AGPPF - Anglo American Platinum: Efficient Business At A Reasonable Price But Still Too Early

2023-12-07 16:57:59 ET

Summary

- Anglo-American Platinum is the largest platinum miner measured in annual production, with a 31% share of the global annual output.

- The company has one of the best balance sheets in its peer group. AGPPF has a 4.3 cash-to-total debt ratio, with $1.77 billion cash and $411 million total debt.

- AGPPF is the most profitable platinum miner measured by ROTC, ROE, and EBITDA margin.

- The company pays dividends with a respectable yield (5.7%), though lower than SBSW (8.6%) and IMPUY (8.6%). The company maintains a 40% payout ratio.

- AGPPF is the most expensive in its peer group but cheaper than its 5Y average figures and 10Y historical peaks.

Introduction

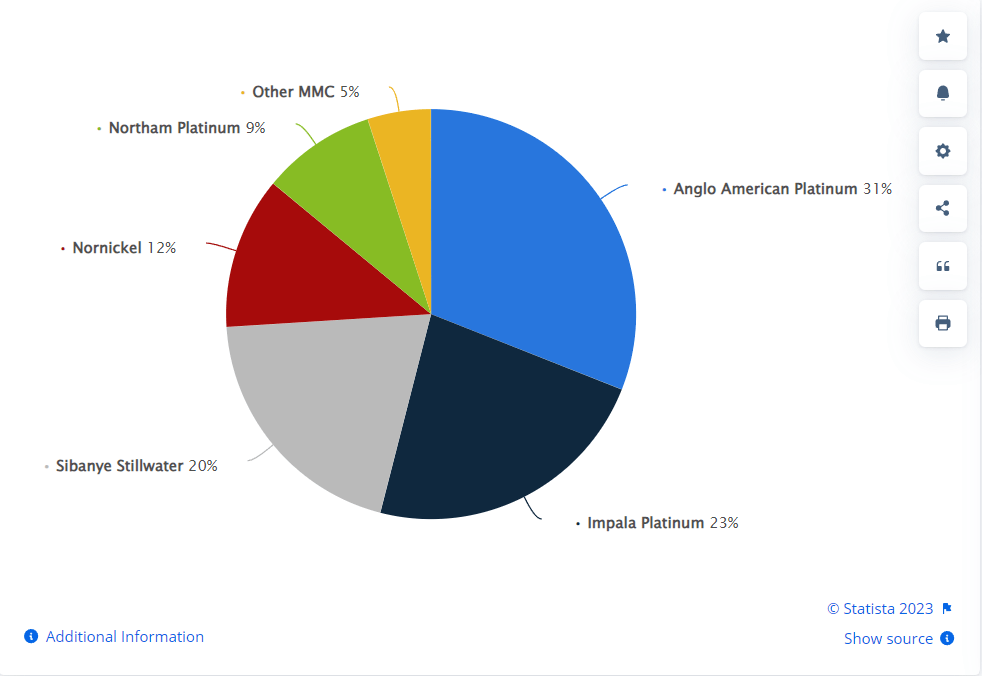

Anglo American Platinum ( AGPPF ) is the largest platinum miner measured in annual production, with a 31% share of the global annual output. The chart below from Statista shows the production shares among the largest platinum miners .

{kind=link}

The company owns the largest platinum open pit mine, Mogalakwena, in South Africa. The company also owns five mines in South Africa and one in Zimbabwe.

AGPPF has $411 in debt and $1.77 billion in cash. It maintains healthy debt-to-equity and interest coverage ratios. The company is the most profitable among its peers, measured by ROE and ROTC. The dividends are inferior to Impala Platinum (IMPUY) and Sibanye Stillwater ( SBSW ), though still adequate with a 5.7% TTM yield.

The company's EV/EBITDA, EV/Sales, and Price/TBV are the highest among the platinum majors. However, it trades below its historical multiples peaks and 5Y average values.

Last year has been challenging for platinum and palladium, pushing PGM stocks into a prolonged bear market. AGPPF is no exception. In December, the price bounced from significant support, although it is early of an entry. For now, I patiently wait on the fence. My verdict is a hold rating.

Company preview

AGPPF is part of the multinational mining conglomerate Anglo American plc (AAUKF). The latter owns 78.5% of AGPPF shares. Company revenue originates from platinum (45%) and palladium (32%). The remaining is distributed between rhodium, gold, iridium, and ruthenium.

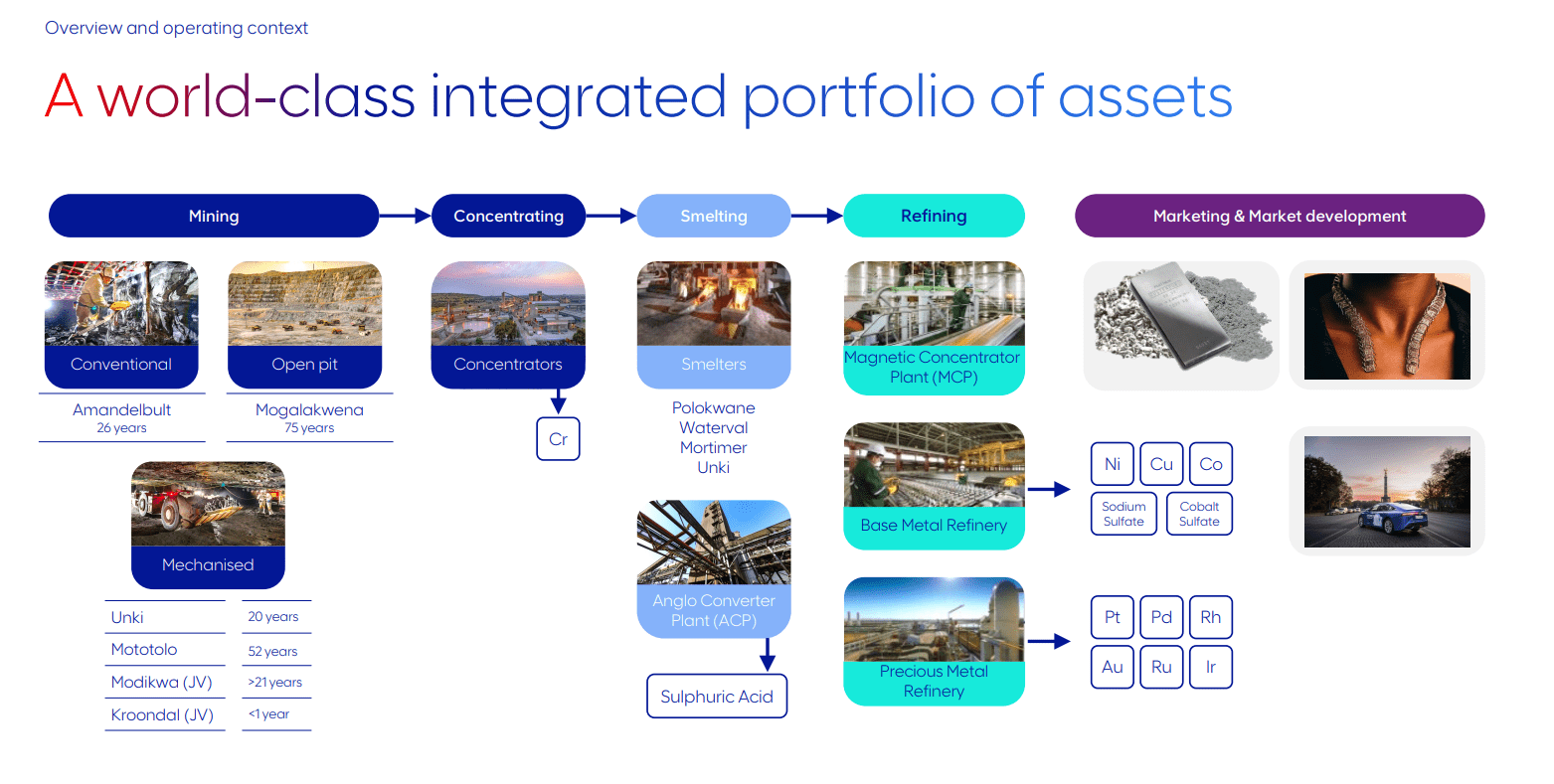

The image below from the last company presentation shows AGPPF at a glance.

Anglo American Platinum presentation

{kind=link}

Mogalakwena has been the flagship asset in the company's portfolio, with 75 years of LOM. The mine has Proven and Probable reserves for 112 M oz 4E (platinum, pallidum, rhodium, gold) and 122 M oz 4E Measured and Indicated resources. Mogalakwena operations realized a 49% EBITDA margin in 1H23.

Amandelbult is the sixth-largest platinum mine globally, with 26 years of LOM. It has 13.1 M oz 4E P&P reserves and 54 M on 4E M&I resources. Amandelbult operations realized a 30% EBITDA margin in 1H23.

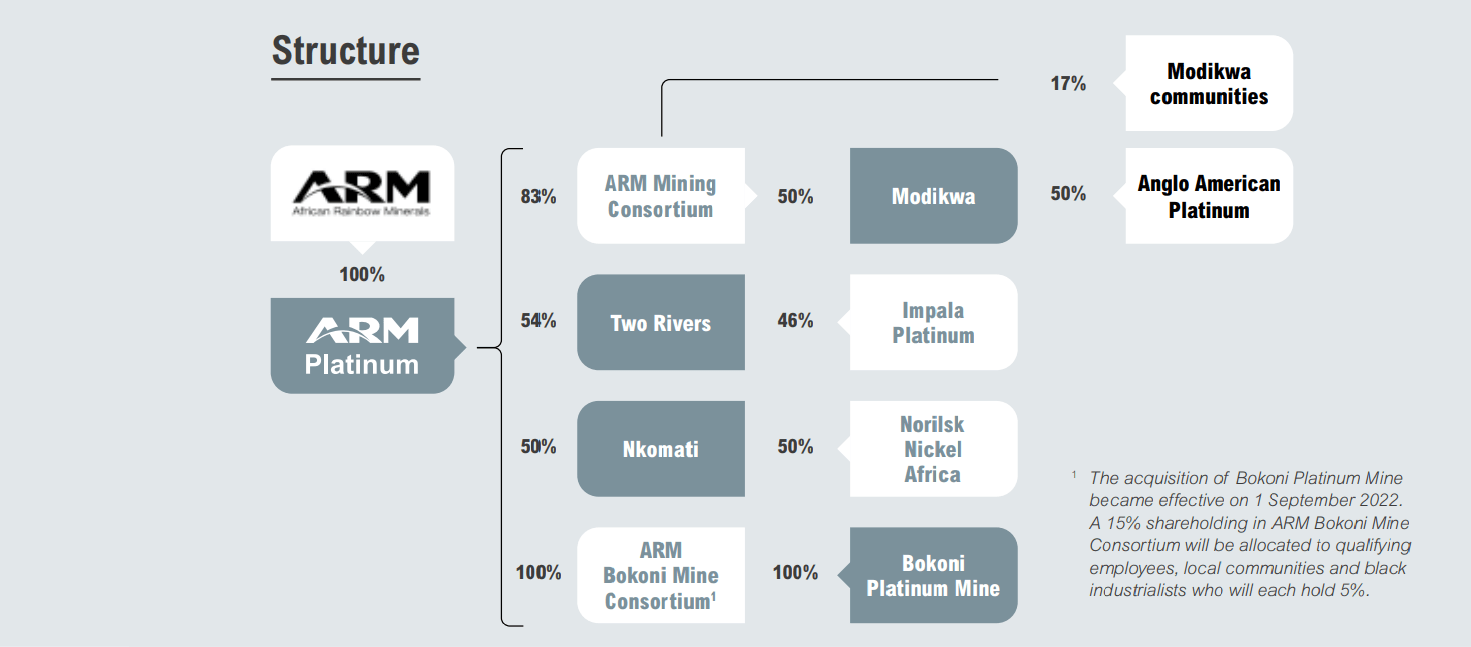

AGPPF and SBSW operate Krondaal mine as 50/50 Joint Venture. The mine has 1.3 M oz 4E P&P reserves and 6.6 M on 4E M&I resources. Modikwa mine is a joint venture between African Rainbow Minerals and AGPPF. The graph below from the last ARM financial report shows the JV structure.

African Rainbow Minerals annual report

{kind=link}

Modikwa holds 5.25 M oz 4E P&P reserves and 40.9 M on 4E M&I resources. Mototolo is the fifth South African mine run by AGPPF with LOM until 2074. It has P&P of 13.6 M oz 4E and M&I 28.5 M oz 4E.

AGPPF has one asset in Zimbabwe, the Unki mine. It is in the second largest platinum deposits region next South African Bushveld Complex – Great Dyke . The Unki mine has a P&P of 5.4 M oz 4E and an M&I of 16.8 M oz 4E. The LOM is expected till 2042. Unki operations realized a 31% EBITDA margin in 1H23.

AGPPF has a complete cycle of PGM production, from mining to refining and production. The company has two smelter facilities in South Africa: Polokwane and Waterval.

AGPPF sales its products globally as seen in the table below:

{kind=link}

Such a diversified customer is an advantage in regional economic downturns. The exposure to China is 9.0%. Such low figures are exceptions for most of the extractive businesses. Usually, China is the largest buyer of their output, thus making company results a function of the Chinese economy. AGPPF is exposed to the Japanese economy to a higher degree. 36% of its output is sold in Japan. The second largest buyer of AGPPF's production is Germany, with 19.9%.

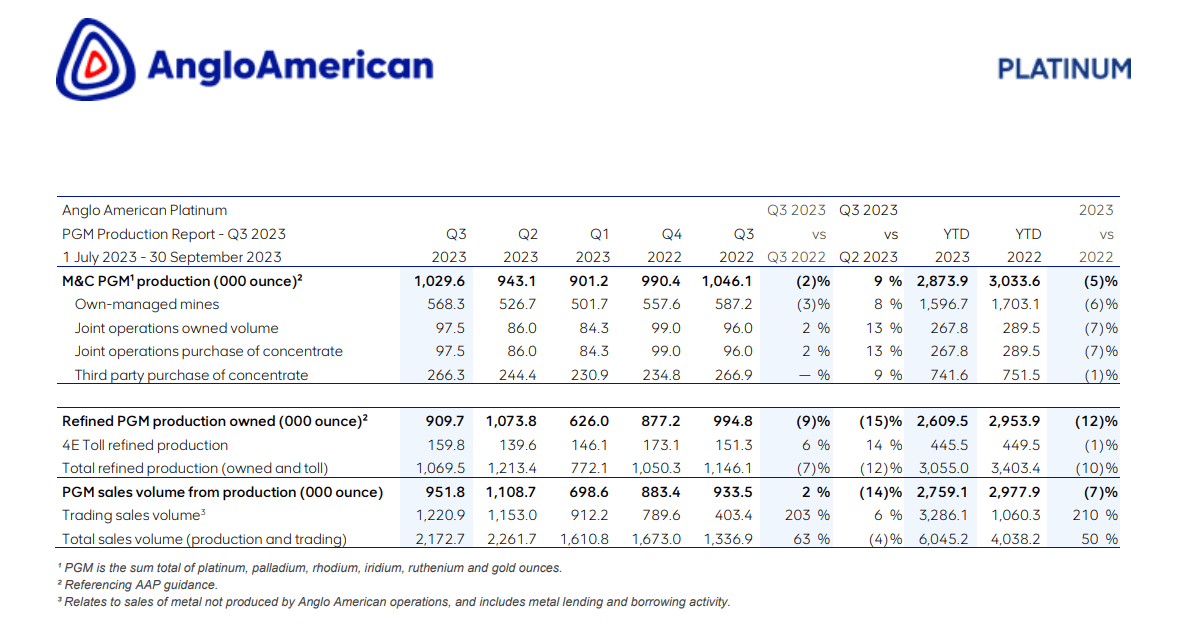

Production results 3Q23

The company published its 3Q23 figures on October 24, 2023. QoQ 6E (4E + iridium and ruthenium) decreased by 2% to 1,029,600 oz. Production sales had increased by 2% to 1,209,600 oz for the same period due to exhausted refined stock.

The table below gives production figures for the last two years.

Anglo American Platinum 3Q23 results

{kind=link}

The reduction in output from Mogalakwena and Amandelbult was the leading cause of the 3% decline in total PGM production in AGPPF-owned mines to 568,200 ounces. At Mogalakwena, PGM production fell by 5% to 246,800 ounces due to lower grades, which led to a 3% drop in 4E head grade, which was 2.84g/t in 3Q22 to 2.75g/t in 3Q23.

Amandelbult's PGM output increased by 25% QoQ, although it decreased by 4% to 184,900 oz YoY. This was primarily due to the mine's Dishaba Mine's poor ground conditions, which continued to reduce accessible ore reserves. PGM production in Unki and Mototolo rose by 1% YoY.

Joint Operations PGM production grew by 2%, reaching 195,000 oz. Modikwa's output increased to 79,200 oz due to higher grades and recoveries, up 5% compared to previous quarters. Kroondal production fell by 1% to 115,800 oz.

Refined PGM production (only production, excluding tolling) decreased by 9% to 909,700 oz. The primary reason is an unplanned multi-municipal water stoppage at the Rustenburg processing plant that disrupted five-day operations (54,000 PGM oz). Additionally, there was a decrease in the production of metal-in-concentrate. Output of refined palladium dropped by 10% to 285,500 ounces, and refined platinum fell by 6% to 428,500 ounces.

Eskom load-curtailment resulted in less than 5,000 ounces of production being held back for later processing. However, the lag did not affect the output. Production of toll-refined PGM rose by 6% to 159,800 PGM ounces.

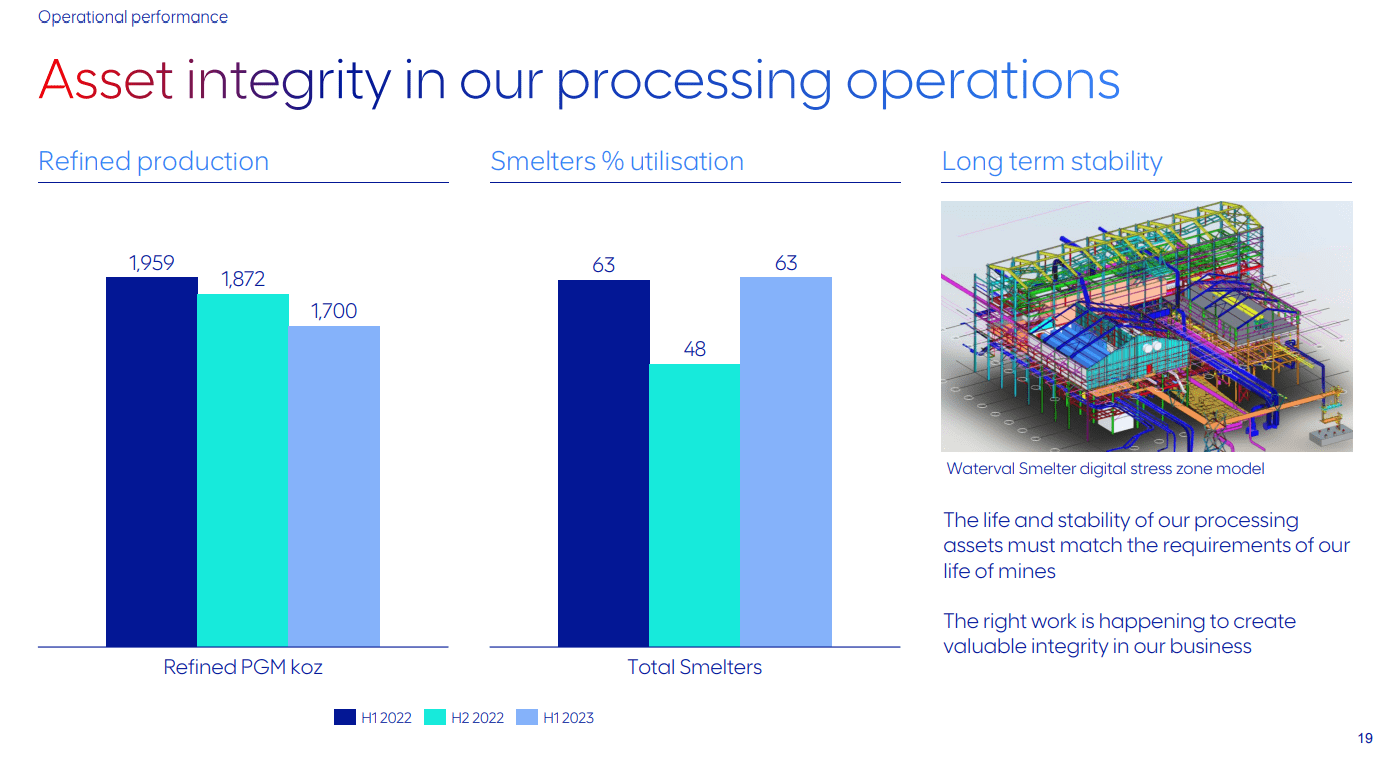

The image below shows the smelting and refining performance for the last two years. The chart is from the last company presentation .

Anglo American Platinum presentation

{kind=link}

Despite the load curtailment, smelter utilization improved HoH, and refined production did not decline significantly. The total number of impacted days was 42, resulting in a full-year impact of 3-3.5% of the refined output. The mining operations have not been affected by power outages.

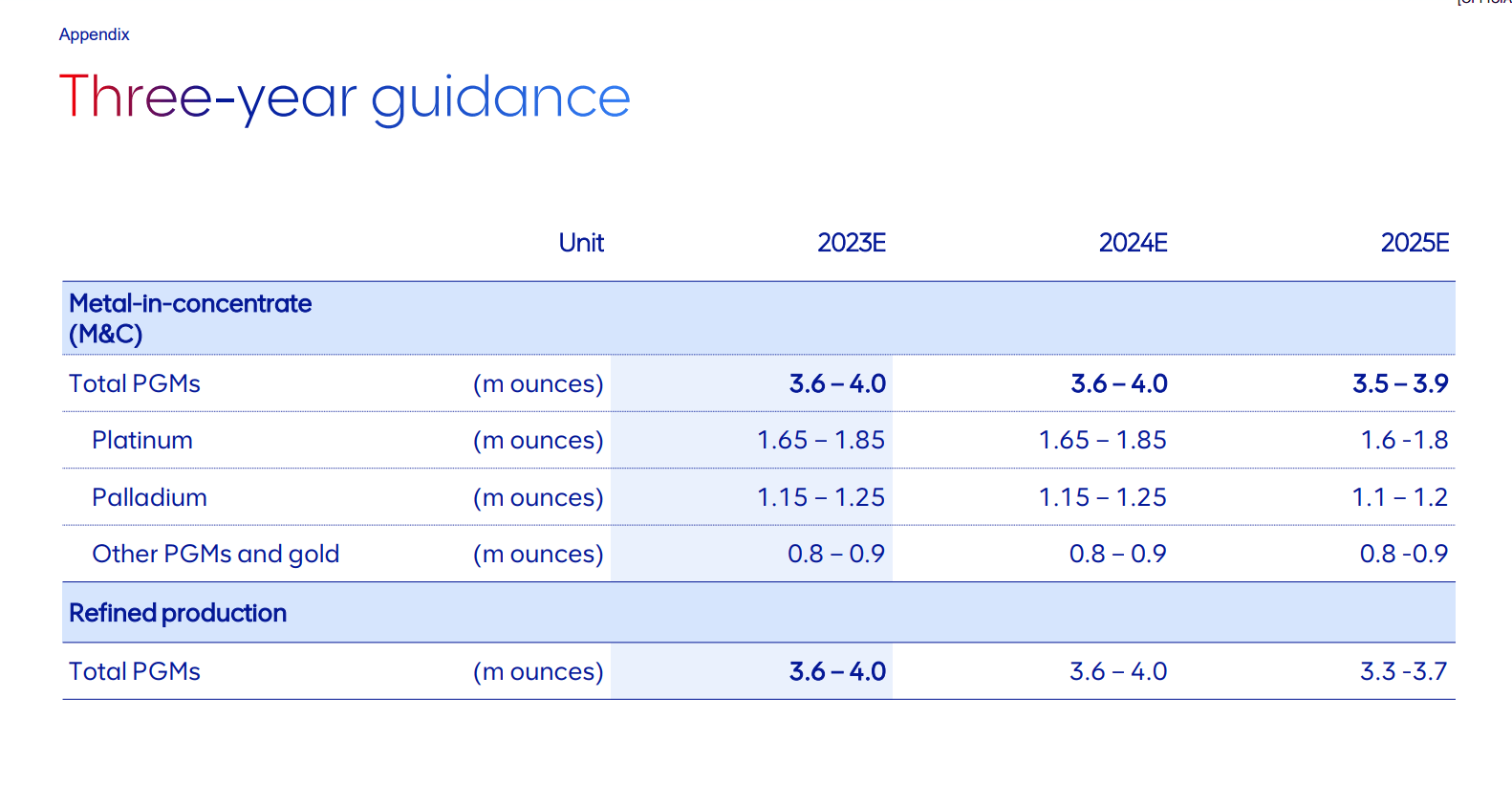

AGPPF guidance for 2023's refined PGM output is 3.6 - 4.0 M oz 6E. Higher cast costs are expected due to load curtailment, foreign exchange rate volatility, and ongoing inflationary pressure. Unit costs per PGM ounce produced are estimated to be between R16,800/oz and R17,800/oz ($887/oz and $939/oz).

In 2024 and 2025, the company expects to maintain its production (M&C) level between 3.6-4.0 M oz 6E. Output per metal is expected to remain the same, too.

Anglo American Platinum presentation

{kind=link}

Balance sheet

Similar to SBSW and IMPUY, AGPPF has a robust balance sheet. Despite the declining PGM prices, the company maintains its solvency and liquidity at impressive levels.

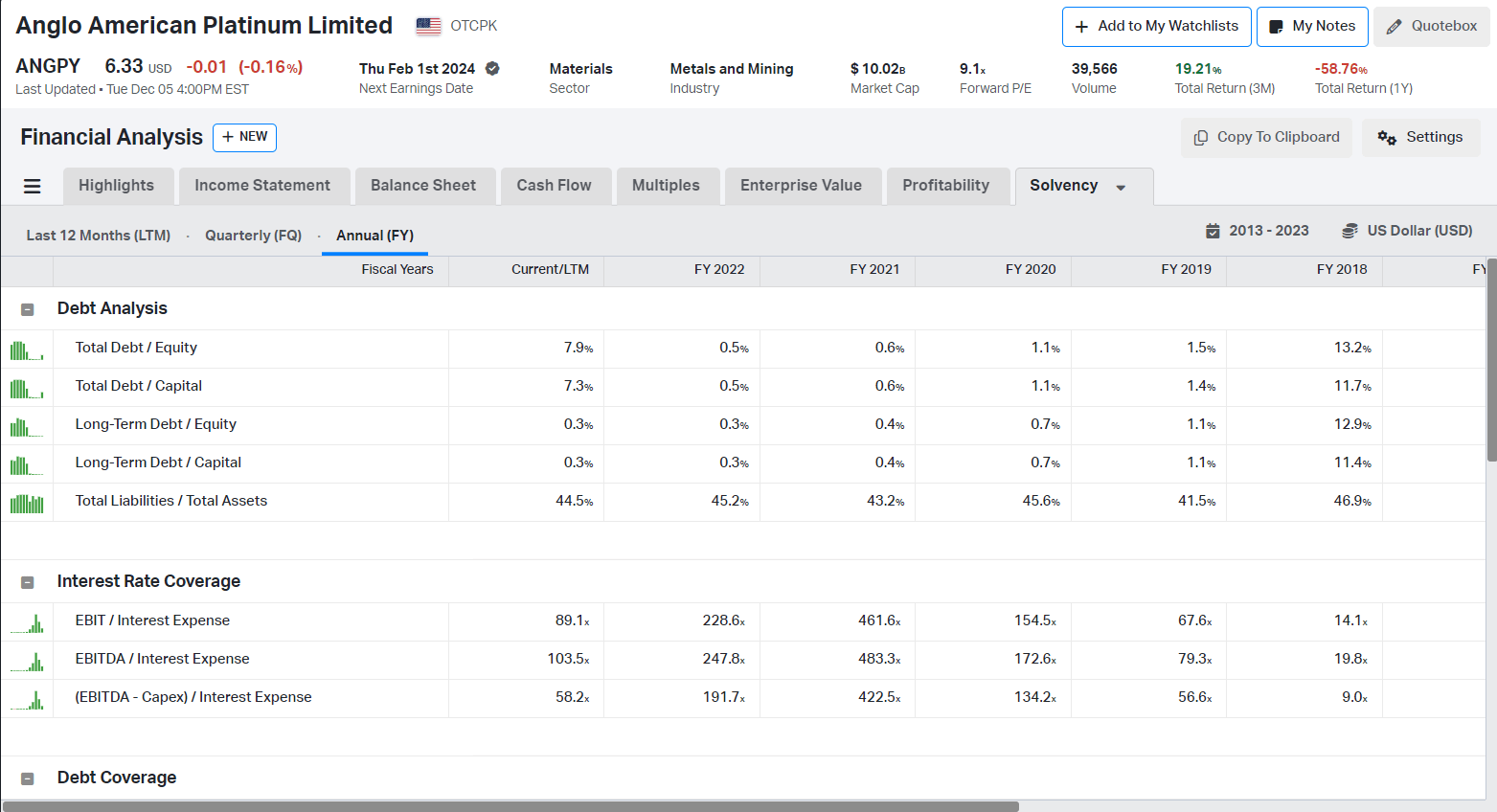

The table below shows AGPPF's solvency and interest coverage figures.

{kind=link}

Interest coverage remained sufficient for the last five years. Even in 2018 and 2019, the company had EBITDA/Interest coverage above 15.

AGPPF has $411 million in total debt and $1.77 billion in cash, resulting in a total debt ratio of 4.3. For reference, SBSW has $1.18 billion cash and $1.38 billion total debt; Northam has $284 million cash and $794 million total debt; IMPUY has $1.43 billion cash and $137 million total debt.

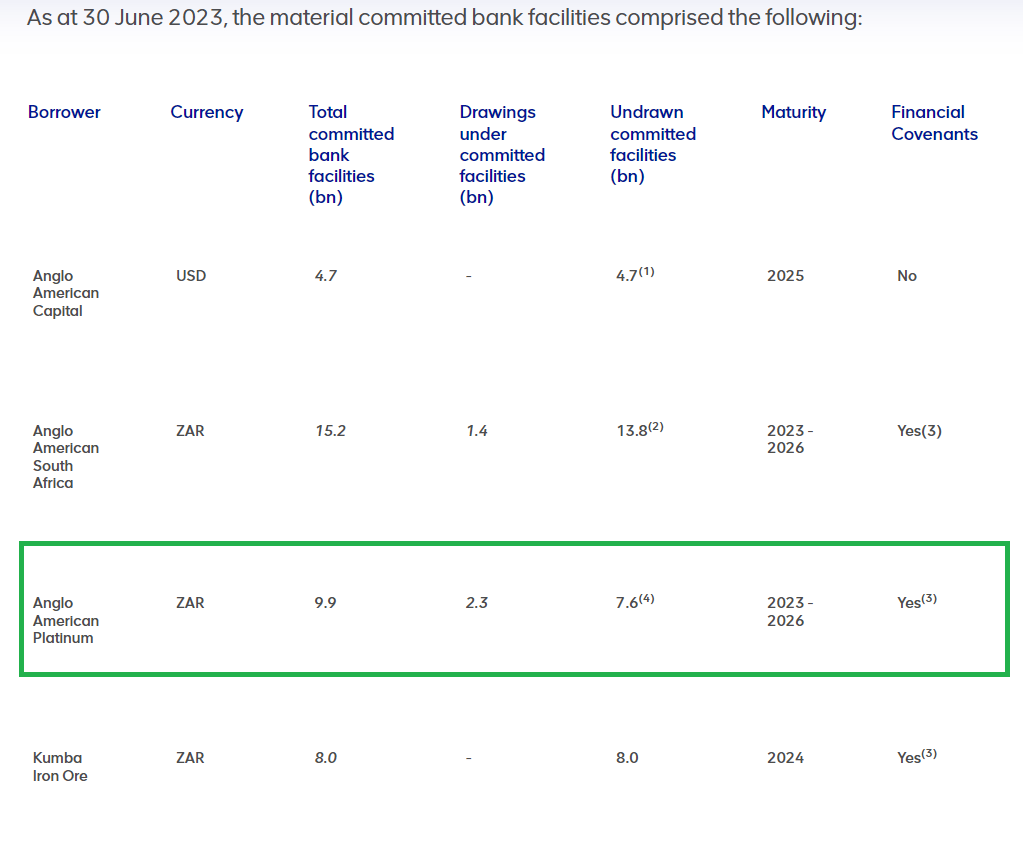

Last year, the total debt/equity ratio increased to 7.9% from 0.5% in 2022. The chart below from the Anglo-American website shows company subsidiaries' bank credit facilities.

{kind=link}

AGPPF has a credit facility with maturities in 2023-2026. A large portion of the debt ($387 million) is due in the coming quarters. Given its solid cash position and adequate operational cash flow, I am confident AGPPF will cover its debt obligations.

Profitability and dividends

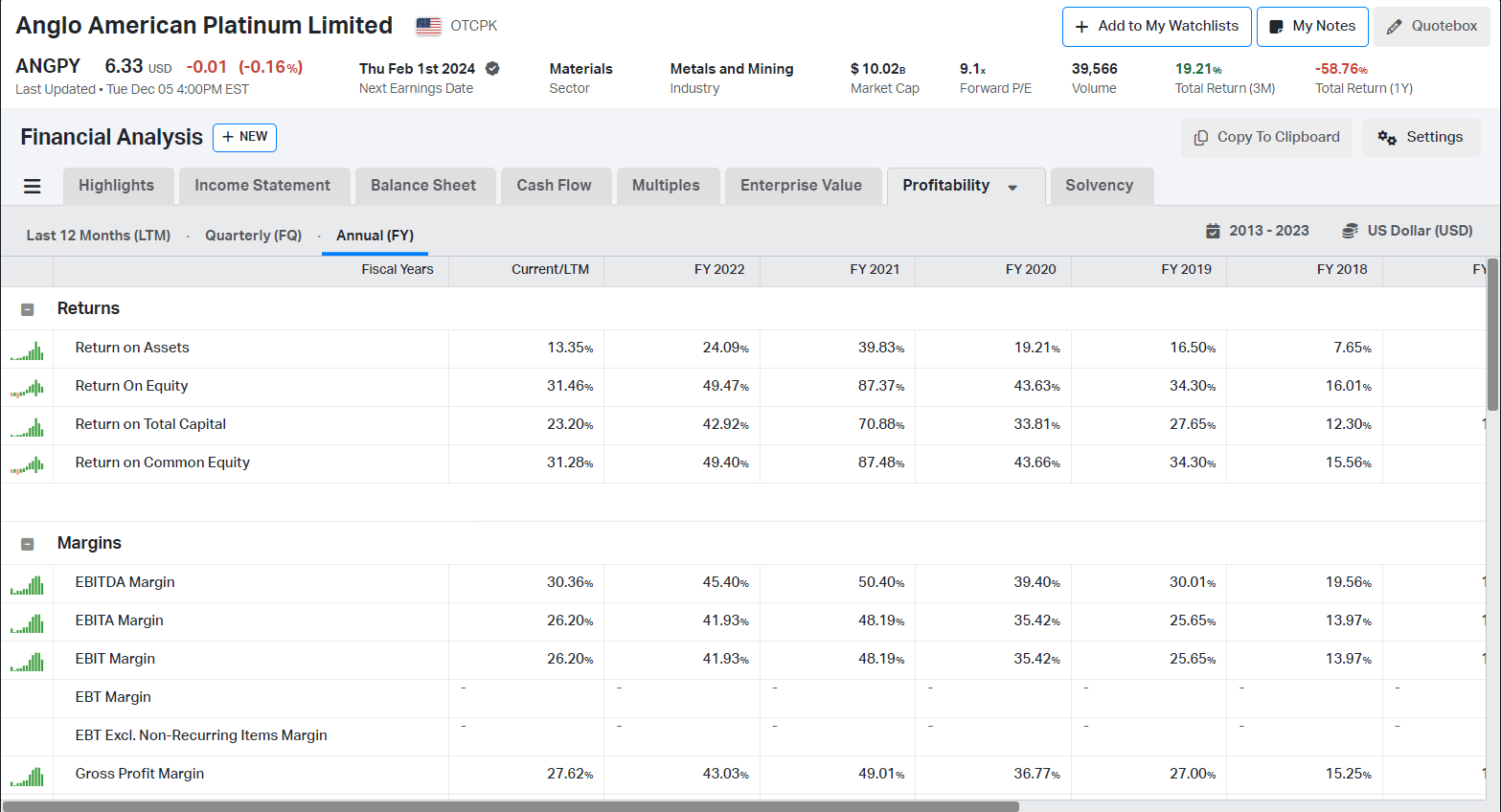

AGPPF is the most profitable platinum miner measured by ROTC, ROE, and EBITDA margin. The table below shows company returns and margins for the last five years.

{kind=link}

Even the PGM bear market cannot suppress the company's profitability. ROTC and ROE have been above 10% for years. Such figures are impressive, given the severe cyclicality of PGM prices.

Let's dig deeper into the company's profitability.

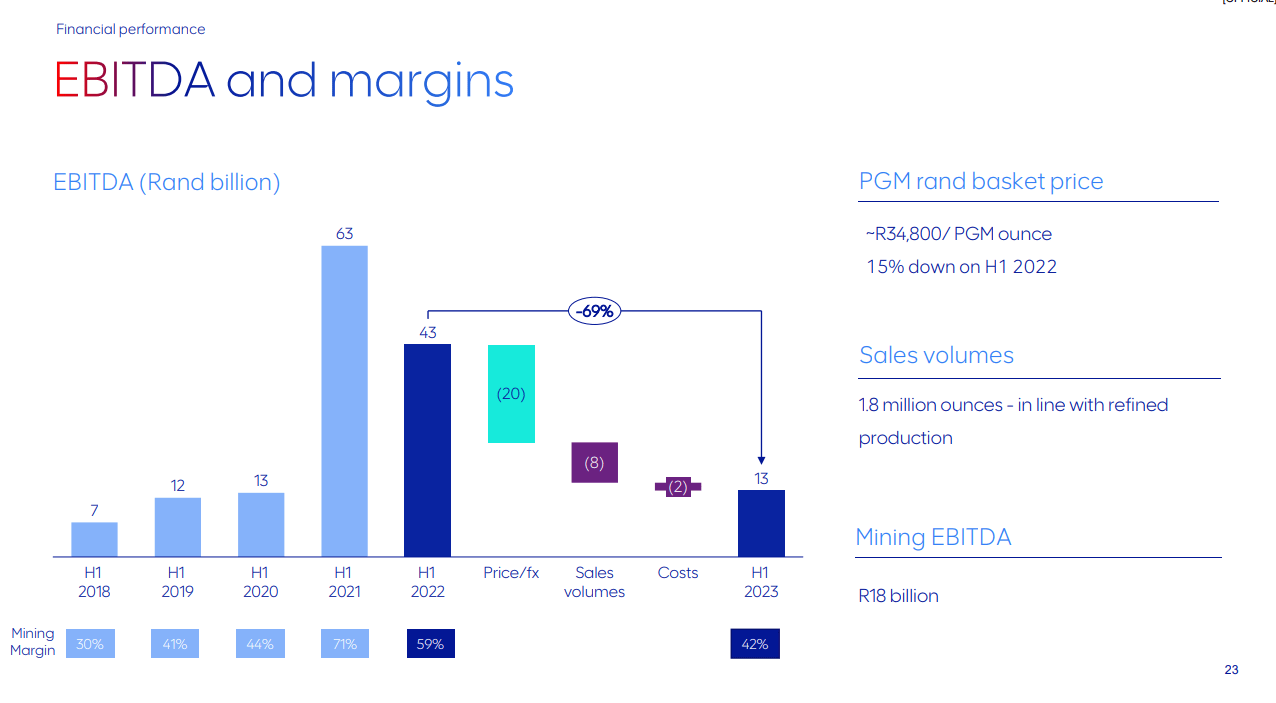

Anglo American Platinum presentation

{kind=link}

The mining margin dropped significantly HoH and YoY due to lower PGM prices. PGM basket price for 1H23 was R34,800/oz ($1837/oz). 1H23 EBITDA is R13 billion or 69% decline YoY.

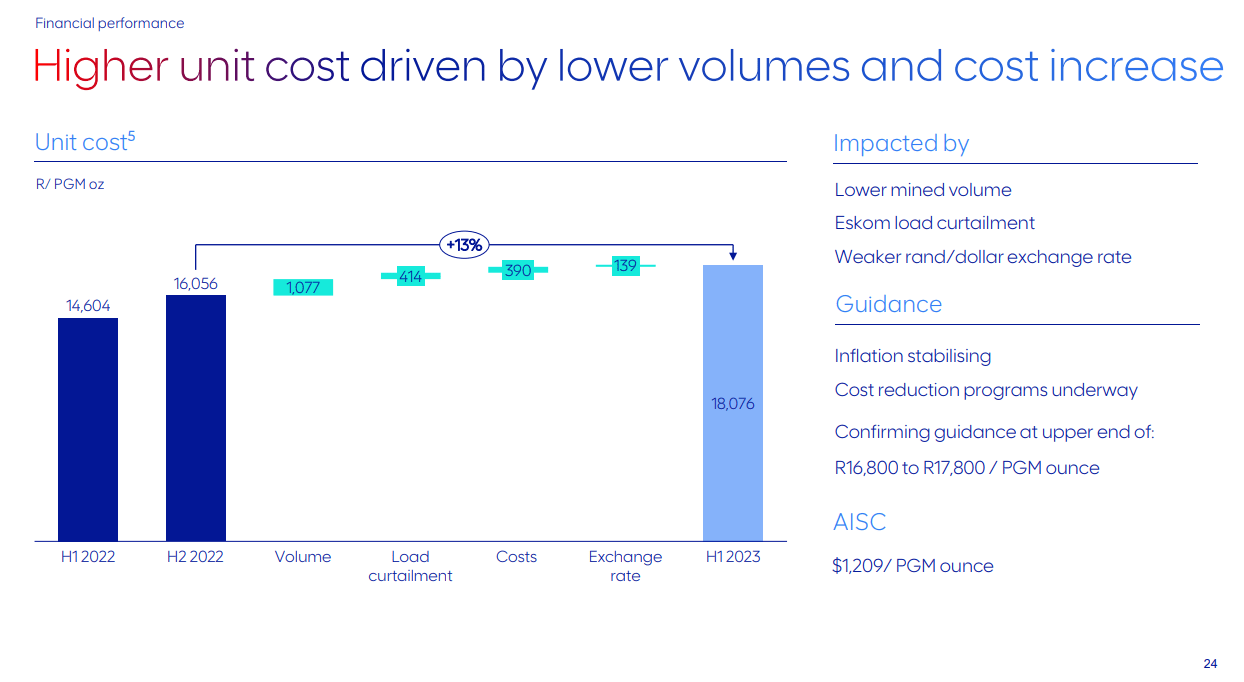

Besides declining PGM prices, unit costs rose by 23% YoY, reaching R18,076/oz ($953/oz). As mentioned, the unit cost will remain elevated due to load curtailment, FX volatility, and inflationary pressures.

Anglo American Platinum presentation

{kind=link}

AGPPF pays dividends with a respectable yield (5.7%), though lower than SBSW (8.6%) and IMPUY (8.6%). The company maintains a 40% payout ratio.

Anglo American Platinum valuation

AGPPF is the most expensive in its peer group using EV/Sales, EV/EBITDA, and Price to Book. For comparison:

- AGPPF trades at 1.14 EV/Sales, 3.76 EV/EBITDA, and 1.93 Price/Book

- SBWS trades at 0.51 EV/Sales, 2.04 EV/EBITDA, and 0.61 Price/Book

- NPTLF trades at 1.32 EV/Sales, 3.16 EV/EBITDA, and 1.32 Price/Book

- IMPUY trades at 0.45 EV/Sales, 1.62 EV/EBITDA, and 0.50 Price/Book

Let’s compare AGPPF with its historical multiples.

{kind=link}

AGPPF trades at lower than 5Y average multiples: 1.14 EV/Sales, 3.76 EV/EBITDA, and 1.93 Price/Book. 5Y average figures are 2.27 EV/Sales, 7.34 EV/EBITDA, and Price/Book 30.24. Besides that, its multiples are well below the previous peaks. Despite being the most expensive in its peer group, AGPPF is cheaper than its 5Y average figures.

Price action

AGPPF stock price bounced from a significant price level. Two tiny monthly candles define the local bottom. The December candle is giving the strong bull signal, but before its closure, it is too early for entry.

{kind=link}

AGPPF stock trades below 36 monthly simple average ((SMA)). SQN indicator says the price is in a bull-quiet regime. Now, it’s time to be patient. I like to see the strong bull December candle. Until then, I'll sit tight and wait for price confirmation.

Risks

The mining business is one of the toughest. Investing in mining carries significant risks. A niche and concentrated market, such as PGMs, has even more risks. Over 80% of the platinum comes from the Bushveld Complex in South Africa. Operating in South Africa is a challenging endeavor.

Five of six AGPPF's mines are there. ESCOM's tradition in mismanagement and corruption peaked in 2023 with permanent load curtailments. Let’s add South Africa's chronic issues, such as racial tensions and a high crime rate. Running the business there is not for the faint hearted, nor is investing.

One of the company mines, Unki, is in Zimbabwe. The country is not the best performer in any “Risk of doing business” contest, though it's less bad than South Africa in my opinion.

The company’s management has been very prudent with its financial decisions. Despite the cyclicality of the PGM market it maintained excellent solvency and liquidity metrics.

Let's not forget the PGM market supply side structure: two producing countries, a few companies, and several mines dominate the market. However, the demand depends on many variables, with China being the most critical. AGPPF has lower exposure to China compared to most industrial metal miners. The company has more weight on Japan and Germany, though neither of the countries contributes with more than a third of company revenue.

In the long term, I am bullish on PGMs, especially platinum. Platinum consumption will grow significantly. ICE is not going anywhere, and catalytic converters will be needed to cover air emissions regulations.

Investors takeaway

AGPPF is the largest platinum miner. It has six mines and three of them are in the top ten mines globally. The company is the most profitable among its peer group, maintaining excellent returns and margins over the years. The company’s management has been conservative keeping the debt level to a minimum. Despite being the most expensive in its peer group, AGPPF is cheaper than its 5Y average figures. I give a hold rating due to the price action. Being too early can be a costly mistake, the same as being too late. For now I am on the fence, but ready for action.

For further details see:

Anglo American Platinum: Efficient Business At A Reasonable Price, But Still Too Early