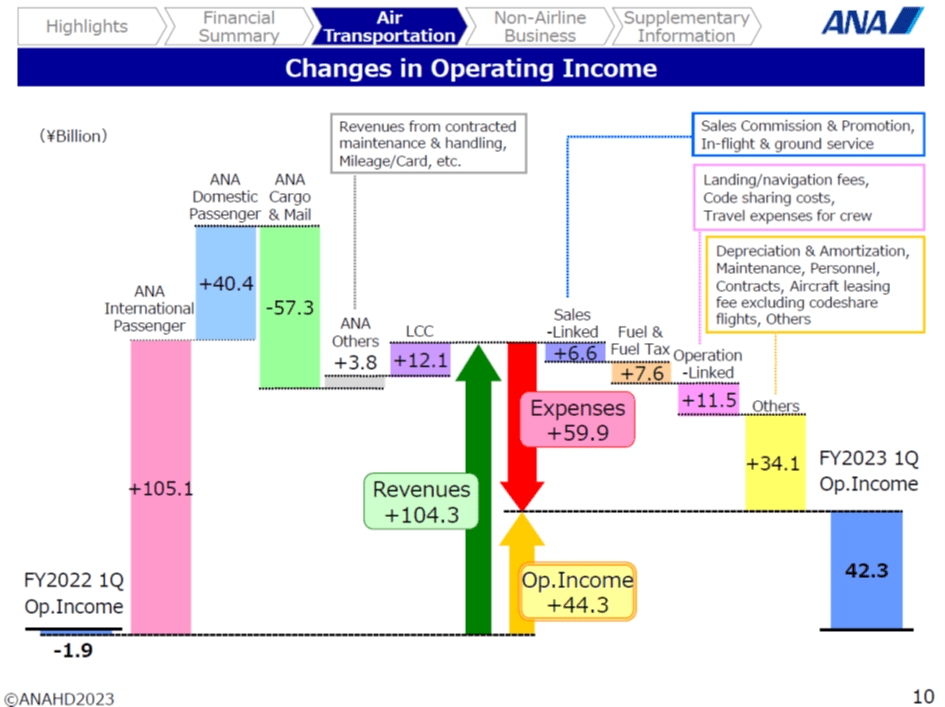

When analyzing company results, one thing I do pay attention to is how management presents the results. When management is able to clearly and concisely discuss and visually present results, it gives a better impression of management’s insights in the company’s performance. The slide above shows exactly that with all moving pieces during the quarter. The airline business saw its revenues increase by 33% while costs increased 19%. That's quite a favorable growth composition.

Between the operating segments, however, there was quite some variance in the performance. The International cargo business saw 4% lower capacity during the quarter, a 13.8 pts contraction in load factor and a 58% decline in unit revenue leading to 60% lower revenues while on the domestic market capacity increased 38%, load factors declined by almost 7 percentage points and unit revenue declined by 35%.

Overall Cargo and Mail revenues declined by 56% as airlines have brought more capacity to the market removing the boosting factor for unit revenues while consumer spending is somewhat pressured due to inflation and changing spending patterns for the time being. Important to keep in mind is that the reduction in cargo revenues has been so big that it fully offset LCC and domestic passenger revenue growth. Domestic passenger capacity grew by 21.1% and with load factors improving to 66.9% from 54% and 15.3% higher unit revenues, we saw passenger revenues improve by nearly 40%. Peach Aviation, which represents the LCC operations, saw 10% capacity growth and strong load factors of 84% up from 67% a year earlier with unit revenues up 62.2% leading to a nearly 80% increase in revenues.

The big growth item was the international passenger service where capacity doubled and revenues increased by nearly 170% aided by a 33% increase in unit revenues. Looking at the revenues by segment in the slide above, we do see that it was basically international expansion that led the way.

The Risks and Opportunities For All Nippon Airways

Pre-pandemic, shares of ANA Holdings (ALNPY) were trading roughly 45% higher than today. Based on the fact that capacity is not fully recovered, one would think that significant upside remains and that could indeed be the case. However, I'm also somewhat cautious about further recovery prospects. Cargo revenues are likely to decline further and we already saw the decline in cargo revenues absorb the growth in domestic and low-cost carrier revenues.

On the international network, the capacity is 73% recovered with revenues slightly above 2019 levels and one can wonder how strong the unit revenues will remain as international carriers are also adding capacity. So, there's a risk that recovery the capacity toward 100% will not fully translate to the top line as unit revenues might weaken. Domestic capacity is more than 90% recovered but passenger revenues are only 85%. So there's some domestic recovery runway ahead but unit revenues are in fact weaker than pre-pandemic on the domestic network.

So, the big risk I see for ANA’s business is the weakness in cargo and mail and some softening in unit revenues for passenger services. For the cargo revenues, ANA expects demand revival in the second half of the year. Simultaneously, the company expects yield pressure on international passenger operations in the second half of the year while domestic business will recover to 80%. There are, however, also opportunities such the ban on group visa being lifted which could result in a flow of Chinese tourists into Japan.

Conclusion: A Challenging Recovery Outlook

All Nippon Airways or ANA Holdings has seen a significant improvement in its financial results, but the big question is whether the strong demand environment will outlast the weakening in for instance cargo revenues. Cargo revenues could be under pressure until 2025 while the domestic passenger network is already under pressure and the yields on the international passenger network are expected to weaken in the second half of the financial year. As a result, I don’t consider ANA Holdings stock as a compelling investment.

For further details see:

ANA Holdings: A Challenging Airline Recovery Profile