ANGO - AngioDynamics: AngioVac Profit Headwinds Not Attractive

2023-05-24 13:16:05 ET

Summary

- Another mixed quarter in Q3 FY'22 for AngioDynamics, despite strengths in its international markets.

- Management revised guidance higher, but this may widen the operating loss as well, in my view.

- AngioVac sales aren't gaining traction, clamping top-line growth.

- Net-net, reiterate hold.

Investment Summary

In the last AngioDynamics, Inc. ( ANGO ) publication, I urged clients against buying the company for a number of key reasons. Chief among these is the platinum tailwind coming to an end (see: last publication, Exhibit 3 ), amid other macro-level growth challenges. I also highlighted the potential lack of quality of assets underpinning the company's balance sheet:

Despite the fact that shares trade at 1.88x book value - a 42% discount to peers - I'd also note that the company's balance sheet is heavily tilted toward intangible sources of value. Of its $552.75mm in total assets, 63.9% is comprised of goodwill and intangibles [36% from goodwill alone]. As such, 35.8% and 47.3% of ANGO's book value is comprised of intangible assets and goodwill, respectively.

Push forward to the company's Q4 FY'23 and it's a similar story for ANGO in my opinion. There were plenty of takeouts from the quarter, each leading to interesting conclusions for the full-year. Here, I'll run through the results, and extrapolate key findings to show that ANGO doesn't satisfy advanced investment criteria. With one quarter to go, ANGO could do $342m in top-line revenues in my opinion, but you're looking at another operating loss (and only marginal profit when adjusting for R&D). Alas, findings from its latest numbers reveal a mixed sentiment, but there's no change to the broad hold thesis in my view. Net-net, ANGO remains a hold in my view.

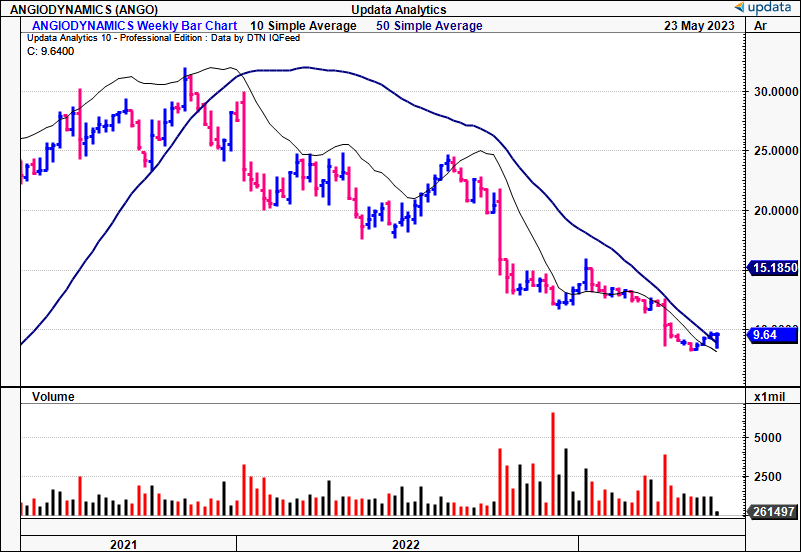

Figure 1. ANGO Cliff-Dive

{kind=link}

Q3 Lifting Veil on FY'23 Expectations

With just one quarter remaining after Q3 , there is plenty to draw from ANGO's numbers. First to the positives. It's been a decent start to the year on a number of fronts, I should say that much. AngioTech opened the gates with an 8% increase in net sales. The med-tech segment clipped 25% growth, and the Medical Devices segment showcasing was slow at 2.5%.

If you look more broadly, however, the negatives still weigh in heavily in my view. Expectations are low based on ANGO's current market value, so a large earnings surprise was needed - instead, it missed at the top and bottom line. Specifically, it came in with $80mm in turnover, growing ~910bps YoY on flat adj. EBITDA of $4.3mm. A detailed analysis is in order to pull apart the contributing factors and identify if there's mispriced value on offer here. My key insights follow.

Insights:

-

Auryon Growth + Expectations

- Auryon sales outperformed with 43% growth in the quarter to $10.4mm. I'd note this surpassed my own and management's expectations.

- It has now treated >35,000 patients since launch in September 2020, illustrating the rapid uptake, ~1,600 patients per month on average to March 30, 2023.

- Most of this uptake has stemmed from market expansion. Most notably, the push into below the knee ("BTK") procedures, and growth of international markets.

-

AlphaVac - Positive Reception

- Management reported positive feedback from physicians for AlphaVac, including the F22 and F18 versions.

- AlphaVac generated revenue of $2mm, booking to YTD revenue of $5.4mm. The current run rate supports the FY'23 guidance figure of $7mm to $9mm.

-

Challenges with AngioVac

- AngioVac sales compressed 16% this quarter, equal to 8% decrease YTD.

- Here comes one of the main issues with complex products. Given the complex nature of the AngioVac procedure, in that it requires specialized training, resources and ICU beds, this poses a challenge in the current environment. One look at the statements of listed hospital owners shows the shortfall of both specialist staff and ICU beds in the current hospital landscape.

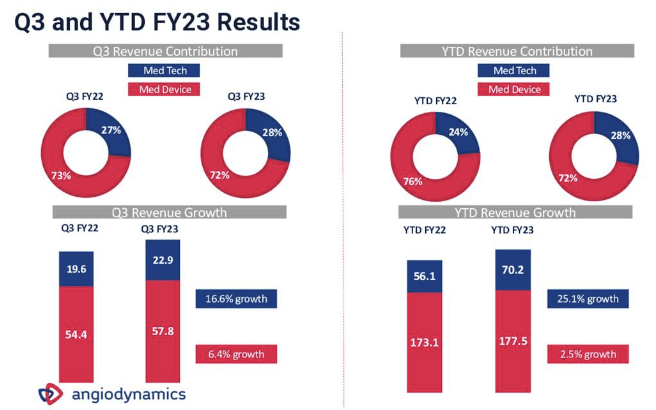

Management are on to solving these issues, but the issue right now is that we'll need a few quarters of data to observe any success. You can note the breakdown in YTD revenue from 2022-'23 in Figure 2, with MedTech outperforming at 25% growth YTD.

Figure 2.

Data: ANGO Investor Presentation

{kind=link}

Detailed view of financials

Rolling our eyes down the P&L, ANGO's Q3 gross was 50.2%, a dip of 200bps compared to the year ago period. Just a friendly reminder, Q3 gross had a ~115bps tailwind thanks to the CARES Act. Productivity and a pricing also gave 225bps of margin together.

In recent times, you can see ANGO has pared back the capital it has invested in productive assets, and this has been beneficial. Figure 3 shows the gross capital productivity as the rolling TTM gross profit divided by total assets each quarter. You can see this number shifting up from 28% in FY'20 to 32% in Q3 FY'23. Key to note - the gains are more a function of lower capital intensity, versus tremendous profit growth.

Figure 3.

Data: Author, ANGO SEC Filings

This advantage was also offset by sticky inflationary pressures of roughly 210bps in Q3, including 1) 110bps of raw material, 2) 90bps of labor, and 3) 10bps of increased freight costs. Let's not forget that the benefit from the mix was countered by lower AngioVac sales, as mentioned earlier. Additional points are as follows:

- Gross margin for ANGO's Med Tech segment clocked in at 64.6%, a decrease of 150bps YoY. This dip was primarily driven by lower sales of AngioVac and the sunk costs incurred from growing the Auryon installed base. Whether these will be recoverable, we'll see down the line. As for ANGO's Med Device segment, you're looking at gross of 54.5%, a 260 basis point decrease YoY.

- Q3 R&D investment danced at $6.9mm, equivalent to 8.5% of sales, compared to $7.3mm or 9.8% of sales a year ago. ANGO will continue its disciplined investment in R&D, all focused product development spend for the Med Tech portfolio. For FY '23, ANGO expects R&D spend to target a range of 8% to 10% of sales.

- Q3 SG&A expense waltzed in at $34.2mm, representing 42.4% margin compared to 39.4% of sales a year ago. The delta was again driven by growth investments in the sales team, especially Auryon. For FY '23, ANGO still calls for SG&A at 40% to 45% of revenue.

- Further, ANGO conjured up $1.4mm in quarterly operating cash flow, increasing net cash by $250,000.

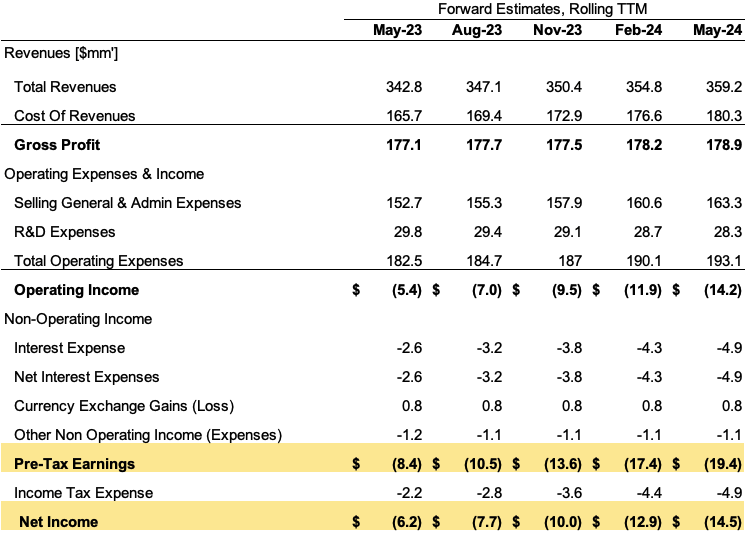

- Gazing to the FY '23 outlook, management revised top-line guidance and now calls for a range of $338mm-$342mm ($342mm to $348mm previous). That's a positive sign if you ask me, but not out of sync with the industry, as many peers are adjusting revenue estimates to the upside.

I'd say $342mm is a fair revenue number accurate, and I am aligned with this, calling for ~$360mm in FY'24 as well. I'd be calling for an operating loss of $5.4mm on this and net loss of $6.2mm this year. I've got ANGO widening its operating loss over the coming 12 months on a rolling TTM basis as well, which could present as a risk to valuation upside in my opinion.

Figure 4.

{kind=link}

Valuation

There's three resounding factors that have any intelligent investor cautious on ANGO at 18x forward EBIT :

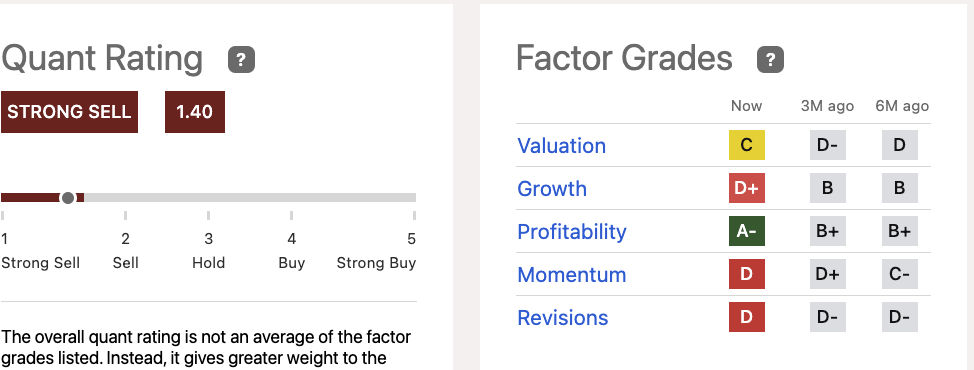

- The quant system has it rated as a "strong sell". These ratings are to be ignored at one's own peril.

- You're not even getting bottom-line growth going forward based on my estimates. The revised guidance to $342mm is welcomed, but would come at a cost to shareholders because the capital required to produce the growth is running at a loss.

- You're paying a premium for no cash earnings, making the firm difficult to value in the first place.

You've even got the company priced at 0.9x book value, which is a 'value' investor's dream, yet something in my investment cortex tells me this is the correct value for the firm. If the market doesn't even place a premium on its net asset value as a going concern, this is worrying - especially when you fold in all the other factors discussed here.

Hence, my estimation is the market has got ANGO correctly priced, but there's scope for it to run lower to the sector's 13x multiple. Further, the quant system, as mentioned, also identifies there's likely no mispricing. If so, we might expect a higher rating in more of the composite shown below. Not the case, however.

Figure 5.

{kind=link}

In short

You'd be surprised to know that ANGO still fetches 18x forward EBIT despite trading near 52-week lows. A mixed quarter with downsides in key segments has me remaining cautious on this name. You've got the AngioVac segment to watch out for going forward, in my view, plus the market has driven the equity down from c.$25 to under $10 in less than 1-year. Something is up, and the expectations going forward aren't high. My findings suggest a combination of flat earnings growth, no profitability, and key asset divestitures may be underneath this. Net-net, there is not enough evidence to advocate that ANGO is an investment-grade company right now, not for those sophisticated investors commanding above-market returns. Reiterate hold.

For further details see:

AngioDynamics: AngioVac, Profit Headwinds Not Attractive