ANGL - ANGL: Time To Nibble On Some Conservative High Yield Exposure

2023-10-31 01:55:08 ET

Summary

- The VanEck Fallen Angel High Yield Bond ETF aims to replicate the performance of the ICE BofAML US Fallen Angel High Yield Index.

- Fallen Angels are bonds that were once rated investment grade but have since been downgraded to junk status.

- The fund is overweight in 'BB' rated bonds, with Vodafone Group being one of the well-known companies in its portfolio.

- In a risk-off scenario similar to October 2022, we estimate a -5% drawdown in the name, mainly driven by credit spread widening.

- The fund benefits from a conservative build via its rating profile, and the propensity of many former investment grade companies to regain their rating.

Thesis

The VanEck Fallen Angel High Yield Bond ETF ( ANGL ) is an exchange traded fund. The vehicle aims to replicate the price and yield performance of the ICE US Fallen Angel High Yield 10% Constrained Index ('H0CF'). The index is composed of below investment grade corporate bonds that were rated investment grade at the time of issuance. The ETF is passively managed, seeking to replicate as closely as possible the price and yield performance of the index. The ICE index rebalances monthly, and constituents are capitalization-weighted, based on their current amount outstanding subject to a 10% issuer cap. Defaulted bonds are removed from the index at the end of the month.

How to frame 'Fallen Angels'

As described above, fallen angels represent bonds that at issuance were rated investment grade, but currently fall in the junk space. This translates into the financial metrics of the underlying companies having deteriorated to such an extent that a downgrade occurred. The impact to a portfolio holding such bonds has a number of facets:

1. Fallen Angels tend to be rated in the 'BB' band, since a downgrade usually occurs for 1 or 2 notches:

Ratings Matrix (S&P)

'BB' bonds are the safest junk bonds, and usually have the tightest spreads and lowest gap-down during risk-off events. They are the 'safest' junk bonds so to speak.

2. Companies which have been downgraded from investment grade to junk, usually want to return to investment grade status in the long run. A retail investor needs to understand there is a massive financial planning differentiation between an investment grade company and a junk one. The cost of capital and balance sheet structure could not be more different.

Investment grade companies have access to cheap revolving bank facilities, and they can place really long dated bonds (10 years and up) at a low all-in cost of capital. Conversely, junk entities have a high amounts of liens on their assets, strict covenants on what they can do and debt maturities that usually top out around the 5 to 6 year mark. They can also see themselves locked out of the funding markets if extreme stressed scenarios exist.

Due to these factors, companies which enter rough patches and get downgraded usually change management, cut costs, divest business lines, and generally try to get back to their old funding model and status quo. Not all, but a large proportion of them. This translates into junk bonds becoming investment grade, and companies retiring that debt or investors seeing spreads compress significantly.

Analytics

- AUM: $2.3 billion.

- Sharpe Ratio: -0.01 (3Y).

- Std. Deviation: 9 (3Y).

- Yield: 8%.

- Premium/Discount to NAV: n/a.

- Z-Stat: n/a.

- Leverage Ratio: 0%.

- Effective Duration: 4.7 years

- Composition: High Yield Bonds

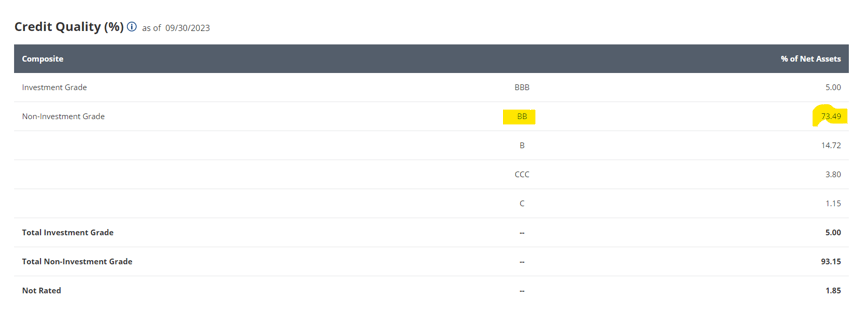

Collateral Composition

The fund is overweight 'BB' names, which make up over 73% of the collateral tape:

{kind=link}

As discussed above, this state of affairs is driven by the fund's mandate, with the ETF focused on fallen angels. When bonds get downgraded, they usually move down in the rating matrix by one or two notches.

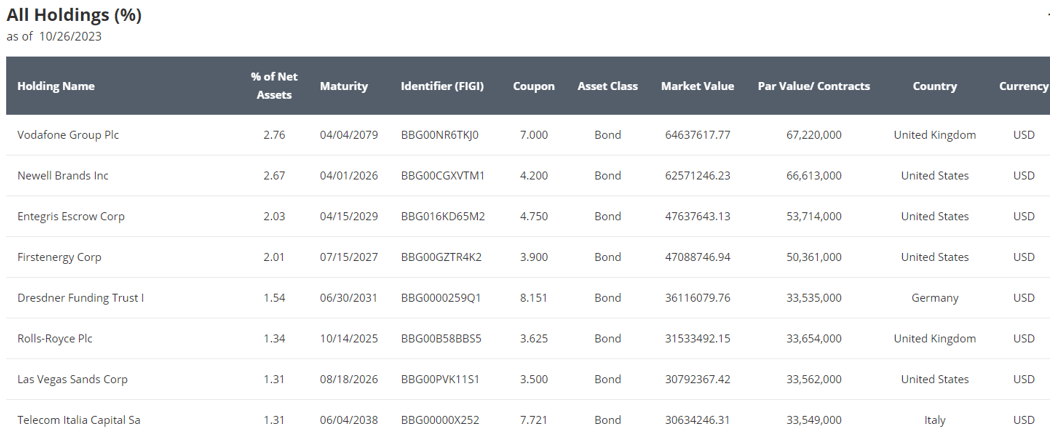

If we look at some of the individual names in the portfolio we can find some very well known companies here:

{kind=link}

Vodafone Group ( VOD ), for example, is the largest European telecom company, with a $25 billion market cap and a 10% yield on its common shares. We are not experts in VOD, but can surely attest we would be very comfortable holding the debt of this name with $25 billion in structural equity subordination and a massive interest savings that can be realized by cutting the dividend on the common shares.

The only slight negative to notice for ANGL is the high concentration in the top names. Very granular funds usually cap individual exposure at around 1%, but not here. All the top names in the ETF are above 1%, and moreover we can see the top four names well above 2% of the holdings. However, given the reduced probability of default for the largest exposures, we are comfortable with the set-up.

What are the risk factors for this fund?

The main risk factors for this fund are constituted by rates and credit spreads. With the Fed now on pause , and with increased speculation we are done with hikes this rate cycle, the focus now comes down on credit spreads:

{kind=link}

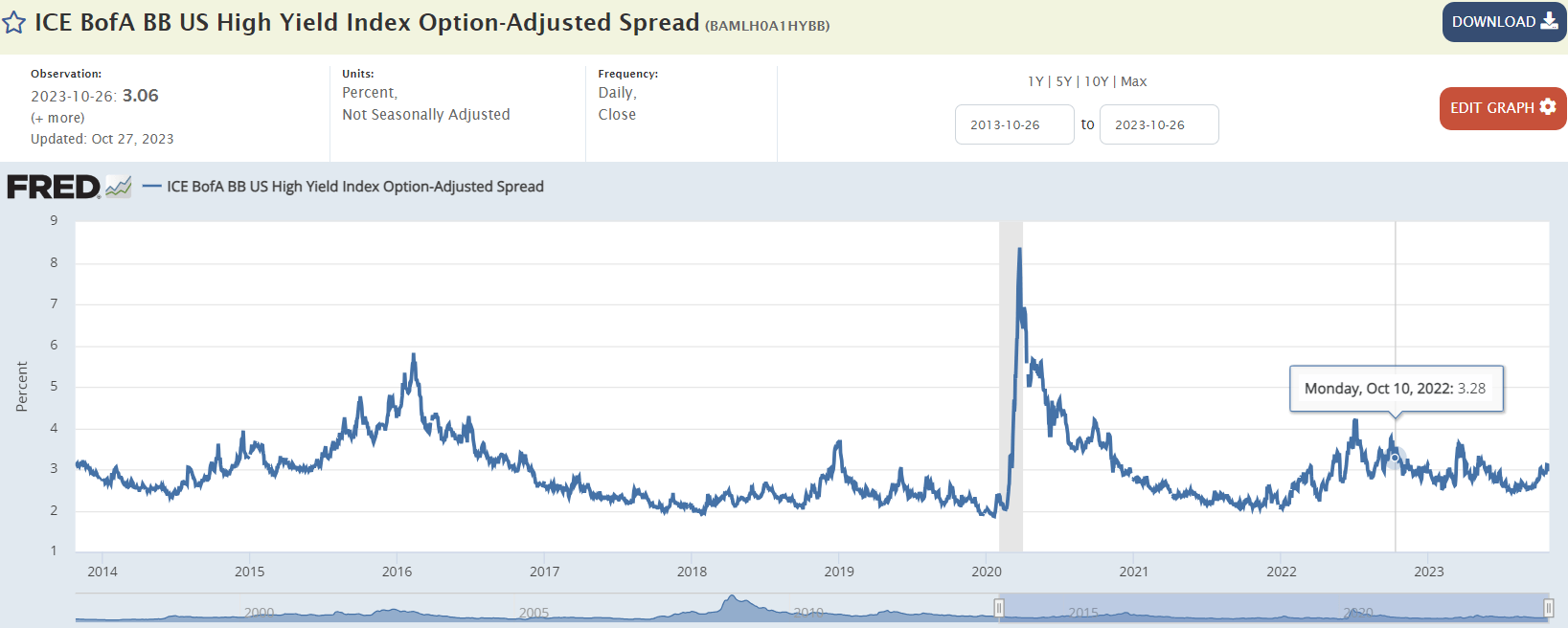

Since the fund is focused on 'BB' names, we are going to have a look at the ICE BofA BB US High Yield Index Option Adjusted Spreads. Currently the index has a 3.06% level, which tallies out nicely with the ANGL all-in yield of 8%. Treasuries yield roughly 5%, plus the 3% on 'BB's gives us 8%.

We can see that during the October low of 2022, spreads moved up to 4%, roughly 100 bps higher than here. Given that ANGL has a 5 year duration, this translates into a -5% drawdown if we experience a risk-off event similar to what we witnessed last year. In an extremely negative scenario where credit spreads would go to 5%, the drawdown would be a maximum of -10%. To note that the rates component represents a higher percentage of the fund, given its overweight positioning in 'BB' names. Rates are peaking, so the main risk factor will actually provide some benefits next year.

In a scenario where we have a severe recession and credit spreads widen out significantly, we should see some benefit in all-in yields via a decrease in rates. The market will start pricing in rate cuts if we have a severe recession. Therefore we have a built-in mitigant here.

Conclusion

ANGL is a fixed income exchange traded fund. The vehicle focuses on bonds which used to be investment grade at issuance, and therefore is overweight a portfolio of 'BB' names. The ETF is more conservatively set up when compared to other HY names because of its 'BB' concentration, and propensity of former investment grade companies to move back to the respective rating band via restructurings.

The fund has credit spreads as its main risk factor, with rates now peaking. In a stressed scenario similar to October 2022, we see a -5% drawdown in this name, well compensated by its 8% 30-day SEC yield. ANGL is not leveraged, and represents a conservative take on high yield via its portfolio composition. With rates peaking, an investor looking to nibble in the high yield space would do well to take small bites into ANGL as compared to leveraged vehicles.

For further details see:

ANGL: Time To Nibble On Some Conservative High Yield Exposure