AU - AngloGold Ashanti: Successful Reserve Replacement In 2022

2023-06-09 15:53:00 ET

Summary

- AngloGold Ashanti successfully grew its reserves YoY in 2022, reversing a trend of reserve declines since 2020.

- The company reported a total attributable mineral resource of 131.4 million ounces of gold, also up over the year-ago period, albeit helped by a higher gold price.

- That said, while there is a path to continued reserve growth over the next few years, I still don't see nearly enough of a margin of safety in the stock here.

2022 was a tough year for the Gold Miners Index ( GDX ), and not just from a margin and cash flow standpoint, with margins down sharply across the board and cash flow also pressured because of inflationary pressures that impacted operating costs, growth capital, and sustaining capital at nearly all mine sites. This was evidenced by the year-end reserve statements from the group, with a sample of large producers I follow seeing a ~2.0% decline in total reserves on balance, and only ~29% of large producers growing reserves year-over-year. This statistic was more alarming given that the average realized gold price used to calculate reserves was a tailwind, increasing from ~$1,295/oz to ~$1,365/oz among this subset of large producers. And among the ~29% of producers that increased reserves, a couple of instances benefited from lumpy gains at one asset or acquisitions (Detour Lake, increased ownership in Yanacocha).

Fortunately, AngloGold Ashanti ( AU ) was one major miner that successfully grew its reserves year-over-year, sharply reversing a trend of reserve declines since the sale of its South African assets to Harmony Gold ( HMY ) in 2020. In addition, mineral resources also increased materially, benefiting from assets that were acquired in the top mining jurisdiction globally (Nevada), continued resource growth at Silicon, a higher gold price assumption, and the newly optimized Cleo Pit cutback at Sunrise Dam. In this update, we'll look at AngloGold Ashanti's ("AngloGold") reserve and resource base, how it stacks up relative to peers, and what the trend is likely to be going forward for this multi-million ounce producer.

{kind=link}

AngloGold Ashanti Operations (Company Website)

Mineral Resources

AngloGold Ashanti announced its year-end 2022 mineral resource update earlier this year, reporting a total attributable mineral resource of 131.4 million ounces of gold (inclusive of reserves), well ahead of Agnico Eagle's ( AEM ) total resource/reserve base of 119.2 million ounces, despite AngloGold being a smaller producer. This 7% growth in resources year-over-year for AngloGold was driven by 5.1 million ounces of additions from acquisitions (North Bullfrog, Mother Lode, Sterling), and 9.8 million ounces added from exploration, related to a newly optimized cutback at the Cleo Pit (Sunrise Dam operations), and a higher gold price. AngloGold also saw material resource growth at Geita and Siguiri related to exploration success (2.3 million and 3.2 million ounces added year-over-year, respectively), but this was partially driven by increasing its gold price used to calculate resources by ~17% from $1,500/oz to $1,750/oz.

{kind=link}

AngloGold Ashanti - Beatty District (Company Website)

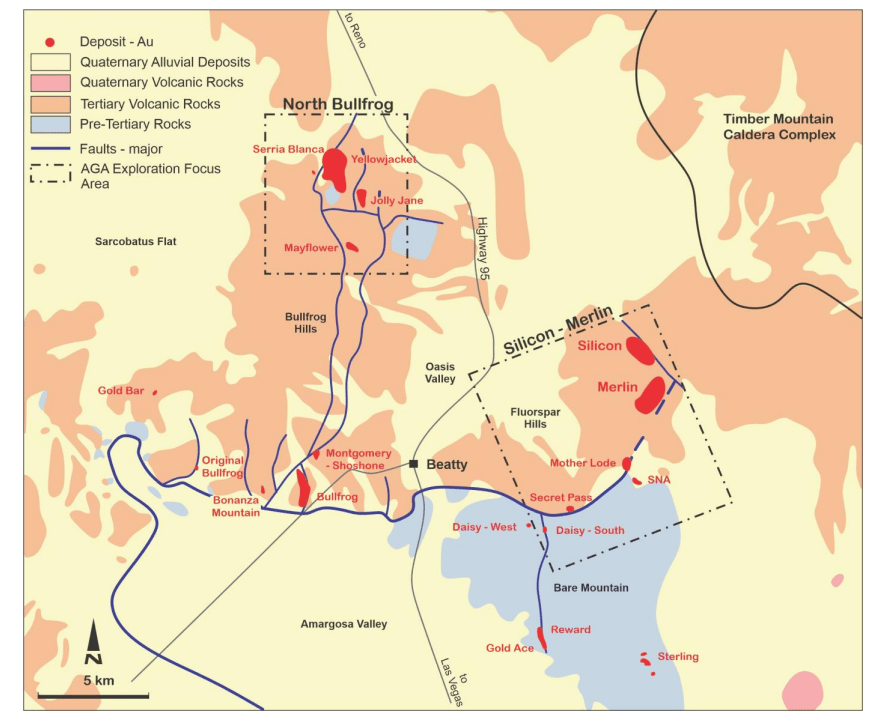

Outside of its primary jurisdictions (Africa, South America) where it holds over 85% of its total resource base, AngloGold reported significant growth in resources at Silicon in Nevada, with the mineral resource here growing from 3.37 million ounces to 4.22 million ounces, driven by a higher gold price assumption and exploration success. Combined with acquisitions made over the past two years, the company's total resource base in the Beatty District of Nevada to 8.4 million ounces. For those unfamiliar, this is the next major pillar for growth in AngloGold's portfolio and it certainly helps that it's in a Tier-1 ranked jurisdiction, which should help to improve AngloGold's jurisdictional profile post-2026. As it stands, feasibility-level work is ongoing at North Bullfrog while pre-feasibility work is underway at Silicon, with the goal appearing to be to pour first gold by 2026 at North Bullfrog, and a larger goal of a 300,000+ ounce production hub in Nevada at industry-leading costs.

{kind=link}

AngloGold Ashanti - Mineral Resources & Reserves & Resource/Reserve Grade (Company Filings, Author's Chart)

Before moving on, it's worth noting that while AngloGold's total resource/reserve base came in above that of Agnico Eagle (a larger producer), there were some key differences. For starters, AngloGold's gold price used to calculate mineral resources is much higher at $1,750/oz vs. Agnico at $1,500/oz to $1,688/oz, and Agnico's resource base is in much more attractive jurisdictions. In fact, while AngloGold has just 14% of its total resources (inclusive of reserves) in Tier-1 ranked jurisdictions (Nevada, Australia), ~95% of Agnico Eagle's reserve/resource base is based out of Tier-1 ranked jurisdictions (Ontario, Nunavut, Quebec, Europe, Australia). Finally, Agnico's optionality projects are primarily sidelined (Hammond Reef) because of having better opportunities in the pipeline that take priority, whereas two contributors to AngloGold's resources (Quebradona, Gramalote 50%) have struggled to make much progress, and the path is less clear, at least under the current political leadership in Colombia .

Mineral Reserves

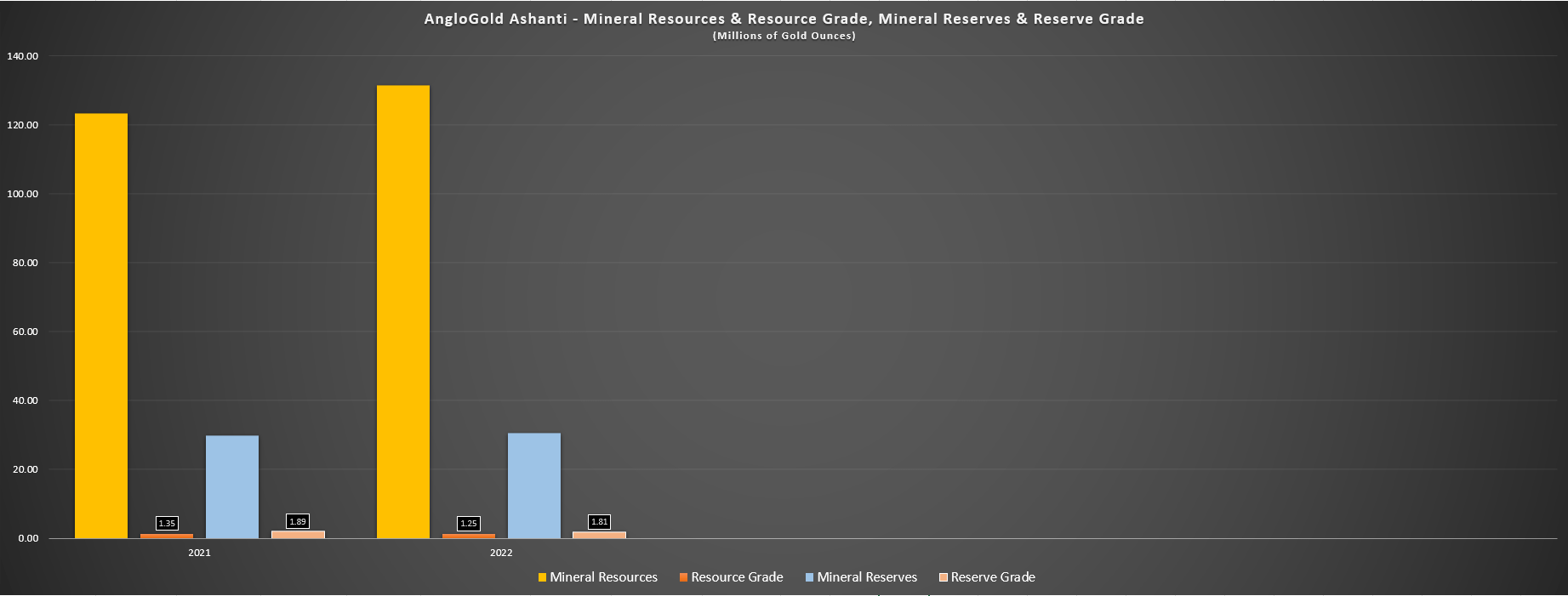

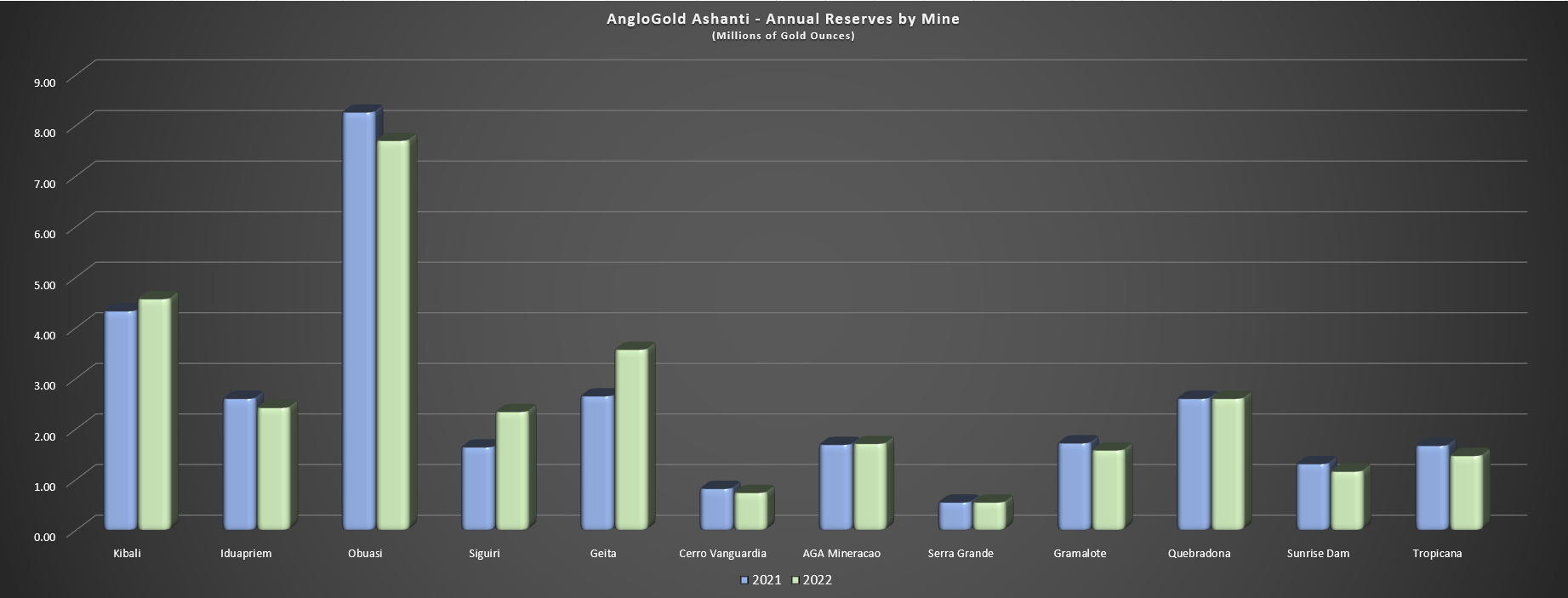

Moving over to mineral reserves, AngloGold reported growth in mineral reserves as well, with ~30.4 million ounces of gold reserves at an average grade of 1.81 grams per tonne of gold. And while we saw a decline in grade (2021: 1.89 grams per tonne of gold), AngloGold's reserves increased 2% year-over-year despite significant depletion in the period. As the chart below shows, the growth in reserves stemmed from larger assets like Kibali (45% ownership), Siguiri, and Geita, with its African portfolio certainly pulling its weight from a reserve growth standpoint. This was offset by minor declines in reserves at Iduapriem and Obuasi, with Obuasi's reserve decline related to the higher mining costs and sustaining capital, resulting in an 8% decrease in reserves year-over-year. That said, Obuasi still has a massive high-grade reserve base (7.70 million ounces at 9.31 grams per tonne of gold) for this Ghanian mine that's been in operation for over 120 years.

{kind=link}

AngloGold Ashanti - Annual Reserves by Mine (Company Filings, Author's Chart)

Looking at the meaningful contributors to reserve growth, Kibali (Democratic Republic of the Congo) benefited from the conversion of the 11000 lode in KCD Underground plus growth in the Ikamva and Oere pits due to exploration success combined with a higher gold price used to calculate reserves. Meanwhile, at Siguiri in Guinea, reserves increased primarily to the initial reporting of reserves at Sorofe, Sanutinti, and Kalamagna, as well as a higher gold price. Finally, at AngloGold's Geita Mine in Tanzania, exploration success led to an increased pit size at Nyamullima, plus it reported maiden reserves at Geita Hill Underground. Additionally, a higher gold price ($1,500/oz vs. $1,300/oz) benefited reserve growth plus reduced costs. Overall, these three assets combined for 3.1 million ounces of reserve growth, more than offsetting the 0.3 million ounce decline in reserves at its Obuasi Mine which is working to ramp up to ~350,000 ounces per annum later this decade.

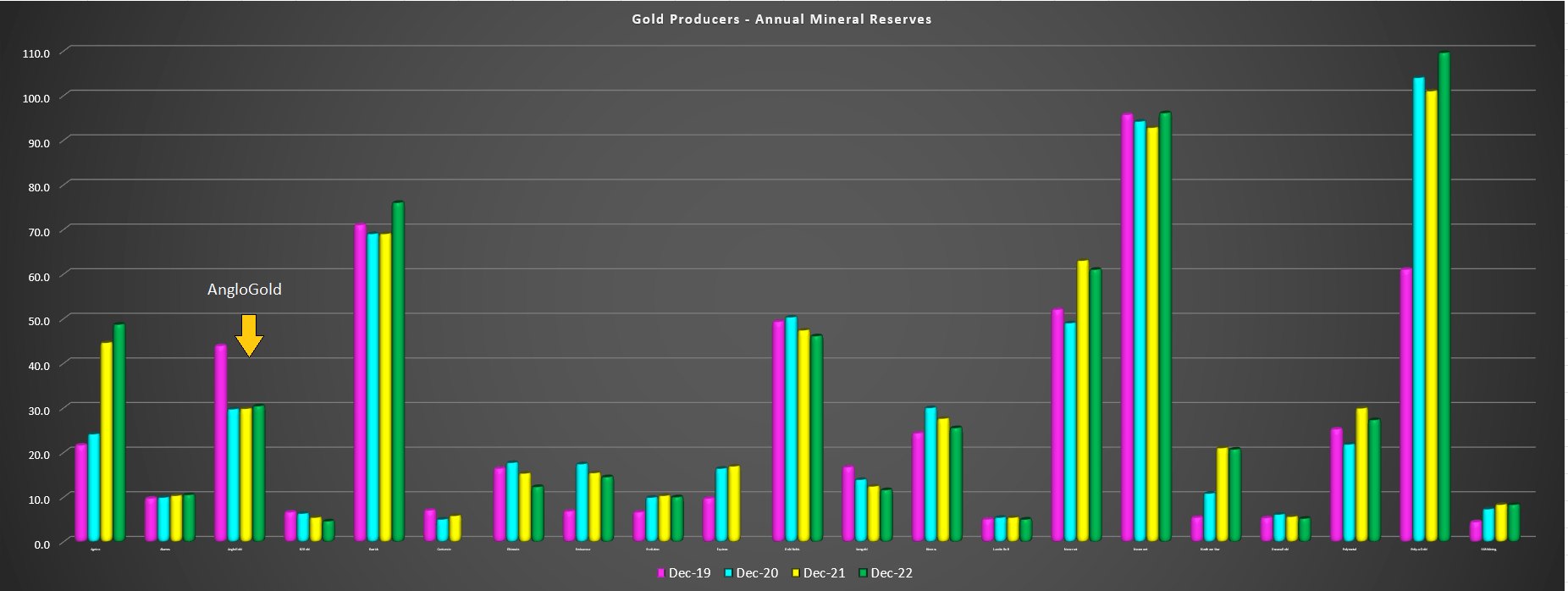

While this reserve growth was positive and certainly places AngloGold among the minority vs. other large producers with very few growing reserves year-over-year (shown below), it is worth noting that AngloGold is much more concentrated in Tier-2 and Tier-3 jurisdictions than its peers, with ~91% of reserves being located in non-Tier-1 jurisdictions, which pales in comparison to other million-ounce producers. In fact, the only producers with less favorable jurisdiction profiles for their reserve bases were Harmony Gold, Endeavour Mining ( OTCQX:EDVMF ), and B2Gold ( BTG ), but two of these peers worked to correct this with the recent acquisition of Sabina Gold in Nunavut (B2Gold), and the acquisition of the Eva Project by Harmony in Australia.

{kind=link}

Large Gold Producers - Annual Mineral Reserves (Company Filings, Author's Chart)

The good news is that while AngloGold may have only seen a minor step up in reserves at year-end 2022 which was undoubtedly helped by the change in its gold price used to calculate reserves, the company should see reserve growth continue as its Nevada portfolio starts seeing successful conversion of resources to reserves. In fact, even if we assume only a 55% conversion rate and ultimately a 10.0 million ounce resource base in the Beatty District, AngloGold would see reserve growth of 5.5+ million ounces this decade, translating to nearly 20% reserve growth from the top ranked mining jurisdiction globally. Hence, while its jurisdictional profile leaves much to be desired currently, it is set to swing the other way in coming years, as is its margin profile, with the company set to see improved costs with a larger production profile at Obuasi, synergies if the Ghana JV goes through, and lower cost ounces in Nevada.

Summary

AngloGold Ashanti's reserve growth in 2022 was certainly positive and the company is making all the right moves to position itself as a more attractive producer, including work to optimize existing assets (Full Asset Potential Program), work to improve its jurisdictional profile (consolidating a major land package in an area ripe for new discoveries in Nevada - the Walker Lane Trend), and working on a joint-venture to improve its Iduapriem Mine's future. If successful on all three fronts which should translate to a higher production profile at lower costs, making the company more attractive to investors that might have preferred names like Endeavour Mining or B2Gold for their higher margins and increased shareholder returns.

{kind=link}

AngloGold Ashanti Operations (Company Presentation)

That said, and as discussed in my previous update , I still don't see enough of a margin of safety to justify going long AngloGold, with the stock trading at ~6.5x FY2023 cash flow per share estimates ($3.80) vs. a historical cash flow multiple of 5.7. And even if we use a higher multiple of 6.6 (15% premium to previous multiple) to reflect its improving jurisdictional profile and path to more competitive costs relative to peers, this still translates to a fair value of just US$25.10, pointing to minimal upside from current levels. So, while a rising gold price will lift all boats, I continue to see far more attractive bets elsewhere in the sector from a reward/risk standpoint. To summarize, I continue to focus elsewhere, and if AU were to rally above US$26.50 before August, I would view this as an opportunity to book some profits.

For further details see:

AngloGold Ashanti: Successful Reserve Replacement In 2022