AU - AngloGold Ashanti: A Better H2 On Deck

2023-08-18 11:18:59 ET

Summary

- AngloGold Ashanti reported Q2 production of ~652,000 ounces of gold, with H1 production tracking in line with its FY2024 guide.

- Unfortunately, costs were above my estimates and are tracking above its guidance midpoint despite the back-end weighted profile, with AISC margins of just $333/oz in H1-23.

- In this update, I'll look at whether AU has dropped into a buy zone after its waterfall decline the past four weeks and recent developments.

Just over three months ago, I wrote on AngloGold Ashanti (AU), noting that while the company was benefiting from higher gold prices due to its leverage as a higher-cost producer, there was no way to justify chasing the stock above US$25.00. Since then, AngloGold has slid over 33% in a span of less than three months, massively underperforming its peer group and reverting back to a negative year-to-date return. And while a decline of this magnitude might suggest the stock is undervalued especially given its success in Nevada, we're still several years away from realizing the fruits of this Nevada success, with only small-scale production targeted for 2026. Let's take a closer look at its Q2 results and recent developments below.

Q2 Production & Sales

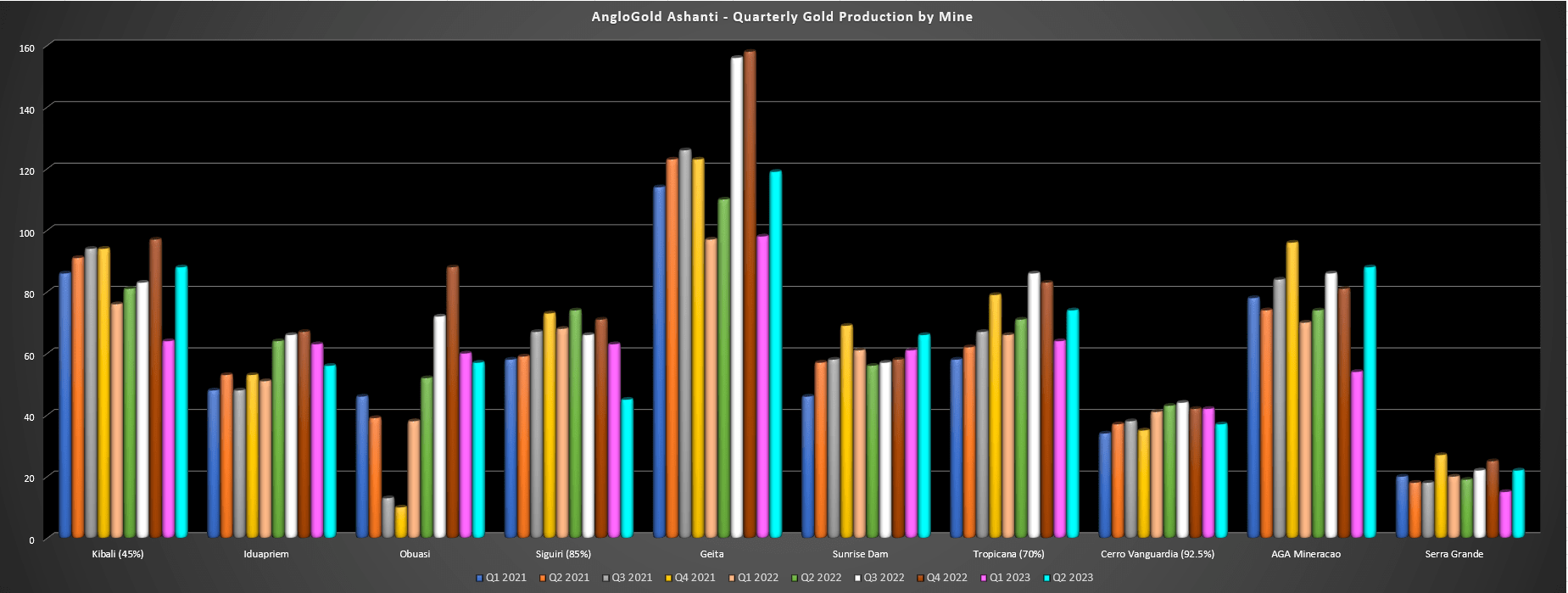

AngloGold Ashanti ("AngloGold") released its Q2 results earlier this month, reporting quarterly production of ~652,000 ounces of gold, a marginal increase from the year-ago period. This pushed H1 production to ~1.24 million ounces of gold (H1 2022: ~1.23 million ounces), with the company tracking in line with its FY2024 guide of ~2.53 million ounces given that the company expects a back-end weighted second half of the year for production. Unfortunately, there were some hiccups in the quarter, with the major one being a CIL tank failure at its Siguiri Mine in Guinea. The ~25,000-ounce impact led to a weaker than planned H1 for its African portfolio, which saw flat production year-over-year in H1 2023 despite the benefit of significantly higher production from Obuasi (higher throughput).

AngloGold Ashanti - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Looking at the quarterly performance a little closer, Kibali saw increased attributable production (~88,000 ounces), benefiting from higher throughput and grades, helped by significantly higher open-pit grades. Meanwhile, Obuasi also benefited from higher throughput, with a further lift in production expected in 2024 once the Phase 3 re-development project is complete. Finally, Geita also had a monster quarter, producing ~119,000 ounces (Q2 2022: ~110,000 ounces), which was driven by higher grades of 2.69 grams per tonne of gold, benefiting from higher open-pit grades. Unfortunately, the increase in production at these two assets was offset by lower attributable production at Siguiri (~45,000 ounces vs. ~74,000 ounces) because of the CIL tank failure (since resolved), and lower production at Iduapriem.

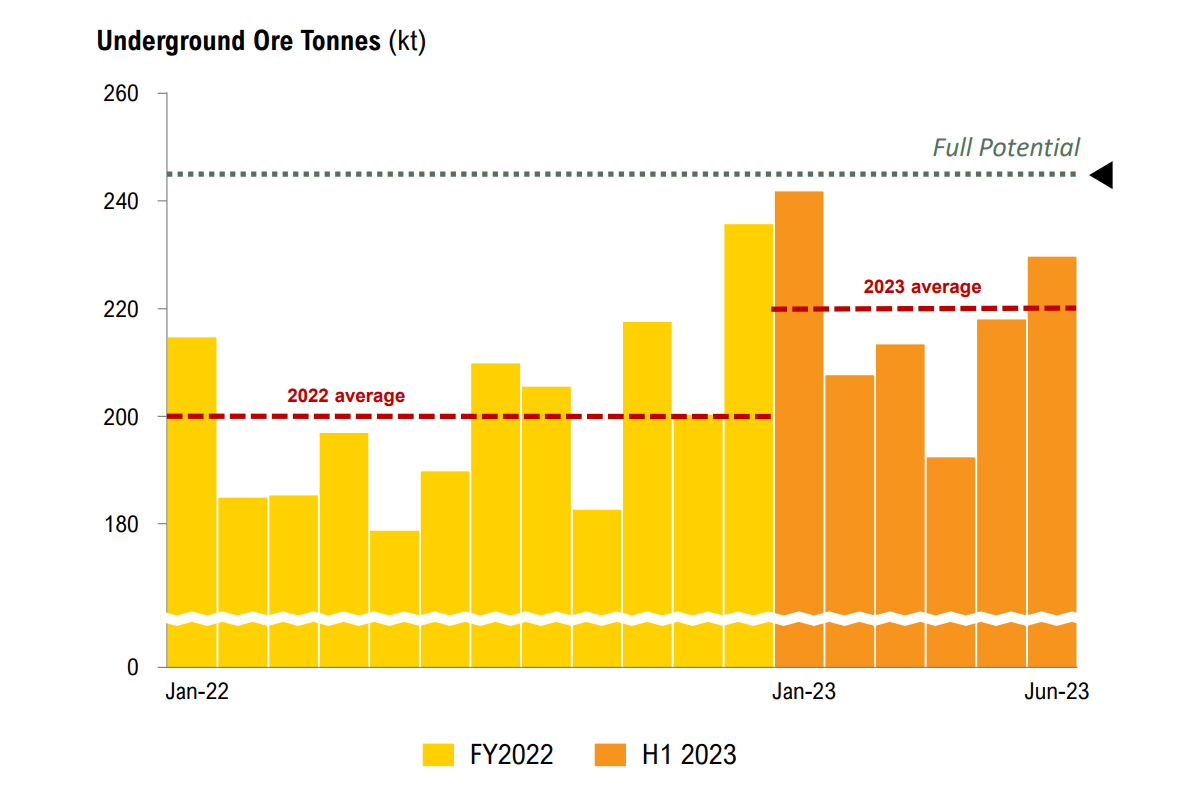

Sunrise Dam - Underground Ore Tonnes (000's) - Company Website

{kind=link}

Moving over to Australia, both Sunrise Dam and Tropicana enjoyed higher production year-over-year, increasing attributable production from its Australian assets to ~140,000 ounces in the quarter. This was driven by higher throughput at both assets and higher grades at Sunrise Dam, where grades improved to 1.58 grams per tonne of gold. Notably, both assets have continued to enjoy gains from the company's Full Asset Potential Program ["FP"], with higher underground tonnes mined at open-pit material movements also improving at Tropicana, and the plant is also tracking ahead of plans on throughput. As for Sunrise Dam, ore tonne targets have been achieved (highlighted above), recovery rates have improved, and the company is investigating the potential for a concentrate leach project. And despite inflationary pressures, Sunrise Dam expects to see cost improvements on a year-over-year basis, with improving cash costs reported in H1 2023 ($1,304/oz vs. $1,377/oz).

Tropicana Operations (Company Presentation)

{kind=link}

Unfortunately, the results weren't nearly as pleasing for the company's Latin American operations, with ~147,000 ounces produced at $1,864/oz all-in sustaining costs in Q2, representing higher costs year-over-year vs. the ~136,000 ounces produced at $1,788/oz in Q2 2022. And while the increased costs can be partially attributed to higher sustaining capital in the period ($45 million vs. $35 million), this has certainly been a drag on the company's AISC profile, with company-wide AISC of $1,559/oz in Q2 2023, up from $1,430/oz in Q2 2022. Let's look at cost performance below and how it's tracking vs. FY2023 guidance.

Costs & Margins

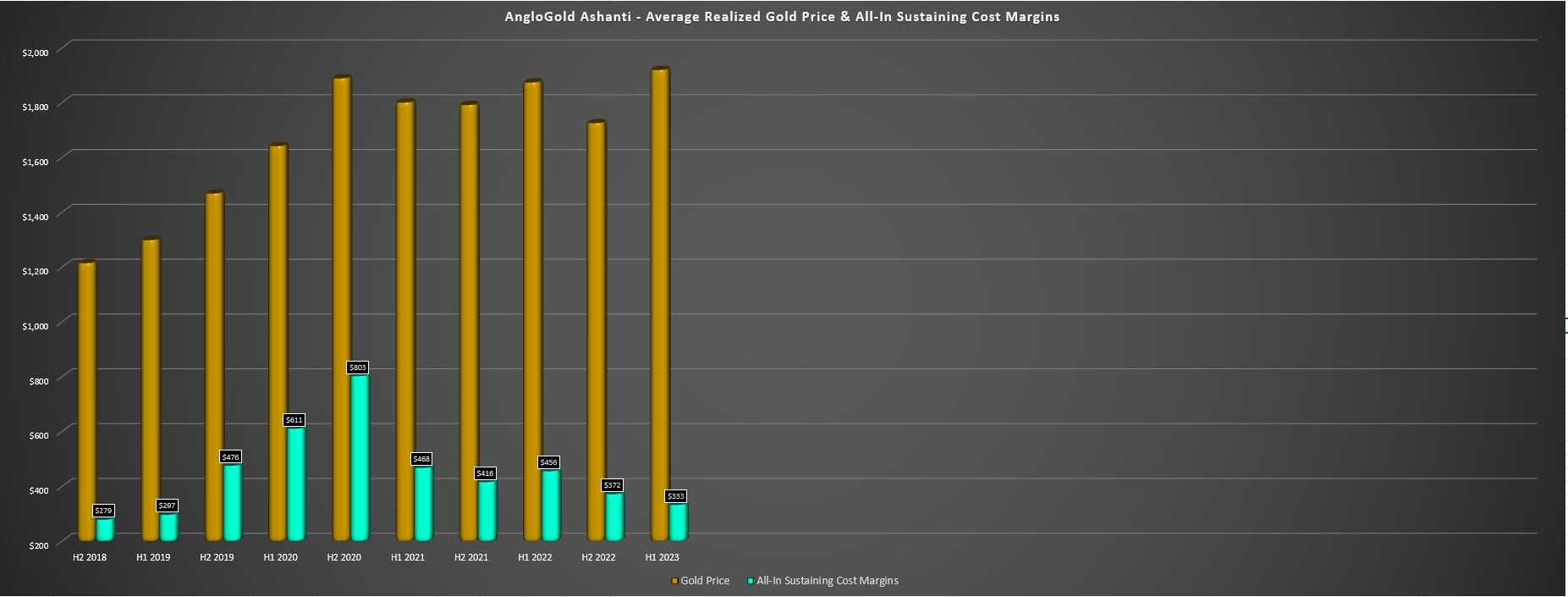

Digging into AngloGold's cost performance, all-in sustaining costs came in at $1,559/oz in Q2 and $1,587/oz in H1, significantly above the estimated industry average (~$1,360/oz) and miles above the company's FY2023 guidance midpoint of $1,428/oz. This was related to higher cash costs due to the rough quarter at Sigiuiri (CIL tank failure) inflationary pressures felt sector-wide, increased waste stripping costs at Tropicana, lower by-product credits, and higher royalties. Given this sharp increase in all-in sustaining costs, AISC margins slid to $333/oz in H1 2023, down from $456/oz last year. Unfortunately, we also saw less impressive financial results, with adjusted net debt increasing vs. year-end to ~$1.2 billion and a free cash outflow of $205 million in the period, impacted by lower cash flow from operations and a ~$25 million drag vs. last year from higher capex spend in the period ($497 million).

AngloGold - Average Realized Gold Price & AISC Margins - Company Filings, Author's Chart

{kind=link}

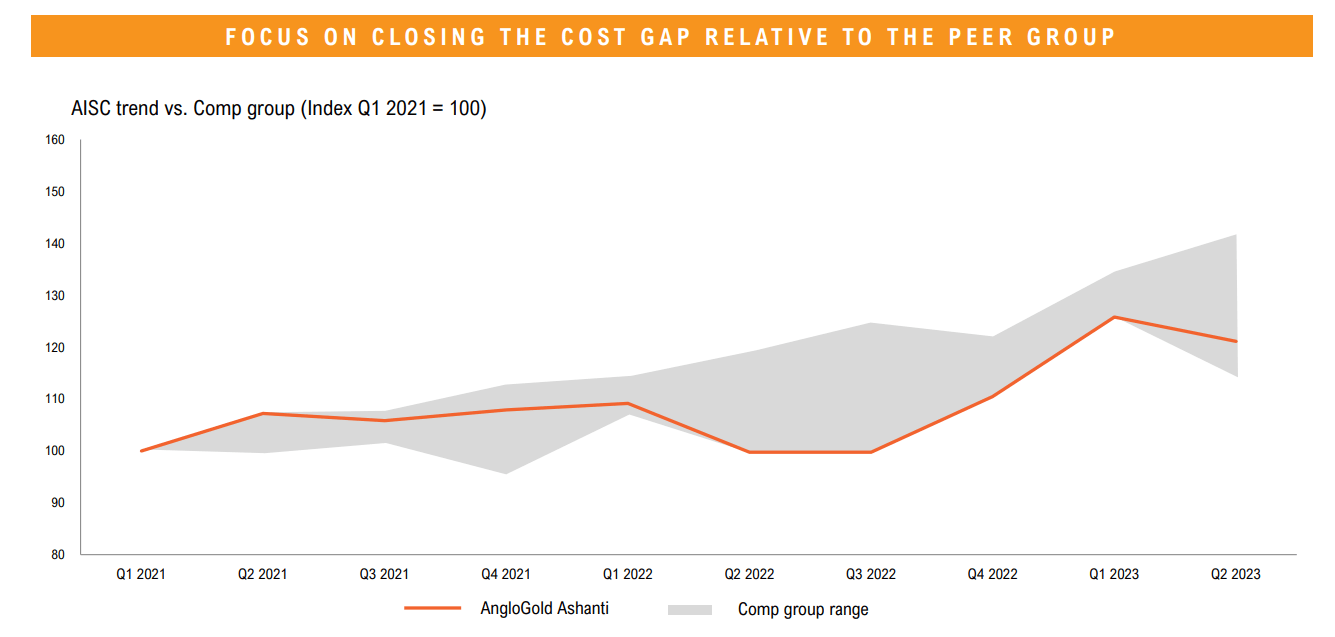

In AngloGold's H1 Presentation, the company has highlighted that while costs have clearly been trending higher due to unprecedented inflationary pressures, the company is actually beating its cost group per its chart. However, it conveniently starts this graph in Q1 2021 with AngloGold reporting a 26% increase in costs to $1,287/oz vs. $1,021/oz in the year-ago period. So, while AngloGold may be correct in its assessment that its outperformed its large peers from a cost standpoint since Q1 2021, this was hardly an accomplishment as it was starting the period with costs of $1,287/oz that had just leaped 26% year-over-year, meaning it should technically outperform the peer group. That said, aside from the favorable start date for this chart, AngloGold should see better cost performance in H2 with higher production levels, but I'm skeptical of its ability to deliver at its guidance mid-point of $1,428/oz at this point.

AngloGold Ashanti - AISC Trend vs. Comp Group vs. Q1 2021 - Company Website

{kind=link}

Recent Developments

Starting with the negatives, AngloGold reported additional impairments in its Latin American portfolio in the period, with an additional $45 million impairment loss related to the suspension of operations at the Quieroz metallurgical plant (Calcinados TSF in process of being designed and completed) and a decision not to restart operations in the dry season. In addition, the company took an additional impairment loss of $26 million on top of last year's $151 million impairment at its Corrego de Sitio Complex in Brazil. It's certainly not ideal to see these large impairments when the gold price is sitting at record levels on a three-year average basis (~$1,850/oz), but this is fortunately in an area of its business where minimal value has been assigned by the market.

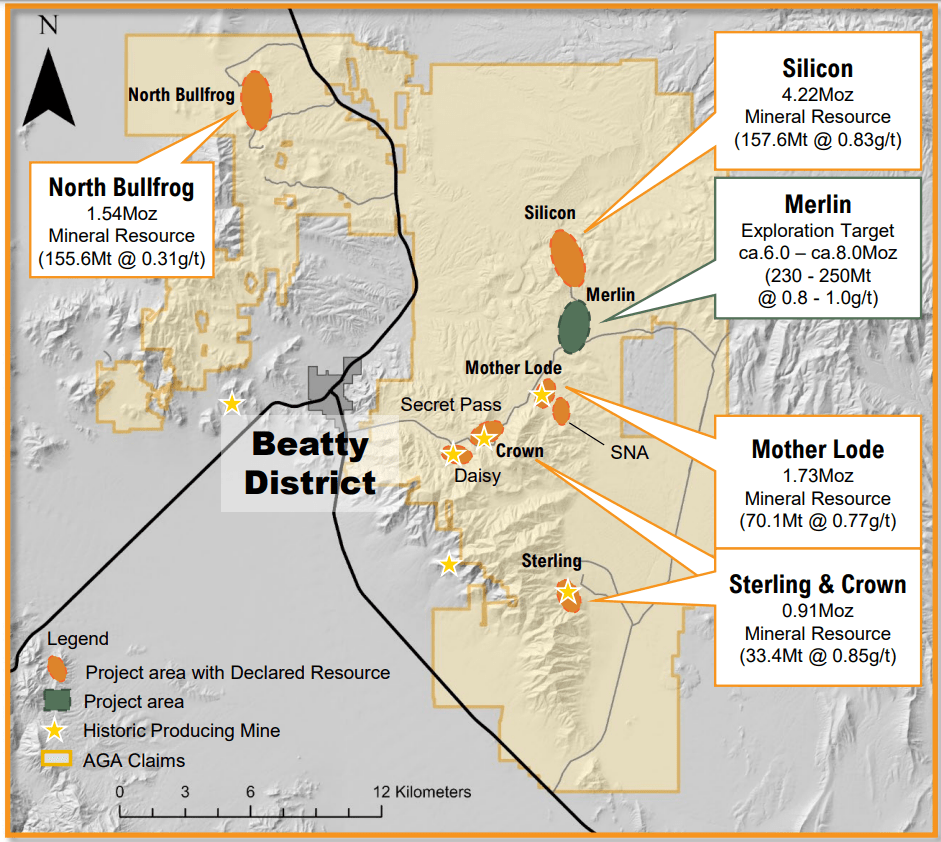

Fortunately, these continued impairments were more than offset by continued exploration success in the Beatty District of Nevada, an area that AngloGold has consolidated with its acquisition of Coeur Mining's (CDE) properties last year and the acquisition of Corvus Gold in 2021. In fact, the company has recently re-branded its Silicon Project to the Expanded Silicon Project, including Silicon to the north and Merlin to the south. And while Silicon boasted an impressive resource of ~4.2 million ounces at 0.83 grams per tonne of gold, Merlin is looking even more impressive, with an exploration target of 6.0 to 8.0 million ounces based on 230 to 250 million tonnes of material at 0.80 to 1.0 grams per tonne of gold. Notably, the potential for a 12 million ounce resource at Expanded Silicon is entirely separate from another 4.0+ million of resources elsewhere in the district (Sterling, Crown, Mother Lode, North Bullfrog).

AngloGold Claims - Beatty District - Company Presentation

{kind=link}

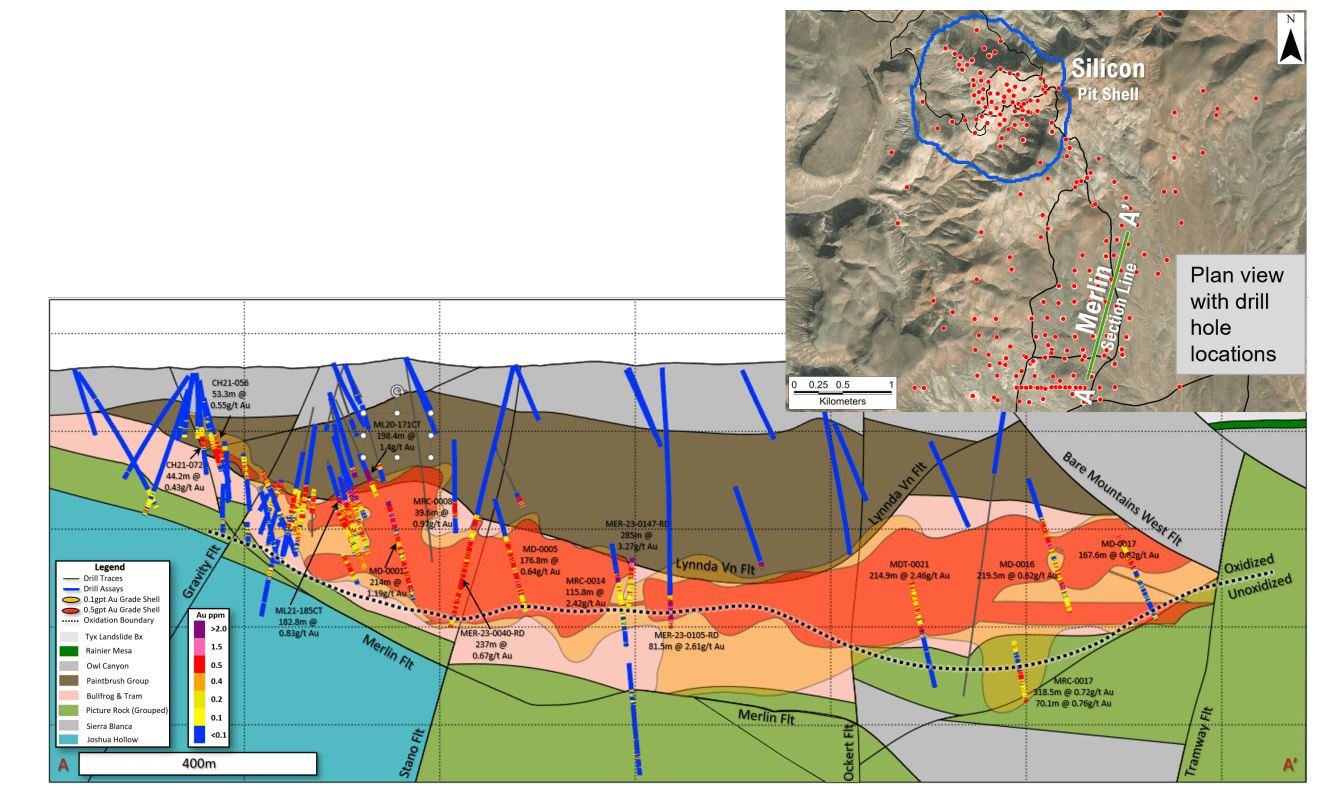

Looking closer at Merlin below, we can see the size of Merlin, which lies south of Silicon, and the impressive continuity highlighted by the 0.50 gram per tonne grade shell above the oxidation boundary. Highlight holes from Merlin are among some of the best reported sector-wide for an oxide project, with hits like 214.8 meters at 2.46 grams per tonne of gold, 285 meters at 3.27 grams per tonne of gold, and 115.8 meters at 2.42 grams per tonne of gold. AngloGold noted in its released that it plans to delay its Pre-Feasibility Study to incorporate Merlin into the new Expanded Silicon Project for a concept study, with this study expected to benefit from economies of scale and integrated infrastructure and the potential for large-scale mining. Per the most recent timeline provided, investors can expect mineral resource at Merlin and the concept study to be released by year-end.

Merlin Section & Merlin/Silicon as part of Expanded Silicon Project - Company Presentation

{kind=link}

Last, for the more advanced North Bullfrog Project, AngloGold continues to expect first production in 2026, albeit at a much smaller scale of ~100,000 ounces vs. its long-term vision for this Nevada Mining Hub. This is a positive development given that these ounces should be relatively high margin compared to its current production profile and also an upgrade from a jurisdictional standpoint. To summarize, while the continued impairments in Brazil are disappointing, this district could be a game-changer long-term for AngloGold and exactly what it needs to transform its portfolio, with the potential for a Tier-1 scale district in the #1 ranked mining jurisdiction at high margins (sub $1,050/oz costs).

However, it's important to note that we are several years away from this production profile (potential for 400,000+ ounces between North Bullfrog and Silicon/Merlin) being achieved, with a Record of Decision needed for North Bullfrog and significant study work and an eventual ROD needed at Silicon/Merlin. Hence, while this is a very positive development worth monitoring for the longer-term investment thesis, I don't expect it to change AngloGold's production or cost profile any time soon.

Valuation

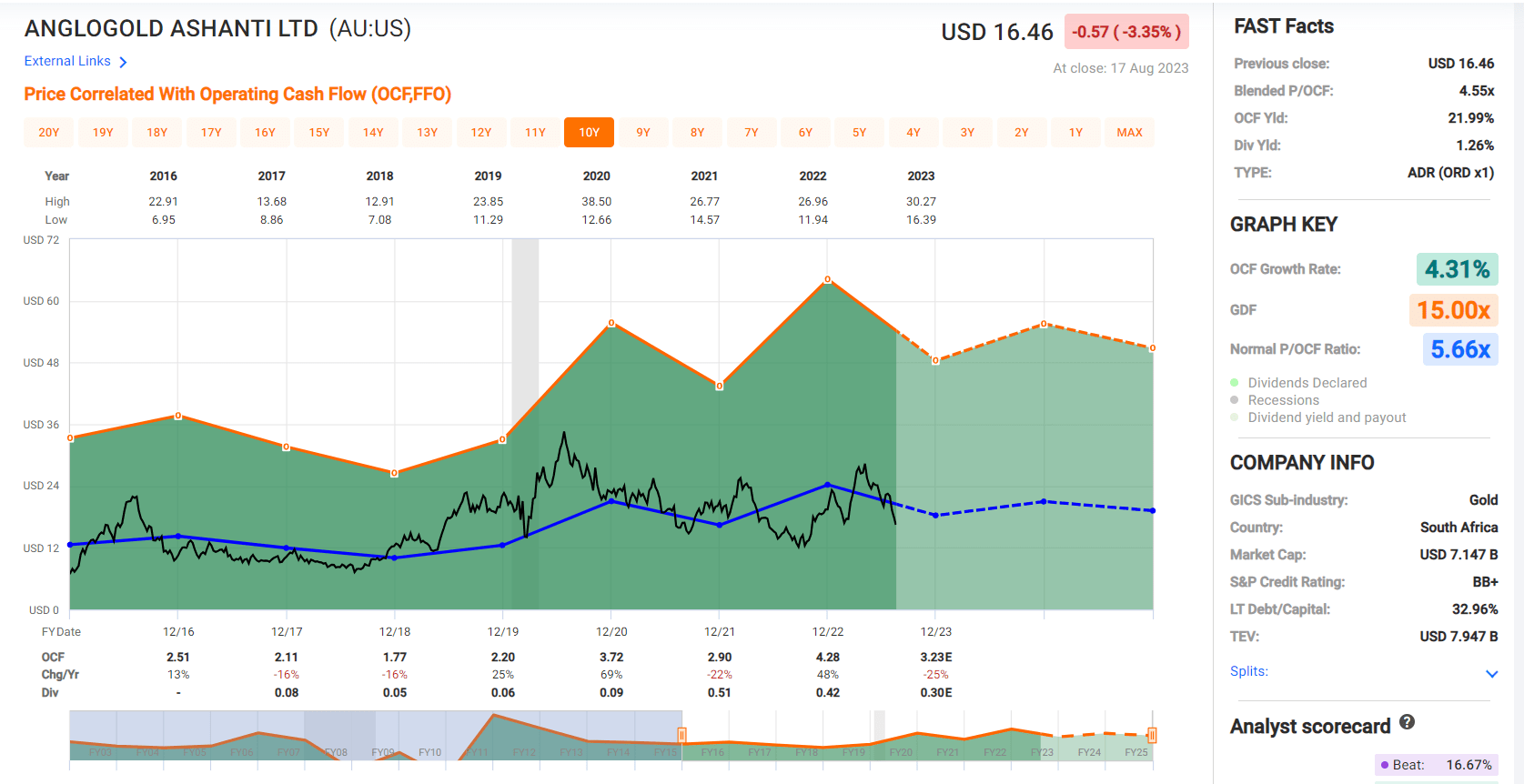

Based on ~421 million shares and a share price of US$15.50, AngloGold trades at a market cap of ~$6.53 billion and an enterprise value of ~$7.70 billion. And while this market cap is down from a peak enterprise value figure of ~$13.5 billion in May, which might suggest the stock is heavily undervalued, it's important to note that was more than fully priced in May and arguably overvalued short term. For this reason, I noted that there was no way to justify chasing the stock above US$25.00 in my May update, with it trading at ~7x forward cash flow (10-year average: ~5.6x). Looking at the current setup, AngloGold has certainly become more reasonably valued and sitting at just ~4.5x FY2024 cash flow per share estimates ($3.45), giving it one of the lowest forward cash flow multiples in its peer group.

AngloGold - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

Using what I believe to be a fair multiple of 6.3x cash flow (15% premium to its 10-year average) and more conservative FY2024 cash flow per share estimates of $3.35, this points to a fair value for AngloGold of US$21.10. And if we assign a conservative ~$1.2 billion ($2.85) in value to its future Nevada Mining Hub in the Beatty District, which is rapidly growing in size, this points a fair value for AngloGold of US$23.85. Measuring from a current share price of US$16.50, this points to a 44% upside from current levels. However, I am looking for a minimum 40% discount to fair value to justify starting new positions in high-cost producers, and AngloGold certainly fits this bill and also operates out of some less attractive jurisdictions (Tanzania, DRC). So, after applying this discount, AngloGold's low-risk buy zone to ensure a margin of safety comes in at US$14.30, suggesting it still hasn't entered a low-risk buy zone just yet.

Summary

AngloGold Ashanti had a softer Q2 than some might have hoped with a CIL tank failure at Siguiri, maintenance at its massive Geita Mine, and higher sustaining capital year-over-year that pushed all-in sustaining costs higher when combined with inflationary pressures (even if we have seen some easing sector-wide). The result of this mediocre start to the year was significant compression in AISC margins to $333/oz, and AISC margins have now fallen nearly 60% from their peak of $803/oz in H2 2020 despite the benefit of a higher average realized gold price ($1,920/oz vs. $1,895/oz). That said, the company continues to excel from a safety standpoint and it is making solid progress across its sites with its Full Potential Program. And with safety and optimization work trending in the right direction, there is a path to lower costs and higher margins for this portfolio post-2025, and a further decline in costs once it brings its Nevada Mining Hub online, which could ultimately have ~400,000-ounce per annum potential.

That said, we're still at least three years away from commercial production at North Bullfrog and while Nevada may be a top-ranked jurisdiction, permitting can be a lengthy progress, suggesting that its larger Nevada operation at Merlin/Silicon may not reach commercial production until late 2028. And with a higher cost portfolio than its peer group, elevated net debt relative to peers like Barrick Gold (GOLD), and a mediocre jurisdictional profile, I don't see any unique attributes here to justify owning AngloGold from an investment standpoint at current prices. And while this will change post-2025, when we get closer to its Nevada Mining Hub coming online, which should enjoy sub $1,000/oz AISC, the investment thesis is less compelling today. So, while the stock could certainly enjoy a bounce after a waterfall decline with four straight weeks down, I wouldn't become interested in the stock unless we see a pullback below US$14.30.

For further details see:

AngloGold Ashanti: A Better H2 On Deck