AU - AngloGold Ashanti: Leverage To Gold At A Reasonable Price

Summary

- AngloGold Ashanti released its H1 results last month, reporting production of 1.23 million ounces of gold, placing it on track to meet its annual guidance.

- While costs were up year-over-year in line with the industry average, costs for the industry may have peaked in Q2 2022, with commodity prices dropping and lower production figures.

- Unfortunately, AngloGold has been impacted by a dent in its growth profile with limited progress at Quebradona/Gramalote and has little hope of meeting its FY2025 targets.

- That said, it has been quick to pivot to assemble a land package capable of a mining complex in the Beatty District of Nevada, and significant negativity looks priced into the stock here.

Just over two months ago, I wrote on AngloGold Ashanti ( AU ), noting that while its investment thesis was less compelling, given that it was a high-cost miner with a potential downgrade to its growth profile due to a less attractive outlook for new projects in Colombia under Gustavo Petro . Since then, the stock has made new lows and is down another 10%, while names like Kinross ( KGC ) have seen a positive return in the period.

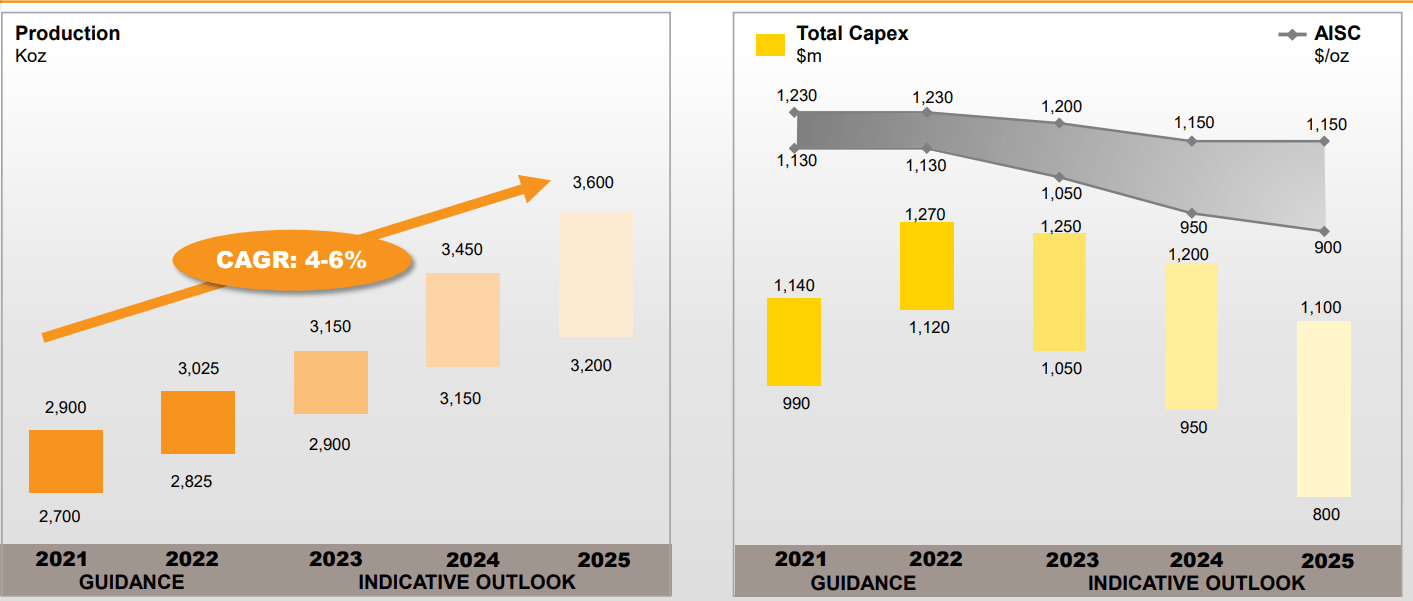

While AngloGold delivered satisfactory H1 2022 results and reaffirmed its FY2022 guidance at Obuasi, the underperformance could be related to the less exciting growth outlook than what was originally unveiled on its 2021 Capital Markets Day. In fact, even pushing production above 3.0 million ounces by FY2025 could be a difficult feat (previous outlook: ~3.4 million ounces), with two of its three planned pillars of growth (Obuasi, Quebradona, Gramalote) not advancing as expected.

AngloGold 2025 Production/Cost Targets (Capital Markets Day Presentation 2021)

{kind=link}

Fortunately, the company has quickly pivoted to lay the groundwork for future growth in a more attractive jurisdiction. Plus, while its delivery against its FY2021 targets won't come to fruition, this failure to deliver looks largely priced into the stock. In fact, the stock trades at barely 3.7x FY2023 cash flow estimates at a share price of $13.00, offering a meaningful margin of safety for investors looking to gain leverage to the gold price and willing to bet on a turnaround story.

H1 Results

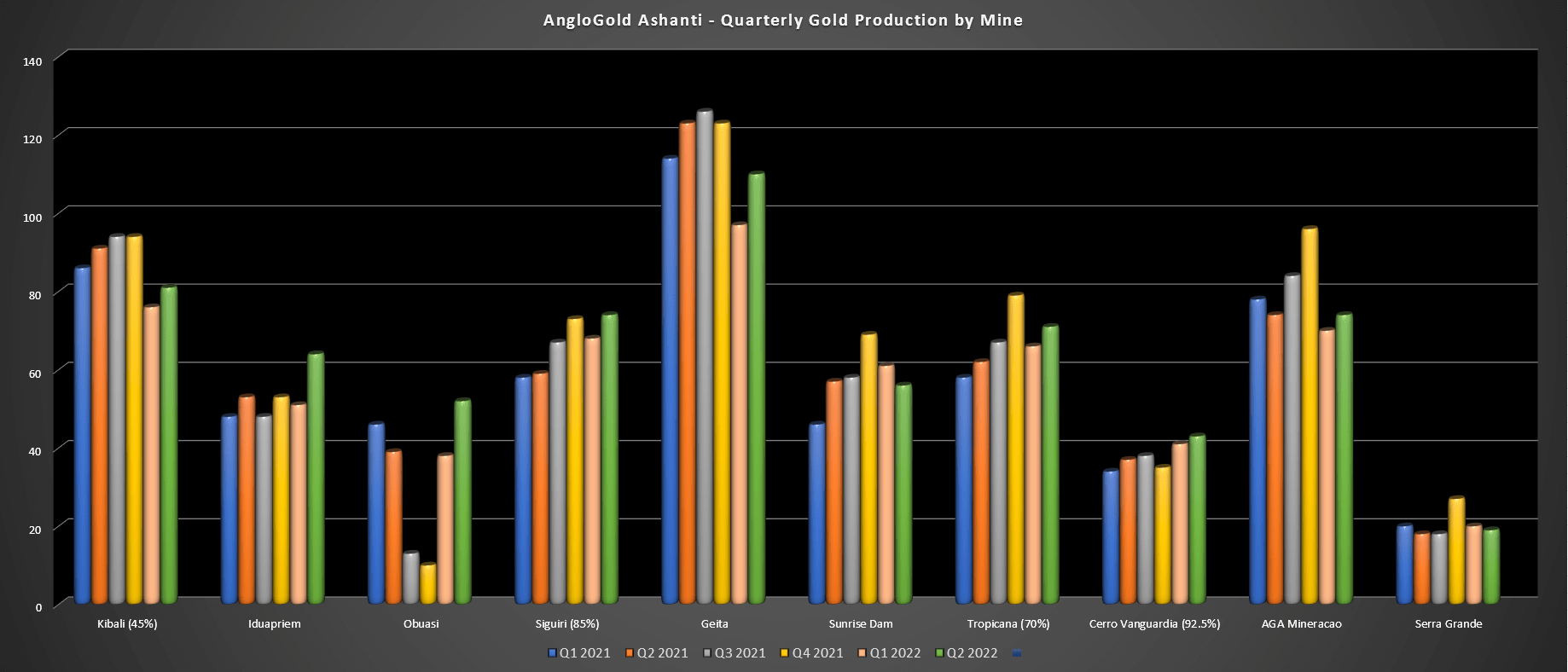

AngloGold Ashanti ("AngloGold") released its H1 results last month, reporting gold production of ~1.23 million ounces, a 3% increase from the year-ago period. The increase in production was helped by higher production in its Americas and Australian segment, offset by a slight decline in production in its African segment (712,000 ounces vs. 717,000 ounces). Unfortunately, while production was up, costs were up as well, increasing another 6% to $1,418/oz, a figure that's well above the industry average of ~$1,290/oz.

AngloGold Ashanti - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Digging into the operations a little closer, Siguiri, Iduapriem, and Obuasi saw higher production in H1 2022 vs. the year-ago period, offset by lower production at its two largest African operations: Geita and Kibali. In the Americas, the company saw lower production at AGA Mineracao due to flooding in Minas Gerais and lower tonnes processed, but Cerro Vanguardia picked up the slack, resulting in a nearly 3% increase in production in this segment. Finally, AngloGold reported strong production growth from Australia despite COVID-19-related absenteeism, which led to a ~4% impact on H1 2022 production (11,000 ounces vs. ~254,000 ounces produced).

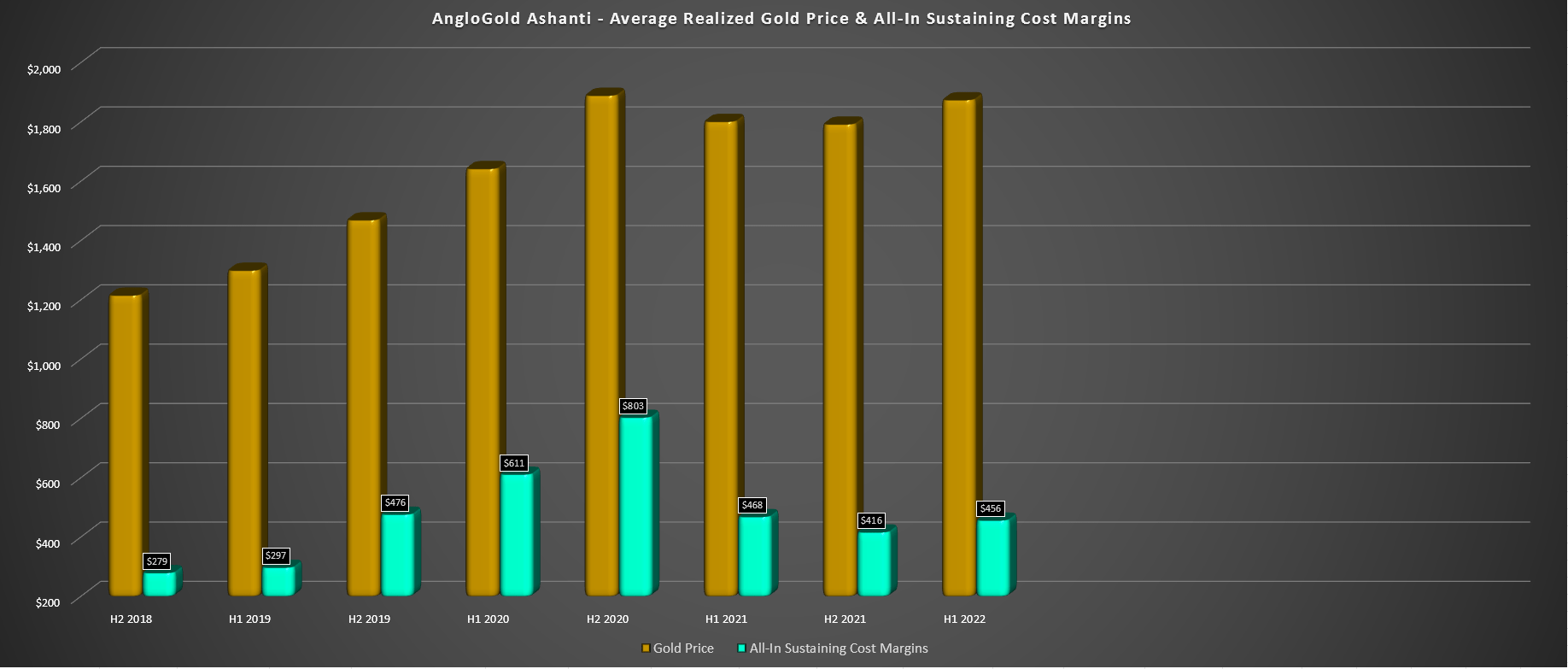

While this increase in production was a welcome development after a tough year for the company (12% production decline), costs rose, and margins sunk further in H1 2022. As the chart below shows, all-in sustaining costs rose 6% to $1,418/oz, translating to AISC margins of $456/oz, a more than 2% decline year-over-year despite the benefit of a higher gold price ($1,874/oz vs. $1,801/oz). On a two-year basis, AngloGold has seen some of the worst margin compression sector-wide, with margins plunging from $611/oz, despite lapping easy comps from a gold price standpoint (sub $1,700/oz).

AngloGold - H1 2022 Average Realized Gold Price & Margins (Company Filings, Author's Chart)

{kind=link}

AngloGold noted that its Australian operations were impacted by a higher turnover rate for operators and maintenance staff, exacerbated by the re-opening of the Australian borders, which led to an increase in COVID-19 cases. Meanwhile, the company has seen an impact from higher diesel, cyanide, and other consumables costs across its business, and labor inflation. Finally, the company shared that it expects inflationary pressures to remain in place for the remainder of the year, consistent with what we've heard from other producers.

The good news is that with AngloGold maintaining its guidance of $1,360/oz at the mid-point, we should see some improvement in costs on a sequential basis in the back half of the year (H2 2022 vs. H1 2022). That said, it will still have costs above the industry average this year. This means that AngloGold has much less breathing room than some of its larger peers if the gold price stays below $1,700/oz, with the company reporting all-in costs of $1,602/oz in H2 2022.

The silver lining is that we may have seen peak costs for the industry in Q2 2022, with prices for several commodities pulling back, and especially fuel which is a major cost for producers behind labor. The other good news is that this inflationary period is forcing many producers to tighten up operations and ensure they are more efficient. AngloGold is already working on this with its Full Asset Review Program, which is focused initially on Sunrise Dam and Siguiri.

To summarize, while the Q2 cost figures might be ugly, and this certainly isn't helped by a weaker gold price, I would be careful to assume that the costs reported in Q2 are what to expect on an annual basis in 2023/2024, given the Q2 spike. That said, there is certainly an elevated risk to owning high-cost producers like AngloGold, and I continue to overweight names like Agnico Eagle ( AEM ) that benefit from sub $1,050/oz costs and could easily survive another sharp leg down in the gold price without seeing all-in costs rise above its realized price briefly in a worst-case scenario.

Recent Developments

As of 2021, the path forward for AngloGold appeared to be Colombia, which would have led to considerable margin expansion, though not much of an improvement from a jurisdictional standpoint. Given that Quebradona continues to be held up and B2Gold ( BTG ) has pivoted to a Mali focus , given its success north of Fekola, this has put a severe dent in the previous to increase FY2025 production to ~3.4 million ounces at $1,025/oz with the help of extremely high-margin ounces from its Colombian development assets.

Colombia's Untapped Gold & Copper Potential for AngloGold (Company Presentation, Alfonso Lopez Suarez, Portafolio.Co)

{kind=link}

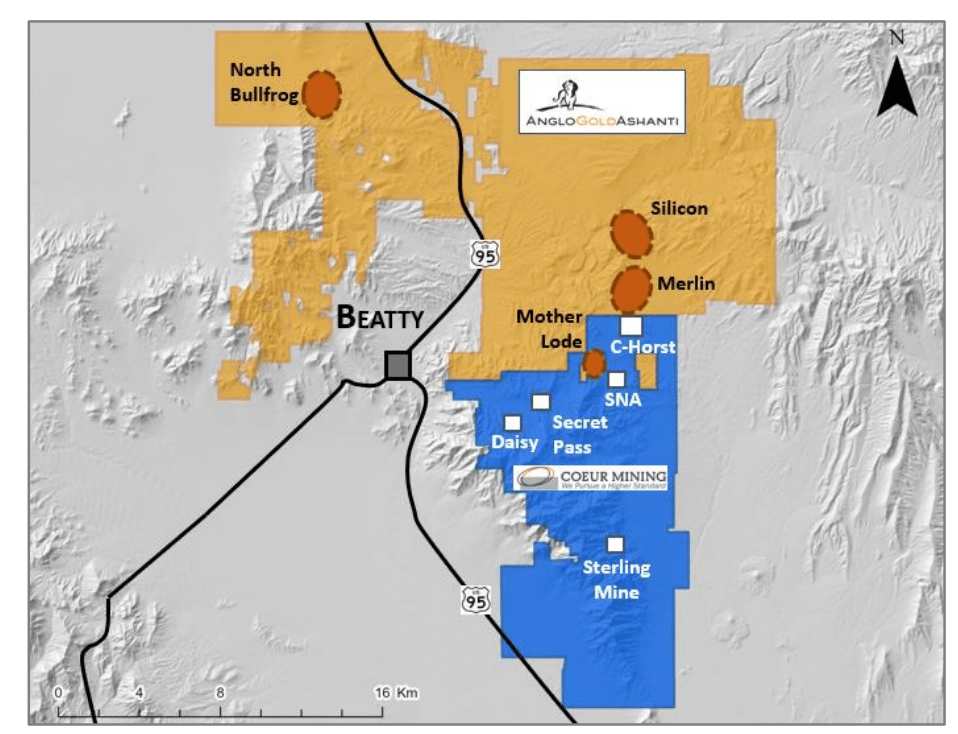

Fortunately, the company has been quick to pivot and did hedge its bets, acquiring Corvus Gold for a very reasonable price with zero share dilution, which beefed up its Nevada footprint. The company recently expanded on this with the acquisition of the C-Horst, SNA, Secret Pass, and Daisy ore bodies, in addition to the historic Sterling Mine and surrounding land. This was acquired from Coeur Mining ( CDE ) for $150 million in cash, with contingent consideration of $50 million if the project can prove up significant additional gold ounces.

{kind=link}

As shown in the above map, this has taken the borders off of its existing Nevada footprint, primarily focused on North Bullfrog, Mother Lode, Silicon, and Merlin in the Beatty District. The hope is to produce 300,000+ ounces from its Nevada portfolio later this decade at sub $1,000/oz all-in sustaining costs. However, we could see upside above this figure with the acquisition of these new properties, with C-Horst and Merlin potentially allowing Silicon to benefit from economies of scale, and potential upside for Mother Lode with new resources now sitting nearby at SNA, as well as Daisy and Secret Pass.

While a Nevada-focused footprint is undoubtedly an improvement from a jurisdictional standpoint vs. Colombia, it is a downgrade from a margin standpoint. This is because Gramalote was expected to have ~60% AISC margins at $1,750/oz gold, and Quebradona likely would have had ~65% AISC margins even at just $3.60/lb copper. Regarding mid-grade oxide gold in Nevada, the company will be lucky to have 43% AISC margins at a similar gold price ($980/oz AISC vs. $1,750/oz gold).

{kind=link}

That said, a 300,000+ ounce production profile would significantly improve the investment and still help to drag AngloGold's AISC down from current levels (~$1,350/oz). In addition, given the land package assembled here, there is certainly the potential to benefit from economies of scale and a larger complex, which should help to sustain sub $1,050/oz AISC margins past 2032, when some of the highest grade material has been mined out. Hence, following this acquisition and given its footprint in the area, I think AngloGold paid a fair price, and its 300,000-ounce projections by 2030 are likely conservative.

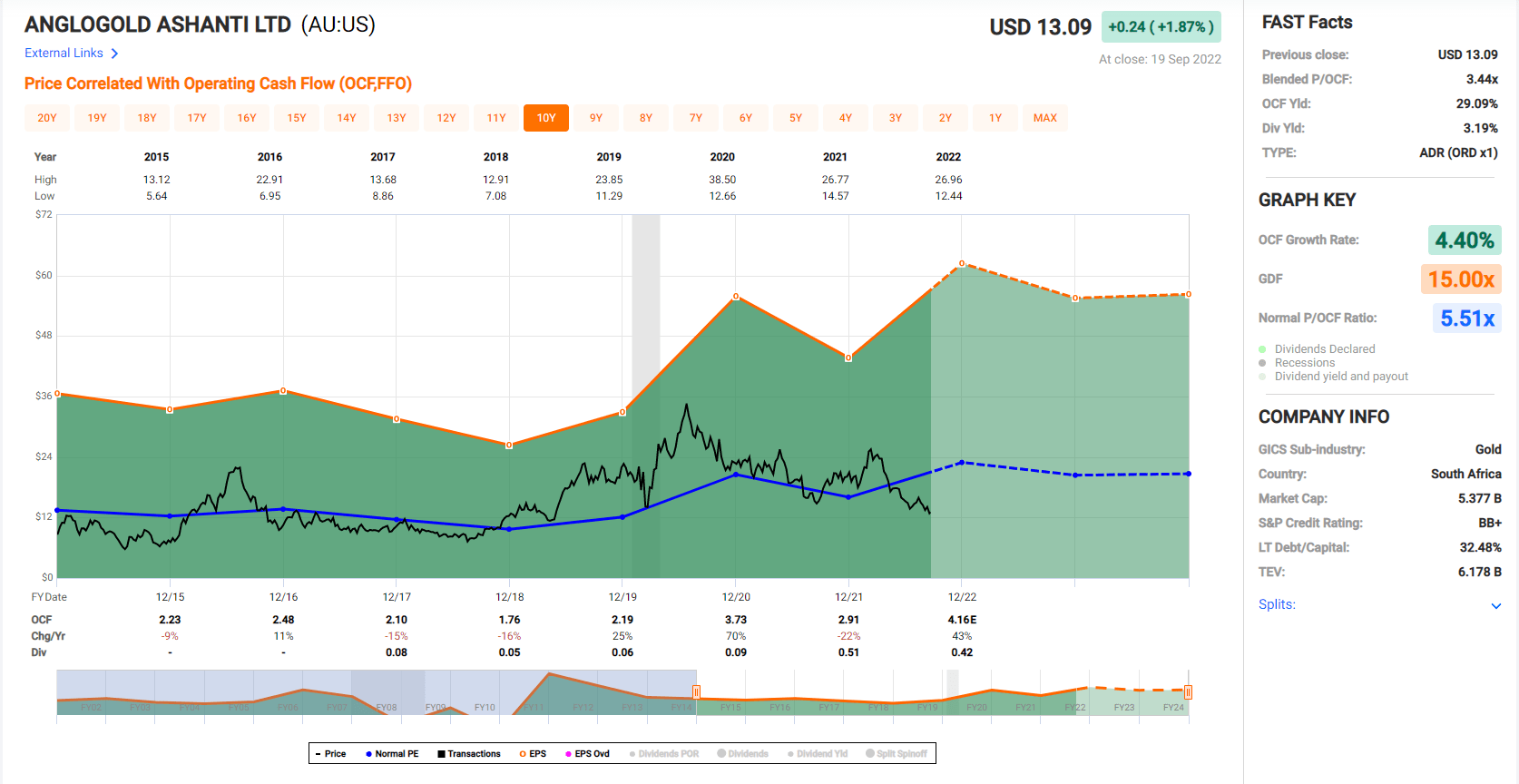

Valuation

Based on ~420 million shares and a share price of $12.70, AngloGold trades at a market cap of ~$5.33 billion, or an enterprise value of ~$6.0 billion, which is a very reasonable valuation for a 2.6 million-ounce producer. Looking at the stock's historical cash flow multiple below, we can see that AU has typically traded at ~5.5x cash flow and currently trades at just ~3.7x FY2023 estimates ($3.50). Even if we apply a more conservative multiple due to the declining gold price, and if we use what I believe to be conservative FY2023 estimates, this points to a fair value north of $17.50.

AngloGold Ashanti Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

It's important to note that this cash flow figure assigns little value to its Nevada portfolio. I would argue it is worth at least $700 million, given the land package assembled to date and current resources. This adds another $1.60 to the share price, pointing to a fair value of more than $19.00 per share. To summarize, AngloGold is clearly undervalued. That said, it will be a few years before we see the first production out of Nevada, and AngloGold will continue to be an above-average cost producer medium-term relative to peers, meaning that it is a riskier bet and likely a market performer at best, especially if the gold price remains under pressure.

Summary

AngloGold is trading at its cheapest levels since March 2020 and just came off a decent H1 report, and production at Obuasi appears to be back on track. Meanwhile, even if we have seen a downgrade to the growth profile from the lack of progress and recent developments with its Colombian assets, the company hedged its bets and has been quick to pivot, laying the foundation for growth in Nevada.

Based on what should be a 3.0+ million-ounce production profile with lower costs post-2026 and a very reasonable valuation, AngloGold has dropped into a low-risk buy zone. That said, I prefer to own what I believe to be the best companies in the sector at the lowest price possible. Even with the Nevada growth pipeline, I see AngloGold as a mediocre company with average costs, an average pipeline, and a relatively average jurisdictional profile. Therefore, I remain focused on names like Agnico Eagle , hence my Neutral/Hold rating.

For further details see:

AngloGold Ashanti: Leverage To Gold At A Reasonable Price