ANGI - Angi Inc.: More Risk Than Reward

2023-05-25 11:05:43 ET

Summary

- ANGI's fundamentals have suffered due to underperforming growth initiatives.

- The new management team aims to improve profitability, but there are concerns about ANGI's poor execution track record and a potential macro slowdown in the home repair industry.

- Lack of key catalysts and overvaluation lead to a neutral rating, with higher risk than reward on the stock.

Angi (ANGI) is an online marketplace that connects homeowners with local service professionals. It offers a platform where homeowners can find and hire professionals for various services such as home improvement, repairs, cleaning, and maintenance.

The business has been through ups and downs since my previous coverage in 2020, where the stock traded at ~$7 per share and I suggested that the business would be facing significant competition from well-funded tech giants like Facebook (META) and Amazon (AMZN).

The stock reached above $16/share in early 2021, when Oisin Hanrahan, who earlier co-founded Handy, a home cleaning service startup acquired by ANGI, took over as CEO. However, the core business performance has been underwhelming since then, while many new initiatives failed to take off successfully, negatively impacting the bottom line.

Hanrahan stepped down in Q4 2022, and the IAC’s CEO Joey Levin, took over as CEO and initiated a turnaround plan - to rationally reassess all of ANGI's business initiatives to emphasize customer lifetime value :

Yes. The only thing I'd just add further to that is the way we're talking about internally, the folks on the Angi team is, I've said to everybody, I want to turn off revenue that is not going to be good for our customer experience and long-term customer relationships. If we're building lifelong customers, let's build the lifelong customers and make that healthy. We've got room on profit to do that. And I want to prioritize the customer experience over revenue right now.

Today, the stock trades at +$3 per share. My assessment of ANGI today suggests that the business is still facing a lot of risks as it undergoes the turnaround plan, while the upside potential remains limited. I maintain a neutral rating for the stock.

Risk

ANGI has struggled with poor strategic decisions and execution, and the recent CEO departure may increase the risk of them repeating in the future. In recent times, the management has failed to scale various initiatives within the Services and membership businesses effectively. Overall, they have impacted profitability and put pressure on the shares' performance.

{kind=link}

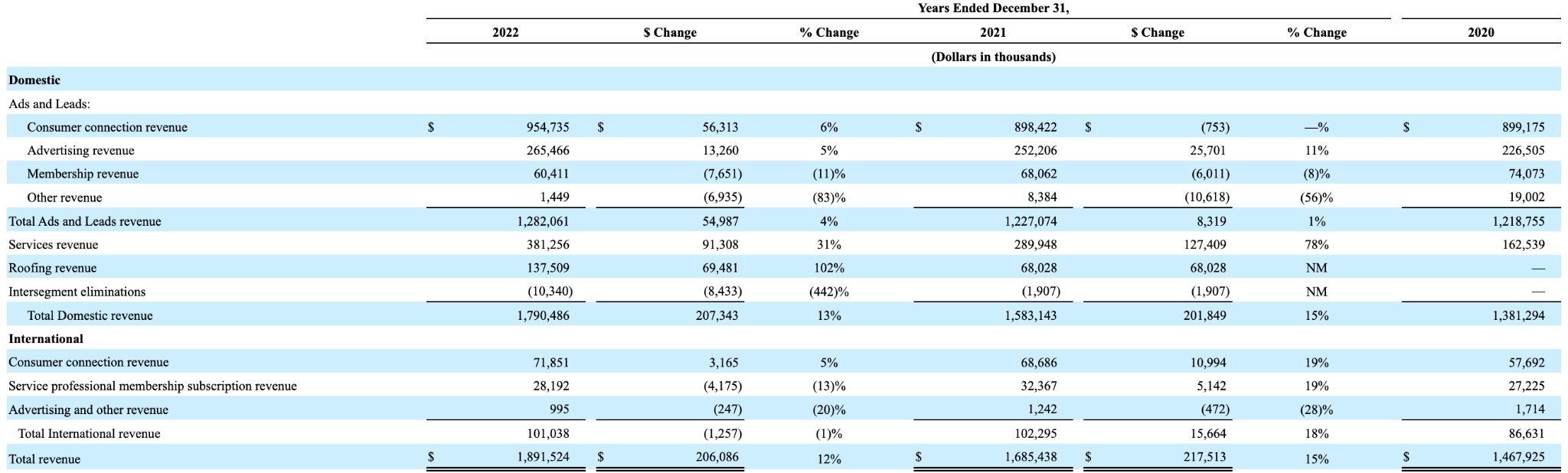

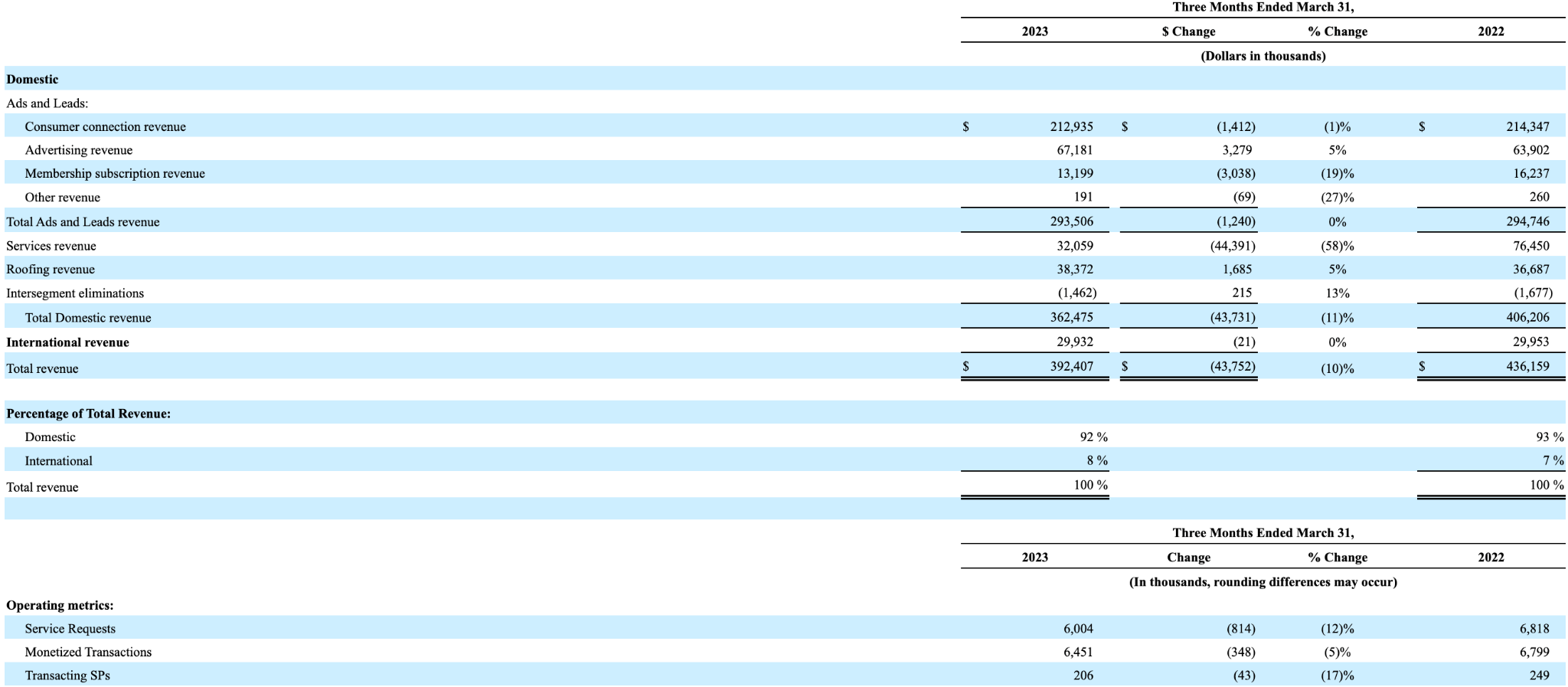

In 2021, the then-new CEO, Oisin Hanrahan, launched a new "Angi Key" membership program for ~$30 per year which targeted the homeowners to unlock exclusive discounts. This is a new program that replaced the older tiered membership program offered under Angie's List - former name of the company. Things did not seem to go according to the plan, since membership revenue experienced an 11% decline in 2022, and then a sharper 19% decline in Q1 2023.

{kind=link}

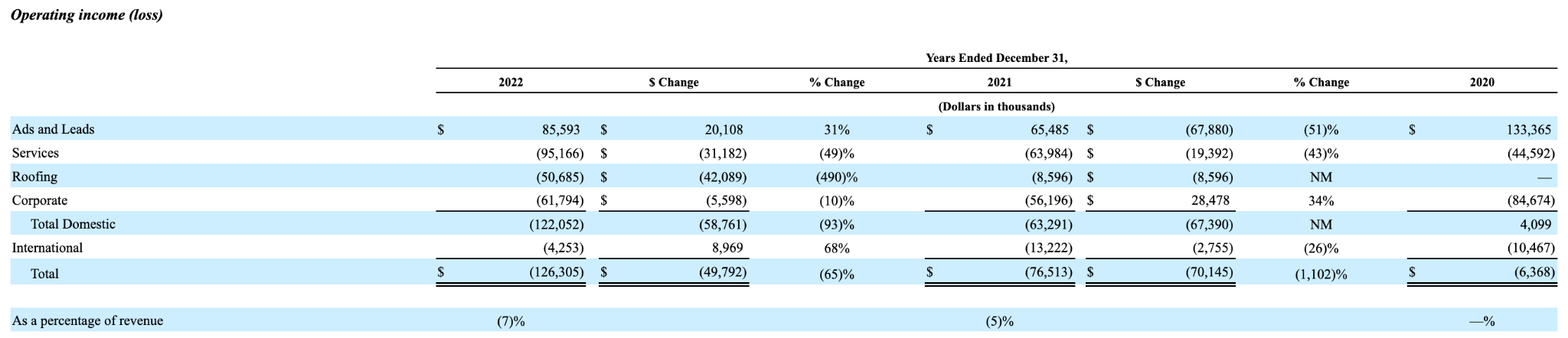

Aside from the core ads and leads business (which also includes the membership business that contributes a small portion of revenue), all of the other businesses have generated operating losses. Services business, for instance, has not been profitable. In fact, half of the increase in the cost of sales in 2022 was due to Services. In general, there is always a fundamental challenge of matching home services/repair requests to professionals, which often adds an extra layer of operational work - higher average order/request value may entail higher revenue potential, but it may also mean higher level of complexity. In Q4 2022 earnings call, the management suggested that a particular higher-average-order value "complex services" category has significantly impacted Services business' profitability, and in Q1 2023, ANGI made the decision to remove that particular category.

Furthermore, ANGI's entry into the more traditional roofing repair business does not seem to be a move that was well thought through and also gives a sense of a lack of direction. While the rationale behind the move was probably to establish a vertical integration between the online service marketplace and the roofing professional supply base for higher margins, ANGI is an inexperienced player in the roofing business. In the last two fiscal years, roofing business suffered operating losses , and in Q1 2023, the new CEO Joey Levin suggested that the management still had not yet figured out a future plan for the business even after it turned profitable.

Although the management hasn't provided much commentary on how the macro slowdown is affecting the business specifically, it appears that there has also been a bit of a macro slowdown affecting ANGI's business since the back half of 2022.

{kind=link}

We can observe weakness in operating metrics that may imply declining demand in 2022, when the 4% YoY growth in ads and leads revenue in that FY was mostly driven by price increase instead of volume. Operating metrics have been in decline since 2020, though, most likely due to the poor executions.

{kind=link}

In Q1 2023, the decline across the operating metrics was even much sharper than in FY 2022. The significant 17% drop in the number of transacting SPs / Service Professionals, which is the key revenue driver of the business, should be a red flag, if any. With the ads and leads revenue also declining by 1%, it seems that the price increase approach from FY 2022 may have turned many SPs away.

Furthermore, I think that the decline in the annual membership revenue may also be a leading indicator of an incoming slowdown for the home repair business since it means that fewer homeowners are considering doing home repairs in the future regardless of discounts and offers.

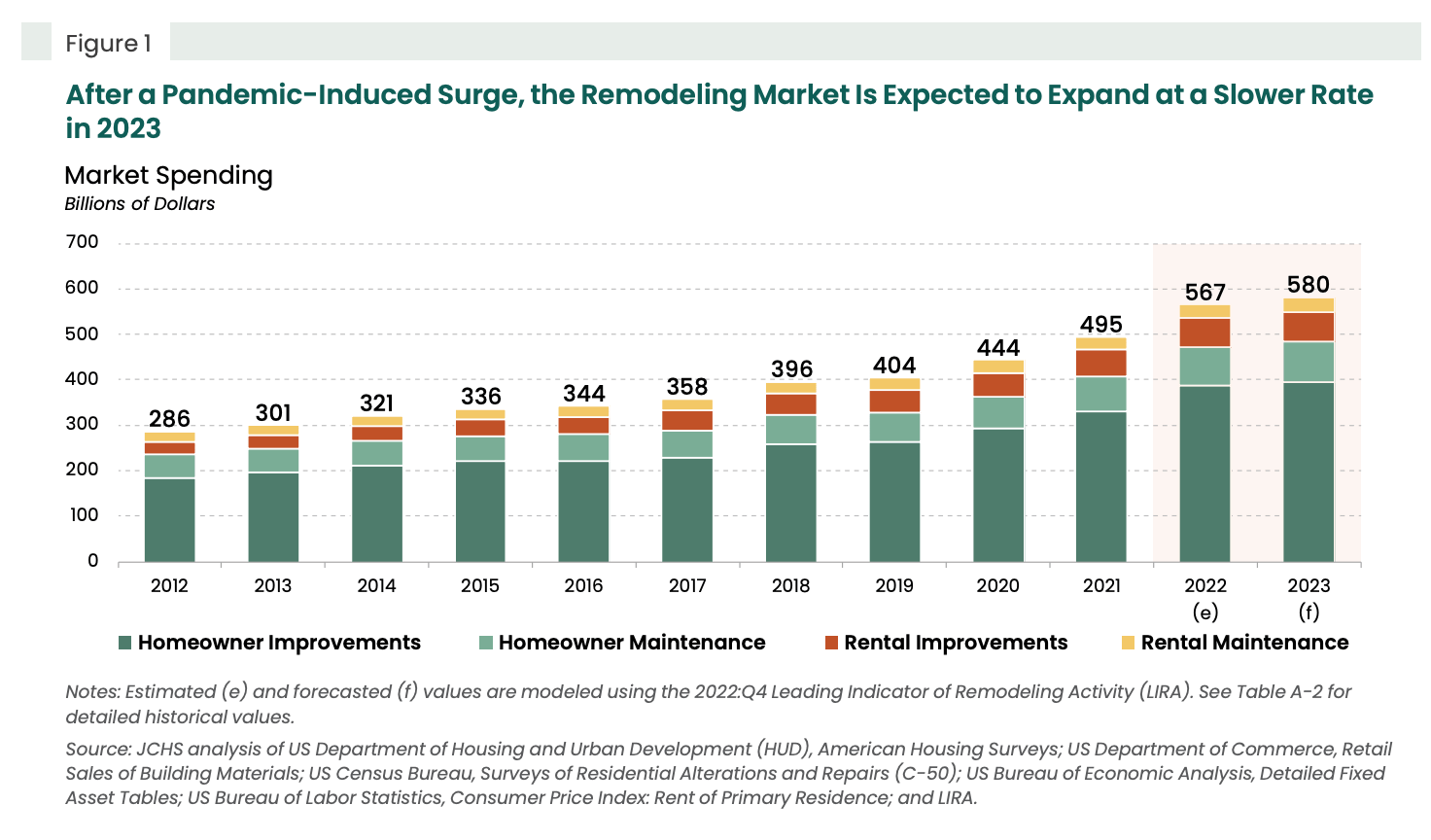

Joint Center for Housing Studies of Harvard University

{kind=link}

Based on the recent study by Joint Center for Housing Studies of Harvard University, the home improvement market is indeed projected to expand slower in FY 2023 , indicating that the slowdown may persist at least until the end of the year.

To some extent, the launch of the new ANGI Key membership business also demonstrates a weak business portfolio strategy by the management. While the intention behind the membership business was probably to create revenue predictability and reduce cyclicality, membership cancellations are likely to increase anyway during recessions. Nonetheless, over the last two FYs, the membership business has not done anything meaningful to support the ads and leads business.

Catalyst

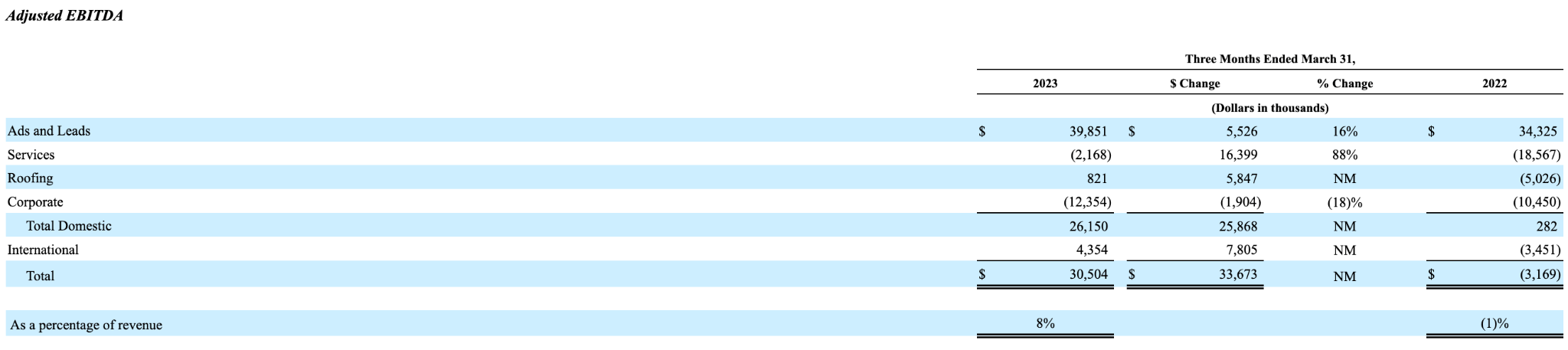

At present, I cannot identify any meaningful catalyst on the stock, though I believe that focusing on the bottom line would be the best option for ANGI at this time, and on that front, it seems that the current management is on the right track. The improvement in adjusted EBITDA from -1% in Q1 2022 to 8% in Q1 2023 is a positive sign. It appears to have brought in more confidence in the market. Today, shares are up ~17% since the Q1 earnings results announcement on May 10.

{kind=link}

With the management's commitment to capturing more margins and identifying areas for scalability, I would expect that further improvement can be achieved, although it may happen at a gradual pace. The new management was surprisingly successful in making roofing business profitable in Q1, and given the narrowing adjusted EBITDA loss in Services, the segment may not be too far away from breakeven. In that sense, there is a possibility that the overall adjusted EBITDA margin expands in Q2, boosting more confidence and creating higher demand for the stock, driving the shares price up.

Valuation / Pricing

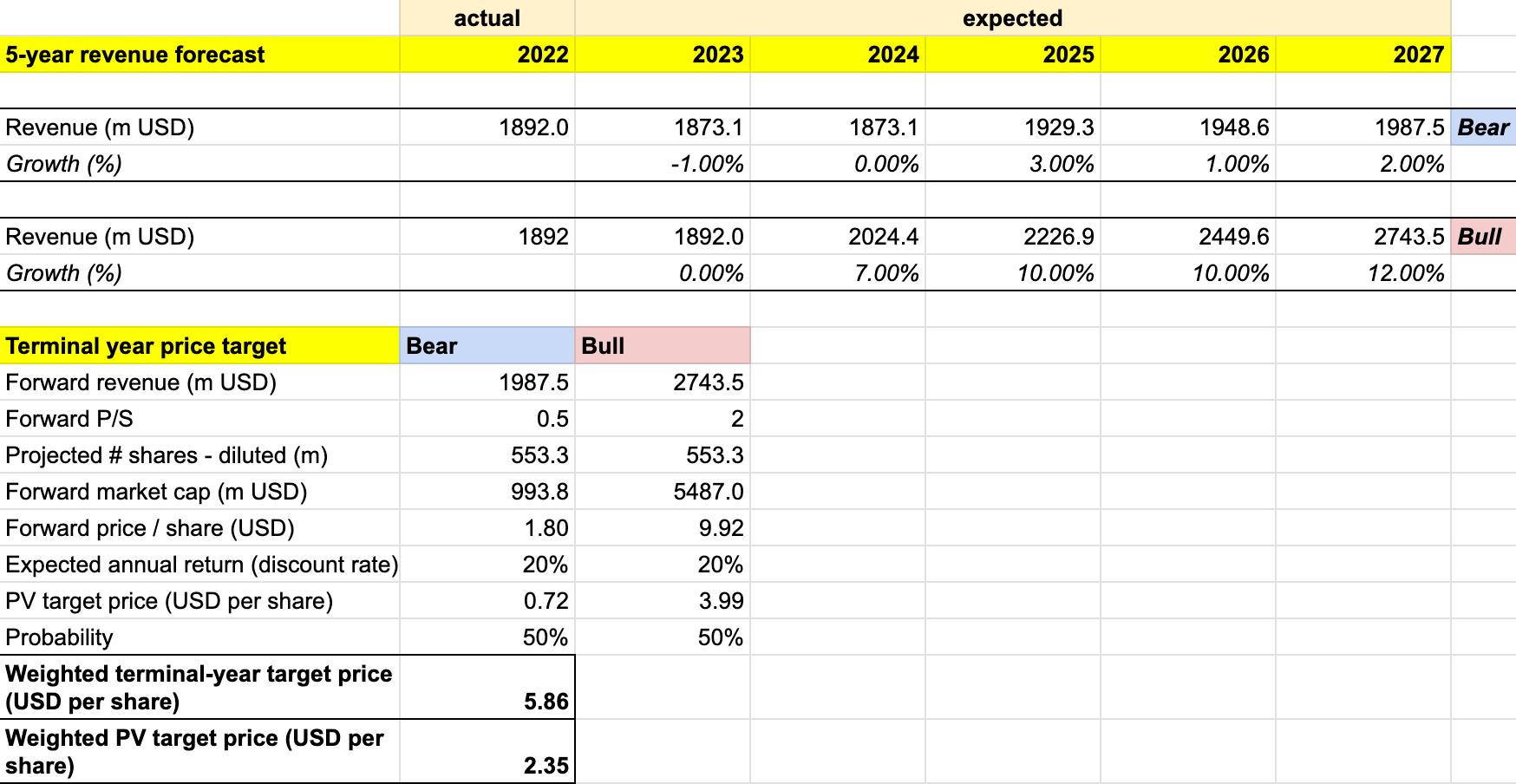

My target price for ANGI is driven by the bull vs bear scenarios of my 5-year revenue forecast below. I would also highlight that my revenue projection also accounts for the adjustment in the revenue recognition for the Services business , which will report revenue on a net, instead of gross basis, from FY 2023 onwards:

- Bull scenario (50% probability) - ANGI to see a relatively successful bottom-line improvement that sees adjusted EBITDA margin expands in FY 2023, at the expense of a flat YoY growth. ANGI will then see revenue growing at 7% in FY 2024, which then reaccelerates to 10% to 12% in FY 2027, driven primarily by a mix of organic/M&A-based growth strategy from the core ads and leads business, bolstered by a potential acquisition of another marketplace competitor sometime before FY 2027. This would be a similar move to the Handy acquisition in 2018. I expect a positive and steady EBITDA between FY 2025 - FY 2027, reflecting a similar outlook to 2018 - 2021. I assign a P/S of 2x for ANGI under the scenario, considering ANGI trading at a ~4x P/S between 2018 and 2021 with higher profitability and growth outlook than the FY 2027 bull scenario.

- Bear scenario (50% probability) - ANGI to see revenue decline by 1% in FY 2023 as it is unable to counterbalance the negative impact of weakening operating metrics and macro slowdown. The difficulty continues in FY 2024, where the growth remains flat. Starting in FY 2025, ANGI to see a slight revenue reacceleration, driven by its core ads and leads business, but to also see a continuing decline of the membership and international business. ANGI will then exit both businesses in FY 2026, and end FY 2027 with a merely 2% growth. I assign a P/S of 0.5x for the stock, lower than today’s ~0.8x P/S, which means that the market is valuing the stock as a distressed opportunity.

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2027 weighted target price of ~$6 per share in FY 2027. Discounting that target price with a 20% discount rate, I reached a Present Value/PV weighted target price of +$2 per share. The 20% discount rate represents the fair expected annual return for holding ANGI, given its risk profile today.

In summary, +$2 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return should my FY 2027 target price of ~$6 be achieved. At ~$3 per share today, the stock trades at a ~50% premium to my target price, indicating that it is highly overvalued.

Conclusion

ANGI has been through ups and downs since my previous coverage in 2020. The business’ fundamentals have been negatively impacted by underperforming growth initiatives in recent times, while the company also experienced a management change. Though the new management team has stepped in to improve the overall profitability outlook, I continue to see higher risk than reward on the stock. I am cautious about ANGI’s poor execution track record, the potential macro slowdown in the home repair industry at present, as well as the minimal presence of any key catalysts. The stock is overvalued based on my target model, and I maintain a neutral rating.

For further details see:

Angi Inc.: More Risk Than Reward